|

| Home | Deposit Insurance | Consumer Protection | Industry Analysis | Regulations & Examinations | Asset Sales | News & Events | About FDIC |

|

|||||||||||||||||||||||||||||||||||

|

Home

> Industry Analysis

> Research & Analysis > FDIC Quarterly |

|||

|

FDIC Quarterly Individual Development Accounts and Banks: A Solid “Match” The more than 8,600 FDIC-insured banks and thrifts in the United States offer a wide variety of financial products and services through more than 94,000 banking offices. During the past decade, the development of alternative delivery channels, such as the Internet, has enhanced accessibility to banking products and services. Yet even with this greater access, about 10 million American households do not use any aspect of the banking system.1 An even larger number, perhaps tens of millions more American households, use only a limited number of banking services. Households, regardless of income level, underuse banking services for a variety of reasons. However, a large body of research provides evidence that limited involvement in the mainstream financial sector is most common among low- and moderate-income households.2 Although their income may be relatively low, these individuals hold assets and regularly conduct financial transactions, frequently with nonbank financial companies. Estimates of nonbank financial company transaction volume vary, but are as high as $250 billion annually.3 Not all of these revenues can be tied directly to low- and moderate-income individuals. However, these estimates are large enough to suggest a reasonable business case for insured institutions trying to attract the banking business of low- and moderate-income consumers. For most people, opening a checking or savings account is the first step toward involvement in the financial mainstream, followed by the use of credit products, investments, and insurance. A relatively low-risk way for banks to introduce low- and moderate-income households to the banking system is through a particular type of savings account—the Individual Development Account (IDA). This article explains how IDAs operate, discusses banks’ experience with IDAs, and provides resources for bankers who want to know more about these programs. History of IDAs Individual development accounts are matched savings accounts that enable low-income families to save money for a particular financial goal, such as buying a home, paying for post-secondary education, or starting or expanding a small business. The framework for IDAs is widely believed to have emerged in the early 1990s through “asset-based” policy research that advocates asset-building programs to alleviate poverty.4 Asset-based policy contends that traditional poverty programs that focus on income transfers, such as Temporary Assistance for Needy Families (TANF) payments or food stamp benefits, are necessary, but meet only short-term consumption needs. Asset-based policy proponents note that accumulating assets, such as contributing to a savings account or buying a home, over a longer time horizon creates a financial cushion for emergencies, which in turn generates social, behavioral, and psychological benefits. Armed with assets, an individual’s options for emerging from poverty and entering the financial mainstream are greatly enhanced. In 1993, Iowa was the first state to enact a law establishing IDAs. Today, 33 states (as well as Puerto Rico and the District of Columbia) have either laws or policies that govern the operations of IDAs (see Table 1 on next page). Of these states, 19 are currently operating programs that are supported by state funding. Approximately 540 community-based and -funded IDA programs operate across the United States including in the 17 states without IDA laws or policies.5 How Are Banks Involved in IDA programs?

