Short-Term Energy Outlook

Release Date: February 12, 2013 | Next Release Date: March 12, 2013 | Full Report | Text Only | All Tables | All Figures

Global Crude Oil and Liquid Fuels

Global Crude Oil and Liquid Fuels Overview

Market fundamentals and expectations strengthened in January 2013 because of earlier-than-expected cutbacks in Saudi Arabian oil production and greater optimism about economic growth, particularly in China, which have supported higher oil prices. EIA expects oil markets to tighten in the first quarter of 2013, but increasing global supply more than offsets higher global consumption through the rest of the forecast period. Projected world supply increases by 1.1 million bbl/d in 2013 and 2.0 million bbl/d in 2014, with most of the growth coming from outside the Organization of the Petroleum Exporting Countries (OPEC). North America will account for much of this growth. Projected world liquid fuels consumption grows by an annual average of 1.0 million bbl/d in 2013 and 1.4 million bbl/d in 2014. Countries outside the Organization for Economic Cooperation and Development (OECD) drive expected consumption growth.

Global Crude Oil and Liquid Fuels Consumption

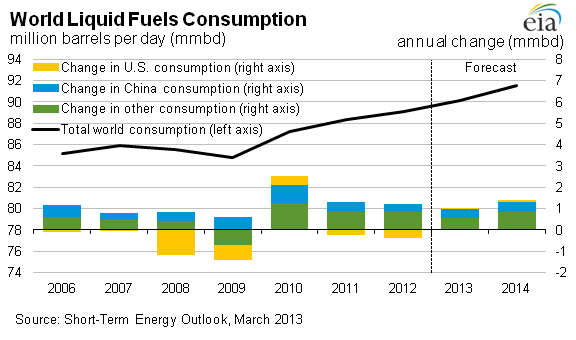

World liquid fuels consumption grew by 0.9 million bbl/d in 2012 to reach 89.2 million bbl/d. EIA expects that this growth will pick up in 2013 and accelerate in 2014 because of a moderate recovery in global economic growth; consumption reaches 90.2 million bbl/d in 2013 and 91.6 million bbl/d in 2014. Non-OECD Asia is the leading regional contributor to expected global consumption growth.

OECD liquid fuels consumption declined by 0.4 million bbl/d in 2012. EIA projects OECD consumption to further decline by 0.3 million bbl/d in 2013 because of declining consumption in Europe. OECD consumption flattens in 2014 as European consumption begins to flatten in response to higher economic growth.

China's economy has improved since the third quarter of 2012. as key manufacturing indexes and refinery crude oil inputs have increased. Infrastructure investment and consumer spending indicate signs of strong economic growth in China, although not at the high rates seen in recent years. EIA also expects refinery crude oil inputs to be bolstered in 2013 as oil product inventories are restocked and new refining capacity comes on line. EIA estimates that liquid fuels consumption in China increased by 380,000 bbl/d in 2012, and will increase by 450,000 bbl/d in 2013 and by 470,000 bbl/d in 2014.

Non-OPEC Supply

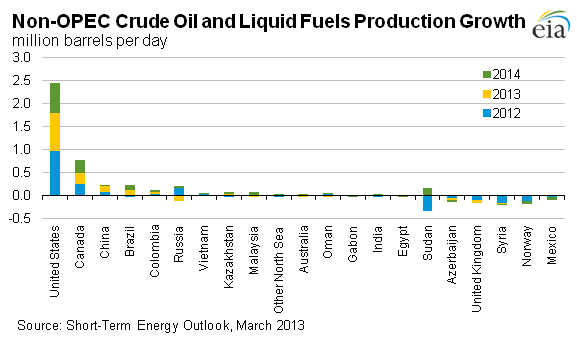

EIA projects non-OPEC liquids production will increase by 1.2 million bbl/d in 2013 and by another 1.4 million bbl/d in 2014. North America accounts for about two-thirds of the projected growth in non-OPEC supply over the next two years because of continued production growth from U.S. tight oil formations and Canadian oil sands. EIA has slightly lowered its forecast for the growth in Canadian oil production in 2013, due in part to further delays in initial production from the Kearl oil sands mining project.

Unplanned production outages in non-OPEC countries persisted at an average level of 0.8 million bbl/d in January 2013. Syria, Sudan, and South Sudan are currently the most significant sources of disruption to non-OPEC production. EIA does not assume a resolution in Syria will occur during the forecast period.

EIA has pushed back the anticipated restart of South Sudan's production due to the persistent uncertainty surrounding border demilitarization. The African Union has set a new and third deadline for Sudan and South Sudan to resolve outstanding issues and avoid sanctions, although the organization has yet to impose any of the sanctions that it has threatened in the past. The countries have three months from January 25, 2013, to resolve pending issues, which include demilitarizing the contested border. EIA now expects production at the Upper Nile fields to resume in the third quarter of this year, with output restarting at mature fields in the following months. On the upside, two new oil fields recently boosted Sudan's oil production: al-Barsaya (6,000 bbl/d) and Hadida (10,000 bbl/d). EIA expects both fields to double output this year. Combined production of both countries is projected to average 150,000 bbl/d in 2013 and 410,000 bbl/d in 2014.

In Australia, Cyclones Narelle and Peta shut in some production from fields near the northwest coast in January 2013. In Colombia, despite continued attacks by leftist rebels on the nation's energy infrastructure, notably the Caño Limón oil pipeline, initial press reports claimed that the country's oil production passed the 1-million-bbl/d mark in January. An additional threat to South American production is the potential for a strike in February by workers of Petrobras, the Brazilian state-owned oil company.

