|

|

|

May 2007

This house was used in a Mortgage Fraud Scheme

Key Findings

Top Areas for Mortgage Fraud

- Analysis of available law enforcement and industry

resources indicates that the top ten mortgage fraud

areas are California, Florida, Georgia, Illinois,

Indiana, Michigan, New York, Ohio, Texas, and Utah.

Other areas significantly affected by mortgage fraud

include Arizona, Colorado, Maryland, Minnesota, Missouri,

Nevada, North Carolina, Tennessee, and Virginia.

- There is a strong correlation between mortgage

fraud and loans which result in default and foreclosure.

Emerging Schemes

- Recent statistics suggest that escalating foreclosures

provide criminals with the opportunity to exploit

and defraud vulnerable homeowners seeking financial

guidance.

- Perpetrators are exploiting the home equity line

of credit (HELOC) application process to conduct mortgage

fraud, check fraud, and potentially money laundering-related

activity.

FBI and Industry Respond to Escalating Mortgage

Fraud

- The FBI is proactively working with the mortgage

industry in an effort to curb mortgage fraud crimes.

The FBI signed a memorandum of agreement with the

MBA to promote the FBI’s Mortgage Fraud Warning

Notice.

Introduction

| The Prieston Group, a risk management

solutions provider that administers an insurance

product covering losses due to fraud and misrepresentation,

calculated that losses attributed to mortgage fraud

will most likely reach $4.2 billion for 2006. This

figure does not take into account another estimated

$1.2 billion spent on fraud prevention tools. |

| - The Prieston Group, 2006 Data,

16 February 2007,and 2 April 2007. |

Mortgage Fraud is defined as the intentional misstatement,

misrepresentation, or omission by an applicant or other

interested parties, relied on by a lender or underwriter

to provide funding for, to purchase, or to insure a

mortgage loan. Although no central repository collects

all mortgage fraud complaints, statistics from multiple

sources indicate that mortgage fraud is on the rise.

Some industry explanations for this increase point to

recent high mortgage loan origination volumes that strained

quality control efforts, the persistent desire of mortgage

lenders to hasten the mortgage loan process, the escalation

of home prices in recent years, and the introduction

of non-traditional loans which contain fewer quality

control restraints such as low documentation and no

documentation loans1.

Mortgage loan fraud is divided into two categories:

fraud for property and fraud for profit. Fraud for property/housing

entails minor misrepresentations by the applicant solely

for the purpose of purchasing a property for a primary

residence. This scheme usually involves a single loan.

Although applicants may embellish income and conceal

debt, their intent is to repay the loan. Fraud for profit,

however, often involves multiple loans and elaborate

schemes perpetrated to gain illicit proceeds from property

sales. It is this second category that is of most concern

to law enforcement and the mortgage industry. Gross

misrepresentations concerning appraisals and loan documents

are common in fraud for profit schemes and participants

are frequently paid for their participation. Recent

events likely resulted in an increase in mortgage fraud

as higher housing prices tempted borrowers to commit

fraud for property in order to qualify for a mortgage

loan. Also, mortgage fraud perpetrators likely seized

the opportunity to take advantage of the relaxed lending

practices to commit fraud for profit.

The most common form of mortgage fraud is illegal property

flipping which entails false appraisals and other fraudulent

loan documents (see figure 1). Combating mortgage fraud

effectively requires the cooperation of law enforcement

and industry entities. No single regulatory agency is

charged with monitoring this crime. The FBI, Department

of Housing and Urban Development-Office of Inspector

General (HUD-OIG), Internal Revenue Service, Postal

Inspection Service, and state and local agencies are

among those investigating mortgage fraud.

Figure 1: Illegal Property Flipping

Scheme

|

Mortgage fraud is a relatively low-risk, high-yield

criminal activity that tempts many. However, according a May

2006 Financial Crimes Enforcement Network (FinCEN) report,

finance-related occupations, including accountants, mortgage

brokers, and lenders, were the most common suspect occupations

associated with reported mortgage fraud2. Perpetrators

in these occupations are familiar with the mortgage loan process

and therefore know how to exploit vulnerabilities in the system.

Victims of mortgage fraud may include borrowers, mortgage

industry entities, and those living in the neighborhoods affected

by mortgage fraud. Lenders are plagued with high foreclosure

costs, broker commissions, reappraisals, attorney fees, rehabilitation

costs, and other related expenses when a mortgage fraud is

committed3. As properties affected by mortgage

fraud are sold at artificially inflated prices, properties

in surrounding neighborhoods also become artificially inflated.

When property values increase, property taxes increase as

well. Legitimate homeowners also find it difficult to sell

their homes as surrounding properties affected by fraud deteriorate.

During boom periods, high mortgage loan volume impacts expedited

quality control efforts which often focus on production. Therefore,

perpetrators may submit loans based on fraudulent information

anticipating that the bogus information will be overlooked.

On the other hand, loan officers, brokers, and others in the

industry are paid by commission and may be tempted to approve

questionable loans when the housing market is down to maintain

current levels of income.

