| April 2008

The above photos are from condos that were involved in a mortgage

fraud. The appraisal described “recently renovated condominiums” to

include Brazilian hardwood, granite countertops, and a value of

$275,000.

Scope Note

The purpose of this study is to provide insight into the breadth

and depth of mortgage fraud crimes perpetrated against the United

States and its citizens. This report updates the 2006 Mortgage

Fraud Report and addresses current mortgage fraud projections,

issues, and “hot spots.” The objective of this study

is to provide FBI program managers with relative data to justify

mortgage fraud resources and for investigators to identify mortgage

fraud activity. The report was requested by the Financial Crimes

Section, Criminal Investigative Division (CID), and prepared by

the Financial Crimes Intelligence Unit, Directorate of Intelligence.

Information for the study was gathered from the FBI, other law

enforcement agencies, the mortgage industry, and open source reporting. |

Key Findings

- Mortgage fraud

continues to be an escalating problem in the United States.

Although no central repository

collects all mortgage

fraud complaints, Suspicious Activity Reports (SARs) from financial

institutions indicated an increase in mortgage fraud reporting.

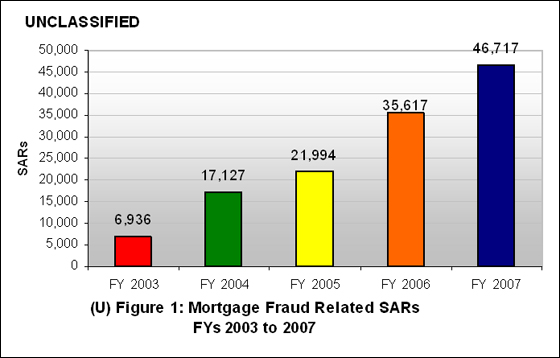

SARs increased 31-percent

to 46,717 during Fiscal Year (FY) 2007. The total dollar loss attributed

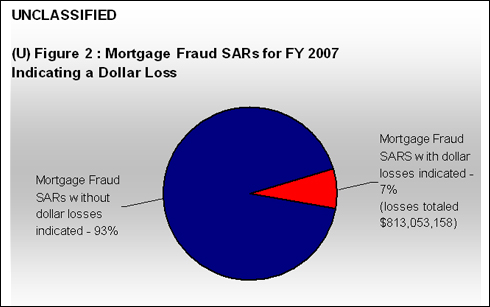

to mortgage fraud is unknown. However, 7 percent of SARs filed during

FY 2007 indicated a specific dollar loss, which totaled

more than $813 million.

- Subprime mortgage issues remain

a key factor in influencing mortgage fraud directly and

indirectly. The

subprime share of outstanding

loans has more than a doubled since 2003 putting a greater share

of loans at higher risk of failure. Additionally, during

2007

there were more than

2.2 million foreclosure filings reported on approximately 1.29

million properties nationally, up 75 percent from 2006.

The declining housing

market affects many in the mortgage industry who are

paid by commission. During

declining markets, mortgage fraud perpetrators may take advantage

of industry personnel attempting to generate loans to maintain

current standards of

living.

- Analysis of available information indicated

that mortgage fraud was most concentrated in the north central

region

of the United States.

Data from law enforcement and industry sources were compared

and mapped to determine which states were most affected

by mortgage

fraud during

2007 and indicated that the top 10 mortgage fraud states

for 2007 were Florida,

Georgia, Michigan, California, Illinois, Ohio, Texas, New York,

Colorado, and Minnesota. Other states significantly affected

by mortgage fraud

according to available sources included Arizona, Maryland,

Utah, Nevada, Missouri,

Indiana, Tennessee, Virginia, New Jersey, and Connecticut.

- The downward trend in the housing market provides an

ideal climate for mortgage fraud perpetrators to employ

a myriad of schemes suitable

to a down market. Several of these schemes have emerged with

the potential to spread as the recent rise in foreclosures,

depressed

housing prices,

and decreased demand place pressure on lenders, builders, and

home sellers. Emerging and re-emerging schemes for 2007

included

builder-bailouts, seller

assistance, short sales, foreclosure rescue, and identity thefts

exploiting home equity lines of credit.

“The potential impact of mortgage fraud on financial

institutions and the stock market is clear. If fraudulent practices

become

systemic within the mortgage industry and mortgage fraud is allowed

to become unrestrained, it will ultimately place financial institutions

at risk and have adverse effects on the stock market.”

