|

DEFERRED MAINTENANCE

The U.S. Department of Labor (DOL) maintains one hundred twenty-two (122) Job Corps centers located throughout the United States. Periodic maintenance is performed to keep these centers in acceptable condition, as determined by Job Corps management. Maintenance requirements are stratified by management into critical and non-critical projects. Critical maintenance involves life, safety, health, and environmental issues, as well as building code compliance deficiencies. Critical maintenance projects are funded and performed in the year they are identified. Non-critical maintenance projects are performed each year to the extent that funding constraints allow. Non-critical maintenance projects that cannot be funded when scheduled are deferred to a future period.

Condition Assessment Surveys

Condition assessment surveys are conducted every three years at each Job Corps center to determine the current condition of buildings and structures (constructed assets) and the estimated maintenance cost to correct deficiencies. Surveys conducted during years one and two of this three year cycle are updated annually to reflect maintenance performed, and rolled up with current assessments to provide a condition assessment for the entire Job Corps portfolio of constructed assets. Condition assessment surveys are based on methods and standards consistently applied, including:

- condition descriptions of facilities

- recommended maintenance schedules

- estimated costs of maintenance actions

- standardized condition codes

Asset Condition

Condition assessment surveys are used to estimate the current plant replacement value and deferred maintenance repair backlog for every constructed asset at each Job Corps center. Plant replacement value and repair backlog are used to calculate a Facilities Condition Index (FCI) for each building and structure. The chart below ranks each asset within one of five categories of asset condition, based on the assets FCI score, for the previous five year period.

Job Corps Center Constructed Assets

Ranking of Individual Asset Condition By FCI Scores(1)

For the Years Ended 2004 — 2008

|

2008 |

2007* |

2006* |

2005* |

2004* |

Asset Condition |

FCI Score |

No. of

Assets |

Asset

% |

No. of

Assets |

Asset

% |

No. of

Assets |

Asset

% |

No. of

Assets |

Asset

% |

No. of

Assets |

Asset

% |

Excellent |

90- 100% |

2,878 |

81.9 |

2,966 |

80.9 |

2,665 |

75.1 |

2,507 |

74.8 |

2,244 |

72.1 |

Good |

80- 89% |

311 |

8.9 |

338 |

9.2 |

433 |

12.2 |

412 |

12.3 |

286 |

9.2 |

Fair |

70- 79% |

115 |

3.3 |

126 |

3.4 |

145 |

4.1 |

151 |

4.5 |

274 |

8.8 |

Poor |

60- 69% |

89 |

2.5 |

98 |

2.7 |

135 |

3.8 |

120 |

3.6 |

146 |

4.7 |

Very Poor |

< 60% |

118 |

3.4 |

136 |

3.8 |

170 |

4.8 |

161 |

4.8 |

162 |

5.2 |

|

|

3,511 |

100.0 |

3,664 |

100.0 |

3,548 |

100.0 |

3,351 |

100.0 |

3,112 |

100.0 |

(1) FCI = 1 — (Repair Backlog / Plant Replacement Value). An FCI closer to 100 % indicates better asset condition.

* Distribution of FCI for 2004 — 2007 was estimated, based on the trend in asset condition established in 2008, when modifications to the calculation were newly implemented.

Portfolio Condition and Deferred Maintenance Cost Estimates

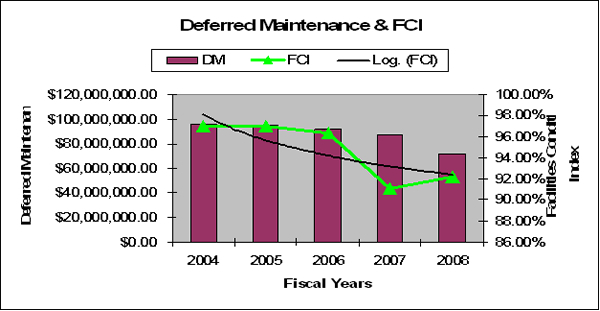

The FCI assessments by building and structure are consolidated to calculate an FCI score for the entire portfolio of constructed assets, which is used to evaluate the overall asset condition of the Job Corps portfolio. Job Corps has set the goal of achieving and maintaining an FCI of 90% or greater (the standard used by the National Association of College and University Business Offices) for its portfolio of constructed assets. In 2008, the portfolio's aggregate FCI score for 3,511 constructed assets was 92.2%, and deferred maintenance costs to return the portfolio to an acceptable condition were estimated at $71.9 million, as shown in the table below. The final graph juxtaposes deferred maintenance cost estimates with the FCI trend line for the five year period ending in 2008.

Job Corps Center Constructed Assets

Portfolio Condition and Deferred Maintenance Cost Estimates at

September 30, 2004 - 2008

|

Constructed Assets - FY |

Number of

Constructed

Assets |

Portfolio Condition

Based on

Aggregate FCI Score |

Deferred Maintenance

Costs to Return Assets

To Acceptable Condition |

|

Buildings and structures - 2008 |

3,511 |

Excellent - 92.2% |

$71,901,425 |

|

Buildings and structures - 2007 |

3,664 |

Excellent - 90.8% |

$87,372,700 |

|

Buildings and structures - 2006 |

3,548 |

Excellent - 96.3% |

$92,100,000 |

|

Buildings and structures - 2005 |

3,351 |

Excellent - 97.0% |

$94,800,000 |

|

Buildings and structures - 2004 |

3,112 |

Excellent - 97.0% |

$95,500,000 |

SOCIAL INSURANCE PROGRAMS

The Federal Accounting Standards Advisory Board (FASAB) has classified certain government income transfer programs as social insurance programs. Recognizing that these programs have complex characteristics that do not fit traditional accounting models, the FASAB has developed accounting standards for social insurance programs which require the presentation of supplementary information to facilitate the assessment of the program's long -term sustainability.

The U.S. Department of Labor operates two programs classified under Federal accounting standards as social insurance programs, the Unemployment Insurance Program and the Black Lung Disability Benefits Program. Presented below is the supplementary information for the two programs.

Unemployment Insurance Program

The Unemployment Insurance (UI) Program was created in 1935 to provide income assistance to unemployed workers who lose their jobs through no fault of their own. The program protects workers during temporary periods of unemployment through the provision of unemployment compensation benefits. These benefits replace part of the unemployed worker's lost wages and, in so doing, stabilize the economy during recessionary periods by increasing the unemployed's purchasing power. The UI program operates counter cyclically, with benefits exceeding tax collections during recessionary periods and UI tax revenues exceeding benefit payments during periods of recovery.

Program Administration and Funding

The UI program is administered through a unique system of Federal-State partnerships, established in Federal law but executed through conforming State laws by State officials. The Federal government provides broad policy guidance and program direction through the oversight of the U.S. Department of Labor, while program details are established through individual State UI statutes, administered through State UI agencies.

Federal and State Unemployment Taxes

The UI program is financed through the collection of Federal and State unemployment taxes levied on subject employers and deposited in the Unemployment Trust Fund (UTF). The UTF was established to account for the receipt, investment and disbursement of unemployment taxes. Federal unemployment taxes are used to pay for the administrative costs of the UI program, including grants to each State to cover the costs of State UI operations and the Federal share of extended UI benefits. Federal unemployment taxes are also used to maintain a loan account within the UTF, from which insolvent States may borrow funds to pay UI benefits. State UI taxes are used exclusively for the payment of regular UI benefits, as well as the State's share of extended benefits.

Federal Unemployment Taxes

Under the provisions of the Federal Unemployment Tax Act (FUTA), a Federal tax is levied on covered employers, at a current rate of 6.2% of the first $7,000 in annual wages paid to each employee. This Federal tax rate is reduced by a credit of up to 5.4%, granted to employers paying State UI taxes under conforming State UI statutes. Accordingly, in conforming States, employers pay an effective Federal tax of 0.8% (0.6% starting January 1, 2009). Federal unemployment taxes are collected by the Internal Revenue Service.

