Electric Power Annual

Overview

The volume of electric power generation and sales to customers rose slightly by 0.2 percent each, from 2005 to 2006. Milder summer and winter temperatures in 2006 than in 2005 dampened overall demand for electric power for heating and air conditioning. With the exception of July, more moderate average temperatures prevailed in large parts of the Nation during the summer months. Summer peak demand (noncoincident) grew to 789,475 megawatts (MW), 4.0 percent higher than the peak in 2005, and 12.1 percent higher than in 2004. Net generation of electric power during June, July and August 2006 increased by 0.9 percent from the previous summer. Winter peak demand (noncoincident), which is always smaller than summer peak demand, was 640,981 MW, growing 2.3 percent, nearly twice the rate of change from the prior year rate and surpassing the rate of growth in winter peak demand over the past several years. Net generation during the winter months (January, February and December 2006) was 1.8 percent lower than the previous year’s winter months. Continuing economic growth in the Nation is reflected in the 0.7 percent growth in retail electricity sales to the commercial and industrial sectors, while the milder weather is reflected in the decline of 0.6 percent in retail electricity sales to the residential sector.

Total net summer capacity increased 0.8 percent, a net increase of 8,195 MW, almost all in the form of natural gas-fired combined-cycle units. Actual available capacity (lower than net summer capacity due to constraints from planned and forced outages and deratings) was 906,155 MW in 2006 for the electric power industry within the contiguous United States. The electrical system net internal demand[1] was 760,108 MW for the contiguous United States. The associated capacity margin rose to 16.1 percent in 2006, a slight increase over the 15.4 percent margin in 2005. Notably, the Florida Reliability Coordinating Council doubled its capacity margin, achieving a level of 17.6 percent in 2006. Retail prices for electricity increased by 9.3 percent to an average of 8.9 cents per kilowatthour. Prices increased in all regions of the country, but most of the larger increases occurred in the East. States with restructuring programs such as Maryland and Delaware had portions of their retail electricity price caps lifted in 2006, contributing to significant price hikes. Additional factors that contributed to higher retail prices include termination of long term wholesale power contracts at some utilities and rate increases that became effective due to higher delivered fuel costs over the past few years.

In 2006, carbon dioxide, sulfur dioxide and nitrogen oxides emissions from conventional electric generation and combined heat and power plants declined. The largest reduction was in sulfur dioxide emissions, which fell 7.9 percent. It was the largest decline since the 9.2 percent reduction in 2000. Carbon dioxide emissions were reduced by 2.2 percent and nitrogen oxides emissions were reduced by 4.1 percent.

Work continued within the electric power industry and at the Federal Energy Regulatory Commission (FERC) to implement the requirements of the Energy Policy Act of 2005. This Act amended the Federal Power Act by adding Section 215, which set the responsibility for overseeing operations, developing procedures, and enforcing mandatory reliability standards in the electric power industry to a new electricity reliability organization (ERO). Section 215 requires FERC to certify the ERO and approve reliability standards proposed by the ERO. In July 2006, FERC certified the North American Electric Reliability Corporation (NERC) to be the ERO.[2] FERC also provided guidance on a pro forma Delegation Agreement between NERC and Regional Entities under which Regional Entities would have the authority to recommend reliability standards to the ERO and enforce them. In Order Nos. 693 and 693-A, the FERC approved 83 of 107 proposed Reliability Standards for which the ERO assumed enforcement responsibilities in June 2007.[3] Under this new authority FERC may undertake enforcement actions independent of the ERO, including the imposition of penalties. The FERC, under its new general oversight responsibilities, continued to examine, provide input, and approve new mandatory standards that became effective in June 2007.

Generation

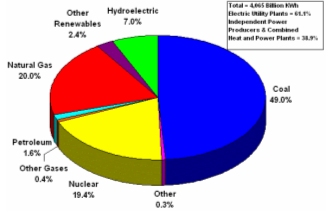

Net generation of electric power increased 0.2 percent from 2005 to 2006, rising to 4,065 million megawatthours (MWh) (Figure ES 1). According to the Bureau of Economic Analysis, the U.S. real gross domestic product increased 3.4 percent in 2006, and the Federal Reserve’s tally of total industrial production showed a 3.0 percent increase in 2006. Notwithstanding these indicators of robust economic activity, which normally correspond to increases in demand for electric power, milder temperatures than in the previous year contributed significantly to the relatively flat rate of increase in electric power generation. According to the National Oceanic and Atmospheric Administration (NOAA), heating degree days in 2006 were 7.4 percent lower and cooling degree days were 2.1 percent lower than they were in 2005. Therefore, demand for electricity for heating and cooling purposes was lower.

