Enforcement of Tax Laws

Internal Revenue Service (IRS) enforcement of the tax laws helps fund the U.S. government. IRS enforcement collects revenue from noncompliant taxpayers and, perhaps more importantly, promotes voluntary compliance by giving taxpayers confidence that others are paying their fair share. IRS last estimated (in 2012) that the gross tax gap—the difference between taxes owed and taxes paid on time—was $450 billion for tax year 2006. For a portion of the gap, IRS is able to identify the responsible taxpayers. The agency has estimated (in 2012) that it will collect $65 billion from these taxpayers through enforcement actions and late payments, leaving a net tax gap of $385 billion for tax year 2006.

Given current and emerging risks, we are expanding the enforcement of tax laws high-risk area to include IRS’s efforts to address tax refund fraud due to identity theft (IDT), which occurs when an identity thief files a fraudulent tax return using a legitimate taxpayer’s identifying information and claims a refund. While acknowledging that the numbers are uncertain, IRS estimated paying about $5.8 billion in fraudulent IDT refunds while preventing $24.2 billion during the 2013 tax filing season.

Since 2010, IRS’s budget has been reduced by about 10 percent, and IRS enforcement performance and staffing levels have declined.

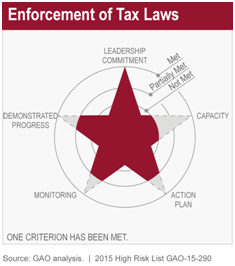

IRS has demonstrated leadership commitment toward addressing the tax gap. For example, IRS continues to research taxpayer noncompliance to better target taxpayer examinations. However, significant capacity challenges—such as reduced staffing and examination coverage in an environment of constrained budgets—and incomplete monitoring of enforcement program performance progress need to be addressed. Over the next two years, we will also assess IRS’s progress in addressing IDT refund fraud against the High Risk List criteria. We will report this information in the 2017 High Risk Update.

IRS has met the criterion of demonstrating a strong commitment to, and top leadership support for, improving tax compliance and addressing the tax gap. Some steps IRS has taken include the following:

- Continuing to research the extent and causes of taxpayer noncompliance and using the results to revise examination programs. We have consistently stressed the importance of IRS conducting tax compliance research.

- Extending a program to encourage taxpayers to voluntarily report their previously undisclosed foreign accounts and assets. IRS has collected over $6 billion since this program was initiated, and has implemented some of our recommendations on better managing the program.

- Implementing provisions from the Foreign Account Tax Compliance Act (FATCA). Under FATCA, U.S. financial institutions and other entities are required to withhold a portion of certain payments made to foreign financial institutions, if those institutions have not entered into an agreement with IRS to report U.S. account holders’ details to IRS. IRS has implemented some of our recommendations aimed at improving FATCA implementation.

However, IRS’s ability to implement these and other initiatives (such as those required by the Patient Protection and Affordable Care Act) and carry out ongoing enforcement programs could be challenged under an uncertain budgetary environment. As a result, IRS does not meet the criterion of having the capacity to demonstrate progress toward improving compliance and addressing the tax gap. From fiscal year 2010 to fiscal year 2015, IRS’s budget declined by about 10 percent (about $1.2 billion). Likewise, staffing has declined: the number of full time equivalents provided for in the enacted fiscal year 2014 budget represented a decrease of 11 percent compared to actual full time equivalents in fiscal year 2010. Amidst such reductions, IRS’s enforcement performance has declined, and IRS officials expect continued decline in fiscal year 2015. For example, IRS’s expects a decline of 20 percent in the individual examination rate in fiscal year 2015 compared to its original target for 2014. Also, IRS has reduced or eliminated services, slowed information systems modernization projects, and substantially reduced employee training.

