This Just In ... OCC's Districts Report on Investment Opportunities for Banks

Looking for new investment ideas? In this article, OCC's district community affairs officers (DCAOs) report on financing initiatives and partnership opportunities in each of the OCC's four districts. DCAOs can provide more information about these and other community development investment opportunities. DCAOs can also consult with national banks in developing successful approaches to community development lending and service delivery approaches.

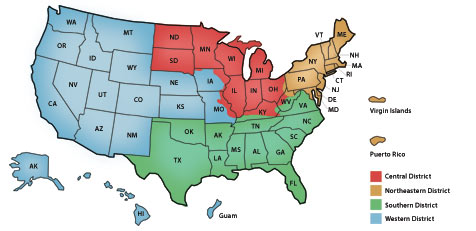

Click on the map below for the DCAOs in your district.

Northeastern District |

|

John Farrell (617) 482-1643

Denise Kirk-Murray (212) 790-4053 |

Environmentally Sustainable and Energy Efficient Housing

Boston Community Capital (BCC), a certified community development financial institution, and its partners in the Green Building Production Network are supporting the economic development of low-income communities throughout Massachusetts and the northeastern United States. They announced that four community organizations were awarded $2 million in commitments to help build or renovate more than 800 units of mixed-income housing with state-of-the-art environmental and energy design features. The projects, located throughout the Boston metropolitan area, are in the Chinatown, Roxbury, Jamaica Plain, and Cambridge neighborhoods.

Financial institutions interested in investing in these developments, or supporting BCC in other ways, should contact DeWitt Jones at (617) 427-3580 or visit BCC's Web site at www.bostoncommunitycapital.org/.

Connecticut Announces New Affordable Housing Investment Opportunity

The Connecticut Housing Finance Authority (CHFA) announced a pilot program that will allow nonprofit organizations in Connecticut to acquire land and property for affordable housing. The Non-Profit Site Acquisition Program will provide capital to qualified nonprofit developers to finance the costs associated with taking an option and/or purchasing property to be used for affordable housing in Connecticut. With these funds, nonprofits can take advantage of opportunities, previously unavailable to them, and provide more affordable housing.

The Non-Profit Site Acquisition program leverages public and private funds and offers a new investment opportunity for financial institutions. The program will be funded through the sale of taxable bonds in which banks may invest. The rate on these bonds will be 1.5 percent, and the term of the bonds is five years. The fund will be administered by an intermediary organization, responsible for allocating the funds to the nonprofits that will acquire and develop properties. The selection of the intermediary organization is expected to occur by late summer, with the program ready for implementation in the fall of 2006.

For further information, contact Connecticut Housing Finance Authority at (860) 721-9501 or check out the organization's Web site at www.chfa.org.

Central District |

|

Paul Ginger (312) 360-8876

Norma Polanco (216) 447-8866

|

The Midwest Assistance Program Loan Fund

The Midwest Assistance Program Loan Fund (MAPLF) is a nonprofit organization that provides predevelopment loans to small rural communities in nine Upper Midwest States - Iowa, Kansas, Minnesota, Missouri, Montana, Nebraska, North Dakota, South Dakota, and Wyoming. Loans can be used for clean water and wastewater projects that serve lower-income populations. Borrowers from MAPLF are rural communities and other public water or wastewater authorities with less than 10,000 in population.

Established in 2003, MAPLF has closed seven loans totaling $105,000, has $250,000 more in process, and has sustained no losses. Loans have been made in four of the nine states in MAPLF's service region. MAPLF is an affiliate of the Midwest Assistance Program, which provides engineering, training, and other consulting services to help small rural communities plan and implement water and wastewater improvement projects. MAPLF typically funds projects that have multiple layers of funding, including grants and loans from a variety of sources. Originally capitalized with $100,000 from the Midwest Assistance Program, MAPLF also funds its loans with the proceeds of a federal grant, and is actively seeking new investors. Banks can participate by investing directly into MAPLF, by referring prospective borrowers that do not meet conventional credit criteria, and by structuring MAPLF into financing packages in which the banks would like to participate.

For more information, visit www.map-inc.org or contact Tom Kopp at (952) 758-4334 or tkmap@bevcomm.net .

Appalachian Region's Progress Fund Expands

Tourism in the Appalachian region of Ohio is getting a boost from the Progress Fund, a certified community development financial institution (CDFI) lending needed capital and providing entrepreneurial coaching to small businesses in the travel and tourism industry.

Using a start-up grant of $200,000 from the State of Ohio, the Progress Fund is expanding its service area, currently encompassing 39 counties in Pennsylvania and West Virginia, into the 29 counties of Ohio's Appalachian region. The Progress Fund supports the niche industry of tourism businesses, including bed and breakfasts, brew-pubs, general stores, restaurants, museums, and similar small businesses that attract and serve visitors in rural areas. The Progress Fund is currently seeking investors to capitalize its Ohio expansion. Investors are asked to invest a minimum of $100,000 to help meet the organization's goal of a $5 million fund by 2007. Terms are flexible and negotiated individually with investors. Examples of previous investment terms have included a non-amortizing, 10-year loan at below market interest rates.

