Energy in Brief

What's changing in East Coast fuels markets?

Last Updated: July 27, 2012 with introductory text updated on January 18, 2013

The U.S. East Coast petroleum product market has been undergoing fundamental changes from the standpoint of supply and demand over the past several years. In 2011, three refineries were put up for sale with potential closure a likely outcome. One did close, the other two have new owners. Sources of feedstock are changing as crude oils from the midcontinent are being shipped by rail into the Mid Atlantic. A transition to ultra-low sulfur diesel for heating oil use began with New York in the summer of 2012, other states will soon follow. This article provides an overview of EIA's recent analyses related to East Coast fuels markets.

Several refineries supplying the East Coast to be sold or closed

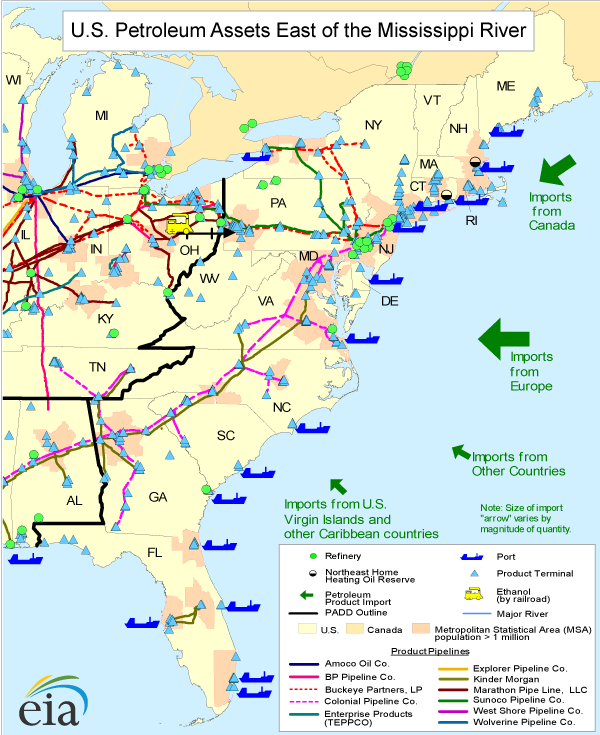

Since September 2011, two refineries in the Philadelphia area (ConocoPhillips' Trainer refinery and Sunoco's Marcus Hook refinery) and two major Caribbean export refineries supplying the East Coast (HOVENSA's U.S. Virgin Islands refinery and Valero's Aruba refinery) have or will soon close. In addition, Sunoco has announced plans to idle its remaining Philadelphia-area refinery (Sunoco Philadelphia) in July 2012 if no buyer is found. The three Philadelphia-area refineries (Trainer, Marcus Hook, and Philadelphia) taken together represented 50% of total East Coast refining capacity as of August 2011.

Refining capacity is available outside of the East Coast, but transportation constraints may hinder the delivery of refined petroleum products in the short term, especially into Pennsylvania and western New York, areas currently supplied by pipelines originating in the Philadelphia area refinery complex. Infrastructure changes will be necessary to accommodate the changing product flows.

If the Sunoco Philadelphia refinery closes, price impacts are highly uncertain. In the short term, prices could spike if areas are not adequately supplied. In the longer run, higher prices and possibly higher price volatility can result from longer supply chains.

Ultra-low sulfur diesel (ULSD) will be the most challenging product to replace as there are few alternative supply sources outside of the U.S. Gulf Coast. A number of states in the Northeast are slated to begin requiring ULSD for heating oil beginning with New York in July 2012. The current transition schedule accompanies this article. Connecticut does not appear on the schedule because its 2011 law required New York, Massachusetts, and Rhode Island to have similar requirements in order to trigger compliance, and the three states do not have ULSD requirements in place.

This article provides some key points and graphics from recent EIA reports and articles related to East Coast fuels markets. EIA has provided a review of these developments in two recent reports:

- A preliminary report, Reductions in Northeast Refining Activity: Potential Implications for Petroleum Product Markets, was released on December 23, 2011

- An expanded report, Potential Impacts of Reductions in Refinery Activity on Northeast Petroleum Product Markets, was released on February 27, 2012 and updated on May 11, 2012

- An addendum addressing the Jones Act was released on May 11, 2012

The situation is evolving, and EIA will continue to monitor it closely.