State Unemployment Taxes

In addition to the Federal tax, individual States finance their UI programs through State tax contributions from subject employers based on the wages of covered employees. (Three States also collect contributions from employees.) Within Federal confines, State tax rates are assigned in accordance with an employer's experience with unemployment. Actual tax rates vary greatly among the States and among individual employers within a State. At a minimum, these rates must be applied to the Federal tax base of $7,000; however, States may adopt a higher wage base than the minimum established by FUTA. State UI agencies are responsible for the collection of State unemployment taxes.

Unemployment Trust Fund

Federal and State UI taxes are deposited into designated accounts within the Unemployment Trust Fund. The UTF was established under the authority of Title IX, Section 904 of the Social Security Act of 1935, as amended, to receive, hold, invest, loan and disburse Federal and State UI taxes. The U.S. Department of the Treasury acts as custodian over monies deposited into the UTF, investing amounts in excess of disbursing requirements in Treasury securities. The UTF is comprised of the following accounts:

Federal Accounts

The Employment Security Administration Account (ESAA) was established pursuant to Section 901 of the Act. All tax receipts collected under the Federal Unemployment Tax Act (FUTA) are appropriated to the ESAA and used to pay the costs of Federal and State administration of the unemployment insurance program and veterans' employment services, as well as 97 percent of the costs of the State employment services. Excess balances in ESAA, as defined under the Act, are transferred to other Federal accounts within the Fund, as described below.

The Federal Unemployment Account (FUA) was established pursuant to Section 904 of the Act. FUA is funded by any excesses from the ESAA as determined in accordance with Section 902 of the Act. Title XII, Section 1201 of the Act authorizes the FUA to loan Federal monies to State accounts that are unable to make benefit payments because the State UI account balance has been exhausted. Title XII loans must be repaid with interest. The FUA may borrow from the ESAA or EUCA, without interest, or may also receive repayable advances, with interest, from the general fund of the U.S. Treasury, when the FUA has a balance insufficient to make advances to the States.

The Extended Unemployment Compensation Account (EUCA) was established pursuant to Section 905 of the Act. EUCA provides for the payment of extended unemployment benefits authorized under the Federal-State Extended Unemployment Compensation Act of 1970, as amended. Under the extended benefits program, extended unemployment benefits are paid to individuals who have exhausted their regular unemployment benefits. These extended benefits are financed one-half by State unemployment taxes and one-half by FUTA taxes from the EUCA. The EUCA is funded by a percentage of the FUTA tax transferred from the ESAA in accordance with Section 905(b)(1) and (2) of the Act. The EUCA may borrow from the ESAA or the FUA, without interest, or may also receive repayable advances from the general fund of the Treasury when the EUCA has a balance insufficient to pay the Federal share of extended benefits. During periods of sustained high unemployment, the EUCA may also receive payments and non-repayable advances from the general fund of the Treasury to finance emergency unemployment compensation benefits. Emergency unemployment benefits require Congressional authorization.

The Federal Employees Compensation Account (FEC) was established pursuant to Section 909 of the Act. The FEC account provides funds to States for unemployment compensation benefits paid to eligible former Federal civilian personnel and ex-service members. Generally, benefits paid are reimbursed to the Federal Employees Compensation Account by the various Federal agencies. Any additional resources necessary to assure that the account can make the required payments to States, due to the timing of the benefit payments and subsequent reimbursements, will be provided by non-repayable advances from the general fund of the Treasury.

State Accounts

Separate State Accounts were established for each State and territory depositing monies into the Fund, in accordance with Section 904 of the Act. State unemployment taxes are deposited into these individual accounts and may be used only to pay State unemployment benefits. States may receive repayable advances from the FUA when their balances in the Fund are insufficient to pay benefits.

Railroad Retirement Accounts

The Railroad UI Account and Railroad UI Administrative Account were established under Section 904 of the Act to provide for a separate unemployment insurance program for railroad employees. This separate unemployment insurance program is administered by the Railroad Retirement Board, an agency independent of DOL. DOL is not responsible for the administrative oversight or solvency of the railroad unemployment insurance system. Receipts from taxes on railroad payrolls are deposited in the Railroad UI Account and the Railroad UI Administrative Account to meet benefit payment and related administrative expenses.

UI Program Benefits

The UI program provides regular and extended benefit payments to eligible unemployed workers. Regular UI program benefits are established under State law, payable for a period not to exceed a maximum duration. In 1970, Federal law began to require States to extend this maximum period of benefit duration by fifty percent during periods of high unemployment. These extended benefit payments are paid equally from Federal and State accounts.

Regular UI Benefits

There are no Federal standards regarding eligibility, amount or duration of regular UI benefits. Eligibility requirements, as well as benefit amounts and benefit duration are determined under State law. Under State laws, worker eligibility for benefits depends on experience in covered employment during a past base period, which attempts to measure the workers' recent attachment to the labor force. Three factors are common to State eligibility requirements: (1) a minimum duration of recent employment and earnings during a base period prior to unemployment, (2) unemployment not the fault of the unemployed, and (3) availability of the unemployed for work.

Benefit payment amounts under all State laws vary with the worker's base period wage history. Generally, States compute the amount of weekly UI benefits as a percentage of an individual's average weekly base period earnings, within certain minimum and maximum limits. Most States set the duration of UI benefits by the amount of earnings an individual has received during the base period. Currently, almost all States have established the maximum duration for regular UI benefits at 26 weeks. Regular UI benefits are paid by the State UI agencies from monies drawn down from the State's account within the Unemployment Trust Fund.

Extended UI Benefits

The Federal/State Extended Unemployment Compensation Act of 1970 provides for the extension of the duration of UI benefits during periods of high unemployment. When the insured unemployment level within a State, or in some cases total unemployment, reaches certain specified levels, the State must extend benefit duration by fifty percent, up to a combined maximum of 39 weeks. Fifty percent of the cost of extended unemployment benefits is paid from the Extended Unemployment Compensation Account within the UTF, and fifty percent by the State, from the State's UTF account.

Emergency UI Benefits

During prolonged periods of high unemployment, Congress may authorize the payment of emergency unemployment benefits to supplement extended UI benefit payments. Emergency benefits began in July 2008, authorized under the Supplemental Appropriations Act, 2008. Before this fiscal year, emergency benefits were last authorized in 2002 under the Temporary Extended Unemployment Compensation Act. Payments in excess of $23 billion were paid under the program which ended in January 2005. Prior to that, emergency benefits were authorized in 1991 under the Emergency Unemployment Compensation Act. Emergency benefit payments in excess of $28 billion were paid over the three year period ended in 1994.

Federal UI Benefits

Unemployment benefits to unemployed Federal workers are paid from the Federal Employment Compensation Account within the Unemployment Trust Fund. These benefit costs are reimbursed by the responsible Federal agency and are not considered to be social insurance benefits. Federal unemployment compensation benefits are not included in this discussion of social insurance programs.

Program Finances and Sustainability

At September 30, 2008, total assets within the UTF exceeded liabilities by $72.1 billion. This fund balance approximates the accumulated surplus of tax revenues and earnings on these revenues over benefit payment expenses and is available to finance benefit payments in future periods when tax revenues may be insufficient. Treasury invests this accumulated surplus in Federal securities. The net value of these securities, including interest receivable, at September 30, 2008 was $73.3 billion. This interest is distributed to eligible State and Federal accounts within the UTF. Interest income from these investments during FY 2008 was $3.6 billion. Federal and State UI tax and reimbursable revenues of $39.4 billion and regular, extended and emergency benefit payment expense of $42.5 billion were recognized for the year ended September 30, 2008.

As discussed in Note 1.L.1 to the consolidated financial statements, DOL recognized a liability for regular, extended and emergency unemployment benefits to the extent of unpaid benefits applicable to the current period and for benefits paid by States that have not been reimbursed by the UTF. Accrued unemployment benefits payable at September 30, 2008 were $1.2 billion.