| Figure ES 1. U.S. Electric Power Industry Net Generation, 2006 |

|

| Sources: Energy Information Administration, Form EIA-906, "Power Plant Report;" and Form EIA-920 "Combined Heat and Power Plant Report." |

The three primary energy sources for generating electric power in the United States are coal, natural gas, and nuclear energy. These three sources consistently provided between 84.6 and 88.6 percent of total net generation during the period 1995 through 2006. Petroleum’s share of total net generation peaked at 3.6 percent in 1998. It has declined thereafter to a low of 1.6 percent in 2006. Conventional hydroelectric power’s contribution has declined from 9.3 percent in 1995 to 7.1 in 2006. Renewable energy sources, other than hydroelectric, contributed 2.4 percent of the Nation’s net electric generation in 2006. Since 1995, renewable generating capacity, on average, has accounted for 2.1 percent of net generation. In that time, 2001 was the only year in which net generation by renewable resources was less than 2.0 percent of total net generation (1.9 percent).

Electricity generation from coal in 2006 fell 1.1 percent from 2005 to 1,991 million MWh. In the past decade, generation from coal declined only one other time, between 2000 and 2001. Coal’s share of total net generation continued its slow decline over the past decade, from its peak of 52.8 percent in 1997 to 49.0 percent in 2006. Coal-fired plants continued to be the primary source of baseload generation. However, its share of total net generation decreased notwithstanding that total net generation increased by 0.1 percent. This was attributable to continued growth in natural gas and nuclear generation, reflecting the cumulative effects of the growth in natural gas-fired capacity and upgrades of nuclear power plants that emerged following 1997. It also reflects a reduction in net summer coal-fired generating capacity, with 967 MW retired or derated, only partially offset by 542 MW of new capacity.

The average annual growth in natural gas-fired electric power generation from 1995 to 2006 was 4.6 percent, compared to 1.4 percent average annual growth for both coal and nuclear power generation. Most of the new electric power plants placed in service in the United States since 1999 have been natural gas-fired, which are generally cleaner and more efficient than coal plants. Natural gas generation showed the highest rate of growth from 2005 to 2006 of the traditional energy sources, increasing 7.3 percent and reaching 813 million MWh. Part of the growth in 2006 was attributable to the disruption of natural gas supplies in 2005 due to Hurricanes Katrina, Rita, and Wilma, which contributed to high natural gas prices nationally, and lower natural gas electric power generation in the Gulf Coast States. By 2006, more normal conditions had returned to the region, and natural gas prices returned to a more competitive level.

Net generation at nuclear plants increased 0.7 percent in 2006 to 787 million MWh. Between 1995 and 2006, nuclear generation has ranged from an 18.0-20.6 percent share of total net generation with an annual average growth in net generation of 1.4 percent from 1995 through 2006, despite the fact that no new nuclear units have been constructed. The continued growth in nuclear generation is due to the improved capacity utilization (the capacity factors for nuclear plants have increased nearly 17.6 percentage points over the last decade) and incremental capacity upgrades to existing units. In 2006, upgrades produced 346 MW of incremental capacity and capacity factors increased from 89.3 percent in 2005 to 89.6 percent in 2006. The increase in capacity, plus improved capacity utilization, combined with the reduction in coal-fired generation contributed to the rise in nuclear generation’s share of total net generation.

Net generation from conventional hydroelectric plants increased 7.0 percent over 2005, to 289 million MWh, although the level was still lower than the peak year for hydroelectric production over the past decade (356 billion kilowatthours in 1997). During the period from 1999 through 2004, the western United States experienced one of the most severe droughts in its history. Beginning in spring 2005, precipitation levels improved in the Northwest, and reservoirs began to recover, but aggregated reservoir levels were still low at year end.[4] Above average precipitation in 2006 ended the drought in the Northwest. As a result, Washington, Oregon, and Idaho, three of the major hydroelectric power producing States in the country, collectively produced 17.6 percent more hydroelectric generation than in 2005. Washington had the largest increase in conventional hydroelectric generation, increasing by 9.9 million MWh over 2005.

Petroleum-fired generation fell 47.5 percent, to 64.4 million MWh and accounted for only 1.6 percent of total net generation. Over the past decade, petroleum-fired electric power generation has declined at an average annual rate of 1.3 percent. The large decrease in 2006 is directly attributable to sustained high petroleum prices following the 50.1 percent price increase in 2005, as petroleum prices declined only 3.3 percent in 2006.

