Background

Basic Structure and Scope of Proposal

Details on Program Design

Impact of the Program

Loan Modification Program Guide – "Mod in a Box"

Background

Although foreclosures are costly to lenders, borrowers and communities, the pace of loan modifications continues to be extremely slow (around 4 percent of seriously delinquent loans each month). It is imperative to provide incentives to achieve a sufficient scale in loan modifications to stem the reductions in housing prices and rising foreclosures.

Modifications should be provided using a systematic and sustainable process. The FDIC has initiated a systematic loan modification program at IndyMac Federal Bank to reduce first lien mortgage payments to as low as 31% of monthly income. Modifications are based on interest rate reductions, extension of term, and principal forbearance. A loss share guarantee on redefaults of modified mortgages can provide the necessary incentive to modify mortgages on a sufficient scale, while leveraging available government funds to affect more mortgages than outright purchases or specific incentives for every modification. The FDIC would be prepared to serve as contractor for Treasury and already has extensive experience in the IndyMac modification process.

Basic Structure and Scope of Proposal

This proposal is designed to promote wider adoption of such a systematic loan modification program:

- by paying servicers $1,000 to cover expenses for each loan modified according to the required standards; and

- sharing up to 50% of losses incurred if a modified loan should subsequently re-default

We envision that the program can be applied to the estimated 1.4 million non-GSE mortgage loans that were 60 days or more past due as of June 2008, plus an additional 3 million non-GSE loans that are projected to become delinquent by year-end 2009. Of this total of approximately 4.4 million problem loans, we expect that about half can be modified, resulting in some 2.2 million loan modifications under the plan.

Details on Program Design

- Eligible Borrowers: The

program will be limited to loans secured by owner-occupied properties.

- Exclusion for Early Payment Default: To

promote sustainable mortgages, government loss sharing would be available

only after the borrower has made six payments on the modified mortgage.

- Standard NPV Test: In order to promote consistency and simplicity in implementation and audit, a standard test comparing the expected net present value (NPV) of modifying past due loans compared to the strategy of foreclosing on them will be applied. Under this NPV test, standard assumptions will be used to ensure that a consistent standard for affordability is provided based on a 31% borrower mortgage debt-to-income ratio.

- Systematic Loan Review by

Participating Servicers: Participating servicers would

be required to undertake a systematic review of all of the loans under

their management, to subject each loan to a standard NPV test to determine

whether it is a suitable candidate for modification, and to modify all loans

that pass this test. The penalty for failing to undertake such a

systematic review and to carry out modifications where they are justified would

be disqualification from further participation in the program until such a

systematic program was introduced.

- Reduced Loss Share Percentage for

"Underwater Loans": For LTVs above 100%, the government

loss share will be progressively reduced from 50% to 20% as the current

LTV rises.1

If the LTV for the first lien exceeds 150%, no loss sharing would be

provided.

- Simplified Loss Share Calculation: In

order to ensure the administrative efficiency of this program, the calculation

of loss share basis would be as simple as possible. In general terms, the

calculation would be based on the difference between the net present value

of the modified loan and the amount of recoveries obtained in a disposition

by refinancing, short sale or REO sale, net of disposal costs as estimated

according to industry standards. Interim modifications would be allowed.

- De minimis Test: To lower administrative costs,

a de minimis test excludes

from loss sharing any modification that did not lower the monthly payment

at least 10 percent.

- Eight-year Limit on Loss Sharing Payments:

The loss sharing guarantee ends eight years of the modification.

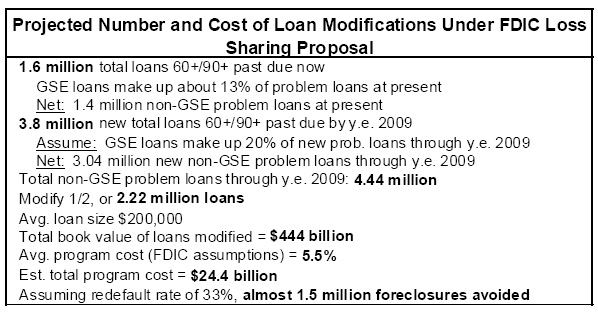

Impact of the Program

The table below outlines some of the basic assumptions behind the scale of the plan and its expected costs.2 To summarize, we expect that about half of the projected 4.4 million problem loans between now and year-end 2009 can be modified. Assuming a redefault rate of 33 percent, this plan could reduce the number of foreclosures during this period by some 1.5 million at a projected program cost of $24.4 billion.

1 Current LTV can be demonstrated by a Broker Price opinion, or BPO.

2 Note: These figures have been updated from previous summaries to reflect a narrower application of the program to non-GSE loans that become delinquent through year-end 2009.