Analysis of mortgage originations indicates a decrease in

demand. As a result of the declining housing market, mortgage

fraud perpetrators may take advantage of eager loan originators

attempting to generate loans for commission. Mortgage loan

originations, including purchases and refinances declined

during 2006 across the United States. The Mortgage Bankers

Association (MBA) estimates that mortgage loan originations

will reach $2.28 trillion during 2007 (see figure 2)4.

According to an MBA December 2006 report, total home sales

during 2006 decreased by approximately 10 percent from 2005

sales. New home sales declined by 17 percent and existing

home sales dipped by 8 percent. In response to a decrease

in demand for housing, builders reduced single-family starts

(through November 2006) which were 14 percent lower than during

the same time period in 2005. The MBA estimates that the oversupply

of housing will continue to affect new home construction,

home sales, and home prices until mid-20075.

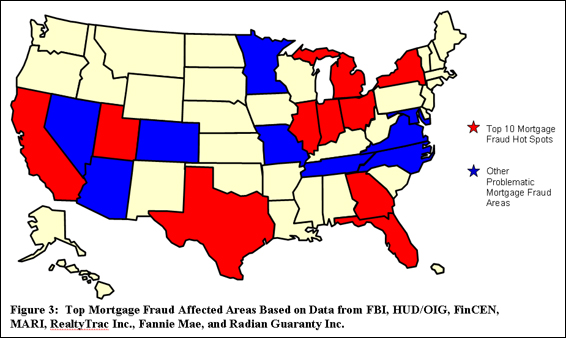

Top Areas for Mortgage Fraud

Data was compiled and analyzed from law enforcement

and industry sources to determine those areas of the country

most affected by mortgage fraud during 2006. Information from

the FBI, HUD-OIG, FinCEN, Mortgage Asset Research Institute

(MARI), Federal National Mortgage Association (Fannie Mae),

RealtyTrac Inc. (foreclosure statistics), and Radian Guaranty

Inc., indicate that the top ten mortgage fraud areas for 2006

were California, Florida, Georgia, Illinois, Indiana, Michigan,

New York, Ohio, Texas, and Utah. Other areas significantly

affected by mortgage fraud include Arizona, Colorado, Maryland,

Minnesota, Missouri, Nevada, North Carolina, Tennessee, and

Virginia (see figure 3).

Analysis of available information indicates that mortgage

fraud is most concentrated in the north central region of

the United States. The north central region is followed by

the southeast and west regions.

Regional analysis of FBI pending mortgage fraud-related investigations

as of FY 2006 reveals that the north central region of the

United States led the nation with the most pending investigations.

The north central region was followed by the southeast, west,

south central, and northeast, respectively (see figure 4).

| The aggregate amount of ARM loans containing

fraudulent misrepresentations is unknown. However, since

mortgage fraud perpetrators hope to inflate the value

of their properties and quickly sell them, they would

likely gravitate towards mortgage loans that offered low

and short-term interest rates such as those offered by

ARMs. |

Delinquency, Default, and Foreclosure: Potential Fraud

Indicators

Mortgage loans based on fraudulent information usually result

in delinquency, default, or foreclosure in a bear market.

According to the MBA, both delinquency and foreclosures rates

increased during 2006 and were largely concentrated in adjustable

rate mortgage (ARM) loans, especially sub-prime ARMs. This

is partly attributable to the recent rise in interest rates,

placing a strain on ARMs borrowers6.

BasePoint Analytics, a fraud analytics company, analyzed

more than 3 million loans and found that between 30 and 70

percent of early payment defaults (EPDs) are linked to significant

misrepresentations in the original loan applications7.

Radian Guaranty, Inc. is a leading provider of mortgage insurance

which protects lenders against loan default. Of the top ten

states Radian Guaranty Inc. ranked highest for mortgage fraud,

seven of them also ranked in the company’s top ten for

EPDs. This suggests that EPDs are a good mortgage fraud indicator.

During 2006 there were more than 1.2 million foreclosure

filings nationally, which represents a 42 percent increase

from 2005 figures. The foreclosure rate for 2006 was one foreclosure

filing for every 92 households8. Foreclosures for

2006 surpassed foreclosures for 2005 during every month of

the year9.

Emerging Schemes

Foreclosure Fraud

Recent statistics suggest that escalating foreclosures provide

criminals with the opportunity to exploit and defraud vulnerable

homeowners seeking financial guidance. The perpetrators convince

homeowners that they can save their homes from foreclosure

through deed transfers and the payment of up-front fees. This

“foreclosure rescue” often involves a manipulated

deed process that results in the preparation of forged deeds.

In extreme instances, perpetrators may sell the home or secure

a second loan without the homeowners’ knowledge, stripping

the property’s equity for personal enrichment.

While foreclosure scams vary, they may be used in combination

with other fraudulent schemes. For instance, perpetrators

may view foreclosure-rescue scams as a new method for fraudulently

acquiring properties to facilitate illegal property-flipping

and equity-skimming.