-Chris Swecker, former FBI Assistant Director, Criminal Investigative Division, Introductory Statement: House Financial Services Subcommittee on Housing and Community Opportunity,

7 October 2004

Introduction

Mortgage Fraud: Two Categories

Mortgage loan fraud is divided into two categories: fraud for

property and fraud for profit.

Fraud for property/housing entails

misrepresentations by the applicant for the purpose of purchasing

a property for a primary residence. This scheme usually involves

a single loan. Although applicants may embellish income and conceal

debt, their intent is to repay the loan.

Fraud for profit,

however, often involves multiple loans and elaborate schemes

perpetrated

to gain illicit proceeds from property sales. It is this second

category that is of most concern to law enforcement and the mortgage

industry. Gross misrepresentations concerning appraisals and

loan documents are common in fraud for profit schemes and participants

are frequently paid for their participation. |

Mortgage Fraud is defined as the intentional misstatement,

misrepresentation, or omission by an applicant or other interested

parties, relied on by a lender or underwriter to provide funding

for, to purchase, or to insure a mortgage loan. Combating mortgage

fraud effectively requires the cooperation of law enforcement and

industry entities. No single regulatory agency is charged with

monitoring this crime. The FBI, Department of Housing and Urban

Development-Office of Inspector General (HUD-OIG), Internal Revenue

Service, Postal Inspection Service, and state and local agencies

are among those investigating mortgage fraud.

Mortgage fraud is a relatively low-risk, high-yield criminal

activity which is accessible to many. However, according a Financial

Crimes Enforcement Network (FinCEN) report, finance-related occupations,

including accountants, mortgage brokers, and lenders were the most

common suspect occupations associated with reported mortgage fraud.1

Perpetrators in mortgage industry occupations are familiar with

the mortgage loan process and therefore know how to exploit vulnerabilities

in the system. Victims of mortgage fraud may include borrowers,

mortgage industry entities, and those living in the neighborhoods

affected by mortgage fraud. As properties affected by mortgage

fraud are sold at artificially inflated prices, properties in surrounding

neighborhoods also become artificially inflated. When property

values are inflated, property taxes increase as well. Legitimate

homeowners also find it difficult to sell their homes as surrounding

properties affected by fraud deteriorate. When properties foreclose

as a result of mortgage fraud, neighborhoods deteriorate and surrounding

properties depreciate.

Financial Institution Reporting of Mortgage Fraud Increases

Although no central repository collects all mortgage fraud complaints,

Suspicious Activity Reports (SARs) from financial institutions

indicated an increase in mortgage fraud reporting. Financial institution

reporting indicated that 46,717 SARs were filed during FY 2007

(see figure 1).

The dollar losses attributed to mortgage fraud

are unknown. However, 7 percent of SARs filed during FY 2007

indicated a dollar loss of more than $813 million (see figure 2)2.

The fact that only 7 percent of SARs from financial institutions

documented

a loss may be attributed to the fact that losses were unknown

at the time of reporting, or fraud was discovered before loan

funding, and therefore a loss was not incurred. The $813 million

statistic

is significant, as it hints to the total amount of financial

institution

and industry entity losses not subject to SAR filing.

Mortgage Fraud in a Depressed Housing Market

During 2007, mortgage loan originations, including purchases and

refinances, were down from 2006 and foreclosures were up nationally,

contributing to a slump in the housing market. Many mortgage industry

professions are paid by commission. During declining markets, mortgage

fraud perpetrators may take advantage of industry personnel attempting

to generate loans to maintain current standards of living.

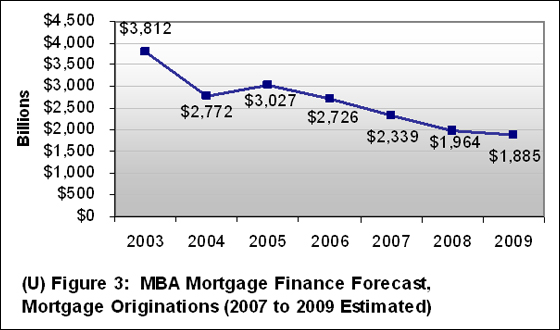

The housing market is expected to continue its downward trend.

The Mortgage Bankers Association (MBA) estimates that mortgage

loan originations will continue to decline through 2009 (see

figure 3).3

According to an MBA report from January 2008, existing home

sales are expected to decline by 13 percent during 2008 from 2007.