IRS partially meets the criterion for having a corrective action plan to improve tax compliance and address the tax gap. Specifically, IRS has a high level strategic plan that discusses general approaches to make voluntary compliance easier for taxpayers and to ensure taxes owed are paid. However, in some areas, the plan does not include specific tactics for improving compliance, particularly in an environment of resource challenges. We have identified several areas that could help IRS improve its corrective action plan, including the following:

- Better measure return on investment. IRS’s declining budget environment and increased workload demands underscore the importance of IRS maximizing its resources in fulfilling its mission. Further refining of direct revenue return-on-investment (ROI) measures of its enforcement programs could improve how IRS allocates resources across its programs. In 2012, we made various recommendations advising IRS to make better use of ROI measures, subject to other considerations of tax administration, such as minimizing compliance costs and ensuring equitable treatment across different groups of taxpayers. IRS is taking steps to implement the recommendations.

- Better leverage automated processes. Taking greater advantage of automated processes could enhance some IRS enforcement programs. For example, IRS does not routinely match the K-1 information return—on which partnerships and S corporations report income distributed to partners or shareholders—to income information on tax returns for partners and shareholders that are themselves partnerships and S corporations. Matching such information might provide another tool for detecting noncompliance by these types of entities. In 2014, we recommended that IRS test the feasibility of such matching. IRS stated it would consider studying such testing if resources become available, but in the interim would not implement the recommendation. Likewise, continuing to enhance automated taxpayer services, such as web services, could result in lower-cost methods of interacting with taxpayers. In 2013, we made various recommendations for IRS to improve web services provided to taxpayers; IRS is taking steps to implement the recommendations.

- Improve enforcement data. More complete enforcement data could help IRS better allocate resources across programs. For example, IRS has limited information about the extent and nature of income misreporting by partnerships and S corporations, as well as about the effectiveness of its examinations in detecting such misreporting. Likewise, IRS does not separately track results of large partnerships examinations. Without such information, IRS cannot make fully-informed decisions about allocating resources to examining such entities. In 2013, we recommended IRS transcribe additional data from paper-filed individual tax returns (for example, on business income) to potentially improve how IRS determines whether to examine an individual tax return, which tax issues on the return should be examined, and what examination techniques should be used. IRS agreed to study the possible benefits of such transcription. In 2014, we made various recommendations on improving enforcement data related to partnerships and S corporations. IRS agreed with the recommendations, but said its ability to fully implement them depends on funding considerations.

IRS partially meets the criterion of having a program to monitor corrective measures. As previously mentioned, IRS continues to research the extent of taxpayer noncompliance, and periodically estimates the voluntary compliance rate—the amount of tax for a given year that is paid on time. However, IRS does not adequately measure the impact of some specific compliance programs, such as the following:

- Correspondence examinations. IRS does not have information to determine how its program of examining tax returns via correspondence affects the agency’s broader strategic goals for compliance, taxpayer burden, and cost. Thus, it is not possible to tell whether the program is performing better or worse from one year to the next. In 2014, we made several recommendations related to monitoring program performance; IRS plans to take action on these recommendations.

- Compliance Assurance Process. IRS does not fully assess the savings it achieves through its Compliance Assurance Process (CAP)—through which large corporate taxpayers and IRS agree on how to report tax issues before tax returns are filed. In 2013, we recommended that IRS track savings from CAP and develop a plan for reinvesting any savings to help insure the program is meeting its goals. Although IRS has taken steps to track savings by analyzing and comparing the workload inventory of account coordinators who handle CAP cases against team coordinators who handle non-CAP cases, it did not show how such a workload comparison proved savings from CAP. Nor has IRS developed a plan for reinvesting any savings. Without a plan for tracking savings and using the savings to increase audit coverage, IRS cannot be assured that the savings are effectively invested in either CAP or non-CAP taxpayers with high compliance risk.

IRS has partially met the criterion of demonstrating progress in implementing corrective measures to improve compliance and reduce the tax gap. For example, as previously mentioned, IRS has collected more than $6 billion through its program to encourage taxpayers to voluntarily report their previously undisclosed foreign accounts and assets. However, for some initiatives, such as those related to FATCA, it is either too soon to measure results or IRS has not been able to demonstrate an effect on the tax gap.

