An official website of the United States government

Official websites use .gov

A .gov website belongs to an official government organization in the United States.

Secure .gov websites use HTTPS

A lock (

) or https:// means you’ve safely connected to the .gov website. Share sensitive information only on official, secure websites.

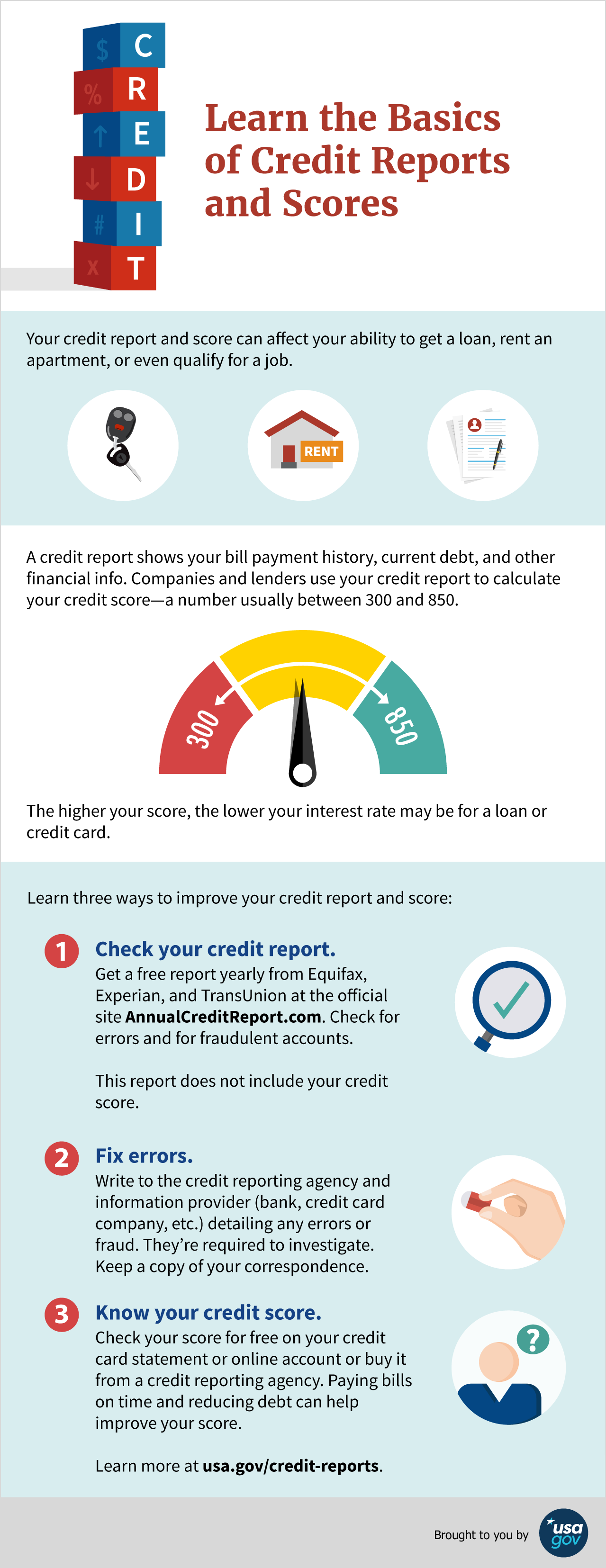

Your credit report and score can affect your ability to get a loan, rent an apartment, or even qualify for a job.

A credit report shows your bill payment history, current debt, and other financial info. Companies and lenders use your credit report to calculate your credit score—a number usually between 300 and 850.

The higher your score, the lower your interest rate may be for a loan or credit card.

Learn three ways to improve your credit report and score:

Check your credit report. Get a free report yearly from Equifax, Experian, and TransUnion at the official site AnnualCreditReport.com. Check for errors and for fraudulent accounts. This report does not include your credit score.