To invest in any of the Progress Funds, please contact David Kahley, CEO, at (724) 529-0384, or visit it's Web site, www.progressfund.org.

Southern District |

|

Karol Klim (678) 731-9723 x252

David Lewis (214) 720-7027

|

Tampa Bay Black Business Investment Corporation

The Tampa Bay Black Business Investment Corporation, Inc. (TBBBIC), a nonprofit community development financial institution, is a public-private partnership between local government and the corporate community. The TBBBIC provides technical assistance and financing for African-American owned start-ups and growing businesses in Hillsborough and Pinellas counties in Florida through the creation of a capital investment fund supported by local financial institutions. TBBBIC assists all small businesses in these counties by working through the Small Business Administration as well as other local programs.

The TBBBIC provides technical assistance to small businesses including advice on the business and marketing plan, preparation of loan packages, business and personal financial statement analysis and small business courses and seminars. TBBBIC offers direct loans for equipment, working capital, accounts receivable, contract financing, and loan guarantees up to the lesser of 50 percent of the loan or $75,000. Currently, TBBBIC has 18 contributing members. Since inception, the TBBBIC has made nearly $7 million in loans; which has produced 460 jobs.

For more information, contact Frances Wimberly at (813) 274-7925, or view the Web site at www.tampabaybbic.com.

Enterprise Corporation of the Delta/HOPE Community Credit Union Offers Opportunity to Help Rebuild

Enterprise Corporation of the Delta/Hope Community Credit Union (ECD/HOPE) is a partner for banks seeking to provide assistance in communities affected by Hurricanes Katrina and Rita. In the months since the hurricanes, cleanup and relief efforts continue, but increasingly the focus is shifting to rebuilding and planning for recovery of the affected areas. Tens of thousands of homes and businesses were destroyed or heavily damaged, displacing families, and disrupting lives. Banks can play a large and vital role in the rebuilding process.

ECD/HOPE can bring proven affordable housing, small business lending, and community development expertise to the victims of the hurricanes, as well as, participating financial institutions. ECD/HOPE is headquartered in Jackson, Mississippi, with offices throughout Arkansas, Louisiana, and Mississippi. ECD/HOPE is a nonprofit certified community development financial institution working to strengthen communities, build assets, and improve lives in economically distressed areas of the mid-South. It does this by providing financial and technical assistance to firms, entrepreneurs, homeowners and community development projects, and by forging strategic partnerships across the public, private sectors, and banks. Since its founding in 1994, ECD/HOPE has generated more than $200 million in financing and assisted more than 13,000 people in economically-distressed communities in the region.

For more information on investment and lending opportunities and how your bank can partner with ECD/HOPE, contact Bill Bynum, chief executive officer, at (601) 944-1100.

Return to top

Western District |

|

Susan Howard (818) 240-5175

Dave Miller (720) 475-7670

|

Individual Development Account Opportunity in Utah

The Utah Individual Development Account Network (UIDAN) is a statewide individual development account (IDA) program and a subsidiary of Utah Issues. Utah Issues is a 30-year-old nonprofit striving to improve the quality of life in Utah by seeking long-term solutions to poverty through various means, including asset-based community development. UIDAN was established in 2004 and, in its first year generated more than 30 savers with more than $22,000 in combined funds from savings accounts and matched funds.

UIDAN proposes to match savers' deposits at a ratio of three to one. As with most IDA programs, UIDAN solicits investments for operating and matching funds. Program participation has expanded to include low-income urban, rural, and tribal communities outside of the original Salt Lake City service area. UIDAN plans to expand, again, into southwestern Utah.

For more information, contact Martha Wunderli, UIDAN's Coordinator, at Martha@utahissues.org .

Colorado Single-Family Mortgage Bonds

The Colorado Housing and Finance Authority (CHFA) has developed a private placement bond program, collateralized by a pool of taxable single-family first and second mortgage loans targeted to low- and moderate-income homebuyers and homeowners, to support the efforts of Colorado banks to invest in affordable housing. This private placement bond program provides an investment opportunity for banks that may qualify for consideration under the Community Reinvestment Act. These bonds, though unrated, are additionally secured by CHFA's general obligation pledge.

CHFA's private placement bond program allows each bank investor to select the geographic coverage of its investment, the targeted income of the borrowers, and the size of their investment. CHFA will offer these private placement bonds on a semi-annual basis.

To learn more about these private placement bonds, please contact John Dolton at (303) 297-7328, or visit www.colohfa.org.

Return to top |

_r1_c1.gif)

_r1_c2.gif)