Effect of Projected Cash Inflows and Outflows on the Accumulated Net Assets of the UTF

The ability of the UI program to meet a participant's future benefit payment needs depends on the availability of accumulated taxes and earnings within the UTF. The Department measures the effect of projected benefit payments on the accumulated net assets of the UTF, under an open group scenario, which includes current and future participants in the UI program. Future estimated cash inflows and outflows of the UTF are tracked by the Department for budgetary purposes. These projections allow the Department to monitor the sensitivity of the UI program to differing economic conditions, and to predict the program's sustainability under varying economic assumptions. The significant assumptions used in the projections include total unemployment rates, civilian labor force levels, percent of unemployed receiving benefits, total wages, distribution of benefit payments by state, state tax rate structures, state taxable wage bases and interest rates on UTF investments.

Presented on the following pages is the effect of projected economic conditions on the net assets of the UTF, excluding the Federal Employees Compensation Account.

Expected Economic Conditions

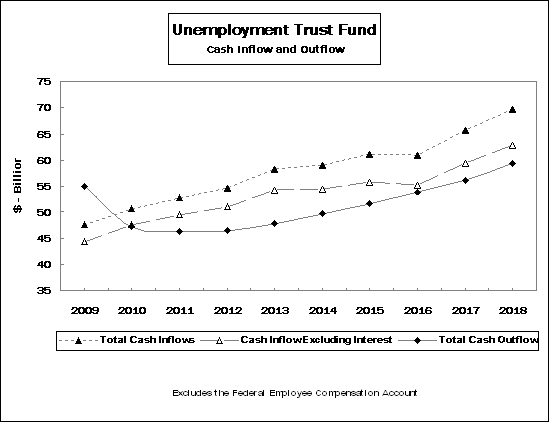

Charts I and II graphically depict the effect of expected economic conditions on the UTF over the next ten years.

Projected Cash Inflows and Outflows Under Expected Economic Conditions

Chart I depicts projected cash inflows and outflows of the UTF over the next ten years under expected economic conditions. Both cash inflows and cash inflows excluding interest earnings are displayed. Current estimates by the Department are based on an expected unemployment rate of 5.58% during FY 2009, decreasing to 4.80% in FY 2013 and thereafter. Total cash inflows exceed total cash outflows for all years projected after FY 2009. The net inflow increases from $3.5 billion in FY 2010 to $10.5 billion in FY 2013, leveling off at the $7.1 billion to $10.2 billion range after that, indicating that most States have replenished their funds to desired levels. The net inflow is sustained by the excess of Federal tax collections over Federal expenditures.

These projections, excluding interest earnings, indicate increasing net cash inflows from FY 2010 to FY 2013, then net cash inflows at varied levels through 2018.

Chart I

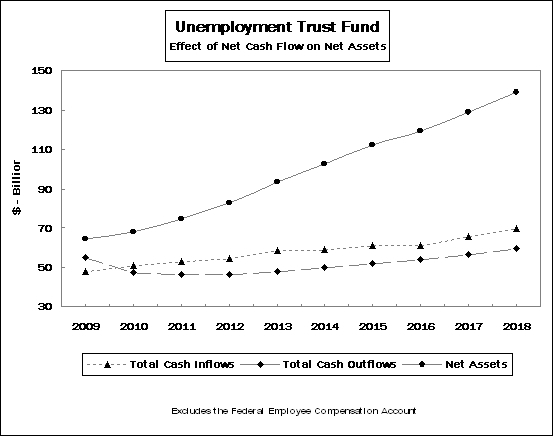

Effect of Expected Cash Flows on UTF Assets

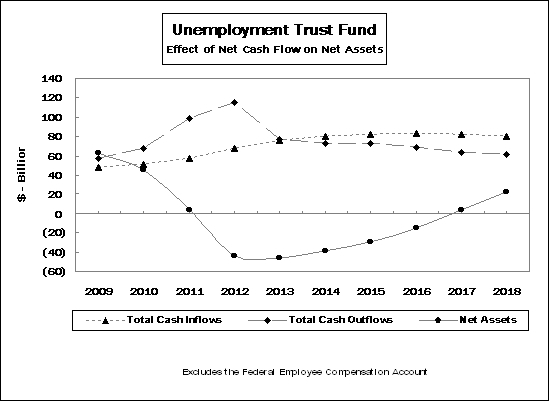

Chart II demonstrates the effect of these expected cash inflows and outflows on the net assets of the UTF over the ten year period ended September 30, 2018. Yearly projected total cash inflows, including interest earnings, and cash outflows are depicted, as well as the net effect of this cash flow on UTF assets.

Total cash inflows exceed cash outflows for all years projected after FY 2009, with this excess peaking in FY 2013. Starting at $64.7 billion in FY 2009, net UTF assets increase by 114.7% over the next nine years to $138.9 billion by the end of FY 2018.

Chart II

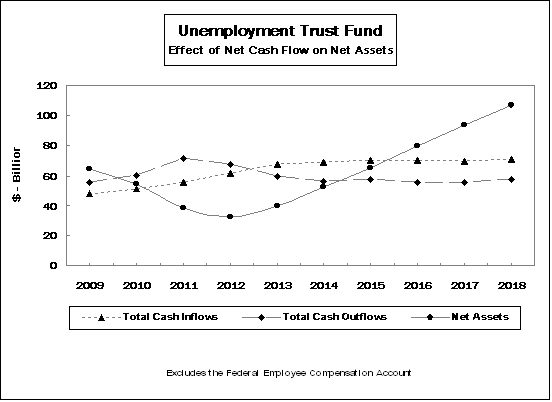

Recessionary Scenarios

Charts III and IV demonstrate the effect on accumulated UTF assets of projected total cash inflows and cash outflows of the UTF over the ten year period ending September 30, 2018, under mild and severe recession scenarios. Each scenario uses an open group, which includes current and future participants in the UI program. Charts III and IV assume increased rates of unemployment during mild and deep periods of recession.

Effect on UTF Assets of Mild Recession

The Department projects the effect of moderate recession on the cash inflows and outflows of the UTF. Under this scenario, which utilizes an unemployment rate peaking at 7.43% in FY 2011, net cash outflows including projected interest earnings and expenses from Federal sources are projected in FY 2009 through FY 2012. Net cash inflows are reestablished in FY 2013 and peak in FY 2016 with a drop in the unemployment rate to 5.11%. Net assets never fall below $32.4 billion and are within $32.4 billion of the balance under expected economic conditions by 2018. The crossover pattern remains the same when interest earnings are excluded.

Chart III

Effect on UTF Assets of Deep Recession

The Department also estimates the effect of severe recession on the cash inflows and outflows of the UTF. This scenario assumes a rising unemployment rate peaking at 10.14% in FY 2012. Under this scenario, net cash outflows including projected interest earnings and expenses from Federal sources are projected in FY 2009 through FY 2013, with the fund in a deficit situation from 2012 to 2016. The net assets of the UTF decrease from $62.6 billion in FY 2009 to negative $45.2 billion in 2013, a decline of $107.8 billion. State accounts without sufficient reserve balances to absorb negative cash flows would be forced to borrow funds from the FUA to meet benefit payment requirements. State borrowing demands could also deplete the FUA, which borrows from the ESAA and the EUCA until they are depleted. The FUA would then require advances from the general fund of the U.S. Treasury to provide for State borrowings. (See following discussion of State solvency measures.)

Net cash inflows are reestablished in FY 2014, with a drop in the unemployment rate to 7.26%. By the end of FY 2018, this positive cash flow has replenished UTF account balances to $22.0 billion. This example demonstrates the counter cyclical nature of the UI program, which experiences net cash outflows during periods of recession to be replenished through net cash inflows during periods of recovery. However, at the end of the projection period, net assets are $117.0 billion less than under expected economic conditions.