OPEC Supply

OPEC member countries, particularly Saudi Arabia, cut production heavily in fourth-quarter 2012, which contributed to an increase in crude oil prices at the start of 2013. Projected OPEC crude oil supply decreases by 0.3 million bbl/d in 2013 from the year before and then rises by 0.3 million bbl/d in 2014. Most of the decline in 2013 comes from Saudi Arabia, which responds to non-OPEC growth and increasing production from some OPEC members, such as Iraq, Nigeria, and Angola. In Angola, output at the BP-operated PSVM (Plutão, Saturno, Vénus, and Marte) development recently came on line. Production at PSVM is expected to build this year and peak at 150,000 bbl/d in 2014.

New threats to energy infrastructure in the Middle East and North Africa emerged in January 2013 as a militant group stormed the Ain Amenas natural gas facility in east Algeria causing a four-day standoff that resulted in both facility worker and militant casualties. Militants later attacked a natural gas pipeline. In response, Algeria and international energy firms operating in the country have increased security at oil and gas facilities, and nearby countries such as Tunisia and Libya have followed suit. EIA's oil supply outlook for Algeria remains unchanged, as there has been no indication that recent events have affected current oil operations or deterred future investments.

Libya's energy sector continues to be plagued by a series of small disruptions. Protesters have expressed economic and political grievances by disrupting operations at several key facilities over the last month, including the Ras Lanuf refinery and the Zueitina export terminal, which was responsible for an average of approximately 130,000 bbl/d of Libya's crude oil exports in December 2012. EIA estimates that Libya's crude oil output fell to an average of 1.3 million bbl/d in January 2013, which would be the lowest monthly average since February 2012.

EIA estimates that OPEC surplus capacity, which is overwhelmingly concentrated in Saudi Arabia, was around 2.7 million bbl/d in January 2013, an increase from previous months. Projected OPEC surplus capacity averages 2.9 million bbl/d in 2013 and 3.4 million bbl/d in 2014. These estimates do not include additional capacity that may be available in Iran but which is currently off line because of the effects of U.S. and EU sanctions on Iran's ability to sell its oil.

OECD Petroleum Inventories

EIA estimates that OECD commercial oil inventories at the end of 2012 totaled 2.66 billion barrels, equivalent to 57.2 days of supply. Projected OECD oil inventories fall slightly and end 2013 at 2.63 billion barrels (56.4 days of supply). Inventories increase slightly to 2.69 billion barrels (57.8 days of supply) by the end of 2014.

Global Crude Oil Prices

EIA projects the Brent crude oil spot price will fall from an average of $112 per barrel in 2012 to annual averages of $109 per barrel and $101 per barrel in 2013 and 2014, respectively, reflecting the increasing supply of liquid fuels from non-OPEC countries. After averaging $94 per barrel in 2012, the projected WTI price averages $93 per barrel in 2013 and $92 per barrel in 2014. By 2014, several pipeline projects from the midcontinent to the Gulf Coast refining centers are expected to come on line, reducing the cost of transporting crude oil to refiners, which is reflected in a drop in the price discount of WTI to Brent from an average $18 per barrel in 2012 to $9 per barrel in 2014.

Energy price forecasts are highly uncertain (Market Prices and Uncertainty Report). WTI futures for May 2013 delivery during the five-day period ending February 7, 2013, averaged $97.55 per barrel. Implied volatility averaged 21 percent, establishing the lower and upper limits of the 95-percent confidence interval for the market's expectations of monthly average WTI prices in May 2013 at $82 per barrel and $117 per barrel, respectively. Last year at this time, WTI for May 2012 delivery averaged $99 per barrel and implied volatility averaged 31 percent. The corresponding lower and upper limits of the 95-percent confidence interval were $75 per barrel and $130 per barrel.

| International Crude Oil and Liquid Fuels Summary | ||||

|---|---|---|---|---|

| 2011 | 2012 | 2013 projected | 2014 projected | |

|

a Weighted by oil consumption. b Foreign currency per U.S. dollar. |

||||

| Supply & Consumption | (million barrels per day) | |||

| Non-OPEC Production | 51.91 | 52.48 | 53.66 | 55.09 |

| OPEC Production | 35.17 | 36.48 | 36.37 | 36.94 |

| OPEC Crude Oil Portion | 29.82 | 30.93 | 30.58 | 30.86 |

| Total World Production | 87.08 | 88.97 | 90.04 | 92.03 |

| OECD Commercial Inventory (end-of-year) | 2606 | 2664 | 2634 | 2688 |

| Total OPEC surplus crude oil production capacity | 3.01 | 2.09 | 2.85 | 3.38 |

| OECD Consumption | 46.45 | 46.01 | 45.75 | 45.69 |

| Non-OECD Consumption | 41.85 | 43.15 | 44.46 | 45.93 |

| Total World Consumption | 88.29 | 89.16 | 90.21 | 91.62 |

| Primary Assumptions | (percent change from prior year) | |||

| World Real Gross Domestic Producta | 2.9 | 2.8 | 2.4 | 3.3 |

| Real U.S. Dollar Exchange Rateb | -2.6 | 3.7 | 2.1 | 1.6 |

Interactive Data Viewers

Provides custom data views of historical and forecast data

STEO Custom Table Builder ›

Real Prices Viewer ›

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Related Articles | ||

|---|---|---|

| Today In Energy | Daily | |

| Key drivers for EIA's short-term U.S. crude oil production outlook | Feb-2013 | |

| Brent Crude Oil Spot Price Forecast | Jul-2012 | |

| Probabilities of Possible Future Prices | Apr-2010 | |

| Energy Price Volatility and Forecast Uncertainty | Oct-2009 |