Renewable energy, other than hydroelectric, grew 10.6 percent and accounted for 2.4 percent of net generation in 2006. The greatest growth in the renewable sector was in wind generation, which contributed 95 percent of the growth in renewable energy. Wind generators produced 26.6 million MWh, 49.3 percent higher than in 2005.

Generation from other gases (refinery gases, blast furnace gas, etc.) and other miscellaneous sources accounted for the remaining net generation. Net generation from these sources increased from 28.8 million MWh in 2005 to 30.0 million MWh in 2006. The generation produced by these resources excludes the generation required by pumped-storage hydroelectric generation. In both 2005 and 2006, the net energy requirement for pumped-storage hydroelectric generation was 6.6 million MWh.

Fossil Fuel Stocks at Electric Power Plants

End-of-year coal stocks reversed the declines of the previous three years and grew to a level that was just below the total seen at the end of 2002, the highest level experienced over the past 12 years. Stocks as of December 31 totaled 141.0 million tons, 39.4 percent higher than December 31, 2005. The resumption of more normal railroad operations from mines in the Powder River Basin (PRB) of north-central Wyoming and southeastern Montana was the major factor contributing to the recovery of subbituminous coal stocks. Deliveries of coal from these mines were disrupted beginning in mid-May 2005 when two major train derailments exposed a need for immediate major maintenance on the PRB rail lines. Flooding in the region had also damaged the tracks. Extensive repair and rebuilding disrupted rail traffic flows and resulted in a shortfall in rail shipments, of as much as 15 percent below the normal level. Rail operations were disrupted throughout the entire second half of 2005, and to a lesser extent into 2006. NERC was concerned enough that the issue was placed on its “Watch List.” However, as of release of the NERC’s 2006/2007 Winter Assessment in November 2006, railroad coal operations in the region were sufficient to remove the issue from the “Watch List.”[5]

In 2006, inventories of petroleum increased by 3.0 percent to 51.6 million barrels by year end. Stock levels during 2004, 2005, and 2006 were lower compared to the beginning of the decade. In 2004 and 2005, this reflected the continued growth in the use of petroleum generation to meet higher summer peak demand, which limited the inventory build-up. Conversely, in 2006, the continuation of high petroleum product prices relative to pre-2005 prices contributed to both a 48.2 percent decrease in total petroleum deliveries to generators and a 47.5 percent reduction in petroleum-fired generation resulting in a modest inventory build.

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Historical | ||

| Back Issues | ||

| Historical Spreadsheets | xls | |

| Related Links | ||

| Electric Generating Capacity (Existing) | html | |

| Electric Generating Capacity (Planned) | html | |

| Electricity Database Files | dbf | |

Capacity

Total U.S. net summer generating capacity as of December 31, 2006 was 986,125 MW, an increase of 0.8 percent from January 1, 2006 (Figure ES 2). New generating capacity added during 2006 totaled 12,129 MW, while retirements totaled 3,458 MW. Natural gas-fired generating units accounted for 8,563 MW or 70.6 percent of capacity additions. Of that amount, 7,374 MW were highly efficient combined-cycle units. Since the late 1990s, natural gas has been the fuel of choice for the majority of new generating units, resulting in a 99.0 percent increase in natural gas-fired capacity since 1999. The construction of natural gas plants began increasing in 1999, peaked during 2002 and 2003, but has since declined considerably.

On December 31, 2006, natural gas-fired generating capacity represented 388,294 MW or 39.4 percent of total net summer generating capacity (Figure ES 2). Although new natural gas-fired combined-cycle plants produce electricity more efficiently than older fossil-fueled plants, high natural gas prices can work against full utilization of these plants if such prices adversely affect economic dispatch.

Petroleum-fired capacity totaled 58,097 MW, down slightly from prior year levels. This represents 5.9 percent of all generating capacity and includes approximately 31,700 MW of primarily residual oil-fired steam units located in Florida, New York, Pennsylvania, Connecticut, and Massachusetts. Gas turbines (20,300 MW of capacity) and internal combustion units (5,000 MW of capacity) account for most of the remaining petroleum-fired capacity.