Likewise, new home sales are expected to decline 15 percent from

2007 figures. Median home prices are also expected to decline in

2008.4 The current and future market conditions will have mortgage

industry professionals pursuing a smaller pool of customers. As

such, professional fraudsters will devise new and improved schemes

to exploit the weaknesses in the housing market.5

The financial impact subprime lending has had on the mortgage

industry and the economy as a whole has been widely reported. The

subprime share of outstanding loans has more than doubled from

2003, putting a greater share of loans at a higher risk of failure

(see figure 4).6

Subprime mortgage loans are designed for persons

with blemished or limited credit histories. To compensate for the

increased credit risk, subprime loans carry a higher rate of interest

than prime loans.7 According to First American CoreLogic LoanPerformance

data, 64.5 percent of the securitized subprime loans originated

during 2005 had adjustable rates; 79.4 percent of these loans were

2/28 hybrid adjustable-rate loans (HARMS).8 These

HARMS had fixed mortgage rates for the first two years after

origination and were

subject to reset in 2007. Therefore, once the loan introductory “teaser

rate” expired, the rate was subject to increase.

Wall Street Journal, March 2008

“So far, banks and insurers have written down more

than $150 billion in securities tied to subprime-mortgage loans.”

- Excerpt from: Carrick Mollenkamp and Mark Whitehouse, “Banks

Fear a Deepening of Turmoil,” Wall Street Journal, 17 March

2008.

|

The upward

movement in interest rates and the declining housing market subjected

borrowers to increased payment shock and elevated the possibility

of default. The recent decline in the housing market and property

depreciation exacerbated the subprime problem. As properties depreciated

and demand decreased, property owners could not sell their homes

to satisfy their debts.

A report by MARI indicates that two factors pressured the industry

into non-traditional lending practices that contributed to fraud.

The first includes the persistent drive of mortgage lenders to

hasten the mortgage loan process, and the second involves the

escalation of home prices of recent years.9 According to congressional

statements,

by the spring of 2004, regulators began to document the fact

that lending standards were easing. Also, interest rates were

increasing.10

Notably, mortgage fraud SARs filed during 2004 more than doubled

from 2003 (see figures 1 and 4). These recent events likely resulted

in an increase in mortgage fraud as higher housing prices tempted

borrowers to exaggerate income and assets to qualify for a mortgage

loan. Mortgage fraud perpetrators also likely seized the opportunity

to take advantage of the relaxed lending practices to commit

fraud for profit.

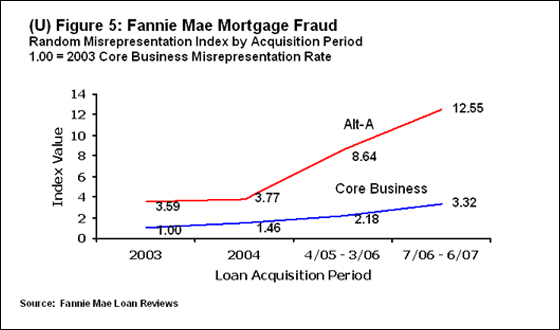

Alt-A loans are designed for prime-quality borrowers, and

in many instances do not require documentation, making them ideal

for fraud exploitation. Alt-A loans include stated income, stated

income/stated asset or no income/no asset loans that are offered

by both prime and subprime lenders. BasePoint Analytics, a fraud

analysis and consulting service, analyzed loans that were originated

between 2002 and 2006; nearly 1 million Alt-A loans and 3 million

nonprime loans were evaluated. The relative fraud-loss rate of

Alt-A loans was more than three times higher than nonprime loans.

Losses within Alt-A loans were caused by income misrepresentations,

employment frauds, straw buyers, investor-related frauds, and occupancy

frauds.11 The Federal National Mortgage Association (Fannie Mae)

