Short-Term Energy Outlook

Release Date: September 11, 2012 | Next Release Date: October 10, 2012 | Full Report | Text Only | All Tables | All Figures

Natural Gas

U.S. Natural Gas Consumption

EIA expects that natural gas consumption will average 69.8 billion cubic feet per day (Bcf/d) in 2012, an increase of 3.2 Bcf/d (4.8 percent) from 2011. Large gains in electric power use in 2012 more than offset declines in residential and commercial use. Projected consumption of natural gas in the electric power sector averages 25.2 Bcf/d in 2012, 21 percent higher than in 2011, primarily driven by the improved relative cost advantages of natural gas over coal for power generation in some regions. Consumption in the electric power sector during 2012 peaks at 31.1 Bcf/d in the third quarter, when electricity demand for air conditioning is highest.

Total natural gas consumption increases by 0.2 Bcf/d (0.2 percent) in 2013. Expected increases in residential, commercial, and industrial consumption offset expected declines in the electric power sector. A forecast of near-normal weather during the upcoming winter drives 2013 increases in residential and commercial consumption of 9.9 percent and 9.3 percent, respectively. Although higher natural gas prices contribute to an 8.4 percent decline in forecast natural gas consumption in the electric power sector in 2013, consumption in the power sector next year is still expected to be about 2.3 Bcf/d higher than 2011 levels.

U.S. Natural Gas Production and Imports

Total marketed production of natural gas grew by 4.8 Bcf/d (7.9 percent) in 2011. This strong growth was driven in large part by increases in shale gas production. EIA expects continued year-over-year growth in 2012 of 2.6 Bcf/d. EIA, however, expects a small drop in production in the coming months, reflecting both losses from hurricanes (2012 Outlook for Hurricane-Related Production Outages in the Gulf of Mexico) and declines related to recent drops in the rig count. Hurricane Isaac hit the Gulf of Mexico on August 28 and has affected natural gas production for several days, with shut-ins in the Gulf of Mexico totaling 27.9 Bcf through September 10. According to Baker Hughes, the natural gas rig count was 452 as of September 7, 2012, compared with 811 at the start of 2012.

EIA forecasts that production growth will slow to 0.5 Bcf/d in 2013, as the slowdown in drilling activity is offset by growth in production from liquids-rich natural gas production areas such as the Eagle Ford and wet areas of the Marcellus Shale, and associated gas from the growth in domestic crude oil production.

EIA expects pipeline gross imports will fall by 0.1 Bcf/d (1.4 percent) in 2012, as domestic supply continues to displace Canadian sources. The warm winter in the United States early this year also added to the year-over-year decline in imports, particularly to the Northeast where imported natural gas can serve as additional supply in times of very cold weather. EIA expects little change in pipeline gross imports in 2013. Pipeline gross exports grew by 1.0 Bcf/d (33 percent) in 2011, driven by increased exports to Mexico, but are expected to remain flat in 2012, and grow by 0.1 Bcf/d in 2013.

Liquefied natural gas (LNG) imports are expected to fall by about one-half in 2012 from the year before. EIA expects that an average of about 0.4 Bcf/d will arrive in the United States (mainly at the Elba Island terminal in Georgia) both in 2012 and 2013, either to fulfill long-term contract obligations or to take advantage of temporarily high local prices due to cold snaps and disruptions. Higher prices for LNG, particularly in Asian markets, have made the United States a market of last resort for LNG suppliers.

U.S. Natural Gas Inventories

Working natural gas inventories remain at historically high levels for this time of year. As of August 31, 2012, according to EIA's Weekly Natural Gas Storage Report, working inventories totaled 3,402 Bcf, which is 395 Bcf greater than last year's level and 329 Bcf above the five-year average. EIA expects that inventory levels at the end of October 2012 will set a new record of 3,950 Bcf. Because of very high inventories at the start of the summer injection season this year, working inventories have remained high and stock builds since April, with a few exceptions, have been below the five-year average and below last year's levels. The projected increase of 1,473 Bcf in working gas inventory during the 2012 injection season (from the end of March to the end of October) would be the smallest build since 1991.

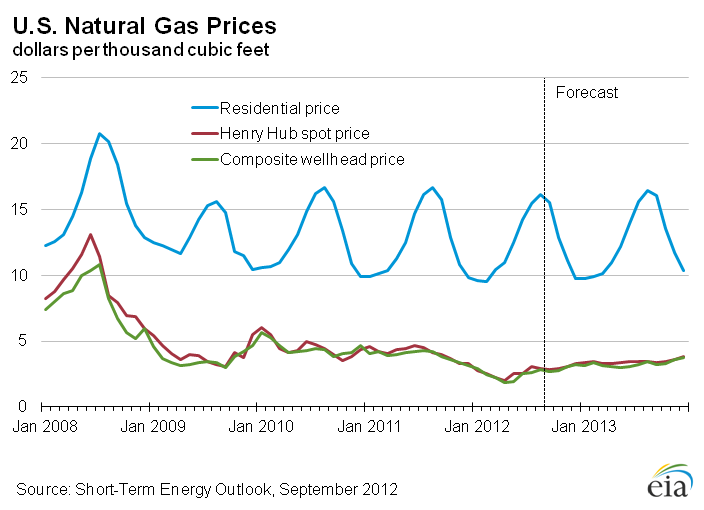

U.S. Natural Gas Prices

Natural gas spot prices averaged $2.84 per MMBtu at the Henry Hub in August 2012, down $0.11 per MMBtu from the July average and $1.21 per MMBtu (30 percent) lower than the August 2011 average. While abundant supplies have kept prices relatively low, a hot summer and associated increases in demand for natural gas for power generation contributed to the increase in prices in July. EIA expects the Henry Hub natural gas price will average $2.65 per MMBtu in 2012, with prices remaining below $3.00 per MMBtu until December. EIA expects 2013 prices will average $3.34 per MMBtu.