In addition to these two reports, a number of EIA articles focused on different facets of East Coast fuels markets. Some main points from these articles include:

- East Coast Gasoline Imports: Recent Trends and Developments — This reduction in refinery activity, if fully implemented and made permanent, looks set to reverse recent declines in U.S. gasoline imports even if end-user demand for gasoline continues to edge lower. See related article — This Week in Petroleum, January 19, 2012

- Diverging Trends in Regional Crude Acquisition Costs — The cost of crude oil is the largest factor in the cost of gasoline and diesel fuel, but not all refiners get to pick from the least expensive crudes. The East Coast refineries have the highest average cost of crude among U.S. refiners. See related article — This Week in Petroleum, January 25, 2012

- Midstream Makeover — Changing market dynamics could significantly alter the web of pipelines, storage tanks, and terminal facilities on which the oil industry and the nation depend to link supply centers and end-users. See related article — This Week in Petroleum, February 15, 2012

- The HOVENSA Refinery Closure — The closure of HOVENSA, a major refinery and the largest employer in the U.S. Virgin Islands, is another in a string of Atlantic Basin refinery closures over the past several years. See related article — This Week in Petroleum, February 23, 2012

- Adding Barges Still Leaves Concerns — EIA's updated report (#2 above) mentioned 56 Jones Act tankers handling petroleum, including tankers being decommissioned. But the table did not show the many barges that are also used to transport petroleum in coastal waters. Updated information suggests that less than 40 tankers and perhaps as many as 270 coastal barges are in operation. See full article — This Week in Petroleum, April 4, 2012

- U.S. Imports of Nigerian Crude Oil Continue to Decline — The trend of declining crude oil imports into the United States continued in the first month of 2012. There has been a particularly sharp decline in imports from Nigeria due to the idling in late 2011 of two refineries on the East Coast, which were significant buyers of Nigerian crude, and reduced imports by refiners on the Gulf Coast. See full article — Today in Energy, April 10, 2012

- Buyer of Trainer Refinery Plans to Increase Jet Fuel Yield — Delta Air Lines recently purchased the Trainer refinery, which is located in the Philadelphia area and had been idle since the fourth quarter of 2011. In a Securities and Exchange Commission (SEC) regulatory (8K) filing, Delta Air Lines indicated that it plans to increase Trainer's jet fuel yield to 32%, higher than was previously seen at Trainer and significantly above the average yield of jet fuel in any U.S. refining region. See full article — Today in Energy, June 12, 2012

- Update of the Status of East Coast Refineries — Concerns regarding the supply of refined products on the U.S. East Coast have eased considerably in recent months, reflecting both an improved outlook for regional refining activity and success in meeting logistical challenges. See related article — This Week in Petroleum, July 25, 2012

Learn More

Did You Know?

Distillate fuel oil includes diesel fuels classified based on the sulfur composition:

Ultra-low sulfur diesel (ULSD) less than 15 parts per million (ppm) sulfur used mostly in on-highway vehicles.

Higher Sulfur (Non-ULSD) Distillate (more than 15 ppm sulfur) including No. 2 distillate heating oil (dyed red); used in residential and commercial heating systems, industrial, and power generation applications, waterborne and rail transportation, and off-highway.

| Year | Heating Oil Transition to ULSD in the Northeast |

|---|---|

| 2012 | New York ULSD required |

| 2014 | Massachusetts 1st phase <500 ppm sulfur |

| New Jersey 1st phase <500 ppm sulfur |

|

| Vermont 1st phase <500 ppm sulfur |

|

| 2016 | Maine 1st phase <500 ppm sulfur |

| New Jersey 2nd phase ULSD required |

|

| 2018 | Maine 2nd phase ULSD required |

| Massachusetts 1st phase <500 ppm sulfur |

|

| Vermont 2nd phase ULSD required |