Proceeds From Terminated Securitizations

September 13, 2004

Audit Report

No. 04-034

Federal Deposit Insurance Corporation

Office of Audits

Office of Inspector General

Washington, D.C. 20434

DATE: September 13, 2004

MEMORANDUM TO: Mitchell L. Glassman, Director,

Division of Resolutions and Receiverships

FROM: Russell A. Rau [Electronically

produced version; original signed by Russell Rau], Assistant

Inspector General for Audits

SUBJECT: Proceeds From Terminated Securitizations (Audit Report

Number 04-034)

This report presents the results of the Federal Deposit Insurance Corporation (FDIC) Office of Inspector General's (OIG) audit of proceeds from terminated securitizations. Securitizations and related termination proceeds are described in detail in the Background section of our report. We found that the Division of Resolutions and Receiverships (DRR) had an adequate management control process to ensure that funds from terminated securitization transactions are properly reported and credited to the FDIC. Therefore, we concluded our field work on this audit after completion of the audit survey.

The objective of this audit was to determine whether funds from terminated securitization transactions had been properly reported and credited to the FDIC by third parties. [1] The scope of our audit included 32 Resolution Trust Corporation (RTC) [2] securitizations terminated from January 2001 to March 2004, including the final RTC securitization that was terminated on March 25, 2004. We did not review asset disposition strategies or other activities related to DRR's securitization program in conjunction with this audit. Additional details on our objective, scope, and methodology are in the Appendix.

BACKGROUND

Securitization is the process by which assets with generally predictable cash flows are packaged into interest-bearing securities with marketable investment characteristics. Securitized assets have been created using diverse types of collateral, including home mortgages, commercial mortgages, mobile home loans, leases, and installment contracts on personal property. The most common securitized product is the mortgage-backed security (MBS).

From 1991 to 1995, the RTC created a total of 72 securitizations in administering its responsibilities for managing the liquidation of assets from failed financial institutions. These transactions were backed by collateral consisting of residential mortgage loans, multi-family mortgage loans, commercial mortgage loans, and other types of loan pools with characteristics that generally conform to one of these three categories.

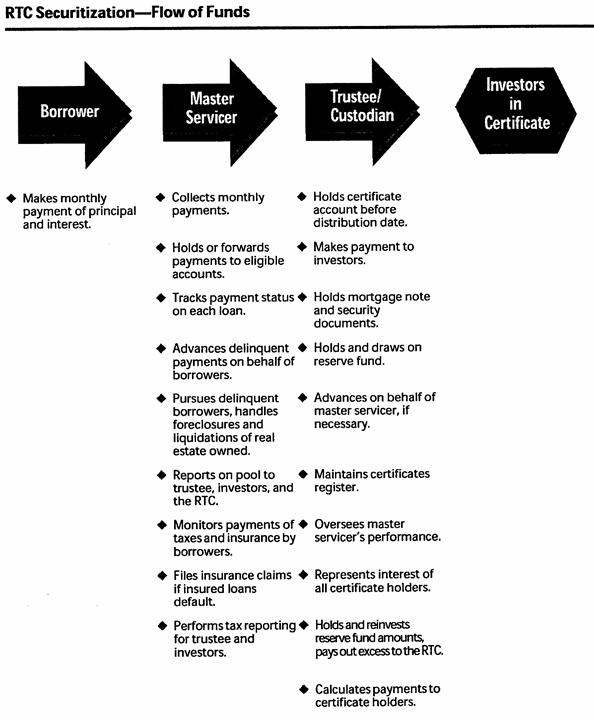

In general, each securitization was accomplished through the creation of a trust, [3] which obtained the collateral (loans) from one or more institutions for which the RTC had acted as receiver [4] or conservator. [5] The borrowers on each of the mortgage loans serving as collateral made monthly payments of principal and interest. The loans in each trust were pooled and stratified, and the resulting cash flow was directed into a number of certificates. [6] The certificates were sold in a public offering managed by a lead underwriter.

A mortgage-backed securities master servicer (servicer) and a trustee were appointed for each trust. The servicer's primary responsibilities were to collect the payments from the individual borrowers; track payment status; provide reports on loan payment activity to the trustee, the investors, and the FDIC; and follow up on delinquencies. The servicer held the loan payments until the end of each remittance period, at which time the payments were sent to the trustee for distribution to the certificate holders. The trustee's principal responsibility was to protect the interest of the certificate holders. [7] Each month, the trustee calculated the amount of monthly distributions payable to certificate holders; prepared their monthly statements, summarizing the payments received by the trust and the amounts paid to each certificate holder; and made the respective distributions. In addition, the trustee was generally responsible for the preparation of the trust's income tax return and related informational tax filings. The RTC's securitization flow of funds is illustrated on the next page.

Source: Lehman Brothers Completed Transactions Book, Security Series 1991-1 (July 1991).

Source: Lehman Brothers Completed Transactions Book, Security Series 1991-1 (July 1991).

[D]

When each securitization was terminated, it retained two assets -- reserve funds and residual certificates. To obtain a high credit rating, the RTC pledged reserve funds for each securitization that were funded using a portion of the proceeds from the sale of loans to the trust. The purpose of the reserve funds, up to the amount funded at the closing of each securitization, was to ensure timely payment of all principal and interest due to investors by reimbursing losses to the trust on the underlying loans. At securitization termination, the amount remaining in the reserve fund was released by the trust to the FDIC.

The residual certificates entitled the FDIC to all assets remaining in a trust after all other certificate holders had been paid in full. At termination of each trust, the trustee sold the remaining loans and used the proceeds to pay off the remaining certificate balances. Any proceeds remaining after payment of termination expenses were paid to the FDIC as a final distribution of the residual certificate. In a few cases, the provisions of the trust documents provided for all or a portion of excess interest [8] to be distributed to the residual certificate holder on a monthly basis during the life of the trust. Accordingly, there may have been no residual distribution at the termination of a securitization.

The FDIC's oversight rights of a securitization were based on ownership of the pledged reserve fund and as holder of the residual certificate. DRR implemented a quality review program for the securitization process, using contractors with expertise in securitizations to monitor servicing of each securitization. The quality review program included monthly reconciliations of the trustees' account statements on the reserves with the statements to certificate holders. The program also included annual on-site reviews of servicing operations, including a review of financial transactions on specific RTC securitizations.

DRR is responsible for coordinating and directing all the FDIC's activities in conjunction with the termination of an RTC securitization. The rules governing the termination of a securitization transaction are contained in the Pooling and Servicing Agreement (PSA) created between the RTC, servicer, and trustee. The PSA provides detailed guidance regarding loan servicing, reporting requirements, maintenance and use of reserves, remittance of funds from the servicer to the trustee, and the monthly pass-through of funds from the trustee to certificate holders. Additional guidance is in the FDIC Securitization Termination Oversight Procedures Guide (STOP Guide), dated June 12, 1997. The STOP Guide describes the appropriate and timely execution of the FDIC's contractual responsibilities under the documents governing RTC issued securitization transactions. In addition, a post-termination analysis for each RTC securitization is performed by a contractor within 30 days of the termination date. The post termination analysis files, maintained by DRR, provide final reconciliations and verifications that all funds from the securitization were properly reported and credited to the FDIC by third parties.

RESULTS OF AUDIT

Based on our review of post-termination analyses for four securitization transactions, we determined that DRR had established and implemented effective procedures for ensuring that funds from those transactions were properly reported and credited to the FDIC by third parties. Specifically, DRR had conducted reviews of the reserves and residual distributions related to all the RTC securitizations terminated since January 2001. The documented post-termination analyses for the four terminated securitizations we reviewed showed that third parties properly reported and credited to the FDIC all funds related to the securitizations.

Securitization Post-termination Analysis

The DRR post-termination analyses we reviewed for 4 of 32 securitizations terminated since January 2001 showed that DRR had adequate procedures for ensuring that funds from the terminated securitization transactions were properly reported and credited to the FDIC by third parties. Specifically, DRR's contractor had conducted procedures to verify that reserve funds and residual distributions were properly credited to the FDIC upon terminations of the securitizations. Further, the post-termination analyses of the securitizations were adequately documented and provided sufficient evidence that all issues were properly resolved.

The reserve fund releases and residual distributions from the four securitization transactions totaled $341,578,536 and $241,120,162, respectively. We determined that the procedures established for ensuring that funds due to the FDIC from the reserves and residual distributions provided adequate assurance that all funds had been properly reported and credited. For example, the procedures ensured that the calculation of the residual distributions to the FDIC was consistent with the terms of the PSA, that the calculations were mathematically correct, and that all funds were received by the FDIC. Procedures also verified that proceeds remaining in reserve funds after the terminations were returned to the FDIC and that the reserve fund was fully accounted for and cleared from the FDIC's general ledger.

Post-termination analysis files were complete and provided adequate documentation of the work performed. The work performed during each of the post-termination analyses was in a standard format that included: a list of Work Products, Summary and Documentation Checklist, Sales Due To/Due From Analysis, Residual Distribution Analysis, Reserve Fund Analysis, Final Pricing Analysis, and Follow-up Analysis. Each of the four files provided detailed descriptions of procedures performed; analysis summaries; and sufficient cross-indexing to schedules, reports, and other documentation showing that funds had been properly reported and credited to the FDIC by third parties.

To determine the accuracy of the procedures performed for the four securitized transactions, we recalculated amounts in the Flow of Funds Schedules and other schedules, which had been prepared by DRR's contractor for its analysis of the reserves and the residual distributions. We also traced selected procedures to supporting documentation, verifying that the work had been adequately documented. Further, we traced all termination follow-up issues to additional work performed to ensure that they had been appropriately resolved. No significant exceptions were noted in the four files we reviewed.

Because we noted no significant exceptions during our audit work, we are making no recommendations related to the audit objective.

CORPORATION COMMENTS AND OIG EVALUATION

A written response was not required for the report. DRR notified the OIG that it had no official comments.

OBJECTIVE, SCOPE, AND METHODOLOGY

The objective of the audit was to determine whether funds from terminated securitization transactions had been properly reported and credited to the FDIC by third parties. We reviewed the DRR policies and procedures established for securitization termination oversight and related procedures used by DRR's contractor in performing post-termination analysis. The audit scope included 4 of the 32 RTC securitizations terminated since January 2001. We terminated our field work on this audit based on a review of the four securitization post-termination analysis files and the DRR procedures established for securitization terminations. We performed our work from June through July 2004 in accordance with generally accepted government auditing standards.

To accomplish our objectives and to gain an understanding of internal controls, we reviewed the following DRR documents.

- Securitization Termination Oversight Procedures Guide, June 1997

- Statement of Work for Securitization Financial Services Support to MBS-Administration

- Pooling and Servicing Agreement, Securitization Series 1994-C1

- Pooling and Servicing Agreement, Securitization Series 1995-01

- Securitization Post-Termination Analysis Procedures

We interviewed key personnel in DRR's Analysis and Evaluations Unit and contract personnel that performed the post-termination analyses on RTC securitizations. We conducted tests of the post-termination analysis procedures performed for the four securitizations and evaluated the extent of procedures performed to ensure that funds from the terminated securitizations had been properly reported and credited to the FDIC by third parties. To test the accuracy of procedures conducted by DRR, we traced summaries of procedures to supporting documentation and recalculated the amounts in the schedules related to the reserve fund and residual distributions.

Government Performance and Results Act, Fraud and Illegal Acts, and Compliance with Laws and Regulations

To determine whether DRR had any performance measures that we should consider in this audit, we reviewed the DRR 2004 Strategic Plan. We did not identify any DRR performance goals that specifically related to our audit objective.

Our audit program included steps for providing reasonable assurance of detecting fraud or illegal acts. Also, we gained an understanding of applicable laws and regulations by examining the Federal Deposit Insurance Act of September 21, 1950, Pub. L. No. 797, as codified at 12 United States Code (U.S.C.), section 1821(d), Powers and Duties of Corporation as Conservator or Receiver; and the RTC Completion Act of December 17, 1993, Pub. L. No. 103-204, as codified at 12 U.S.C., section 1441a.(m), Termination.

Computer-Processed Data

We determined that computer-processed data was not significant to the audit objective.

|