We expect the economy to grow moderately for the remainder of 2012 and over the following two years. Taking into account incoming data and the additional monetary stimulus, we anticipate that gross domestic product will expand about 2.5% in 2013 and 3.3% in 2014. — Sylvain Leduc » Read more in FedViews • October 11 Is China Due for a Slowdown? • FRBSF Economic Letter 2012-31 Many analysts have predicted that a Chinese economic slowdown is inevitable because the country is approaching the per capita income at which growth in other countries began to decelerate. However, China may escape such a slowdown because of its uneven development. An analysis based on episodes of rapid expansion in four other Asian countries suggests that growth in China’s more developed provinces may slow to 5.5% by the close of the decade. But growth in the country’s less-developed provinces is expected to run at a robust 7.5% pace. Malkin • Spiegel • October 15, 2012 District Trends Beige Book • October 10, 2012 Economic activity grew at a modest pace. Upward price pressures remained limited overall, and upward wage pressures remained muted. » Summary • 12th District • Full report 12L Economic Trends • September 2012 (pdf, 511kb) ETC: Economic Trends & Conditions • September 2012 (pdf, 136kb) |

Improving Fed Transparency Opening the Temple: An Essay by President and CEO John C. Williams Recent FOMC Communications Initiatives

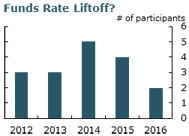

On January 25, the FOMC took two important steps to improve transparency about monetary policy in the U.S. First, the FOMC provided a statement that outlines its longer-run goals and monetary policy strategy. Second, the FOMC provided guidance about its expectations for future monetary policy in the form of quantitative projections of the federal funds rate. New in Research In the News China’s Advantage of Backwardness • by Bob Davis, Real Time Economics, WSJ blog • October 17, 2012 "China will slow over the coming years, but not as much as many predict, write Israel Malkin and Mark Spiegel, because of much of the country is so lightly developed that growth there will continue to speed along. “There is an advantage to backwardness, in the sense that a poorer region or nation has a lot of catching up to do before it prices itself out of certain activities,” said Mr. Spiegel." » Read more in "Is China Due for a Slowdown" • Malkin • Spiegel Norway’s Housing Boom Could Lead to Spain-Style Bust, Say Some • by Holly Ellyatt, CNBC • October 17, 2012 "Norway's house price rise has been so dramatic that the Federal Reserve Bank of San Francisco wrote a paper on the subject in June that made parallels between the lead up to the U.S. housing crisis and the “irrationally exuberant bubble” of Norway’s present boom." » Read more in "Housing Bubbles and Homeownership Returns" • Jurgilas • Lansing Fed's Williams: Fed Actions Will Improve Growth • by Michael Derby and Ian Sherr, WSJ Online • October 16, 2012 "The "strong measures" taken by the Federal Reserve at its September meeting should spur better levels of growth in the U.S. economy, a key central bank official said Monday." » Read more in "The Economy, Fiscal Policy, and Monetary Policy" • Williams Give Us a Brake: When Fiscal Policy Is in Chaos, Companies Cannot Plan for the Future” • taken from The Economist • October 6, 2012 "Uncertainty about future economic conditions has added at least a percentage point to the unemployment rate, according to Sylvain Leduc and Zheng Liu of the Federal Reserve Bank of San Francisco." » Read more in "Uncertainty, Unemployment, and Inflation" • Leduc • Liu Housing Supply and Foreclosures • Working paper 2012-20 TWe explore the role of foreclosure inventories in a model of housing supply. The foreclosure variable is necessary to account for the steep and sustained drop in new construction activity following the U.S. housing market bust beginning in 2006. There is modest evidence that local banking conditions play a role in determining housing starts. Even with state-level foreclosures and banking variables in the model, there is a sizeable post-2006 residual common to all states. We argue that, in addition to observable macro and local factors, housing starts in the Great Recession have been weighed down in part by aggregate uncertainty factors. Hedberg • Krainer • September 2012 Upcoming Seminars Seminar (Finance) • Annette Vissing-Jorgensen (Northwestern Kellogg) • October 1 Seminar (Macro) • Karl Walentin (Sveriges Riksbank) • October 2 Seminar (Finance) • Seth Pruitt (Board) • October 9 Seminar (Finance) • Wayne Passmore (Board) • October 10 Seminar (International) • Assaf Razin (Cornell) • October 12

Research Centers |