Chart IV

U.S. DEPARTMENT OF LABOR

SUPPLEMENTARY SOCIAL INSURANCE

INFORMATION

CASH INFLOW AND OUTFLOW OF THE

UNEMPLOYMENT TRUST FUND EXCLUDING THE FEDERAL

EMPLOYEES COMPENSATION ACCOUNT

FOR THE TEN YEAR PERIOD ENDING SEPTEMBER 30,

2018

(1) EXPECTED ECONOMIC CONDITIONS

(Dollars in thousands) |

|

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

Balance, start of year |

|

$72,100,304 |

$64,661,399 |

$68,131,002 |

$74,717,426 |

$82,808,250 |

$93,269,206 |

$102,651,295 |

$112,059,861 |

$119,141,289 |

$128,708,473 |

Cash inflow |

|

|

|

|

|

|

|

|

|

|

|

|

State unemployment taxes |

|

38,072,000 |

41,417,000 |

43,096,000 |

44,132,000 |

46,577,000 |

46,653,000 |

47,430,000 |

47,778,000 |

49,586,000 |

52,374,000 |

|

Federal unemployment taxes |

|

6,172,000 |

5,878,000 |

6,146,000 |

6,576,000 |

7,447,000 |

7,503,000 |

8,205,000 |

7,237,000 |

9,586,000 |

10,257,000 |

|

Interest on loans |

|

45,000 |

103,000 |

138,000 |

146,000 |

107,000 |

80,000 |

59,000 |

101,000 |

135,000 |

92,000 |

|

Deposits by the Railroad Retirement Board |

95,800 |

108,600 |

123,600 |

125,000 |

119,800 |

120,800 |

124,200 |

127,800 |

130,000 |

126,500 |

|

|

|

Total cash inflow excluding interest |

44,384,800 |

47,506,600 |

49,503,600 |

50,979,000 |

54,250,800 |

54,356,800 |

55,818,200 |

55,243,800 |

59,437,000 |

62,849,500 |

|

Interest on Federal securities |

|

3,239,026 |

3,059,153 |

3,258,347 |

3,559,654 |

4,029,380 |

4,704,935 |

5,256,206 |

5,636,059 |

6,216,956 |

6,729,081 |

|

|

|

Total cash inflow |

|

47,623,826 |

50,565,753 |

52,761,947 |

54,538,654 |

58,280,180 |

59,061,735 |

61,074,406 |

60,879,859 |

65,653,956 |

69,578,581 |

Cash outflow |

|

|

|

|

|

|

|

|

|

|

|

|

State unemployment benefits |

|

51,028,000 |

43,930,000 |

43,042,000 |

43,317,000 |

44,697,000 |

46,570,000 |

48,568,000 |

50,714,000 |

53,005,000 |

56,275,000 |

|

State administrative costs |

|

3,721,505 |

2,847,000 |

2,807,000 |

2,799,000 |

2,786,000 |

2,769,000 |

2,753,000 |

2,735,000 |

2,726,000 |

2,714,000 |

|

Federal administrative costs |

|

203,453 |

202,847 |

205,365 |

207,938 |

210,568 |

212,256 |

214,003 |

216,811 |

219,681 |

222,614 |

|

Interest on tax refunds |

|

3,188 |

2,973 |

3,082 |

3,270 |

3,743 |

3,932 |

4,388 |

3,925 |

5,250 |

5,651 |

|

Railroad Retirement Board withdrawals |

106,585 |

113,330 |

118,076 |

120,622 |

121,913 |

124,458 |

126,449 |

128,695 |

130,841 |

132,832 |

|

|

|

Total cash outflow |

|

55,062,731 |

47,096,150 |

46,175,523 |

46,447,830 |

47,819,224 |

49,679,646 |

51,665,840 |

53,798,431 |

56,086,772 |

59,350,097 |

|

|

|

Excess of total cash inflow excluding interest over total cash outflow |

|

(10,677,931) |

410,450 |

3,328,077 |

4,531,170 |

6,431,576 |

4,677,154 |

4,152,360 |

1,445,369 |

3,350,228 |

3,499,403 |

|

|

|

Excess of total cash inflow over total cash outflow |

|

(7,438,905) |

3,469,603 |

6,586,424 |

8,090,824 |

10,460,956 |

9,382,089 |

9,408,566 |

7,081,428 |

9,567,184 |

10,228,484 |

Balance, end of year |

|

$64,661,399 |

$68,131,002 |

$74,717,426 |

$82,808,250 |

$93,269,206 |

$102,651,295 |

$112,059,861 |

$119,141,289 |

$128,708,473 |

$138,936,957 |

|

|

|

Total unemployment rate |

|

5.58% |

5.35% |

5.03% |

4.85% |

4.80% |

4.80% |

4.80% |

4.80% |

4.80% |

4.80% |

U.S. DEPARTMENT OF LABOR

SUPPLEMENTARY SOCIAL INSURANCE

INFORMATION

CASH INFLOW AND OUTFLOW OF THE

UNEMPLOYMENT TRUST FUND EXCLUDING THE FEDERAL

EMPLOYEES COMPENSATION ACCOUNT

FOR THE TEN YEAR PERIOD ENDING SEPTEMBER 30,

2018

(2) MILD RECESSIONARY UNEMPLOYMENT RATE

(Dollars in thousands) |

|

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

Balance, start of year |

|

$72,100,304 |

$64,174,037 |

$54,659,117 |

$38,450,008 |

$32,406,538 |

$39,908,254 |

$52,395,150 |

$65,089,586 |

$79,595,289 |

$93,354,396 |

Cash inflow |

|

|

|

|

|

|

|

|

|

|

|

|

State unemployment taxes |

|

38,098,000 |

41,900,000 |

46,799,000 |

51,051,000 |

54,622,000 |

54,928,000 |

54,763,000 |

54,758,000 |

53,437,000 |

54,095,000 |

|

Federal unemployment taxes |

|

6,159,000 |

5,796,000 |

5,978,000 |

7,173,000 |

9,124,000 |

10,380,000 |

11,210,000 |

11,107,000 |

10,743,000 |

11,285,000 |

|

General revenue appropriation |

|

414,000 |

51,000 |

109,000 |

57,000 |

1,000 |

- |

- |

- |

- |

- |

|

Interest on loans |

|

44,000 |

169,000 |

636,000 |

1,192,000 |

1,343,000 |

1,181,000 |

1,052,000 |

917,000 |

768,000 |

618,000 |

|

Deposits by the Railroad Retirement Board |

95,800 |

108,600 |

123,600 |

125,000 |

119,800 |

120,800 |

124,200 |

127,800 |

130,000 |

126,500 |

|

|

|

Total cash inflow excluding interest |

44,810,800 |

48,024,600 |

53,645,600 |

59,598,000 |

65,209,800 |

66,609,800 |

67,149,200 |

66,909,800 |

65,078,000 |

66,124,500 |

|

Interest on Federal securities |

|

3,234,152 |

2,710,589 |

2,033,730 |

1,928,307 |

2,086,383 |

2,476,850 |

2,900,983 |

3,441,133 |

4,296,213 |

5,006,600 |

|

|

|

Total cash inflow |

|

48,044,952 |

50,735,189 |

55,679,330 |

61,526,307 |

67,296,183 |

69,086,650 |

70,050,183 |

70,350,933 |

69,374,213 |

71,131,100 |

Cash outflow |

|

|

|

|

|

|

|

|

|

|

|

|

State unemployment benefits |

|

51,924,000 |

56,898,000 |

68,416,000 |

64,126,000 |

56,445,000 |

53,348,000 |

54,147,000 |

52,702,000 |

52,517,000 |

54,912,000 |

|

State administrative costs |

|

3,734,000 |

3,033,000 |

3,146,000 |

3,111,650 |

3,012,400 |

2,909,600 |

2,862,300 |

2,791,700 |

2,741,700 |

2,722,300 |

|

Federal administrative costs |

|

203,453 |

202,847 |

205,365 |

207,938 |

210,568 |

212,256 |

214,003 |

216,811 |

219,681 |

222,614 |

|

Interest on tax refunds |

|

3,181 |

2,932 |

2,998 |

3,567 |

4,586 |

5,440 |

5,995 |

6,024 |

5,884 |

6,217 |

|

Railroad Retirement Board withdrawals |

106,585 |

113,330 |

118,076 |

120,622 |

121,913 |

124,458 |

126,449 |

128,695 |

130,841 |

132,832 |

|

|

|

Total cash outflow |

|

55,971,219 |

60,250,109 |

71,888,439 |

67,569,777 |

59,794,467 |

56,599,754 |

57,355,747 |

55,845,230 |

55,615,106 |

57,995,963 |

|

|

|

Excess of total cash inflow excluding interest over total cash outflow |

|

(11,160,419) |

(12,225,509) |

(18,242,839) |

(7,971,777) |

5,415,333 |

10,010,046 |

9,793,453 |

11,064,570 |

9,462,894 |

8,128,537 |

|

|

|

Excess of total cash inflow over total cash outflow |

|

(7,926,267) |

(9,514,920) |

(16,209,109) |

(6,043,470) |

7,501,716 |

12,486,896 |

12,694,436 |

14,505,703 |

13,759,107 |

13,135,137 |

Balance, end of year |

|

$64,174,037 |

$54,659,117 |

$38,450,008 |

$32,406,538 |

$39,908,254 |

$52,395,150 |

$65,089,586 |

$79,595,289 |

$93,354,396 |

$106,489,533 |

|

|

|

Total unemployment rate |

|

5.71% |

6.62% |

7.43% |

7.09% |

6.35% |

5.61% |

5.47% |

5.11% |

4.80% |

4.80% |

U.S. DEPARTMENT OF LABOR

SUPPLEMENTARY

SOCIAL INSURANCE INFORMATION

CASH INFLOW AND OUTFLOW

OF THE

UNEMPLOYMENT TRUST FUND EXCLUDING THE FEDERAL

EMPLOYEES COMPENSATION ACCOUNT

FOR THE TEN YEAR

PERIOD ENDING SEPTEMBER 30, 2018

(3) DEEP RECESSIONARY

UNEMPLOYMENT RATE

(Dollars in thousands) |

|

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

Balance, start of year |

|

$72,100,304 |

$62,558,151 |

$45,279,776 |

$3,870,099 |

$(43,717,343) |

$(45,231,242) |

$(38,241,644) |

$(29,140,004) |

$(14,904,722) |

$3,720,184 |

Cash inflow |

|

|

|

|

|

|

|

|

|

|

|

|

State unemployment taxes |

|

38,120,000 |

42,420,000 |

48,765,000 |

56,504,000 |

62,206,000 |

63,818,000 |

63,952,000 |

63,098,000 |

61,256,000 |

59,574,000 |

|

Federal unemployment taxes |

|

6,145,000 |

5,751,000 |

5,849,000 |

6,941,000 |

8,938,000 |

11,391,000 |

13,742,000 |

14,989,000 |

15,779,000 |

15,681,000 |

|

General revenue appropriation |

|

427,000 |

89,000 |

148,000 |

174,000 |

44,000 |

4,000 |

4,000 |

- |

- |

- |

|

Interest on loans |

|

45,000 |

247,000 |

1,187,000 |

2,868,000 |

3,744,000 |

3,783,000 |

3,728,000 |

3,574,000 |

3,171,000 |

2,743,000 |

|

Deposits by the Railroad Retirement Board |

95,800 |

108,600 |

123,600 |

125,000 |

119,800 |

120,800 |

124,200 |

127,800 |

130,000 |

126,500 |

|

|

|

Total cash inflow excluding interest |

|

44,832,800 |

48,615,600 |

56,072,600 |

66,612,000 |

75,051,800 |

79,116,800 |

81,550,200 |

81,788,800 |

80,336,000 |

78,124,500 |

|

Interest on Federal securities |

|

3,214,259 |

2,429,111 |

1,628,097 |

1,024,369 |

784,924 |

829,732 |

1,050,141 |

1,312,417 |

1,760,420 |

2,214,216 |

|

|

|

Total cash inflow |

|

48,047,059 |

51,044,711 |

57,700,697 |

67,636,369 |

75,836,724 |

79,946,532 |

82,600,341 |

83,101,217 |

82,096,420 |

80,338,716 |

Cash outflow |

|

|

|

|

|

|

|

|

|

|

|

|

State unemployment benefits |

|

53,522,000 |

64,864,000 |

94,933,000 |

109,606,000 |

70,933,000 |

66,671,000 |

67,554,000 |

63,424,000 |

58,741,000 |

58,231,000 |

|

State administrative costs |

|

3,754,000 |

3,140,000 |

3,551,000 |

3,685,800 |

3,280,650 |

3,143,250 |

3,096,900 |

2,988,300 |

2,871,350 |

2,803,900 |

|

Federal administrative costs |

|

203,453 |

202,847 |

205,365 |

207,938 |

210,568 |

212,256 |

214,003 |

216,811 |

219,681 |

222,614 |

|

Interest on tax refunds |

|

3,174 |

2,909 |

2,933 |

3,451 |

4,492 |

5,970 |

7,349 |

8,129 |

8,642 |

8,639 |

|

Interest on General Fund advances |

|

- |

- |

300,000 |

1,600,000 |

2,800,000 |

2,800,000 |

2,500,000 |

2,100,000 |

1,500,000 |

700,000 |

|

Railroad Retirement Board withdrawals |

106,585 |

113,330 |

118,076 |

120,622 |

121,913 |

124,458 |

126,449 |

128,695 |

130,841 |

132,832 |

|

|

|

Total cash outflow |

|

57,589,212 |

68,323,086 |

99,110,374 |

115,223,811 |

77,350,623 |

72,956,934 |

73,498,701 |

68,865,935 |

63,471,514 |

62,098,985 |

|

|

|

Excess of total cash inflow excluding interest over total cash outflow |

|

(12,756,412) |

(19,707,486) |

(43,037,774) |

(48,611,811) |

(2,298,823) |

6,159,866 |

8,051,499 |

12,922,865 |

16,864,486 |

16,025,515 |

|

|

|

Excess of total cash inflow over total cash outflow |

|

(9,542,153) |

(17,278,375) |

(41,409,677) |

(47,587,442) |

(1,513,899) |

6,989,598 |

9,101,640 |

14,235,282 |

18,624,906 |

18,239,731 |

|

Balance, end of year |

$62,558,151 |

$45,279,776 |

$3,870,099 |

$(43,717,343) |

$(45,231,242) |

$(38,241,644) |

$(29,140,004) |

$(14,904,722) |

$3,720,184 |

$21,959,915 |

|

|

|

Total unemployment rate |

|

5.86% |

7.30% |

9.10% |

10.14% |

7.81% |

7.26% |

7.05% |

6.43% |

5.62% |

5.25% |

States Minimally Solvent

Each State's accumulated UTF net assets or reserve balance should provide a defined level of benefit payments over a defined period. To be minimally solvent, a State's reserve balance should provide for one year's projected benefit payment needs based on the highest levels of benefit payments experienced by the State over the last twenty years. A ratio of 1.0 or greater prior to a recession indicates a state is minimally solvent. States below this level are vulnerable to exhausting their funds in a recession. States exhausting their reserve balance must borrow funds from the Federal Unemployment Account (FUA) to make benefit payments. During periods of high-sustained unemployment, balances in the FUA may be depleted. In these circumstances, FUA is authorized to borrow from the Treasury general fund.

Chart V presents the State by State results of this analysis at September 30, 2008 in descending order by ratio. As the table below illustrates, 29 state funds were below minimal solvency ratio at September 30, 2008.

Chart V

Minimally Solvent |

Not Minimally Solvent |

State |

Ratio |

State |

Ratio |

Wyoming |

2.99 |

West Virginia |

0.99 |

New Mexico |

2.90 |

Delaware |

0.93 |

Mississippi |

2.84 |

Alabama |

0.89 |

Utah |

2.69 |

Maryland |

0.89 |

Louisiana |

2.59 |

Florida |

0.88 |

Montana |

2.49 |

Virginia |

0.83 |

Oklahoma |

2.42 |

Tennessee |

0.72 |

Oregon |

2.01 |

South Dakota |

0.66 |

Washington |

1.98 |

Illinois |

0.64 |

Nebraska |

1.95 |

Minnesota |

0.57 |

Iowa |

1.67 |

Texas |

0.54 |

Maine |

1.66 |

Idaho |

0.53 |

North Dakota |

1.62 |

Massachusetts |

0.53 |

Hawaii |

1.59 |

Virgin Islands |

0.53 |

Arizona |

1.54 |

Connecticut |

0.51 |

Kansas |

1.54 |

Pennsylvania |

0.45 |

Alaska |

1.47 |

Arkansas |

0.39 |

District of Columbia |

1.47 |

Wisconsin |

0.37 |

Nevada |

1.25 |

North Carolina |

0.34 |

Puerto Rico |

1.21 |

Kentucky |

0.32 |

Vermont |

1.19 |

Missouri |

0.28 |

New Hampshire |

1.14 |

New Jersey |

0.28 |

Georgia |

1.11 |

Rhode Island |

0.28 |

Colorado |

1.00 |

California |

0.22 |

|

|

South Carolina |

0.20 |

|

|

Ohio |

0.19 |

|

|

New York |

0.16 |

|

|

Indiana |

0.12 |

|

|

Michigan |

0.00 |

Black Lung Disability Benefit Program

The Black Lung Disability Benefit Program provides for compensation, medical and survivor benefits for eligible coal miners who are disabled due to pneumoconiosis (black lung disease) arising out of their coal mine employment. The U.S. Department of Labor operates the Black Lung Disability Benefit Program. The Black Lung Disability Trust Fund (BLDTF) provides benefit payments to eligible coal miners disabled by pneumoconiosis when no responsible mine operator can be assigned the liability.

Program Administration and Funding

Black lung disability benefit payments are funded by excise taxes from coal mine operators based on the sale of coal, as are the fund's administrative costs. These taxes are collected by the Internal Revenue Service and transferred to the BLDTF, which was established under the authority of the Black Lung Benefits Revenue Act, and administered by the U.S. Department of the Treasury. The Black Lung Benefits Revenue Act provides for repayable advances to the BLDTF from the general fund of the Treasury, in the event that BLDTF resources are not adequate to meet program obligations.

Program Finances and Sustainability

At September 30, 2008, total liabilities of the Black Lung Disability Trust Fund exceeded assets by $10.4 billion. This deficit fund balance represented the accumulated shortfall of excise taxes necessary to meet benefit payment and interest expenses. This shortfall was funded by repayable advances to the BLDTF, which are repayable with interest. Outstanding advances at September 30, 2008 were $10.5 billion, bearing interest rates ranging from 4.250 to 13.875 percent. Excise tax revenues of $652.6 million, benefit payment expense of $267.0 million and interest expense of $739.5 million were recognized for the year ended September 30, 2008.

As discussed in Note 1.L.3, DOL recognized a liability for disability benefits to the extent of unpaid benefits applicable to the current period. Accrued disability benefits payable at September 30, 2008 were $19.5 million. Although no liability was recognized for future payments to be made to present and future program participants beyond the due and payable amounts accrued at year end, future estimated cash inflows and outflows of the BLDTF are tracked by the Department for budgetary purposes. The significant assumptions used in the projections are coal excise tax revenue estimates, number of beneficiaries, life expectancy, medical cost inflation, Federal civilian pay raises, and the interest rate on new repayable advances from Treasury. These projections are sensitive to changes in the tax rate and changes in interest rates on repayable advances from Treasury.

These projections, made over the thirty-two year period ending September 30, 2040, indicate that cash inflows from excise taxes will exceed cash outflows for benefit payments and administrative expenses for each period projected. Cumulative net cash inflows are projected to reach $14.1 billion by the year 2040. However, when interest payments required to finance the BLDTF's repayable advances are applied against this surplus cash inflow, the BLDTF's cash flow turns negative during each of the thirty-two periods included in the projections. Net cash outflows after interest payments are projected to reach $53.1 billion by the end of the year 2040, increasing the BLDTF's deficit to $49.4 billion at September 30, 2040. (See Chart I on following page)

The net present value of future projected benefit payments and other cash inflow and outflow activities together with the fund's deficit positions as of September 30, 2008, 2007, 2006, 2005, and 2004 are presented in the Statement of Social Insurance.

The projected decrease in cash inflows in the year 2014 and thereafter is the result of a scheduled reduction in the tax rate on the sale of coal. This rate reduction is projected to result in a fifty-one percent decrease in the amount of excise taxes collected between the years 2013 and 2015. The cumulative effect of this change is estimated to be in excess of $11.9 billion by the year 2040.

Yearly cash inflows and outflows are presented in the table on the following page.

The Energy Improvement and Extension Act of 2008, enacted on October 3, extended the higher coal excise tax rates for an additional five years from January 1, 2014 to December 31, 2018. The Act also authorized the refinancing of high interest rate Advances to U.S. Treasury and replaced them with lower interest rate zero coupon bonds. Additional income from the extension of the higher excise tax amounted to $1.8 billion. The decrease in effective interest payments amounted to $11.121 billion. These changes resulted in a zero fund balance at the end of the projection period.

Refer to Note 23 in the Notes to Consolidated Financial Statements for additional discussion regarding the effects of the Act on the Trust Fund and the Statement of Social Insurance.

U.S. DEPARTMENT OF LABOR

SUPPLEMENTARY SOCIAL INSURANCE INFORMATION

CASH INFLOW AND OUTFLOW OF THE BLACK LUNG DISABILITY TRUST

FUND

FOR THE THIRTY-FOUR YEAR PERIOD ENDING SEPTEMBER 30, 2040

(Dollars in thousands) |

|

2009 |

2010 |

2011 |

2012 |

2013 |

2014 - 2040 |

Total |

Balance, start of year |

|

$(10,439,186) |

$(10,853,741) |

$(11,266,163) |

$(11,663,387) |

$(12,051,321) |

$(12,439,987) |

$(10,439,186) |

Cash inflow |

|

|

|

|

|

|

|

|

|

Excise taxes |

|

653,000 |

661,000 |

681,000 |

696,000 |

702,000 |

10,747,269 |

14,140,269 |

|

|

Total cash inflow |

|

653,000 |

661,000 |

681,000 |

696,000 |

702,000 |

10,747,269 |

14,140,269 |

Cash outflow |

|

|

|

|

|

|

|

|

|

Disabled coal miners benefits |

253,173 |

236,527 |

220,378 |

204,798 |

189,845 |

2,066,602 |

3,171,323 |

|

Administrative costs |

|

57,683 |

59,716 |

59,716 |

59,716 |

59,716 |

1,048,676 |

1,345,223 |

|

|

Cash outflows before interest payments |

310,856 |

296,243 |

280,094 |

264,514 |

249,561 |

3,115,278 |

4,516,546 |

|

|

Cash inflow over cash outflow before interest payments |

342,144 |

364,757 |

400,906 |

431,486 |

452,439 |

7,631,991 |

9,623,723 |

|

Interest on advances |

|

756,699 |

777,179 |

798,130 |

819,420 |

841,105 |

44,571,557 |

48,564,090 |

|

|

Total cash outflow |

|

1,067,555 |

1,073,422 |

1,078,224 |

1,083,934 |

1,090,666 |

47,686,835 |

53,080,636 |

|

|

Total cash outflow over total cash inflow |

(414,555) |

(412,422) |

(397,224) |

(387,934) |

(388,666) |

(36,939,566) |

(38,940,367) |

Balance, end of year |

|

$(10,853,741) |

$(11,266,163) |

$(11,663,387) |

$(12,051,321) |

$(12,439,987) |

$(49,379,553) |

$(49,379,553) |

STATEMENT OF BUDGETARY RESOURCES

The principal Statement of Budgetary Resources combines the availability, status and outlay of DOL's budgetary resources during FY 2008 and 2007. Presented on the following pages is the disaggregation of this combined information for each of the Department's major budget accounts.

COMBINING STATEMENT OF BUDGETARY RESOURCES

For the Year Ended September 30, 2008

(Dollars in thousands) |

|

|

|

|

Employment and Training Administration |

Employment Standards Administration |

Office of Job Corps |

Occupational Safety and Health Administration; |

Bureau of Labor Statistics |

Mine Safety and Health Administration |

Employee Benefits Security Administration |

Veterans' Employment and Training |

Other Departmental Programs |

Total |

BUDGETARY RESOURCES |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Unobligated balance, brought forward, October 1 |

|

$2,403,760 |

$1,837,745 |

$- |

$16,286 |

$ 9,060 |

$1,271 |

$16,976 |

$5,521 |

$21,162 |

$4,311,781 |

|

Recoveries of prior year unpaid obligations |

|

358,350 |

11,401 |

- |

8,309 |

7,506 |

5,719 |

1,797 |

989 |

24,124 |

418,195 |

|

Budget authority |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Appropriations received |

|

|

|

|

52,202,263 |

3,075,668 |

1,626,855 |

494,641 |

476,861 |

339,862 |

141,790 |

31,522 |

394,540 |

58,784,002 |

|

|

Borrowing authority |

|

|

|

|

|

- |

426,000 |

- |

- |

- |

- |

- |

- |

- |

426,000 |

|

|

Spending authority from offsetting collections |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Earned |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Collected |

|

|

|

|

|

74,527 |

2,645,916 |

371 |

2,354 |

5,584 |

1,408 |

12,460 |

124 |

204,692 |

2,947,436 |

|

|

|

|

Change in receivables from Federal sources |

|

- |

(844) |

- |

14 |

- |

- |

- |

- |

(3,166) |

(3,996) |

|

|

|

Change in unfilled customer orders |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Advance received |

|

|

|

|

- |

1,531 |

- |

- |

- |

- |

- |

- |

781 |

2,312 |

|

|

|

|

Without advance from Federal sources |

|

- |

- |

- |

- |

- |

- |

- |

- |

- |

- |

|

|

|

Expenditure transfers from trust funds |

|

3,436,272 |

34,783 |

- |

- |

75,120 |

- |

- |

195,247 |

30,965 |

3,772,387 |

|

Total budget authority |

|

|

|

|

|

55,713,062 |

6,183,054 |

1,627,226 |

497,009 |

557,565 |

341,270 |

154,250 |

226,893 |

627,812 |

65,928,141 |

|

Non expenditure transfers, net |

|

|

|

(7,200) |

(674) |

(13,215) |

(1,035) |

(514) |

(2,182) |

(177) |

- |

15,247 |

(9,750) |

|

Temporarily not available pursuant to Public Law |

|

(62,962) |

(135,595) |

- |

- |

- |

- |

- |

- |

- |

(198,557) |

|

Permanently not available |

|

|

|

|

(766,612) |

(11,546) |

(28,421) |

(13,484) |

(11,090) |

(6,382) |

(3,334) |

(754) |

(11,283) |

(852,906) |

Total budgetary resources |

|

|

|

$57,638,398 |

$7,884,385 |

$1,585,590 |

$507,085 |

$562,527 |

$339,696 |

$169,512 |

$232,649 |

$677,062 |

$69,596,904 |

STATUS OF BUDGETARY RESOURCES |

|

|

|

|

|

|

|

|

|

|

|

|

Obligations incurred |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Direct |

|

|

|

|

|

$56,045,818 |

$3,183,078 |

$1,026,949 |

$491,592 |

$547,532 |

$337,062 |

$154,382 |

$228,869 |

442,017 |

$62,457,299 |

|

|

Reimbursable |

|

|

|

|

|

32,032 |

2,719,549 |

317 |

1,483 |

5,565 |

1,169 |

12,130 |

- |

209,932 |

2,982,177 |

|

Total obligations incurred |

|

|

|

|

56,077,850 |

5,902,627 |

1,027,266 |

493,075 |

553,097 |

338,231 |

166,512 |

228,869 |

651,949 |

65,439,476 |

|

Unobligated balances available |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Apportioned |

|

|

|

|

|

524,223 |

1,411,223 |

558,324 |

15 |

- |

29 |

33 |

49 |

5,376 |

2,499,272 |

|

|

Exempt from apportionment |

|

|

|

- |

239,306 |

- |

- |

- |

- |

- |

- |

93 |

239,399 |

|

Total unobligated balances available |

|

|

524,223 |

1,650,529 |

558,324 |

15 |

- |

29 |

33 |

49 |

5,469 |

2,738,671 |

|

Unobligated balances not available |

|

|

|

1,036,325 |

331,229 |

- |

13,995 |

9,430 |

1,436 |

2,967 |

3,731 |

19,644 |

1,418,757 |

Total status of budgetary resources |

|

|

$57,638,398 |

$7,884,385 |

$1,585,590 |

$507,085 |

$562,527 |

$339,696 |

$169,512 |

$232,649 |

$677,062 |

$69,596,904 |

CHANGE IN OBLIGATED BALANCE |

|

|

|

|

|

|

|

|

|

|

|

|

|

Obligated balance, net |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Unpaid obligations, brought forward, October 1 |

|

$8,370,953 |

$292,207 |

$- |

$95,692 |

$75,289 |

$48,610 |

$40,172 |

$56,100 |

$390,505 |

$9,369,528 |

|

|

Less uncollected customer payments from Federal sources, |

|

|

|

|

|

|

|

|

|

|

|

|

brought forward, October 1 |

|

|

|

(1,242,900) |

(1,027) |

- |

(8,099) |

- |

- |

- |

- |

(9,342) |

(1,261,368) |

|

Total unpaid obligated balance, net |

|

|

|

7,128,053 |

291,180 |

- |

87,593 |

75,289 |

48,610 |

40,172 |

56,100 |

381,163 |

8,108,160 |

|

Obligations incurred, net |

|

|

|

|

56,077,850 |

5,902,627 |

1,027,266 |

493,075 |

553,097 |

338,231 |

166,512 |

228,869 |

651,949 |

65,439,476 |

|

Less gross outlays |

|

|

|

|

|

(55,951,639) |

(5,892,378) |

(755,877) |

(493,520) |

(546,931) |

(346,743) |

(154,261) |

(222,385) |

(663,876) |

(65,027,610) |

|

Less recoveries of prior year unpaid obligations, actual |

|

(358,350) |

(11,401) |

- |

(8,309) |

(7,506) |

(5,719) |

(1,797) |

(989) |

(24,124) |

(418,195) |

|

Change in uncollected customer payments from Federal sources |

66,456 |

844 |

- |

(14) |

- |

- |

- |

- |

10,731 |

78,017 |

|

Obligated balance, net, end of period |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Unpaid obligations |

|

|

|

|

|

8,138,814 |

291,055 |

271,389 |

86,938 |

73,949 |

34,379 |

50,626 |

61,595 |

354,454 |

9,363,199 |

|

|

Less uncollected customer payments from Federal sources |

(1,176,444) |

(183) |

- |

(8,113) |

- |

- |

- |

- |

1,389 |

(1,183,351) |

|

Total unpaid obligated balance, net, end of period |

|

$6,962,370 |

$290,872 |

$271,389 |

$78,825 |

$73,949 |

$34,379 |

$50,626 |

$61,595 |

$355,843 |

$8,179,848 |

NET OUTLAYS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross outlays |

|

|

|

|

|

$55,951,639 |

$5,892,378 |

$755,877 |

$493,520 |

$546,931 |

$346,743 |

$154,261 |

$222,385 |

$663,876 |

$65,027,610 |

|

|

Less offsetting collections |

|

|

|

(3,577,254) |

(2,682,231) |

(371) |

(2,354) |

(80,704) |

(1,408) |

(12,460) |

(195,370) |

(236,438) |

(6,788,590) |

|

|

Less distributed offsetting receipts |

|

|

(736,291) |

(4,589) |

- |

- |

- |

- |

- |

- |

- |

(740,880) |

|

|

Net outlays |

|

|

|

|

|

$51,638,094 |

$3,205,558 |

$755,506 |

$491,166 |

$466,227 |

$345,335 |

$141,801 |

$27,015 |

$427,438 |

$57,498,140 |

COMBINING STATEMENT OF BUDGETARY RESOURCES

For the Year Ended September 30, 2007

(Dollars in thousands) |

|

|

|

|

Employment and Training Administration |

Employment Standards Administration |

Occupational Safety and Health Administration |

Bureau of Labor Statistics |

Mine Safety and Health Administration |

Employee Benefits Security Administration |

Veterans' Employment and Training |

Other Departmental Programs |

Total |

BUDGETARY RESOURCES |

|

|

|

|

|

|

|

|

|

|

|

|

|

Unobligated balance, brought forward, October 1 |

|

$2,387,191 |

$1,715,502 |

$21,835 |

$9,057 |

$22,740 |

$2,077 |

$2,848 |

$35,036 |

$4,196,286 |

|

Recoveries of prior year unpaid obligations |

|

160,292 |

9,100 |

8,739 |

7,130 |

2,971 |

2,798 |

4,428 |

25,215 |

220,673 |

|

Budget authority |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Appropriations received |