Coal-fired generating capacity remained essentially unchanged at 312,956 MW or 31.7 percent of total generating capacity. This share of total capacity represents a slight decline from 2005 due to the fact that capacity additions over the past year have been primarily natural gas-fired. During 2006, 542 MW of new coal-fired generators started commercial operation, while 735 MW of older, inefficient coal-fired capacity were retired from service. The most notable addition to capacity was the 400-MW unit 3 at the Tucson Electric Power Company’s Springerville facility, while the shutdown of 180 MW of capacity at NRG’s C.R. Huntley facility was most notable on the retirement side. Although coal-fired capacity has not changed significantly since 1995, generation by coal-fired plants was 16.5 percent higher in 2006 than in 1995. The utilization of coal-fired generators, a measure of actual generation compared to the theoretical maximum output, has increased from 63 percent in 1995 to 73 percent in 2006. Planned coal-fired capacity on January 1, 2007, totaled 29,698 MW, up slightly from the 27,884 MW reported on January 1, 2006. Most of this proposed capacity is scheduled to start commercial operation between 2009 and 2011. Coal plants planned for Texas, Kentucky, Illinois, and Wisconsin represent over one-half of all proposed coal-fired capacity additions.

| Figure ES 2. U.S. Electric Power Industry Net Summer Capacity, 2006 |

|

| Source: Energy Information Administration, Form EIA-860, “Annual Electric Generator Report.” |

Wind plants accounted for most of the remaining new generating capacity with 2,642 MW of capacity added during 2006, considerably above the levels of 2005. Texas and Washington combined for 1,318 MW, or one-half of all new wind capacity in 2006. The Horse Hollow Wind Energy Center in Taylor County, Texas was completed during 2006. It is the largest wind facility in the Nation with a nameplate capacity of 736 MW. The increase in wind capacity for 2006 was stimulated in part by the production tax credit (PTC). The PTC, which encourages construction of wind plants, has been extended until December 31, 2007. First enacted through the Energy Policy Act of 1992 to encourage construction of wind and qualifying biomass generating facilities, the PTC has expired and been renewed several times. The most recent renewal was enacted through the Energy Policy Act of 2005. The growth in wind generating capacity is expected to continue, with over 5,000 MW of planned wind generating capacity proposed to begin operation during 2007. Texas is expected to add over 1,400 MW of wind capacity, while Colorado, Illinois, and Oregon are also expected to add a significant amount of wind capacity in 2007. The electric generating capacity from non-hydro renewable energy sources increased 13.7 percent from 2005 to 2006, due primarily to this increase in wind generating capacity.

Nuclear net summer generating capacity totaled 100,334 MW or 10.2 percent of total capacity, up slightly from 99,988 MW in 2005. This 346-MW increase in capacity was due to modifications and uprates at existing nuclear units, bringing nuclear to its highest capacity level since 1996. Conventional hydroelectric generating capacity accounted for 7.9 percent of total capacity with a summer net generating capacity of 77,821 MW. Pumped storage hydroelectric generating capacity totaled 21,461 MW. Combined, conventional and pumped storage generating capacity accounted for 10.1 percent of total capacity. Like coal and nuclear, hydroelectric generating capacity has remained relatively unchanged over the last 10 years. In 2006, there were dispersed and distributed generating units, totaling 16,678 MW of capacity. [6] This compares to compares to 9,579 in 2004, the first year for which this data was collected by EIA.

As of December 31, 2006, reported planned capacity additions that are scheduled to start commercial operation from 2007 through 2011 totaled 87,109 MW. This compares with 94,429 MW of planned capacity reported on December 31, 2005, for the 5-year period through 2010. Planned natural gas-fired capacity totaled 46,028 MW or 52.8 percent of total planned capacity additions. This compared with 56,925 MW or 60.3 percent of total planned capacity reported as of December 31, 2005.

Figure ES 3 compares average capacity factors by energy source. As expected, nuclear and coal-fired generation have the highest average capacity factors at 89.6 percent and 72.6 percent, respectively. This is consistent with the economies of scale that these forms of capital intensive and energy efficient generation provide to serve energy requirements. Accordingly, coal and nuclear capacity serve baseload energy requirements, which are reflected by higher average capacity factors relative to other forms of generation. The 72.6 percent average capacity factor for coal-fired generation reflects a modest decrease from the 73.3 percent value achieved in 2005. Notwithstanding, it is well above the 62.7 percent average capacity factor experienced in 1995, and slightly above the 72.0 percent five year average (2002 to 2006). The average capacity factor for nuclear generation increased a modest 0.3 percentage points to 89.6 percent. This compares to the 89.5 percent average over the past five years and the low of 72.0 percent in 1997. The five year average capacity factors for coal and nuclear generation relative to historical improvements dating back to 1995 suggests that the industry may be reaching a plateau in terms of efficiencies gained through improved maintenance practices, and in the case of nuclear, reducing the length of refueling outages.

