Understand how to close the deal

By

now you’ve negotiated for your auto and chosen a loan and lender. But there’s still

a lot of paperwork to go over and sign. Before you drive off, make sure everything

matches what you agreed to when negotiating.

Decisions to make at this step

- Does this loan work for my budget?

- Does this match what I agreed to?

- Am I comfortable with this deal?

- Did the lender sign all the paperwork?

Actions to take

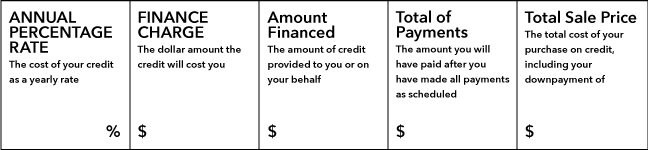

Once you have finalized the negotiations, review all of the paperwork before signing the loan documents. The federal Truth in Lending Act (TILA) requires lenders to give you specific disclosures in writing about important terms before you are legally obligated under the loan. One purpose of TILA is to help consumers make apples-to-apples comparisons between loans. The important terms include:

- Annual

Percentage Rate: the APR is the cost of credit expressed as a yearly rate

in a percentage.

- Finance

Charge: cost of credit expressed as a dollar amount (this is the total amount

of interest and certain fees you will pay over the life of the loan if you make

every payment when due).

- Amount

Financed: the dollar amount of credit provided to you (this is normally the

amount you are borrowing).

- Total

of Payments: the sum of all the payments that you will have made at the end of

the loan (this includes repayment of the principal amount of the loan plus all

of the finance charges).

The TILA disclosure will also include other important terms such as the number of payments, the monthly payment, late fees, whether the loan has a fixed or variable rate, and whether you can prepay your loan without a penalty.

Take the time to review the details of your auto loan, and look over the paperwork. If there are things you don’t understand, ask questions. You are signing a contract and this is a major purchase, it is important that you understand what you are signing.