Given that the tax gap has been a persistent issue, demonstrating progress toward reducing it may require targeted legislative actions, including the following:

- Math error authority. IRS has statutory authority—called math error authority—to correct certain errors, such as calculation mistakes or omitted or inconsistent entries, during tax return processing. Expanding such math error authority—which at various times we have suggested Congress consider—could help IRS correct additional errors before interest is owed by taxpayers and avoid burdensome audits.

- Enhanced electronic filing. Requiring additional taxpayers to electronically file tax and information returns could help IRS improve compliance in a resource-efficient way. For example, in 2014, we suggested Congress consider expanding the mandate for partnerships and corporations to electronically file their tax returns, as this could help IRS reduce return processing costs, select the most productive tax returns to examine, and examine fewer compliant taxpayers.

- Additional information reporting. Taxpayers are much more likely to report their income accurately when the income is also reported to IRS by a third party. By matching information received from third-party payers with what payees report on their tax returns, IRS can detect income underreporting, including the failure to file a tax return. Currently, businesses must report payments for services made to unincorporated persons or businesses to IRS, but payments to corporations generally do not have to be reported. Taxpayers who rent out real estate are required to report expense payments for certain services to IRS, such as payments for property repairs, only if their rental activity is considered a trade or business. In 2008 and 2009, we suggested Congress consider expanding information reporting in these areas to increase payee reporting compliance. In 2010, the Joint Committee on Taxation estimated revenue increases for a 10-year period from third-party reporting of (1) rental real estate service payments to be $2.5 billion, and (2) service payments to corporations to be $3.4 billion.

- Paid preparer regulation. Establishing requirements for paid tax return preparers could improve the accuracy of the tax returns they prepare. Given that they prepare approximately 60 percent of all tax returns filed, paid preparers have an enormous impact on IRS’s ability to administer tax laws effectively. In limited studies, we found that some preparers have made significant errors. Based in part on our recommendation, in 2010, IRS initiated steps to regulate unenrolled preparers—those generally not subject to IRS regulation—through testing and education requirements; however, the courts ruled that IRS lacked such regulation authority. Although IRS has begun a voluntary program to recognize unenrolled preparers who complete continuing education and testing requirements, mandating these requirements could have a greater impact on tax compliance. In 2014, we suggested Congress consider granting IRS the authority to regulate paid tax preparers, if it agrees that significant paid preparer errors exist.

- Tax reform and simplification. A broader opportunity to address the tax gap involves simplifying the Internal Revenue Code, as complexity can cause taxpayer confusion and provide opportunities to hide willful noncompliance. Fundamental tax reform could result in a smaller tax gap if the new system has fewer tax preferences or complex tax code provisions; such reform could reduce IRS’s enforcement challenges and increase public confidence in the fairness of the tax system. Short of fundamental reform, targeted simplification opportunities exist. For example, changing tax laws to include more consistent definitions across tax provisions, such as which higher education expenses qualify for some of the savings and tax credit provisions in the tax code, could help taxpayers more easily understand and comply with their obligations.

Enforcement of Tax Laws: Refund Fraud Related to Identity Theft

IRS has taken steps to address IDT refund fraud, such as recognizing the challenge of IDT refund fraud in its most recent strategic plan, allocating more than 3,000 employees to combat IDT refund fraud, and creating automated fraud filters to detect IDT and prevent fraudulent refunds. However, IDT refund fraud remains a persistent and evolving threat; IRS must do more to address the problem, or the risk of issuing fraudulent IDT refunds could grow.

While there are no simple solutions to combating IDT refund fraud, we have identified various options that could help, some of which would require legislative action. Because some of these options represent a significant change to the tax system that could likely burden taxpayers and impose significant costs to IRS for systems changes, it is important for IRS to assess the relative costs and benefits of the options. This assessment will help ensure an informed discussion among IRS and relevant stakeholders—including Congress—on the best option (or set of options) for preventing IDT refund fraud.