Because of the influx of new combined cycle natural gas generation prior to the significant and sustained price increase that occurred in 2003, average capacity factors for natural gas are calculated for both combined cycle generation and simple cycle natural gas generation.[7] In 2006, combined cycle generating capacity totaled 183,987 MW and supplied 621,162,311 MWh of net generation. This equates to a 38.5 percent average capacity factor. Simple cycle generating capacity totaled 204,307 MW with associated net generation of 191,881,236 MWh. The average capacity factor for simple cycle natural gas-fired generation was 10.7 percent. These results are consistent with the greater efficiency associated with combined cycle generation, which allows it to be dispatched to serve the intermediate portion of utilities’ load curve.

The more recent emphasis placed on wind capacity, which is not a dispatchable resource, is reflected in the reduced performance of renewable resources in aggregate as measured by a composite capacity factor. Renewable generation other than hydroelectric had a 45.6 percent capacity factor in 2006. In 1999, the average capacity factor for other renewable generation was 59.3 percent. Thereafter, it has declined every year. The lower capacity factor for this class of generation relative to baseload generation is consistent with the natural replenishment but limited flow of renewable energy sources. For example, the availability of wind generation is a function of prevailing wind levels. As a result, it is not conducive to continuous dispatch, as compared to solid and liquid fuel biomass generation (e.g., landfill gas, municipal solid waste, black liquor and wood waste solids). Moreover, the addition of wind generating capacity has surpassed all other forms of renewable generation. Between 2000 and 2006, net summer capability of wind generating capacity increased from 2,302 MW to 11,351 MW. Of this capacity, 2,631 MW was placed in service during 2006. During this same period, solid and liquid biomass generation increased from 3,591 MW to 7,858 MW. Therefore, by 2006, the near 6-fold increase resulted in wind capacity exceeding the total amount of installed solid and liquid biomass capacity by 3,493 MW.[8]

Conventional hydroelectric generation had an average capacity factor of 42.4 percent in 2006. Like other renewable resources, conventional hydroelectric generation is limited by the replenishment of water. The 42.4 percent average capacity factor realized in 2006 is consistent with the 42.6 percent average capacity factor between 1995 and 2006.

Fuel Switching Capacity

The total amount of net summer capacity reporting natural gas as the primary fuel was 388,294 megawatts, of which 122,124 MW (31.5 percent) reported a current operational capability to switch to fuel oil as an alternative fuel. This means that the capacity had in working order all necessary equipment, including fuel storage, to switch from gas to petroleum-fired operation. However, most of this capacity is subject to environmental regulatory limits on the use of oil, such as restrictions on how many hours per year a unit is allowed to burn oil. Of the 122,124 MW of gas-fired capacity that reported the ability to switch to oil, only 32,031 MW (26.2 percent) reported no environmental regulatory constraints on oil-fired operations.

“Switchable” capacity is spread across the major generating technologies. Combustion turbine peaking units account for 42.3 percent (51,636 MW) of this capacity. Steam-electric generators (33,470 MW) and combined cycle units (36,139 MW) account for 27.4 percent and 29.6 percent, respectively. Internal combustion engines make up the remaining 0.7 percent. Of the steam-electric capacity that is capable of switching from natural gas to petroleum, which tends to be comprised of older units, almost half of the capacity had no reported environmental regulatory restrictions on petroleum-fired operations. In contrast, only 22.4 percent of the combustion turbine capacity and 11.0 percent of the combined-cycle capacity that are capable of switching fuels report no environmental regulatory restrictions on petroleum-fired operations.

The data show that most of the new natural gas-fired capacity added at the beginning of this decade cannot use oil as a backup or alternative fuel. During the period 2000 to 2006 total natural gas-fired net summer capacity increased from 219,590 MW to 388,294 MW, a gain of 168,704 MW. However, during this same period the amount of gas-fired capacity that can switch to petroleum increased by only 45,367 MW, equivalent to about 26.9 percent of the increase in total natural gas-fired capacity. About 39 percent of the capacity capable of switching from natural gas to petroleum was built prior to 1980 and close to two-thirds was built prior to 2000.

Interconnection Costs

During 2006, 275 generators representing a total nameplate capacity of 13,152 MW were connected for the first time to the electric grid. The interconnection costs are presented by producer type (Table 2.12) and by distribution, subtransmission and transmission voltage class (Table 2.13). Total cost for individual generator interconnection varies based on its components. The components of the total cost may vary based on whether or not an interconnection infrastructure was already in place, and the type of equipment for which costs were incurred, along with other factors associated with the generator technology. Though the amount of capacity connected to the grid was about the same for both independent power producers (IPP) and electric utilities, the total cost for the IPP sector was significantly greater due in part to the interconnection of several large wind plants. Typically sited in relatively remote locations, wind plants usually require the construction of longer transmission line extensions to the plant sites than might be required for conventional power plants.