Natural gas futures prices for December 2012 delivery (for the five-day period ending September 6, 2012) averaged $3.20 per MMBtu, and the average implied volatility based on options and futures prices was 40 percent (Market Prices and Uncertainty Report). Current options and futures prices imply that market participants place the lower and upper bounds for the 95-percent confidence interval for December 2012 contracts at $2.20 per MMBtu and $4.65 per MMBtu, respectively. At this time last year, the December 2011 natural gas futures contract averaged $4.29 per MMBtu and implied volatility averaged 32 percent. The corresponding lower and upper limits of the 95-percent confidence interval were $3.18 per MMBtu and $6.21 per MMBtu.

| U.S. Natural Gas Summary | ||||

|---|---|---|---|---|

| 2010 | 2011 | 2012 projected | 2013 projected | |

| Prices | (dollars per thousand cubic feet) | |||

| Wellhead | 4.48 | 3.90 | 2.60 | 3.27 |

| Henry Hub Spot | 4.52 | 4.12 | 2.73 | 3.44 |

| Residential Sector | 11.37 | 11.01 | 10.90 | 11.09 |

| Commercial Sector | 9.41 | 8.92 | 8.40 | 8.95 |

| Industrial Sector | 5.49 | 5.11 | 3.91 | 4.58 |

| Supply | (billion cubic feet per day) | |||

| Marketed Production | 61.38 | 66.22 | 68.86 | 69.32 |

| Dry Gas Production | 58.44 | 63.01 | 65.38 | 65.84 |

| Pipeline Imports | 9.07 | 8.51 | 8.39 | 8.42 |

| LNG Imports | 1.18 | 0.96 | 0.45 | 0.45 |

| Consumption | (billion cubic feet per day) | |||

| Residential Sector | 13.12 | 12.96 | 12.00 | 13.19 |

| Commercial Sector | 8.50 | 8.67 | 8.07 | 8.83 |

| Industrial Sector | 17.86 | 18.40 | 18.56 | 18.84 |

| Electric Power Sector | 20.24 | 20.83 | 25.21 | 23.09 |

| Total Consumption | 65.14 | 66.60 | 69.79 | 69.96 |

| Primary Assumptions | (percent change from previous year) | |||

| Heating Degree-days | -0.6 | -3.4 | -10.2 | 14.2 |

| Cooling Degree-days | 17.2 | 2.0 | -0.8 | -12.9 |

| Commercial Employment | -0.1 | 1.8 | 1.9 | 1.8 |

| Natural-gas-weighted Industrial Production | 7.6 | 1.6 | 1.3 | 1.3 |

Interactive Data Viewers

Provides custom data views of historical and forecast data

STEO Custom Table Builder ›

Real Prices Viewer ›

| Related Tables | |||||||

|---|---|---|---|---|---|---|---|

| Table WF01. Average Consumer Prices and Expenditures for Heating Fuels During the Winter | |||||||

| Table 1. U.S. Energy Markets Summary | |||||||

| Table 2. U.S. Energy Prices | |||||||

| Table 5a. U.S. Natural Gas Supply, Consumption, and Inventories | |||||||

| Table 5b. U.S. Regional Natural Gas Prices | |||||||

| Table 8. U.S. Renewable Energy Consumption | |||||||

| Table 9a. U.S. Macroeconomic Indicators and CO2 Emissions | |||||||

| Table 9b. U.S. Regional Macroeconomic Data | |||||||

| Table 9c. U.S. Regional Weather Data | |||||||

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Related Articles | ||

|---|---|---|

| Today In Energy | Daily | |

| Natural Gas Weekly Update | Weekly | |

| Peak Underground Working Storage Capacity | Annual | |

| Change in STEO Regional and U.S. Degree Day Calculations | Sep-2012 | |

| 2012 Outlook for Hurricane-Related Production Outages in the Gulf of Mexico | Jun-2012 | |

| 2011-2012 Winter Fuels Outlook Slideshow | Oct-2011 | |

| Changes in Natural Gas Monthly Consumption Data Collection and the Short-Term Energy Outlook | Dec-2010 | |

| Trends in U.S. Residential Natural Gas Consumption | 23-Jun-2010 | |

| Probabilities of Possible Future Prices | Apr-2010 | |

| Energy Price Volatility and Forecast Uncertainty | Oct-2009 | |

| The Implications of Lower Natural Gas Prices for Electric Generators in the Southeast | May-2009 |