Fix errors. Write to the credit reporting agency and information provider (bank, credit card company, etc.) detailing any errors or fraud. They’re required to investigate. Keep a copy of your correspondence.

Know your credit score. Check your score for free on your credit card statement or online account or buy it from a credit reporting agency. Paying bills on time and reducing debt can help improve your score.

Learn more at usa.gov/credit-reports.

Credit Reports

Credit reports list your bill payment history, loans, current debt, and other financial information. They show where you work and live and whether you've been sued, arrested, or filed for bankruptcy.

Credit reports help lenders decide if they'll give you credit or approve a loan. The reports also help determine what interest rate they will charge you. Employers, insurers, and rental property owners may also look at your credit report. You won't know which credit report a creditor or employer will use to check your credit.

Credit reporting agencies (CRAs) collect and maintain information for your credit reports. Each CRA manages its own records and might not have information about all your accounts. Even though there are differences between their reports, no agency is more important than the others. And the information each agency has must be accurate.

It's important to check your credit reports regularly to make sure that your personal and financial information is accurate. It also helps to make sure nobody's opened fraudulent accounts in your name. If you find errors on your credit report, take steps to have them corrected.

Free Credit Reports

On AnnualCreditReport.com you are entitled to a free credit report from each of the three credit reporting agencies (Equifax, Experian, and TransUnion) every week, through April 2021. You can request all three reports at once, or request them one at a time. Learn about other situations when you can request a free credit report.

Annual Credit Report Request Service PO Box 105281 Atlanta, GA 30348-5281

If Your Request for a Free Credit Report is Denied:

Contact the CRA directly to try to resolve the issue. The CRA should tell you the reason they denied your request and explain what to do next. Often, you will only need to provide information that was missing or incorrect on your application for a free credit report.

A credit score is a number that rates your credit risk. It can help creditors determine whether to give you credit, decide the terms they offer, or the interest rate you pay. Having a high score can benefit you in many ways. It can make it easier for you to get a loan, rent an apartment, or lower your insurance rate.

The information in your credit report is used to calculate your credit score. It's based on your:

Payment history

Outstanding balances

Length of credit history

Applications for new credit accounts

Types of credit accounts (mortgages, car loans, credit cards)

It's important to make sure your credit report is accurate, so your credit score can be too. You can have multiple credit scores. They're not calculated by the same credit reporting agencies that maintain your credit reports. Instead, they're created by different companies or lenders that use their own credit scoring system.

Your free annual credit report does not include your credit score, but you can get your credit score from several sources. Your credit card company may give it to you for free. You could also buy it from one of the three major credit reporting agencies. When you receive your score, you often get information on how you can improve it.

Credit Freeze

Placing a credit freeze allows you to restrict access to your credit report. This is important after a data breach or identity theft when someone could use your personal information to apply for new credit accounts. Most creditors look at your credit report before opening a new account. But if you've frozen your credit report, creditors can't access it, and probably won't approve fraudulent applications.

You have the right to place or lift a credit freeze for free. You can place a freeze on your own credit files and on those of your children age 16 or younger.

Place a Credit Freeze

Contact each credit reporting agency to place a freeze on your credit report. Each agency accepts freeze requests online, by phone, or by postal mail.

Experian Online: Experian Freeze Center Phone: 1-888-397-3742 By mail, write to: Experian Security Freeze PO Box 9554 Allen, TX 75013

Equifax Online: Equifax Credit Report Services Phone: 1-800-685-1111 By mail, write to: Equifax Information Services LLC PO Box 105788 Atlanta, GA 30348-5788

TransUnion Online: TransUnion Credit Freezes Phone: 1-888-909-8872 By mail, write to: TransUnion LLC PO Box 2000 Chester, PA 19016

Innovis Online: Innovis Freeze Options Phone: 1-800-540-2505 By mail, write to: Innovis Consumer Assistance PO Box 26 Pittsburgh, PA 15230-0026

Your credit freeze will go into effect the next business day if you place it online or by phone. If you place the freeze by postal mail, it will be in effect three business days after the credit agency receives your request. A credit freeze does not expire. Unless you lift the credit freeze, it stays in effect.