Fuel Costs

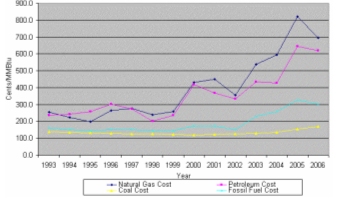

The 2006 average delivered cost for all fossil fuels used at electric power plants (coal, petroleum, and natural gas combined) for electricity generation was $3.02 per MMBtu Figure ES4 as compared to $3.25 per MMBtu in 2005, a decline of 7.1 percent. The decline was attributable to a decrease in the cost of petroleum and natural gas. The cost of petroleum decreased 3.3 percent, while natural gas prices decreased 15.5 percent, notwithstanding the 8.0 percent increase in deliveries to natural gas-fired generators. The decline in the demand and delivered price of petroleum, the increase in natural gas deliveries and the decline in natural gas prices reflect the restoration of natural gas production and transportation infrastructure following hurricanes Katrina and Rita in August and September 2005. Therefore, petroleum-fired generation declined as natural gas supplanted petroleum as the primary fuel for use in dual fuel capacity.

The cost of natural gas at electric power plants in 2006 was $6.94 per MMBtu, 15.5 percent less than the 2005 cost of $8.21 per MMBtu, but still 16.4 percent above the 2004 cost of $5.96 per MMBtu, and 94.9 percent above 2002 when the cost was $3.56 per MMBtu. The fluctuations in natural gas prices are attributable to several causes. The demand for natural gas continues to expand in the electric power industry with increasing natural gas capacity. Disruptions in natural gas production in and around the Gulf of Mexico caused by hurricanes Katrina, Rita and Wilma in 2005 drove prices up to an all-time high of $8.21 per MMBtu. Prices began to drop at the beginning of 2006 as the gas industry recovered from these adverse weather events. An increase in domestic production in 2006, less demand during the mild winter of 2006, and record amounts of natural gas injected into storage to replenish stocks, all contributed to robust supply during 2006. The supply was more than adequate to meet demand, and despite a hot summer with record temperatures in July driving up consumption of natural gas to meet peak summer demands, the annual average cost in 2006 was lower than 2005’s peak level.

The cost of petroleum somewhat mirrored the cost of natural gas. The 2006 cost of petroleum was $6.23 per MMBtu, a 3.3 percent decrease from the 2005, but a 45.2 percent increase from 2004 and an 86.5 percent increase from 2002. These fluctuations since 2002 were due to the effects of hurricanes disrupting production and supply (in 2005) and rising prices in the world oil market due mainly to increased demand from developing Nations. In 2006, several U.S. refineries were still shut down or operated at reduced output because of hurricane damage sustained in 2005. Others began maintenance schedules that had been deferred from the previous fall. The reduction in petroleum supply led to fuel switching at electric power plants, mostly to natural gas, as a result of higher peak electricity demand in the summer. Although the average cost of natural gas was higher than petroleum on a dollar per MMBtu basis ($6.94 versus $6.23), the higher thermal efficiency realized by burning natural gas, measured by heat rates (see Table A6 for average heat rates by prime mover and fuel-type) favored the use of natural gas over petroleum in fuel switchable combined cycle generation.

Coal is the only fossil fuel that has continued to increase in cost at electric plants each year since 2000. The 2006 delivered cost was 9.7 percent higher than 2005, 24.3 percent higher than 2004, and 40.8 percent higher than in 2000 when the trend began (Figure ES 4). Increasing delivered coal costs are the result of several factors. New safety regulations requiring retro-fitting of mining equipment, higher taxes on coal extraction, and higher cost for diesel fuel (used for production and transportation) all contributed to the producers’ increase in coal prices. Coal-fired electricity generators also faced new rail fuel surcharges as well as numerous increases in transportation costs as contract rollovers escalated the delivery price for new contracts.

Emissions

The carbon dioxide, sulfur dioxide and nitrogen oxides emissions estimates for electricity are based on the fossil fuels consumed by electric power plants for electric power generation, and fossil fuels consumed by combined heat and power plants for the generation of electric power and useful thermal output. In addition to the new 2006 estimates, the emissions estimates for carbon dioxide have been revised back to 1995. The revisions are primarily due to updates to the emissions factors used in the estimation methodology (See the discussion of Air Emissions in the Technical Notes and, in particular, Tables A1, A2, and A3).

