Industry CircularNumber: 80-11Date: November 28, 1980 |

Department of the TreasuryBureau of Alcohol, Tobacco, and FirearmsWashington, D.C. 20226 |

To download a PDF file, you must have Adobe Acrobat Reader software installed on your system. To download a free copy of Adobe Reader, click here. |

|||||

|

RECORDS COVERING RECEIPT AND USE OF TAX-FREE ALCOHOL Users of tax-free alcohol and others concerned: Purpose. The purpose of this industry circular is to inform you that Revenue Procedure 62-10 is modified and superseded by a new ATF procedure which will be published in a future quarterly issue of the Alcohol, Tobacco and Firearms Bulletin. The same information contained in Revenue Procedure 62-10 was also published in Industry Circular No. 61-4. The new procedure will read substantially as follows: Section 1. PURPOSE. The purpose of this ATF Procedure is to supply tax-free alcohol permittees with instructions and aids to assist them in the maintenance of records with respect to tax-free alcohol and to simplify the task of preparing annual reports on Form 1451 (5150.28), Report of Tax-Free Alcohol User. Most of the instructions and aids contained in this procedure originally appeared in Industry Circular No. 61-4, dated January 26, 1961, and in Revenue Procedure 62-10, C. B. 1962-1, 437 (Internal Revenue). The material originally contained in Industry Circular No. 61-4 and Revenue Procedure 62-10 is republished here in order to increase the availability of the material and to extend the conversion table which appeared in those publications so that the conversion table includes some metric equivalencies. Sec. 2. BACKGROUND. The Distribution and Use of Tax-Free Alcohol Regulations require that records be kept in suffi- cient detail to enable any internal revenue officer to verify all transactions and to ascertain that per- mittees have complied with the law and regulations. These regulations also require that the records be such as to enable permittees to prepare the annual report, Form 1451. Since figures reported on Form 1451 are to be in proof gallons, permittees are required to identify, on their records, the proof of all alcohol together with the actual quantities for each transaction. Regulations also require that permittees take an inventory at the close of each month and keep such inventory as a part of their records. Sec. 3. BASIC RECORD. .01 Alcohol Received. - The copy of the Form 1473, Shipment and Receipt Specially Denatured, Tax-Free, or Recovered Spirits, which permittees receive covering each shipment of tax-free alcohol will serve as the basic record of alcohol received. Permittees should make the proper notation on this copy (and on the original which is forwarded to the appropriate Regional Regulatory Administrator, ATF) of any losses in transit. The quantity reported on the Form 1473, minus any loss or deficiency in transit, is the quantity which must be reported on Form 1451 as "received." .02 Use of Alcohol. - Each time alcohol is with- drawn from the permittee's supply for any use, an entry should be made on his records, showing the quantity (liquid measure), the proof, and the purpose of removal. Permittees need not convert each sepa- rate quantity so removed to proof gallons unless so desired. Instead, they may total the quantity of alcohol of the same proof removed during the period of one calendar month, and then convert the figure representing the month's removals to total proof gallons removed. The resulting total, or combined total if there is alcohol of more than one proof, will be shown in column (e) of Form 1451 for that month. .03 Monthly Inventory. - At the close of each month, an inventory must be taken of all alcohol remaining in stock. First, the permittee must deter- mine the quantity remaining in each package or tank. If all of the alcohol is of the same proof, he must add these figures and convert the resulting figure to proof gallons. Where there is alcohol of different proofs in stock, the permittee must add the quantity for each proof separately, convert the total quantity for each proof to proof gallons and then total the proof gallons thus obtained. This is the total quan- tity, in proof gallons, on hand at the end of the month. .04 Losses or Gains. 1. After completing the above computations, the permittee will now have records showing all alco- hol received and used during the month and on hand at the end of the month. (This latter, of course, also becomes the quantity on hand at the beginning of the following month to be reported in column (b) for that month.) From these figures the permittee can deter- mine any gains or losses during the month, as follows: 2. Add the quantity received during the month to the quantity on hand at the beginning of the month, and subtract therefrom the quantities used during the month. If the resulting figure is less than the quantity determined from the inventory as on hand at the end of the month, the difference between the two figures represents a gain (Example A). If it is more than the quantity revealed by the inventory, it represents a loss (Example B).

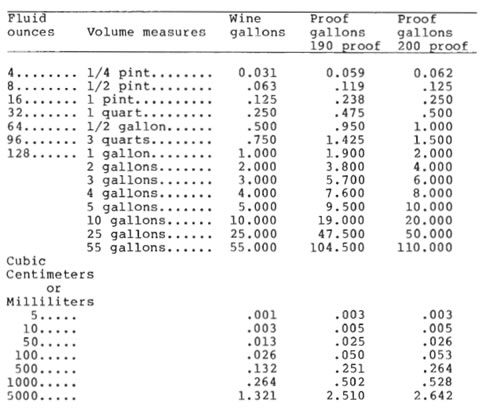

*The regulations require that permittees show in their records all losses by theft or casualty or other unusual losses and that entries covering these losses be made in their records at the time of such losses or when they are discovered. Therefore, these known losses must be taken into account in order to deter- mine any additional loss at the end of the month. However, all losses must be totaled and the combined figure (in the example--4 p.g.) entered in column (h) of Form 1451. .05 Recovered Alcohol or Alcohol Received from the General Services Administration. 1. Permittees receiving alcohol from the General Services Administration or recovering tax- free alcohol must account for such alcohol separately in their records and inventory and make separate entries on Form 1451, appropriately identified. If recovered alcohol is shipped to a distilled spirits plant for restoration, the approximate quantity thereof, in proof gallons, should be entered in column (e), followed by an asterisk, and an explanation of the entry should be shown elsewhere on the form, identifying the distilled spirits plant to which shipment was made. 2. While the above procedures do not cover every transaction, they demonstrate the type of records which can be kept to meet regulatory require- ments. The records must be in sufficient detail to show each transaction and to enable permittees to prepare Form 1451. Also, a record of the inventory taken at the close of each month, along with all other records, must be maintained for a period of three years from the date of the report on Form 1451 covering the transactions. Permittees should observe the instructions on the back of Form 1451 when making entries from their records to the form. .06 Conversion Table. 1. Use of the table below may prove helpful in converting volume measures to proof gallons for alcohol of 190 or 200 degrees of proof. Fluid Wine Proof Proof ounces Volume measures gallons gallons gallons 190 proof 200 proof

2. In computing proof gallons to the nearest tenth for entry to Form 1451, all fractional parts of five-hundredths or more shall be increased to the next tenth; for example, 4.275 proof gallons will be reported as 4.3 proof gallons. Fractional parts of less than five-hundredths shall be dropped; for example, 4.126 proof gallons will be reported as 4.1 proof gallons. Sec. 4. EFFECT ON OTHER DOCUMENTS. Revenue Procedure 62-10, C.B. 1962-1, 437 (Internal Revenue) is superseded. Sec. 5. INQUIRIES. Inquiries concerning this circular should refer to it by number and be addressed to the Assistant Director, Regulatory Enforcement, Bureau of Alcohol, Tobacco and Firearms, 1200 Pennsylvania Avenue, NW., Washington, DC 20226. Acting Director |

|||||