|

|

|

|

52,188,334 |

2,903,394 |

486,925 |

471,056 |

301,570 |

141,573 |

29,244 |

399,705 |

56,921,801 |

|

|

Borrowing authority |

|

|

|

|

|

426,000 |

- |

- |

- |

- |

- |

- |

- |

426,000 |

|

|

Spending authority from offsetting collections |

|

|

|

|

|

|

|

|

|

|

|

|

|

Earned |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Collected |

|

|

|

|

|

74,576 |

2,501,508 |

2,766 |

6,636 |

1,322 |

11,142 |

65 |

189,572 |

2,787,587 |

|

|

|

|

Change in receivables from Federal sources |

|

(1) |

(2,564) |

(1,027) |

- |

(15) |

- |

- |

(1,687) |

(5,294) |

|

|

|

Change in unfilled customer orders |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Advance received |

|

|

|

|

- |

2,907 |

- |

- |

- |

- |

- |

(3,126) |

(219) |

|

|

|

|

Without advance from Federal sources |

|

- |

- |

- |

- |

- |

- |

- |

- |

- |

|

|

|

Expenditure transfers from trust funds |

|

3,328,586 |

35,620 |

- |

75,930 |

- |

- |

193,945 |

31,461 |

3,665,542 |

|

Total budget authority |

|

|

|

|

|

56,017,495 |

5,440,865 |

488,664 |

553,622 |

302,877 |

152,715 |

223,254 |

615,925 |

63,795,417 |

|

Non expenditure transfers, net |

|

|

|

(822,728) |

425,460 |

(1,589) |

(244) |

(147) |

6,849 |

- |

2,772 |

(389,627) |

|

Temporarily not available pursuant to Public Law |

|

(8,454,205) |

(19,799) |

- |

- |

- |

- |

- |

- |

(8,474,004) |

|

Permanently not available |

|

|

|

|

(105,951) |

(2,804) |

(7,243) |

(2,505) |

(628) |

(1,163) |

(1,334) |

(10,563) |

(132,191) |

Total budgetary resources |

|

|

|

$49,182,094 |

$7,568,324 |

$510,406 |

$567,060 |

$327,813 |

$163,276 |

$229,196 |

$668,385 |

$59,216,554 |

STATUS OF BUDGETARY RESOURCES |

|

|

|

|

|

|

|

|

|

|

|

Obligations incurred |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Direct |

|

|

|

|

|

$46,722,026 |

$3,108,239 |

$492,669 |

$551,634 |

$325,427 |

$135,303 |

$223,675 |

$461,098 |

$52,020,071 |

|

|

Reimbursable |

|

|

|

|

|

56,308 |

2,622,340 |

1,451 |

6,366 |

1,115 |

10,997 |

- |

186,125 |

2,884,702 |

|

Total obligations incurred |

|

|

|

|

46,778,334 |

5,730,579 |

494,120 |

558,000 |

326,542 |

146,300 |

223,675 |

647,223 |

54,904,773 |

|

Unobligated balances available |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Apportioned |

|

|

|

|

|

1,000,005 |

1,414,932 |

58 |

305 |

170 |

14,098 |

677 |

10,744 |

2,440,989 |

|

|

Exempt from apportionment |

|

|

|

- |

178,811 |

- |

- |

- |

- |

- |

137 |

178,948 |

|

Total unobligated balances available |

|

|

1,000,005 |

1,593,743 |

58 |

305 |

170 |

14,098 |

677 |

10,881 |

2,619,937 |

|

Unobligated balances not available |

|

|

|

1,403,755 |

244,002 |

16,228 |

8,755 |

1,101 |

2,878 |

4,844 |

10,281 |

1,691,844 |

Total status of budgetary resources |

|

|

$49,182,094 |

$7,568,324 |

$510,406 |

$567,060 |

$327,813 |

$163,276 |

$229,196 |

$668,385 |

$59,216,554 |

CHANGE IN OBLIGATED BALANCE |

|

|

|

|

|

|

|

|

|

|

|

|

Obligated balance,net |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Unpaid obligations, brought forward, October 1 |

|

$8,004,128 |

$295,434 |

$85,115 |

$74,100 |

$24,067 |

$43,819 |

$60,111 |

$433,670 |

$9,020,444 |

|

|

Less uncollected customer payments from Federal sources, |

|

|

|

|

|

|

|

|

|

|

|

brought forward, October 1 |

|

|

|

(1,208,324) |

(5,618) |

(9,126) |

- |

(15) |

- |

- |

(13,769) |

(1,236,852) |

|

Total unpaid obligated balance, net |

|

|

|

6,795,804 |

289,816 |

75,989 |

74,100 |

24,052 |

43,819 |

60,111 |

419,901 |

7,783,592 |

|

Obligations incurred, net |

|

|

|

|

46,778,334 |

5,730,579 |

494,120 |

558,000 |

326,542 |

146,300 |

223,675 |

647,223 |

54,904,773 |

|

Less gross outlays |

|

|

|

|

|

(46,251,217) |

(5,724,706) |

(474,804) |

(549,681) |

(299,028) |

(147,149) |

(223,258) |

(665,173) |

(54,335,016) |

|

Less recoveries of prior year unpaid obligations, actual |

|

(160,292) |

(9,100) |

(8,739) |

(7,130) |

(2,971) |

(2,798) |

(4,428) |

(25,215) |

(220,673) |

|

Change in uncollected customer payments from Federal sources |

(34,576) |

4,591 |

1,027 |

- |

15 |

- |

- |

4,427 |

(24,516) |

|

Obligated balance, net, end of period |

|

|

|

|

|

|

|

|

|

|

|

|

|

Unpaid obligations |

|

|

|

|

|

8,370,953 |

292,207 |

95,692 |

75,289 |

48,610 |

40,172 |

56,100 |

390,505 |

9,369,528 |

|

|

Less uncollected customer payments from Federal sources |

(1,242,900) |

(1,027) |

(8,099) |

- |

- |

- |

- |

(9,342) |

(1,261,368) |

|

Total unpaid obligated balance, net, end of period |

|

$7,128,053 |

$291,180 |

$87,593 |

$75,289 |

$48,610 |

$40,172 |

$56,100 |

$381,163 |

$8,108,160 |

NET OUTLAYS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross outlays |

|

|

|

|

|

$46,251,217 |

$5,724,706 |

$474,804 |

$549,681 |

$299,028 |

$147,149 |

$223,258 |

$665,173 |

$54,335,016 |

|

|

Less offsetting collections |

|

|

|

(3,368,584) |

(2,542,063) |

(2,766) |

(82,566) |

(1,322) |

(11,142) |

(194,010) |

(217,907) |

(6,420,360) |

|

|

Less distributed off setting receipts |

|

|

(761,562) |

(6,388) |

(170) |

(12) |

(49) |

(24,168) |

- |

(2,662) |

(795,011) |

|

|

Net outlays |

|

|

|

|

|

$42,121,071 |

$3,176,255 |

$471,868 |

$467,103 |

$297,657 |

$111,839 |

$29,248 |

$444,604 |

$47,119,645 |

|

|

|

|