Home Equity Lines of Credit

| According to a DOJ press release, Mi Su

Yi and her husband, Paul Amorello, were sentenced in California

in July 2006 for operating a $3 million bust-out scheme

involving business lines of credit and HELOCs. The couple

accessed lines of credit that had been obtained by others

and paid the balances with worthless checks. They subsequently

withdrew cash from the lines of credit before the checks

were returned for insufficient funds. The couple laundered

their proceeds through bank accounts opened under three

false identities. In an attempt to avoid detection, the

couple deposited cash amounts of less than $10,000 into

these accounts. |

| -US DOJ, “New Jersey Residents Sentenced

to Prison for Running a $3 Million ‘Bust-Out’

Scheme,” Press Release, 25 July 2006, available

at http://www.usdoj.gov |

Individuals and criminal groups are exploiting the home equity

line of credit (HELOC) application process to conduct multiple-funding

mortgage fraud schemes, check fraud schemes, and potentially

money laundering-related activity. HELOCs differ from standard

home equity loans because the homeowner may borrow against

the line of credit over a period of time using a checkbook

or credit card. HELOCs are aggressively marketed by lenders

as an easy, fast, and inexpensive means to obtain funds. HELOC

funds are normally withdrawn on an as-needed basis to conduct

home repairs or to pay bills, but fraud perpetrators may withdraw

the entire amount within a short time period. Lenders typically

focus on property equity prior to funding HELOCs. As such,

many lenders do not demand a full property appraisal or a

full property title search.

Perpetrators apply for multiple HELOCs to different

lending institutions for a single property within a short

time period. Prior to providing the funding, lenders conduct

searches to determine if the property is encumbered by a lien.

However, liens on a property may not be recorded for several

days or months and thus cannot be immediately verified. Consequently,

lenders do not discover that they hold a third, fourth, or

fifth lien on a property (rather than the expected second

lien) until later. The money obtained from the multiple HELOCs

totals more than the original property purchase price, exceeding

the out-of-pocket expenses incurred to secure the property.

Perpetrators conducting check fraud schemes may manipulate

HELOC accounts and cause lenders to incur losses. For example,

a perpetrator secures a HELOC and withdraws the entire allotted

amount. A fraudulent check is then used to pay the balance

owed on the HELOC. However, the perpetrator quickly withdraws

the check amount from the HELOC before the bank realizes the

check is worthless. When the check is returned for insufficient

funds, the line of credit surpasses its maximum limit and

the lender experiences a loss. HELOC accounts have also been

used in common check frauds where perpetrators stole HELOC

checks, fraudulently completed them, and deposited the funds

into their own personal accounts.

HELOCs may also be used as a means of depositing and withdrawing

laundered proceeds to further conceal the original funding

source. As long as withdrawals from the HELOC do not exceed

the line of credit limit, payments deposited into the account

may be withdrawn later.

FBI and Industry Respond to Escalating Mortgage Fraud

The FBI is proactively working with the mortgage industry

in an effort to curb mortgage fraud crimes. On March 8, 2007,

the FBI signed a memorandum of agreement with the MBA to promote

the FBI’s Mortgage Fraud Warning Notice (see figure

5). The Notice states that it is illegal to make any false

statement regarding income, assets, debt or matters of identification,

or to willfully inflate property value to influence the action

of a financial institution. Under the agreement, the MBA and

the FBI will make the notice available to mortgage lenders

to use voluntarily as a means of educating consumers and mortgage

professionals of the penalties and consequences of mortgage

fraud.10

1Mortgage Asset Research Institute, “Eighth

Periodic Mortgage Fraud Case Report to MBA,” p. 3, 11,

12, April 2006.

2FinCEN, “The SAR Activity Review Trends,

Tips and Issues,” p. 15, May 2006, available at http://www.fincen.gov/sarreviewissue10.pdf

3Bits Financial Round Table, “Fraud Production

Strategies for Consumer, Commercial, and Mortgage Loan Documents,”

A Publication of the Bits Fraud Reductions Steering Committee,

p. 7, January 2005.

4Mortgage Bankers Association Mortgage Finance

Forecast, 13 March 2007, 8 November 2006, 7 December 2005,

and MBA 1-4 Family Mortgage Originations 1990-2005.

5Mortgage Bankers Association, “Year in Review:

Normalization of the Housing Market,” 29 December 2006.

6Mortgage Bankers Association, “Year in Review,

Normalization of the Housing Market, 29 December 2006.

7BasePoint White Paper, “New Early Payment

Default-Links to Fraud and Impact on Mortgage Lenders and

Investment Banks,” p. 2, 2007.

8RealtyTrac Staff, “More Than 1.2 Million

Foreclosures Reported in 2006,” RealtyTrac Inc. Press

Release, 25 January 2007

9RealtyTrac Incorporated, 2005 and 2006 Percent

of Households in Foreclosure, data provided 17 January 2007.

10Mortgage Bankers Association, “MBA Signs Memorandum

of Agreement with FBI to Promote Use of FBI’s Mortgage Fraud

Warning Notice,” Press Release, 8 March 2007.

Criminal Investigative Division, Criminal Intelligence

Section

|