IDA programs are generally created by nonprofit organizations or divisions of state or local government. However, for-profit entities, including FDIC-insured banks and thrifts, have also created IDA programs. The organization creating the IDA program, called the program sponsor, establishes the parameters of program participation (within state law or policy where appropriate). The program sponsor applies for matching funds and deposits those funds in a reserve account at a financial institution. Because the sponsor typically administers the IDA paperwork, it is sometimes called the administrator. The financial institution establishes and services individual savings accounts for program participants. Some services, such as providing periodic account statements, are similar to the institution’s typical savings accounts. However, other services, such as waiving minimum account balances or heightened monitoring to prevent premature withdrawals, may be specialized. The program sponsor usually assumes responsibility for allocating matching funds to individual accounts. The relationship between the program sponsor and the financial institution is commonly governed by a written agreement. In practice, many IDA programs involve partnerships of multiple nonprofit or government organizations and financial institutions. Financial institutions may provide some or all of the matching funds tothe sponsoring organization, and also may provide general operational support and funding, such as absorbing the costs of marketing or providing financial education to participants. According to data from CFED, a nonprofit organization that provides a clearinghouse of information on IDAs, 244 FDIC-insured banks and thrifts and 53 credit unions participated in IDA programs in 2005 (the most recent data available).6 How Do IDAs Operate? In general, IDAs operate similarly to other types of “matched” savings plans, such as 401(k) retirement accounts.7 With an IDA, the account holder deposits money in a savings account, and the funds are matched anywhere from dollar for dollar up to eight dollars to one dollar, depending on the rules of the particular program and state law. Two or three dollars to one dollar is the common match range. A “ceiling” of dollars and time frames typically is established for the match amount. Money for the match is provided through a variety of public and private sources (see Charts 1 and 2 on next page). The U.S. Treasury, under the Assets for Independence Act of 1998 (AFI), provides most of the matching funds. The AFI has provided an average of $25 million in annual appropriations to fund IDA matches. As shown in Chart 1, almost 60 percent of IDA programs that receive funding obtain matching funds through the AFI. State programs, faith-based organizations, philanthropic groups, and corporations also provide matching funds. Banks are important contributors as well; as shown in Chart 2, they provide matching funds to about 25 percent of IDA programs that receive funding. Banks also provide about 30 percent of the general operational funding to these programs. IDA participation requirements, which are based on state laws and policies as well as rules and requirements of the sponsoring organization, commonly include some combination of the following:

Potential Benefits to Banks of Participating in an IDA Banks can use IDAs to tap into new markets by establishing relationships with individuals who may have no banking relationships (unbanked) or only minimal relationships with mainstream financial companies (underbanked). Estimates of the size of this market vary, but research indicates that a substantial portion of the population does not fully use the banking system. For example, the results of the Federal Reserve’s 2004 Survey of Consumer Finances showed that nearly 9 percent of American households are unbanked; they do not have a checking or savings account. A study by the Center for Financial Services Innovation(CFSI) indicates that the unbanked rate is 30 percent for low- and moderate-income households.11 This study also shows that of the 70 percent of low- and moderate-income households that have bank accounts, almost two-thirds may be considered “underbanked,” as they continue to use nonbank financial services.12 These customers are considered low- and moderate-income, but they do conduct a large volume of financial transactions. For instance, the nearly 1 million households surveyed by the CFSI during 2003 and 2004 bought 1.2 million money orders and cashed 1.9 million checks per month.13 Extrapolating this activity across the country suggests that low- and moderate-income households conduct a significant level of transactions outside mainstream banking. Banks can offer IDAs as a way of introducing customers to the mainstream financial system with a very simple, low-risk product—a savings account. The initial product may be small and perhaps not yet profitable. However, over time, at least some of these customers likely will continue the relationship and expand into other products, becoming profitable in the long run. As the goal of the IDA is often home purchase, further education, or small business needs, account holders may also choose credit products from the IDA-administering banks. In addition to establishing an initial relationship with new customers, banks can benefit as administrators of the master reserve account and the individual accounts. Banks can use the funds for general purposes while the customer is restricted from withdrawing the matched money, usually for a year or more. Establishing IDAs with direct deposit might be particularly beneficial, as both the saver and the financial institution are virtually assured that regular contributions will be made. Participants who use direct deposit are much more likely to be savers and remain active in the IDA program.14 Intangible benefits also accrue to banks that provide IDAs. These programs generate goodwill throughout communities as well as with existing customers by working with local organizations to assist the needy and disadvantaged. Local nonprofit organizations that sponsor IDAs routinely recognize the efforts of their financial institution partners, and these initiatives often receive positive local press coverage. More tangibly, banks could receive positive consideration from financial institution regulators as their investment, lending, and service performance is evaluated under the Community Reinvestment Act (CRA). Although each bank, situation, and IDA program is different and would be evaluated on its own merits, the following are examples of how bank participation in IDA programs could receive positive CRA consideration:

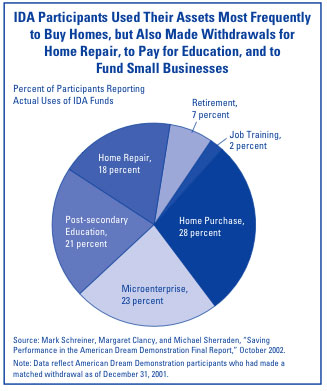

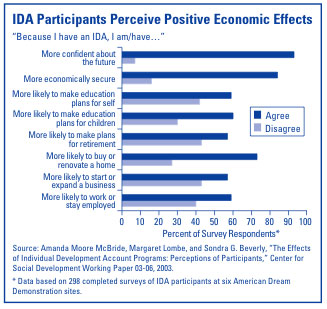

Do IDAs Really Work? A review of the effectiveness of IDAs was conducted by the American Dream Demonstration(ADD) from 1997 to 2001; this survey encompassed 14 IDA programs across the country.16 The ADD survey was organized by CFED, conducted by the Center for Social Development, and funded by various philanthropic foundations. The following statistics demonstrate that IDAs can help low-income Americans enter the financial mainstream and build assets:

In addition to the national ADD study, the FDIC tracks the success of local IDA programs. FDIC Community Affairs staff routinely serves as communication facilitators between banks and nonprofit IDA sponsors and advises about the financial education component of IDA programs. More specifically, the FDIC provides access to instructor education on the FDIC’s Money Smart financial education curriculum. Money Smart was developed by the FDIC in 2001 to help low- and moderate-income adults enhance their money management skills, understand basic mainstream financial services, avoid pitfalls, and build financial confidence to use banking services effectively.18 The textbox on page 32 describes the outcomes of an IDA program facilitated by the FDIC in the Kansas City metro area. This program is sponsored by a local nonprofit, The Family Conservancy in Kansas City, and involves three banks, UMB Bank, N.A., U.S. Bank, N.A., and Emporia State Bank.19 The program has been successful in creating savers; as of year-end 2006, more than 371 individuals have successfully exited the program with their matched funds. Additionally, this program provides tangible evidence that IDA customers do migrate to other bank products; about half the 170 participants who purchased a home received a mortgage from their IDA bank. Are IDAs Profitable for Banks?Very little empirical data exist about the profitability of IDAs for banks. A study conducted in 2003 by the Center for Community Capitalism concluded that IDA programs have not been subjected to robust cost-benefit analysis at banks.20 Further, it is likely that these institutions’ community development goals probably result in relaxed profitability targets in the short term.21 The same study noted that short-term costs, particularly for labor, can be high. As described below, federal legislation has been introduced that would provide tax credits to insured institutions to offset some of these costs, potentially accelerating the timeframe for profitability. However, taking a longer-term view—potentially developing long-term customers and “graduating” IDA participants into credit and other products—may be more appropriate than the traditional break-even analysis.22 What Lies Ahead for IDAs?While IDAs have helped low- and moderate-income Americans transition to the financial mainstream and a potentially more secure future, a number of barriers appear to constrain IDA use on a large scale. For instance, as with any program that relies on donations, there is a persistent shortage of matched and operational funds. However, other, perhaps less obvious barriers also exist. These barriers are described below, along with potential solutions. Lack of Knowledge about IDAs – A National IDA FrameworkIndividuals who may qualify for an IDA and banks that may want to participate in IDA programs may find it difficult to obtain critical information because IDAs are dispersed among many organizations. Federal IDA laws have been debated that would standardize what is currently a patchwork of several hundred programs operated under various state laws and community program parameters. Most recently, the Saving for Working Families Act was reintroduced in March 2007. This act, first introduced in 2003, would establish a national framework for IDAs and would provide $1.2 billion in tax credits to allow banks to offset part of the cost of opening and maintaining the accounts. No Ability to Save – Linking Taxes and SavingsPotential IDA participants may be discouraged from participating because they do not believe they will be able or are not disciplined enough to contribute funds to the account. Some policymakers believe this obstacle could be overcome, at least in part, by linking tax refunds and savings. Generally, the same individuals who qualify for IDAs qualify for the Earned Income Tax Credit and tend to receive sizable tax refunds. Every year, the Internal Revenue Service processes funds averaging $2,100 for more than 100 million taxpayers, many of whom are poor and perhaps underbanked.23 In the past, banks and community and charitable organizations have been successful in recruiting IDA participants through the Voluntary Income Tax Assistance (VITA) program. Under the VITA program, volunteers prepare tax returns for low- and moderate-income Americans at nonprofit locations. Program sponsors and banks often use this opportunity to market IDAs to consumers, suggesting that they place all or a portion of their refunds in IDAs. In 2007, in compliance with the Pension Protection Act of 2006, the Internal Revenue Service began giving taxpayers the option of electronically splitting their tax refund among two or three financial institution accounts. Consumers now can choose to divide their refunds between their IDA and a checking account, for example, which would give them immediate access to some of the funds while allowing them to save the remainder for longer-term goals. The ability to split refunds will streamline the process of opening IDAs and may help expand the use of this program. A small-scale demonstration of refund splitting was conducted in the 2004 tax season by the Doorways to Dreams (D2D) Fund in Boston, Massachusetts. D2D is a nonprofit research firm that explores ways to use technology to address poverty-related issues. D2D used its methodology to split the refunds, with the following results:

Too Much Debt to Save – Linking Small-Dollar Credit with SavingsSome individuals may feel that debt service payments on high-cost credit are too large, leaving them no funds to set aside in savings. On December 4, 2006, the FDIC released for comment the “Affordable Small Loan Guidelines,” which encourage banks to offer small-dollar credit that is affordable, yet safe and sound, as an alternative to short-term, high-cost credit, such as payday loans.25 The final Guidelines are expected to be issued very soon. As part of small-dollar loan programs, banks are encouraged to include a savings component, whereby borrowers can either set aside a percentage of the amount borrowed or of the periodic payment in a savings account. Over the long term, this approach can help banks develop a relationship with borrowers and can help borrowers build assets to lessen their reliance on short-term loans. Depending on the rules of a particular IDA program, banks may be able to offer customers the option to use an IDA account for the savings component of small-dollar loan programs as a means of leveraging the use of the match feature. IDA Resources for BanksBanks often become involved in IDA programs through contacts and relationships with charitable and other nonprofit organizations. The FDIC’s Community Affairs staff has developed relationships with local organizations and can facilitate communications between IDA sponsors and banks. The FDIC has also established the Alliance for Economic Inclusion (AEI), a new national initiative of broad-based coalitions of financial institutions, community-based organizations, and other partners in nine markets across the country to bring unbanked and underbanked individuals into the financial mainstream.26 For more information on these initiatives, contact the FDIC’s Community Affairs Office in your state (see Table 2 on next page).

The following organizations are additional sources of information for banks that may want to participate in an IDA program.27

IDAs: Indeed a “Good” MatchA sound business case exists for banks to develop strategies to attract low- and moderate-income customers, as these individuals are generating significant revenues for nonbank financial companies. IDAs are a straightforward, low-risk way to appeal to such customers. Although IDAs are unlikely to be profitable in the short term, expanding relationships with these customers may generate profitability over the longer term. In addition, other benefits accrue to banks participating in IDA programs, such as positive consideration during CRA examinations and goodwill in the community. If some of the barriers can be overcome, then IDA programs may become more widespread, providing additional opportunities for low-income individuals to join the financial mainstream and for banks to reach out to new customers.

Author: Rae-Ann Miller, Special Advisor to the Director, Division of Insurance and Research, rmiller@fdic.gov Contributor: Susan Burhouse, Financial Economist, Division of Insurance and Research, sburhouse@fdic.gov The author wishes to thank Elizabeth Russell List (Community Affairs Officer, FDIC), Kim Lowry (Writer/Editor, FDIC), Vanessa Vaughn (Community Relations Specialist, UMB Bank, N.A.), Turner Pettway (Community Development Manager, U.S. Bank, N.A.), Kim Pate (Director, Field Development, CFED), Emily Appel (Program Manager, Field Development, CFED), and Julie Riddle (Manager, Asset Building and Family Support Programs, The Family Conservancy). The author wishes to extend special thanks to Susan Burhouse, without whose significant assistance this article would not have been completed. Notes

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||

| Last Updated 10/25/2007 | Questions, Suggestions & Requests | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Home Contact Us Search Help SiteMap Forms Freedom of Information Act (FOIA) Service Center Website Policies USA.gov |

| FDIC Office of Inspector General |