Economic Indicator: Growth Has Been In Store (and Online) for Much of Retail

Monday, July 16th, the Census Bureau will release its June advance estimates of retail sales. Current consensus expectations are for sales to tick up following two months of declines. When the data come out, many of us will jump right to the figures for general merchandise stores. Indeed, when we hear the word “retail,” our local department store may come to mind. About 3 million, or 1 in 5, retail jobs are in general merchandise stores. And with monthly sales of around $52 million, this retail sector is on par with food and beverage stores as the second largest retail segment. (Motor vehicle car dealers tops the list.)

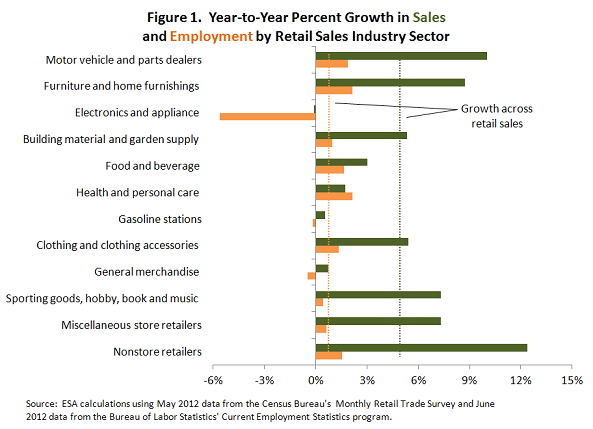

Currently, a number of retail segments are posting solid sales gains as well as adding back jobs. (See Figure 1.) Leading the way is “non-store retailers,” reflecting the continuing surge in online spending. Sales in electronic shopping and mail-order houses have been climbing about 14 percent year over year—a blistering pace. (Earlier this year, I bought a garbage disposal at a major online retailer—something that would have seemed absurd to me not long ago.)

Given the resurgence of the U.S. automotive sector, it is not surprising to see the strong growth in motor vehicle and parts sales. The ongoing recovery in this sector has meant the return of thousands of production workers to the factory line, with 62,000 jobs added in just past year. Dealers also have been bringing back jobs: 32,000 over the past year. My own car has 215,000 miles; it may be time to consider a visit to one of these dealers.

In addition, the improving state of the housing recovery is reflected in the upswing, particularly in furniture and home furnishings: sales are up more than 8 percent over the year, and this sector has added about 9,000 jobs. Thus, while general merchandise stores, particularly traditional and discount department stores, have been struggling somewhat, overall the retail sector has many areas of strength.

The current situation for general merchandise stores is less sanguine. But before digging deeper into these trends, it is worthwhile to define what we mean by a “general merchandise store.” As a frequent shopper and a new member of our nearby warehouse club, I feel that it is my duty to point out that “general merchandise stores” is actually a rather diverse retail grouping. It is divided into four major categories:

- conventional department store

- discount department stores

- warehouse clubs and super stores

- all other general merchandise stores.

The distribution of sales across these categories has shifted massively over the past decade, with the share of sales going to warehouse clubs and super stores doubling from 31 percent to 62 percent. (See Figure 2.) This shift is due to a 229-percent increase in nominal sales combined with a 33-percent drop in sales at conventional department stores and 10-percent drop at discount department stores. Some of the latter decline may reflect store conversions to super stores

In terms of employment and sales, 2012 has been a less than robust year for general merchandise stores, but as we have seen, this actually belies overall strength in the retail sector. So while employment in June declined by 11,500 jobs, and over the year both employment and sales have been flat, the trends for general merchandise stores appear to be more the exception than the rule. A closer look across retail uncovers many segments that are experiencing considerable growth in sales with a commensurate growth in their sales force.

In sum, much of the retail sector is contributing steadily to growth in sales and employment. We hope to see this trend continue with Monday’s report and in coming months. I, for one, will get online right away to check out new cars… after I get home from work.

David Langdon

Economist

Office of the Chief Economist

Economics and Statistics Administration

U.S. Department of Commerce