The fiscal cliff is done. But the era of cliffs has just begun.

Last night, the House of Representatives signed off on a deal to avert the massive tax hikes and spending cuts known, nearly posthumously, as the "fiscal cliff." Today we are a presidential signature away from the official end of this absurd national nightmare. But did the president make a bad deal? Did he make a secretly ingenious deal? What's in it, anyway? Those are questions. These are our answers ...

What's in the fiscal cliff deal?

The Tweet-length version of this deal is: No more payroll tax holiday, higher taxes for the super-rich, and we'll figure out the rest later.

The centerpiece of the deal is an increase in the top marginal rate to 39.6 percent on all income over $400,000 (for individuals) and $450,000 (for families). It is the first major tax increase since the early 1990s. The other rates from the Bush tax cuts are made permanent. Here's how it changes our taxes.

The end of the payroll tax holiday will reduce take-home pay for lower-income families by hundreds of dollars. But the tax changes at the top are measured in the hundreds of thousands of dollars.

Also in taxes: the Alternative Minimum Tax is permanently "fixed"; high-earners will pay 20 percent on income from capital gains and dividends; high earners will be privy to fewer deductions and exemptions; the estate tax is trimmed; and more. Crucially for the jobless, unemployment insurance is extended for the rest of the year.

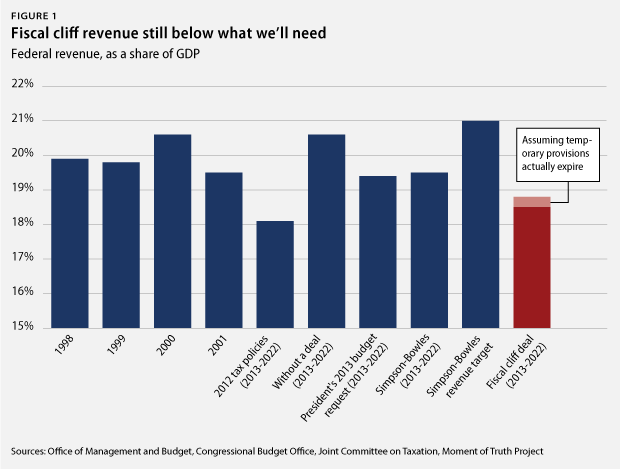

What's not in the deal is just as important: payroll taxes, spending cuts, and the debt limit. The payroll tax holiday is officially over. That means payroll taxes will rise by 2 percentage points on all workers. There are no spending cuts in the fiscal cliff deal. But there is also no guarantee to raise the debt limit, in the next two months. Republicans want to use the debt limit debate for force spending cuts. President Obama has repeatedly promised not to negotiate over the debt limit, since failing to raise it could trigger a financial crisis.

What's the best reason for us to like it?

Deficits won't kill the U.S. economy in 2013. But austerity might. In a weak economy, we want taxes low and short-term deficits high. This deal preserves both.

Don't think of the U.S. as having "a deficit crisis." That's too simple. Think of us as having three deficit challenges. In the short term, we need high deficits to support weak growth. In the medium term, we need higher revenue and slightly less spending. In the long term, we need to make health care more affordable -- not just for the government, but for everybody.

This deal doesn't fix our health care problem, but that's a multi-decade problem that we don't have to "fix" (as if we even could) in January 2013. This deal doesn't raise taxes as much as we ultimately need to, nor does it touch spending, but that's okay for now, because those are medium-term goals. In the short term, we need more jobs, more spending, more economic activity, especially around housing. High deficits can't save an economy. But austerity can strangle it.

What's the best reason to hate it?

The fiscal cliff was a triple-whammy: taxes, spending, and the debt limit. This deal resolves the first, and most pressing issue, which was the threat of rising taxes on every family in a weak economy. But the deal doesn't solve the other two whammies: the automatic spending cuts passed in the Budget Control Act of 2011 (aka: the sequester) and the debt ceiling. We punted both of those debates by two months.

The Media Metaphor Committee hasn't yet settled on a scary-and-not-even-really-accurate topographical analogy for these debates, but ... I don't know, Budget Mountain? Debt Valley? I'll get back to you tomorrow. The upshot is that the era of perpetual crisis in Washington is far from over.

I heard that this bill increases our deficits by $3.9 trillion in the next ten years. Is that true?

Sort of, but that's really the wrong way to think about it.

The

fiscal cliff deal raises taxes by about $600 billion in the next ten

years compared to an extension of 2012 tax policy. But if Congress had

done nothing to avert the fiscal cliff, the Bush/Obama tax cuts would

have expired and taxes would have gone up on everybody dramatically,

sucking the economy into a short, sharp recession. Compared to that tax hike, this deal reduces revenue (or increases the deficit) by nearly $4

trillion. So the folks saying this deal increases the deficit by $4

trillion are sort of right. But they're comparing this deal to an

alternate reality that was always utterly inconceivable.

What did the GOP win/lose?

The GOP wins the permanent extension of 80% of the Bush tax cuts. They lose (potentially) the leverage to force cuts to spending -- in particular, to entitlements -- this year.

What did the Democrats win/lose?

The Democrats win the first major tax increase in 20 years without trading spending cuts or entitlement changes. They lose hundreds of billions in revenue from the president's initial (and seemingly non-negotiable) offer to raise taxes. They also lost the opportunity to take the debt ceiling off the table. Obama says he won't negotiate over the debt ceiling. But liberals should be forgiven if they suspect the president is incapable of not negotiating.

What did deficit hawks win/lose?

They won the first bipartisan plan to raise revenue over current policy in two decades. But they lost the grand bargain.

If you had to give the deal a grade, what would you give it?

B-minus. The deal isn't bad, just incomplete. It fulfills two-thirds of a campaign promise to raise taxes, but it opens the door to more showdowns over the budget. It preserves tall deficits now, but doesn't aim for the ultimate grand bargain: trading long-term deficit reduction for short-term stimulus.

More »

Four long years after his first presidential oath of office, Barack Obama's second term begins in an uncomfortably familiar place. The U.S. unemployment rate is 7.8 percent, according to this morning's BLS report, the exact same number as on that cold, historic day in January 2009.

Four long years after his first presidential oath of office, Barack Obama's second term begins in an uncomfortably familiar place. The U.S. unemployment rate is 7.8 percent, according to this morning's BLS report, the exact same number as on that cold, historic day in January 2009.

5. Not just for the old. Most benefits are spent on the elderly, through Social Security and Medicare, and nearly every household with an adult over 65 receives federal benefits of some kind. But perhaps the most common benefit available -- unemployment benefits -- can help Americans as young as teenagers. From the report: "The use of entitlement begins at an early age for many Americans, the survey finds. A third (33%) of all adults ages 18 to 29 say they have received at least one major entitlement payment or service in their lives."

5. Not just for the old. Most benefits are spent on the elderly, through Social Security and Medicare, and nearly every household with an adult over 65 receives federal benefits of some kind. But perhaps the most common benefit available -- unemployment benefits -- can help Americans as young as teenagers. From the report: "The use of entitlement begins at an early age for many Americans, the survey finds. A third (33%) of all adults ages 18 to 29 say they have received at least one major entitlement payment or service in their lives."