Lift a Credit Freeze

If you want lenders and other companies to be able to access your credit files again, you will need to lift your credit freeze permanently or temporarily. Contact each credit reporting agency. You'll use a PIN or password to lift your credit freeze. You can lift your credit freeze as often as you need to, without penalties.

It takes one hour for a lift request to take effect if you place it online or by phone. It can take three business days if you request the lift by mail.

Errors on Your Credit Report

If you find errors on your credit report, write a letter disputing the error and include any supporting documentation. Then, send it to:

The credit reporting agency (CRA) and the information provider are liable for correcting your credit report. This includes any inaccuracies or incomplete information. The responsibility to fix any errors falls under the Fair Credit Reporting Act.

Negative information in a credit report can include public records--tax liens, judgments, bankruptcies--that provide insight into your financial status and obligations. A credit reporting company generally can report most negative information for seven years.

Information about a lawsuit or a judgment against you can be reported for seven years or until the statute of limitations runs out, whichever is longer. Bankruptcies can be kept on your report for up to 10 years, and unpaid tax liens for 15 years.

Fixing Errors in a Credit Report

Anyone who denies you credit, housing, insurance, or a job because of a credit report must give you the name, address, and telephone number of the credit reporting agency (CRA) that provided the report. Under the Fair Credit Reporting Act (FCRA), you have the right to request a free report within 60 days if a company denies you credit based on the report.

You can get your credit report fixed if it contains inaccurate or incomplete information:

Contact both the credit reporting agency and the company that provided the information to the CRA.

Tell the CRA, in writing, what information you believe is inaccurate. Keep a copy of all correspondence.

Some companies may promise to repair or fix your credit for an upfront fee--but there is no way to remove negative information in your credit report if it is accurate.

A medical history report is a summary of your medical conditions. Insurance companies use these reports to decide if they will offer you insurance. You have the right to get a copy of your report from MIB, the company that manages and owns the reporting database.

Sources of Information for a Medical History Report

If you reported a medical condition on an insurance application, the insurer may want to report it to MIB. An insurer can only share your medical condition with MIB if you give written permission. If you do give permission, the condition will be included in your medical history report.

Your medical history report does not include your complete medical records. Doctors, hospitals, pharmacies, and other health professionals can’t submit information to MIB. The report won’t include every diagnosis, blood test, or a list of your medicines.

A piece of information stays on your report for seven years. Your report can only be updated when you apply for an insurance policy with an MIB-member company, and give them permission to submit your medical conditions to MIB.

How Insurers Use Medical History Reports

When you apply for insurance, the insurer may ask for permission to review your medical history report. An insurance company can only access your report if you give them permission. The report contains the information you included in past insurance applications. Insurers read these reports before they'll approve applications for:

life

health

long-term

critical illness, or

disability insurance applications.

Request Your Free Medical History Report

You have the right to get one free copy of your medical history report, also known as your MIB consumer file, each year. You can request a copy for:

Yourself

Your minor child

Someone else, as a legal guardian

Someone else, as an agent under power of attorney

You can request a medical history report online from MIB or by phone at 1-866-692-6901.

Not everyone has a medical history report. Even if you currently have an insurance plan, you won't have a report if:

You haven't applied for insurance within the last seven years

Your insurance policy is through a group or employer policy

The insurance company isn’t a member of MIB

You didn’t give an insurer permission to submit your medical reports to MIB

Medical ID Reports and Scams

Use your medical history report to detect if you are a victim of medical ID theft. You may be a victim if there is a report in your name, but you haven't applied for insurance in the last seven years. Another sign of medical ID theft is if your report includes illnesses that you don't have.

File a Dispute

Review your report to verify that it only includes medical conditions that you have. Request a re-investigation if your report is incorrect. Email your dispute to infoline@mib.com or write: