Economic Effects of Animal Diseases Linked

to Trade Dependency

Though global meat trade

has not fallen in response to animal disease outbreaks,

a few countries have seen significant changes to

their exports and imports.

Don P. Blayney;

John Dyck;

David Harvey

|

|

|

|

Global

levels of meat trade have not declined

despite the last decade’s high-profile

bans on meat trade flows. |

|

|

The

economic effects of disease-related

trade bans on an individual country

depend on the size of its livestock

trade relative to domestic consumption.

The most severe im-pacts have been felt

in a few export-dependent markets and

in those import-dependent markets where

substitutes for banned trade were not

found. |

|

|

The

economic significance of animal disease

outbreaks is also influenced by consumer

response: Fears that the disease can

spread to humans can lead to sharp drops

in consumption. |

|

| This

article is drawn from . . . |

| Disease-Related

Trade Restrictions Shaped Animal Product Markets

in 2004 and Stamp Imprints on 2005 Forecasts,

by Don P. Blayney, LDP-M-133-01, USDA, Economic

Research Service, August 2005.

Livestock,

Dairy, and Poultry Outlook, coordinated

by Mildred Haley, LDP-M-140, USDA, Economic

Research Service, February 2006.

Livestock,

Dairy, and Poultry Outlook, coordinated

by Mildred Haley, LDP-M-139, USDA, Economic

Research Service, January 2006.

|

| You

may also be interested in . . . |

| ERS Briefing

Room on Japan

ERS Briefing Room on Animal

Production and Marketing Issues |

The importance of livestock and

poultry trade to producers and consumers around

the world increased in the last part of the 20th

century. Producers in major exporting countries

grew to rely on trade as a significant outlet for

their products, and consumers in the importing countries

relied increasingly on trade for a significant contribution

to their diets.

In the last decade, however, a

spate of animal disease outbreaks has repeatedly

disrupted livestock and poultry meat trade and created

uncertainty about future trade disruptions. Two

diseases, avian influenza (AI) and bovine spongiform

encephalopathy (BSE), are at the forefront of today’s

trade disruptions, but a third disease, foot-and-mouth

disease (FMD), has caused havoc in livestock markets

for the past decade and emerged again very recently

in Brazil. Some of the trade disruptions have resulted

in losses for livestock industries, such

as the pork exporters of Taiwan, whose exports

were nearly eliminated from early 1997 to the present

because of FMD. Disease-related interruptions of

trade flows have also affected the food industry

and consumers in the importing countries, when the

meat affected by the ban could not be replaced by

either domestic producers or other exporting countries

or when consumers reduced purchases because of fears

for their health.

The economic costs of these disruptions

vary, and three criteria help explain the extent

of damage done by a disease outbreak. First is the

relative importance of meat exports to producers

in the affected country. Loss of export markets

is much more serious if 40 percent of the country’s

output is exported than if 5 percent is exported.

For example, disease outbreaks among the pork industries

in Denmark and Taiwan and the poultry industry in

Thailand, all heavily dependent on exports, have

inflicted great damage on producers in those countries.

A sudden end to trade leaves an increased supply

of meat that must be sold domestically, reducing

prices. In contrast, a large country like China

has suffered less disruption from AI because it

was less dependent on poultry exports.

Second is the relative importance

of imports from an affected country to consumers

in an importing country. If a country affected by

disease supplies 20 percent of an importing country’s

meat, a sudden end to the imports can lead to a

fall in consumption unless domestic production or

imports from another country can make up the deficit.

For example, after the AI outbreaks in China and

Southeast Asia, Japan was able to partially replace

poultry imports from Asia with imports from Brazil.

In contrast, Japan’s beef imports from the

U.S. were not so easily replaced.

The final factor is whether the

animal disease poses a threat to humans, because

consumers’ fears can reduce consumption. FMD

and highly pathogenic AI are both contagious viral

infections in animals and birds that cannot be contained

easily. BSE is a different kind of disease—it

is not contagious and does not spread rapidly. FMD

does not typically affect humans, but the highly

pathogenic H5N1 strain of AI appears to have been

transmitted to humans through very close contact

with infected birds. Cooking kills the viral agents

of FMD and AI in meat but not the BSE agents. BSE

is thought to cause a fatal brain disease in humans

who eat high-risk tissue from infected animals.

A Decade of FMD Shocks

Brings an End to Taiwanese Pork Exports

FMD is a very contagious viral

infection that can cause death or permanent disability

for cattle and swine and can spread very rapidly

in a number of different ways. Beef and pork trade

flows have long been defined by the identification

of “FMD-free” and “FMD”

zones. For much of the 20th century, the FMD-free

zone was a stable group of countries or territories

including the U.S., Canada, Australia, New Zealand,

Japan, South Korea, Taiwan, and, sometimes, Denmark.

Because these countries recognized each other as

free of FMD, sanitary barriers did not ordinarily

inhibit trade among them or affect their exports

to countries that were not FMD-free. Countries not

recognized as FMD-free can export only cooked meats,

such as corned beef or canned hams (cooking kills

the virus), to the FMD-free zone, not chilled or

frozen meat. The strict enforcement of FMD trade

restrictions reflects the efforts that went into

eradicating the disease in places where it was done

successfully. Japan’s eradication in 1907,

and the eradications in Taiwan and the U.S. in the

1920s, required massive campaigns. Reportedly, all

hogs on the island of Taiwan were destroyed, an

action that made the island FMD-free for the next

50 years. The stability of the FMD-free zone ended

in the latter half of the 1990s.

Trade in beef and pork (and live

cattle and swine), both within the disease-free

zones and among countries that had not yet achieved

FMD-free status, was shaken by events beginning

in 1997. FMD began to spread widely around the world,

and Taiwan experienced an outbreak in that year

so severe that more than a third of the island’s

hogs (4 million of the 11 million on the island)

died or were slaughtered and the carcasses destroyed,

not eaten. Dependence on exports was high, with

40 percent of output going to Japan. A decade later,

despite efforts to recover FMD-free status and regain

its once-large export presence, Taiwan has a much

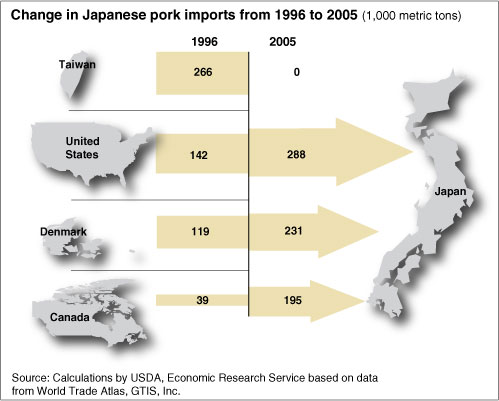

smaller hog population and lower exports. Exports

from Taiwan made up 40 percent of Japan’s

pork imports, but that loss was offset by rising

imports from Canada, Denmark, and the U.S., as well

as greater-than-expected production within Japan

itself. Pork from Taiwan had distinct appeal in

Japan’s market, but was not so differentiated

that it could not be replaced.

Over the next 5 years, smaller

outbreaks occurred in Japan and South Korea (both

FMD-free for many decades) and a large outbreak

swept parts of Western Europe, which had long struggled

to become FMD-free. In South America, Argentina

and Brazil had been working hard to achieve FMD-free

status, but experienced outbreaks after 2000. The

stability of the FMD-free zone from about 1930 to

1997 has given way to volatility caused by the outbreaks

of the last decade, and renewed fear among producers

in all the exporting countries.

In the past, FMD outbreaks typically

resulted in bans on imports from anywhere in affected

countries. However, over the last two decades, in

order to help mitigate the drastic consequences

of whole-country bans, importing countries have

sometimes agreed to restrict their trade bans to

those regions within the country where the outbreak

occurred, allowing imports from other regions that

are disease free, a practice known as regionalization.

BSE Perceptions Affect

Consumers in Japan and Korea More Than U.S. Producers

Unlike FMD, the discoveries of

BSE in cattle have caused widespread concern about

the safety of beef consumption in some markets.

BSE, also called mad cow disease, is a neurological

disease in cattle that was first discovered in Britain

in 1986. It was thought to affect only cattle until

1996, when the British Government announced a possible

link to a new human variant of Creutzfeldt-Jacob

Disease, and BSE was elevated from an animal health

concern to a human health concern. Unlike viral

diseases, such as AI and FMD, scientific research

indicates that cooking does not kill the causal

agent of BSE. But, with measures in place to remove

the significant risk materials from the food system,

human health risks from BSE are minimized.

The Canadian Government announced

the discovery of the first case of BSE in a North

American-born animal, a beef cow in Alberta, in

May 2003. All of the country’s major trading

partners, including the U.S., banned imports of

Canadian beef and live cattle immediately. In August,

the U.S. allowed boneless beef from cattle under

30 months of age, but not live cattle, to be imported

from Canada. Then, in December 2003, discovery of

a BSE-infected cow in Washington State led some

70 countries, including Canada and Mexico, to impose

import bans of varying degrees on U.S. beef and

cattle. U.S. beef exports dropped from a record

2.5 billion pounds in 2003 to 461 million pounds

in 2004, a fall of over 80 percent. The bans on

U.S. beef exports clearly were significant to U.S.

exporters and to the consumers of U.S. high-quality,

grain-fed beef in countries such as Japan, Korea,

and Hong Kong, whose markets were closed to the

U.S. and where beef prices rose. While the U.S.

beef industry depended on exports to take 9-10 percent

of output, the domestic market was strong and absorbed

the increase in supply.

The U.S. ban on Canadian beef imports

in May 2003 came at a time when U.S. beef supplies

were already tight, and the ban led to even tighter

supplies. By October 2003, the supply situation

had generated record-high U.S. cattle and beef prices.

Domestic beef production was declining because producers

had been reducing inventories since 1996, while

the demand for high-quality, grain-fed beef remained

high. With the domestic market fetching high prices,

the beef industry was better able to absorb losses

in export revenue. In addition, U.S. meat consumers

did not abandon eating beef after the BSE discoveries

as consumers in Europe and Japan had done, at least

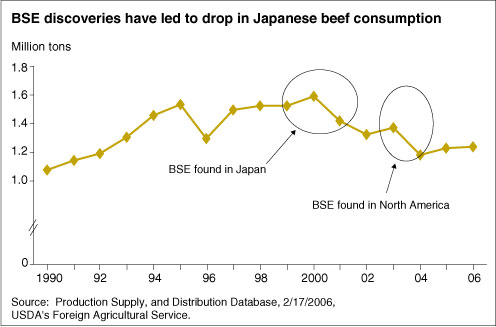

for limited periods. Japan’s annual consumption

of beef dropped by about 15 percent in 2001, when

BSE was discovered in Japan.

|

Japanese and Korean consumption

of beef fell even more when U.S. beef was cut off.

The two Asian markets depended heavily on North

American, especially U.S., beef. North American

beef constituted one-fourth of total Japanese consumption

in 2002. Furthermore, beef

trade was concentrated on a few cuts of beef,

particularly short plate and short ribs. Japanese

and Korean restaurants had developed a strong demand

for dishes made with these cuts. No other BSE-free

beef supply in the world was big enough to replace

the U.S. supply of these cuts. Japanese and Korean

consumers also liked the taste of grain-fed beef

from North America. Beef from Australia and New

Zealand has traditionally been grass fed, and attempts

to feed grain to the degree that it is fed in North

America have not been viable on a large scale. Most

North American beef has not been replaced in the

two Asian markets. Japan’s beef consumption

in 2004 was 25 percent below 2000 levels because

of the combined effect of drops in demand and reduced

supply.

Asian Poultry Markets Disrupted

by Avian Influenza

Well-publicized outbreaks of the

highly pathogenic H5N1 strain of AI began in Asia

in 1998. The strain was first identified in Hong

Kong, where it killed several people. In response,

the entire poultry population in Hong Kong—millions

of birds—was slaughtered to eradicate the

disease. However, in 2001, H5N1 reappeared in China,

and in 2003 and 2004, it affected several poultry

populations in Southeast Asia. In 2005, it spread

across Asia and reached Europe; cases were reported

in Europe and Africa in early 2006. Highly pathogenic

strains of AI are very dangerous to birds, spreading

quickly and often killing the birds. The H5N1 strain

has also spread from birds to people when people

have been in close contact with diseased birds.

Like FMD, AI viruses in meat are

killed by cooking. Unlike FMD, however, H5N1 can

infect and kill humans from bird-to-human contact.

Medical experts worry about a possible human pandemic

if the H5N1 variant mutates in ways that make transmission

of the virus directly between people easier. This

worry has led to extra efforts to eradicate AI,

such as killing or banning all live chickens and

other birds in major Asian cities—examples

include Hong Kong and cities in Vietnam—and

to campaigns to vaccinate entire populations of

various species of birds against H5N1 AI.

Trade disruptions from H5N1 AI

affected two of the world’s major exporters

of chicken meat, Thailand and China. Thailand’s

broiler industry depends heavily on exports and

was hard-hit by the bans. China’s exports

are a small share of its chicken meat output, and

the impact of bans on its exports was less significant

nationally, although severe for producers focused

primarily on the Japanese market.

Consumer concerns about the safety of poultry in

certain markets—e.g., Japan, China, Vietnam,

and Thailand—led to sudden drops in consumption,

although cooked chicken meat and egg products are

safe to eat. But even though Japan is dependent

on imports for a large share of consumption, the

AI outbreaks in China and Thailand have not negatively

affected supplies in Japan. Brazil has greatly expanded

its exports to Japan, and China and Thailand have

transformed their exports into heat-treated products

that to some extent replace earlier frozen exports

(see “Asian Markets Restructured

by AI”).

Animal Diseases Are a Continuing

Threat

Meat sectors in a number of countries

have suffered serious damage from disease outbreaks.

On a global scale, however, trade disruption by

and consumer reaction to fears of infectious animal

diseases are not readily apparent (see “Effects

of AI on U.S. Poultry Industry So Far Are Minimal”).

Global production, consumption, and trade of pork

and broiler meat have continued to grow through

the animal disease episodes of the last decade,

and global beef production and consumption have

stayed relatively constant since 1990. In most cases,

disease-related import bans have been mitigated

by increasing supplies from domestic or alternative

foreign sources of meat. Similarly, global feed

use of corn has continued to rise, despite drops

in annual corn use as high as 25 percent in certain

countries (Thailand from 2001 to 2003, Taiwan from

1996 to 1998).

Meat trade increasingly requires

that a supply chain for meat can be identified that

both the importing and exporting countries agree

poses low risk of disease transmission. Elements

of this risk-based decisionmaking have been adopted

by the World Organization for Animal Health for

BSE and AI and in recent agreements among countries

affected by BSE (e.g., Japan, Canada, and the U.S.).

It may lead to a reduction in the extent and duration

of trade bans. Technological advances in identifying

disease strains and in tracing the origin of meats

and the increasing use of risk analysis offer hope

that outbreaks may be avoided or contained more

quickly. Animal diseases, however, remain volatile

threats to global trade in meats.

| Asian

Markets Restructured by AI

In the 1990s, the principal

driver of Asia’s poultry meat trade

was Japanese demand for imports supplied by

China and Thailand. Because fresh poultry

meat does not keep as long as beef and pork,

the trade focused mainly on frozen cuts, primarily

from broilers. The Japanese place a higher

value on chicken legs than on white meat,

a factor exploited by the Asian exporters

that supplied such products as de-boned legs.

These de-boned products competed successfully

against the bone-in legs long supplied by

the U.S. Thailand also successfully developed

a large export market to the European Union.

In addition to supplying

frozen products, Thailand and China also supplied

Japan with further processed broiler meat,

often seasoned, cooked, cut, packaged, and

ready for restaurants or consumers to use,

once reheated. Shipments of further processed

products had a considerably higher value than

did frozen cuts, reflecting the greater convenience

they offered to customers and the higher costs

of inputs needed to manufacture them. By 2000,

Japan was importing over 150,000 tons of prepared

and preserved broiler meat, valued at over

$500 million. China, because of the relatively

short sea passage between its Shandong Province

and Japan, was also able to ship chilled broiler

meat to Japan that could compete with the

fresh and chilled Japanese meat in supermarkets.

The discovery of the high-pathogenic

H5N1 strain of AI in Hong Kong in 1998 brought

new uncertainty to Asia’s poultry meat

trade. China’s chilled and frozen exports

to Japan were halted for 3 months (July-September)

in 2001 after an H5N1 outbreak in China. Late

in 2003 and early in 2004, H5N1 AI appeared

in all of Japan’s large Asian suppliers,

and their exports of chilled and frozen broiler

meat ceased. South Korea, an emerging importer,

also banned chilled and frozen poultry product

imports from all major Asian suppliers.

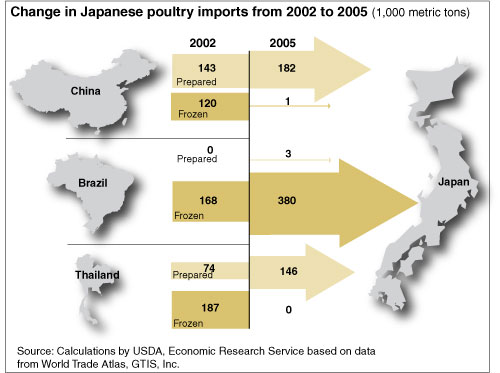

A direct result of the outbreak

was a large increase in Japanese imports from

Brazil. Brazil had not experienced any AI

outbreaks and, except for the U.S. bone-in

legs, faced almost no competition for the

frozen cut markets in Japan and smaller Asian

importing countries. Brazil’s exports

of frozen broiler meat to Japan shot up from

109,000 tons in 2000 to 403,000 tons in 2005.

In another shift, Chinese

and Thai poultry-exporting firms refocused

on increasing production of prepared and preserved

broiler cuts. The heat treatment for such

further processed cuts kills the AI virus

if it is present. The share of further processed

cuts in Thai poultry exports rose from 28

percent in 2000 to 88 percent in 2004 and

to 98 percent in 2005. The share of China’s

exports of further processed cuts of poultry

went from 20 percent in 2000 to 58 percent

in 2005 (China still ships chilled/frozen

poultry meat to its Hong Kong Special Autonomous

Region). Poultry meat exports from major Asian

suppliers to Japan and South Korea are now

almost 100 percent prepared and preserved

meat. In contrast, Brazil ships almost entirely

frozen, unprocessed chicken meat to Asia.

The AI outbreaks have helped

depress Asia’s poultry meat trade since

2000. However, trade is recovering—Japan’s

import volume in 2005 exceeded 2000 levels,

and the unit value of its imports is higher,

reflecting the value added from processing

in China and Thailand. The AI outbreaks in

Asia thus accelerated a transition to production

and export of higher valued products that

was already underway in several countries. |

| Effects

of AI on U.S. Poultry Industry So Far Are

Minimal

So far, the U.S. has been

spared from major disruptions of its poultry

trade. AI outbreaks in the U.S. have been

mostly of the less dangerous low-pathogenic

varieties. U.S. poultry producers and processors

enjoy a healthy domestic market situation

partly supported by slowly growing retail

prices relative to other meat prices and steady

per capita consumption. (See “Chicken

Consumption Continues Longrun Rise”)

Most of the bans on U.S. poultry product exports

due to AI or other poultry diseases have been

regionalized quickly. For example, in 2002,

U.S. trading partners banned poultry product

imports from selected States including, at

various times, Maine, North Carolina, Pennsylvania,

Texas, Virginia, and West Virginia, after

outbreaks of the low-pathogenic AI. If such

regionalization does not affect areas that

are primary sources of poultry product exports,

national exports may not be seriously affected.

Of the five largest broiler-producing States—Georgia,

Arkansas, Alabama, Mississippi, and North

Carolina—only North Carolina has been

included in trade bans. However, the U.S.

is the second largest exporter of poultry

products in the world. That position in international

markets makes AI-related trade issues a key

concern for the U.S. poultry industry. |

|