- Accelerate W-2 deadlines. Currently, wage information that employers report on Form W-2 (Wage and Tax Statement) is not available to IRS until after it issues most refunds. If IRS had access to W-2 data earlier, it could match such information to taxpayers’ returns and identify discrepancies before issuing billions of dollars of fraudulent refunds. The Department of the Treasury (Treasury) has proposed that Congress accelerate W-2 deadlines to January 31. However, IRS has not fully assessed the impacts of this proposal, which could involve challenges such as a potential increase in W-2s that need to be corrected, required upgrades to IRS’s information technology systems, and logistical challenges for the Social Security Administration (which processes W-2 data before transmitting it to IRS). Further, we found that pre-refund W-2 matching may require other policy changes, such as delaying refunds and the start of the filing season. In 2014, we recommended that IRS fully study the costs and benefits of accelerating W-2 deadlines and determine what other policy changes are needed; in November 2014, IRS reported that it had convened an internal working group to address our recommendations and that it anticipated implementing our recommendation by July 2015.

- Increase electronic filing of W-2s. Increased electronic filing would allow IRS to obtain timely, accurate data from a significant number of additional employers and could further enhance the benefits IRS could obtain from the accelerated W-2 deadline and pre-refund W-2 matching. Treasury has requested authority to reduce the current, 250-return threshold for employers electronically filing information returns. In 2014, we suggested that Congress consider providing Treasury with the regulatory authority to lower the threshold for electronic filing of W-2s from 250 returns annually to between 5 to 10 returns, as appropriate.

- Improve third-party partnership programs. IRS collaborates with financial institutions and other third parties to obtain valuable information about emerging IDT refund trends and fraudulent returns that have passed through IRS detection systems. However, IRS provides limited feedback on IDT refund leads that third parties submit, and offers limited general information on IDT refund fraud trends. As a result, third parties do not know if the leads they provide to IRS are useful. In 2014, we recommended that IRS provide information to third parties on the success of leads in identifying suspicious returns and emerging IDT trends. We also recommended that IRS develop metrics to track external leads by the submitting third party. According to IRS, the agency anticipates implementing our recommendations by November 2015.

Over the next two years, we will assess IRS’s progress in addressing IDT refund fraud against the High Risk List criteria and will report this information in the 2017 High Risk Update.

In order to make progress in enforcing tax laws, IRS should implement our open recommendations—such as those discussed above—related to having a corrective action plan and monitoring measures for improving tax compliance and addressing the tax gap. These actions should also help IRS gauge progress in improving compliance and addressing the gap. Congress should also consider the legislative options we have suggested, as discussed above, to help IRS achieve progress. Additionally, given the capacity constraints IRS has faced, and may continue to face, it should develop a long-term strategy to address operations amidst an uncertain budget environment. The ongoing debate about tax reform also provides opportunities to consider the effect of tax simplification on taxpayer compliance and the tax gap.

Similarly, with regard to IDT refund fraud, IRS should implement our open recommendations, discussed above, including those focused on assessing the costs and benefits of the various options for combating IDT refund fraud. The legislative options discussed above—and that we suggest Congress consider—could also provide IRS with additional tools to combat IDT refund fraud.

GAO-15-163: Published: Dec 16, 2014. Publicly Released: Dec 16, 2014.

GAO-14-732: Published: Sep 18, 2014. Publicly Released: Sep 18, 2014.

GAO-14-633: Published: Aug 20, 2014. Publicly Released: Sep 22, 2014.

GAO-14-605: Published: Jun 12, 2014. Publicly Released: Jun 12, 2014.

GAO-14-479: Published: Jun 5, 2014. Publicly Released: Jul 7, 2014.

GAO-14-453: Published: May 14, 2014. Publicly Released: Jun 13, 2014.

GAO-14-467T: Published: Apr 8, 2014. Publicly Released: Apr 8, 2014.

GAO-13-662: Published: Aug 22, 2013. Publicly Released: Sep 23, 2013.

GAO-13-480: Published: May 24, 2013. Publicly Released: May 24, 2013.

GAO-13-318: Published: Mar 27, 2013. Publicly Released: Apr 26, 2013.

-

- James R. McTigue, Jr.

- Director, Strategic Issues

- mctiguej@gao.gov

- (202) 512-9110