This is a printer friendly version.

Statement of Steven A. Kandarian

Executive Director

Pension Benefit Guaranty Corporation

before the

Subcommittee on Oversight

Committee on Ways and Means

U.S. House of Representatives

Mr. Chairman, Mr. Coyne, and Members of the Subcommittee:

It is a pleasure to appear before this Subcommittee today. I became Executive Director of the PBGC on December 3, 2001, a little over six months ago. You have asked me to provide you with information on the status of defined benefit plans.

Defined benefit plans have historically played an essential role in the three-legged stool of retirement income. The hearings you are holding today provide a welcome focus on the future role of defined benefit plans.

Overview of PBGC

I would like to take a few minutes to give you some background on the PBGC and its role in the pension system. PBGC was created by ERISA, the Employee Retirement Income Security Act of 1974, to guarantee private defined benefit pension plans that terminate without sufficient assets. Defined benefit plans provide a monthly retirement benefit, usually based on salary and years of service. The benefit amount does not depend on investment performance.

PBGC is one of the three so-called "ERISA agencies" with jurisdiction over private pension plans. The other two agencies are the Department of the Treasury (including the Internal Revenue Service) and the Department of Labor's Pension and Welfare Benefits Administration (PWBA). Treasury and PWBA deal with both defined benefit plans and defined contribution plans, including 401(k) plans. PBGC deals only with defined benefit plans, and only to a limited extent, as guarantor of benefits in underfunded plans that terminate. PBGC has very limited regulatory or enforcement authority over ongoing plans; the authority PBGC does have relates to certain employer reporting requirements and to determining whether a plan should be terminated to protect the insurance program.

PBGC protects the benefits of about 44 million participants and beneficiaries in slightly more than 35,000 ongoing defined benefit pension plans. When a plan insured by PBGC terminates without sufficient assets, PBGC becomes trustee of the plan and pays plan benefits, subject to statutory limits. For the vast majority of participants in PBGC-trusteed plans, plan benefits are paid in full. On average, participants receive over 94 percent of the benefits they had earned at termination. However, some participants receive a considerably smaller portion of their earned benefit. In addition, the 94 percent figure does not take into consideration benefits for which the participant had not yet satisfied all conditions at the time of termination, such as 30-and-out benefits

At the end of FY 2001, PBGC was responsible for paying current or future pension benefits to about 624,000 people in terminated plans, and payments, for the first time, exceeded $1 billion. PBGC has added over 140,000 new participants already in this fiscal year.

PBGC is a wholly-owned federal government corporation. It operates under the guidance of a three-member Board of Directors — the Secretary of Labor, who is the Chair, and the Secretaries of Commerce and the Treasury.

PBGC receives no funds from general tax revenues. Operations are financed by insurance premiums set by Congress and paid by sponsors of defined benefit plans, assets from pension plans trusteed by PBGC, investment income, and recoveries from the companies formerly responsible for the trusteed plans. There is a two-part annual premium for single-employer plans -- a flat-rate premium of $19 per plan participant plus a variable-rate premium of $9 per $1,000 of the plan's unfunded vested benefits. PBGC has a separate, smaller insurance program for multiemployer plans, which are collectively bargained plans maintained by two or more unrelated employers.

PBGC's statutory mandate is: (1) to encourage the continuation and maintenance of voluntary private pension plans for the benefit of their participants, (2) to provide for the timely and uninterrupted payment of pension benefits to participants and beneficiaries under PBGC-insured plans, and (3) to maintain premiums at the lowest level consistent with carrying out the agency's statutory obligations.

Financial Condition of the PBGC

For its first 21 years, PBGC operated at a deficit. Beginning in 1996, PBGC has gradually built up a surplus as a result of legislative reforms, a strong economy, good returns on investments, and no major terminations from 1996-2000. PBGC had a surplus of $9.7 billion in its single-employer program at the end of fiscal 2000 (September 30, 2000). At the end of fiscal 2001 (September 30, 2001), the surplus had dropped to approximately $7.7 billion. As of April 30, our unaudited surplus had fallen to under $5 billion.

Net Position

FY 1990 - 2002

(Unaudited Projection)

NOTE: PBGC was in deficit for all years prior to 1990

Source: PBGC Annual Reports (1990 - 2001), 2002 projection

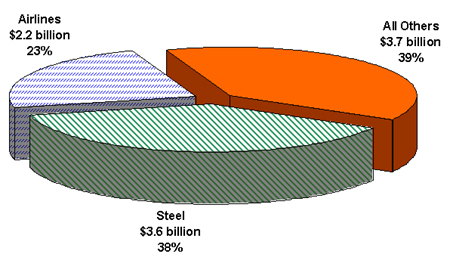

I'm concerned that our surplus may decline even further. Including the approximately $1.6 billion in claims from the LTV plans, the steel industry now accounts for about 38% of all claims against PBGC.

And we still face over another $9 billion in underfunding in the steel industry, nearly half of which is in steel companies that are in bankruptcy proceedings. We also face large amounts of underfunding in troubled companies in the airline and retail sectors.

PBGC Claims

1975 - 2002

SOURCE: PBGC Annual Reports (1990 - 2001), 2002 projection

Integrated Steel Plan Underfunding

SOURCE: PBGC Analysis of Actuarial Valuation Reports

Administrative Workload

Not only does the PBGC face a challenge financially, we face a challenge administratively. Large plan terminations have always been, and continue to be, the single most important factor determining PBGC's workload as well as its financial condition. PBGC became responsible for 104 plans with 89,000 participants last year, the largest number of new participants in PBGC's 27-year history. This year, we already have become responsible for over 140,000 new participants, and the end-of-year figure could be as high as 200,000. Little relief is in sight. If the plans of some of the troubled steel companies, airlines and others are terminated, new participants coming to PBGC in fiscal year 2003 could exceed this year's 200,000 new participant figure.

New Participants in Trusteed Plans

Fiscal Year 1988 - 2003 (projected)

SOURCE: PBGC Insurance Operations Department Reports

PBGC Actions to Address these Problems

We are taking steps to deal with this financial and administrative challenge. From a financial perspective, PBGC is closely monitoring troubled companies with underfunded plans. And PBGC is carefully examining each situation to determine if PBGC must terminate plans now in order to avoid even greater losses to the PBGC insurance program in the future. PBGC is totally financed by our premium payers -- the sponsors of defined benefit plans. We have an obligation to those premium payers to be fiscally responsible and take the necessary difficult actions to keep PBGC financially sound.

From an administrative viewpoint, we continue to accelerate our use of computer technology, contractors, and other measures to get participants into pay status as soon as they are eligible, to reduce waiting times for final benefit determinations, and to provide superior customer service. Participants feel a great deal of stress when their pension plan terminates, frequently at the same time they lose their jobs. PBGC should be a source of reassurance, not another source of stress. To this end, we are both continually learning from what participants and plan sponsors tell us and proactively designing new ways of providing better information. For example, in LTV, for the first time, we sent out letters to participants before we took over the plan so they would know what to expect.

Trends in Defined Benefit Plans

I would now like to turn to what is happening to defined benefits plans.

Number of Defined Benefit Plans

The percentage of private-sector workers with pension coverage in their current jobs has remained constant at just under 50 percent since the mid-1970s. But there has been a large and continuing shift away from defined benefit plans to defined contribution plans. The number of PBGC-insured defined benefit plans peaked in 1985 at about 114,000. Since then there has been a sharp decline to slightly more than 35,000 plans in 2001, a decline of almost 70 percent.

SOURCE: PBGC Premium Filings

This reduction in the number of plans has not been proportional across all plan sizes. Plans with fewer than 100 participants have shown the most marked decline, from about 90,000 in 1985 to 20,500 in 2001. There also has been a sharp decline for plans with between 100 and 999 participants, from more than 19,000 in 1985 to less than 10,000 in 2001.

In marked contrast to the trends for plans with fewer than 1,000 participants, the number of plans with more than 1,000 participants has shown modest growth. Since 1980, the number of PBGC-insured plans with between 1,000 and 9,999 participants has grown by about 1 percent, from 4,017 to 4,070 in 2001. The number of plans with at least 10,000 participants has grown from 469 in 1980 to 809 in 2001, an increase of 72 percent.

The growth in the number of large plans is attributable to two factors. First, the rapid increase in inactive participants (retirees and separated vested participants) has pushed some plans into higher size categories. Second, in instances where one employer maintained more than one plan, frequently as a result of corporate mergers and acquisitions, the employer has merged those plans.

Number of Participants

In contrast to the dramatic reduction in the total number of plans, the total number of participants in PBGC-insured defined benefit plans has shown modest growth. In 1980, there were 35.5 million participants. By 2001, this number had increased to about 44 million.

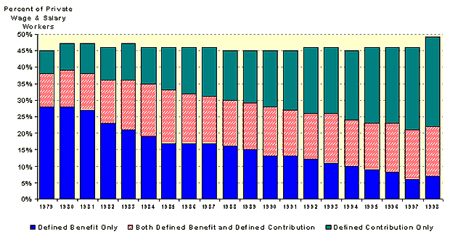

These numbers, however, mask the downward trend in the defined benefit system because total participants include not only active workers but also retirees (or their surviving spouses) and separated vested participants. The latter two categories of participants reflect past coverage patterns in defined benefit plans. A better forward-looking measure is the trend in the number of active participants, workers currently earning pension accruals. Here, the numbers continue to decline.

In 1985, there were 29.0 million active participants in defined benefit plans; by 1998, this number had fallen to an estimated 23.0 million, a decrease of 21 percent. At the same time, the number of inactive participants has been growing. In 1985, inactive participants accounted for only 27 percent of total participants in defined benefit plans. This number has increased to 45 percent by 1998. If this trend continues, by the year 2003 the number of inactive participants will exceed the number of active workers.

Ratio of Participants in

Defined Benefit Pension Plans

1985 - 2006 (estimated)

SOURCE: U.S. Department of Labor, Pension Welfare & Benefits Administration,

Abstract of 1998 Form 5500 Annual Reports, Winter 2001 - 2002

Decline of Defined Benefit Plans

The percentage of the workforce participating in either a defined benefit or defined contribution pension plan has not changed appreciably in the last 20 years. But the mix has changed. The percentage of the private sector workforce that has a defined benefit plan declined from 38 percent in 1980 to 22 percent in 1998. In 1980, over 80 percent of workers with a pension plan had a defined benefit plan. By 1998, that percentage had dropped to less than 50 percent. In 1980, about two-thirds of workers who had a defined benefit plan had no other employer-sponsored plan; by 1998, that ratio had reversed with only about one-third having no other plan. As defined benefit plans declined, 401(k) plans, a type of defined contribution plan, grew. Introduced in the early 1980s, the number of 401(k) plans grew from 17,000 in 1984 to over 300,000 in 1998.

Private Workforce Participation in

Defined Benefit Plans

1975 - 1998

SOURCE: U.S. Department of Labor, Pension Welfare & Benefits Administration,

Abstract of 1998 Form 5500 Annual Reports, Winter 2001 - 2002

Pension Participation Rates

1979 - 1998

SOURCE: U.S. Department of Labor, Pension Welfare & Benefits Administration,

Abstract of 1998 Form 5500 Annual Reports, Winter 2001 - 2002

Reasons for the Decline of Defined Benefit Plans

A number of factors have caused the shift away from defined benefit plans since the mid-1980s. Employment has shifted from the unionized, large manufacturing sector companies where defined benefit plans were common to the non-manufacturing sector with smaller employers where defined contribution plans predominate. Workers placed less value on defined benefit plans, and employer attitudes towards pensions changed from one of paternalism to one of worker self-reliance.

A new type of plan, the 401(k) plan, became available in the mid-1980s, and employers now had another option. Younger, more mobile workers preferred the portability and investment control offered by these 401(k) plans.

Changes to pension and tax laws have increased the complexity and costs of administering defined benefit plans. Companies with defined benefit plans found themselves increasingly competing, domestically and globally, with companies that did not offer any plan or offered only a defined contribution plan. Funding of defined contribution plans, unlike funding of defined benefit plans, is more predictable and easier to control.

The only type of defined benefit plan that is increasing in number is the cash balance plan. Cash balance plans typically credit a percentage of a worker's salary plus interest each year to a participant's cash balance account. At retirement, the participant generally has a choice between taking a lump sum or an annuity. Because there is a nominal account with a growing balance, the plan looks like a 401(k) account. A growing number of employers with defined benefit plans are shifting to cash balance plans rather than abandoning defined benefit plans altogether.

Conclusion

Mr. Chairman, I appreciate the opportunity to address the Subcommittee. Your consideration of the future of defined benefit plans is important to this Nation's long-term retirement outlook. Defined benefit plans remain a vital component of our retirement system.

My staff and I would be happy to provide any information that the Subcommittee might need in the future as you study defined benefit plans. I'd be happy to answer any questions from the Subcommittee.