Estimated carbon dioxide emissions by U.S. electric generators and combined heat and power facilities decreased by 2.2 percent from 2005 to 2006 (from 2,514 million metric tons to 2,460 million metric tons). This was the first decrease reported since 2001. The decline reflects both the decrease in total net generation of electric power from fossil fuels and the changes in the contribution of each fossil fuel to electric power generation in the United States. Coal consumption declined 1.1 percent, while petroleum consumption declined 43.3 percent. Consumption of natural gas, which contributes the least amount of carbon dioxide per Btu consumed, rose by 5.6 percent in 2006. Overall, electric power generation by these three fossil fuels fell 0.9 percent from 2005 to 2006.

Estimated emissions of nitrogen oxides and sulfur dioxide also declined between 2005 and 2006. Nitrogen oxides emissions dropped by 4.1 percent (from 3.961 to 3.799 million metric tons). Sulfur dioxide emissions decreased by 7.9 percent (from 10.340 to 9.524 million metric tons).

Emissions trends followed the use of fossil fuels and the impacts of Federal and State pollution control regulations on power plant operations. One factor is the increase in required installations of new pollution control equipment. For example, coal-fired generating capacity with equipment for removing sulfur dioxide (flue gas desulfurization units, also referred to as scrubbers) increased by 26.1 percent between 1994 and 2005, from 80.6 to 101.6 gigawatts, covering 32.5 percent of total coal-fired capacity. Another factor affecting emission decreases is changes in fuel mix, particularly the increased use of subbituminous coal. Many plants have switched from bituminous coal to subbituminous coal which emits less sulfur dioxide and nitrogen oxides when burned due to the relatively low sulfur content and low combustion temperature associated with subbituminous coal.

Trade

Total wholesale purchases of electric power in the United States declined in 2006 for the third straight year to 5,503 million MWh, a 9.7 percent reduction. Almost half the volume of wholesale sales is provided by energy-only providers, or power marketing companies, a class of electric entities, authorized by FERC to transact at market based rates, that came into being during the late 1990s with the deregulation of the wholesale power markets. However, total sales volumes from wholesale power marketers have declined dramatically from 5,757 million MWh in 2002 to 2,446 million MWh in 2006, and their market share has declined from over 67.2 percent to 44.5 percent over the same period. Between 2004 and 2006, capacity margins declined from 20.9 percent to 16.1 percent. In tighter capacity markets, utilities with retail native load and wholesale requirements service obligations have less surplus capacity and energy available to engage in off-system sales with third parties. Correspondingly, all of the traditional electric utility ownership classes have increased their market share of wholesale sales notwithstanding that their sales volumes have held steady. Traditional utilities tend to have longer term contracts, providing sales volume stability. The number of power marketing companies participating in wholesale markets has shrunk from 2002 to 2006. This is the result of fewer sales and reduced margins for the marketing companies. Independent power producers continue to provide an increasing share of the volume, reaching 24.1 percent in 2006.

The Nation’s only international trade in electric power is with Canada and Mexico, and nearly all the trade is conducted with Canada. Most Mexican electric power trade is done with the State of California, while transactions with Canada are conducted through several large transmission corridors located in the Pacific Northwest, the Northern Plains, and New England. Much of the electricity provided from Canada is hydroelectric generation available for sale because of heavy seasonal river flows.

Total international net imports of electric power declined from about 24.7 million MWh in 2005 to about 18.4 million MWh in 2006, consistent with weak demand growth in the United States. Canadian sales to the United States declined from 42.9 million MWh in 2005 to 41.5 million MWh in 2006, and U.S. exports to Canada increased by 21.1 percent. Overall, total U.S. imports declined to 42.7 million MWh from 44.5 million MWh in 2005, and total exports grew to 24.3 million MWh from 19.8 million MWh in 2005.

Revenue and Expense Statistics

In 2006, major investor-owned electric utility operating revenues (from sales to ultimate customers, sales for resale, and other electric income) were $277 billion, a 3.6 percent increase from 2005. Operating expenses in 2006 stayed in line with revenue growth, also increasing 3.6 percent, to $247 billion. Net income in 2006 was $29.9 billion, a slight increase over the $28.9 billion of net income realized in 2005.

Increases in operating expenses were driven by increasing delivered fuel costs (up about 6 percent) and increases in “other” production costs[9] (up about $3.8 billion). Unlike 2005, purchased power expenses were held in check, increasing only slightly over 2005 levels. Transmission expenses increased for the fifth consecutive year and have more than doubled since 2001, averaging a 21.2 percent annual increase over that period. Distribution expenses, however, remained flat in 2006, increasing only slightly from 2005, while averaging only a 2.6 percent annual increase since 2001. Average operating expenses for fuel at investor-owned fossil steam plants posted another significant increase in 2006, rising 8.8 percent to 3.2 mills per kilowatthour (kWh). Average operation expenses at all plants other than hydroelectric increased, as did average maintenance expenses.

Electricity Prices and Sales

In 2006, the average retail price for all customers rose to 8.9 cents per kWh, a sharp increase of three-fourths of a cent from the 2005 price level. The 9.3 percent increase was the largest since 1981. Fourteen States and the District of Columbia saw the average price of electricity rise by 10 percent or more from 2005 to 2006. Prices increased in all regions of the country but most of the larger increases occurred in the East. Another 14 States saw increases between 5 and 10 percent between 2005 and 2006. States with restructuring programs such as Maryland and Delaware had portions of their retail electricity price caps lifted in 2006, contributing to significant price hikes.

Residential prices increased to 10.4 cents per kWh, almost a cent, or 10.1 percent, between 2005 and 2006. Average residential prices rose sharply in the New England and West South Central Census Divisions as Connecticut and Texas had large price increases for the second year in a row. Delaware had the highest average residential price increase at almost 30 percent.

Average industrial prices increased to 6.2 cents per kWh, or 7.5 percent above 2005. Average commercial prices increased to 9.5 cents per kWh, a 9.1 percent increase. In Texas, where the largest volume of industrial sales on a State level occurs, industrial prices increased almost 10 percent. About two-thirds of the industrial market in Texas is now served by energy service providers. Of the remaining one-third, investor-owned utilities served 17.1 percent; distribution cooperatives served 7.5 percent, and municipal utilities 6.2 percent. In the six New England States, average industrial prices increased more than 28 percent.

Total retail sales of electricity in 2006 were 3,670 million MWh. Annual growth in electricity sales in 2006 was 0.2 percent, showing virtually no growth compared with the 1.8 percent average annual growth since 1995. Sales to the residential sector decreased by 0.6 percent from 2005 to 2006. This marks only the second time residential sales decreased since 1974. Sales to the commercial sector increased by 1.9 percent, and sales to the industrial sector decreased 0.8 percent. Total retail sales increased by more than 5 percent in five States, led by West Virginia, which showed a 7.2 percent increase. Sales fell in 18 States, including both Maryland and New York where sales decreased by over 5 percent.

In the last few years, some States have encouraged utilities to adopt customer service programs which respond to growing concerns about the environment, electricity reliability, and the rising cost of providing electricity. Green pricing programs allow consumers to purchase electricity generated from wind and other renewable sources and pay for renewable energy development. Customers subscribing to green pricing programs increased steadily between 2002 and 2005. In 2006 however, the single largest provider of green pricing services in the country discontinued service in two States. More than 297,600 customers in green pricing programs reverted to standard service tariffs, predominantly in Ohio and Pennsylvania.

Net metering programs allow consumers with onsite generators to send excess generation to the grid and receive credit for that energy on their bill. The number of customers in these programs has been steadily increasing. In 2002 there were 4,472 customers in net metering programs; in 2006 there were more than 34,000 customers. Seventy-five percent of these net metering customers are in California. Despite the growth of green pricing and net metering customers over the past few years, the total number of customers in both programs is still less than 1 percent of the national total.

Demand-Side Management

In 2006, electricity providers reported total peak-load reductions of 27,240 MW resulting from demand-side management (DSM) programs, a 6.0 percent increase from the amount reported in 2005. Reported DSM costs increased to $2.1 billion, a 6.7 percent increase from costs reported in 2005. DSM costs can vary significantly from year to year because of business cycle fluctuations and regulatory changes. Since costs are reported as they occur, while program effects may appear in future years, DSM costs and effects may not always show a direct relationship. However, DSM costs and program benefits have tracked consistently in the last 4 years. Nominal DSM expenditures have increased significantly since 2003, averaging 16.5 percent average annual growth over the period. Actual peak load reductions have improved by an annual average of 5.9 percent, while energy savings have risen 8.3 percent on average since 2003. New pricing programs designed to deliver real-time signals to consumers may account for some of the recent cost increases and improved efficiency over the last several years.