conducts random post purchase reviews. Statistics generated from

these reviews indicate that misrepresentations within Alt-A loans

are higher than the overall population of loans (see figure

5).12

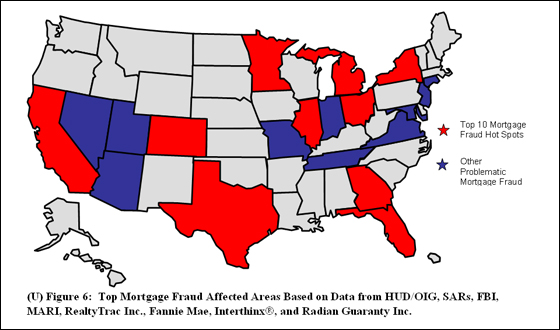

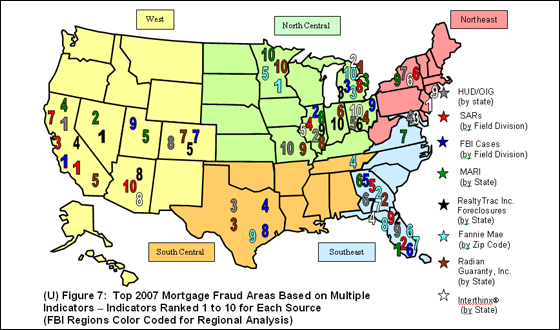

Top Areas for Mortgage Fraud

Data from law enforcement and industry sources were compared and

mapped to determine which areas of the country were most affected

by mortgage fraud during 2007. Information from the FBI, HUD-OIG,

FinCEN, Mortgage Asset Research Institute (MARI), Fannie Mae, RealtyTrac

Inc., Interthinx®, and Radian Guaranty Inc., indicated that

the top 10 mortgage fraud states for 2007 were Florida, Georgia,

Michigan,

California, Illinois, Ohio, Texas, New York, Colorado, and Minnesota

(see figures 6 and 7 for a breakdown of source data). Other states

significantly affected by mortgage fraud according to aforementioned

sources included Arizona, Maryland, Utah, Nevada, Missouri, Indiana,

Tennessee, Virginia, New Jersey, and Connecticut.

Analysis of available information indicated that mortgage fraud

was most concentrated in the north central region of the United

States (see figure 7). This region is followed by the west and

southeast regions.

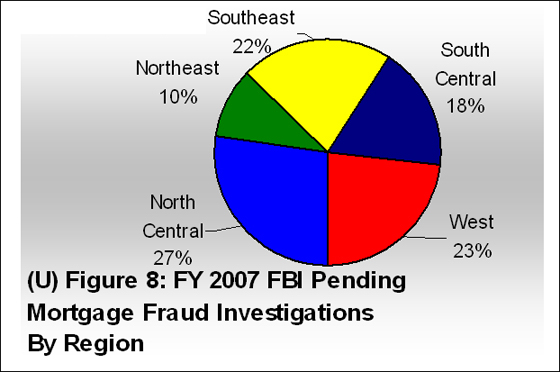

Breakdown of Sources Used to Identify Top Mortgage Fraud Areas

Federal Bureau of Investigation Regional analysis of FBI pending

mortgage fraud-related investigations as of FY 2007 revealed that

the north central region of the United States led the nation with

the most pending investigations. The north central region was followed

by the west, southeast, south central, and northeast, respectively

(see figures 7 and 8).

FBI mortgage fraud investigations at the end of FY 2007 totaled

1,204, a 47-percent increase from FY 2006 and a 176-percent increase

from FY 2003 (see figure 9).13 Fifty-six percent of pending FBI mortgage

fraud investigations in FY 2007 were associated with dollar losses

of more than $1 million (see figure 10). FBI field divisions that

ranked in the top 10 for pending investigations during FY 2007

included Los Angeles, Chicago, Detroit, Dallas, Atlanta, Miami,

Denver14, Houston, Cleveland and Salt Lake City15 (tied for 9th), respectively.16

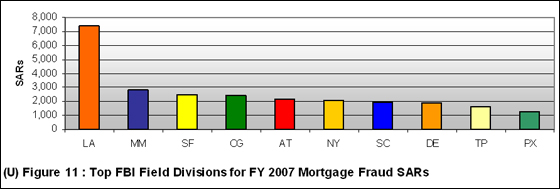

Financial Crimes Enforcement Network

According to SAR reporting, the Los Angeles, Miami, San Francisco,

Chicago, Atlanta, New York, Sacramento, Detroit, Tampa, and Phoenix

Divisions, respectively were the top 10 FBI field offices impacted

by mortgage fraud during FY 2007 (see figure 11).17

US Department of Housing and Urban Development - Office of Inspector

General

HUD-OIG is charged with detecting and preventing waste, fraud,

and abuse in relation to HUD programs. As part of this mission,

HUD-OIG investigates mortgage fraud related to Federal Housing

Administration (FHA) loans. As of 30 September 2007, HUD-OIG had

466 single family (SF) residential loan investigations pending.

In FY 2007, HUD-OIG opened 151 SF mortgage fraud investigations,

a decline from the 239 SF mortgage fraud investigations opened

during FY 2006. This decline can be attributed to the substantial

decline in FHA market share. One reason for the FHA loss of market

share was the increased prevalence of subprime loans from commercial

lenders; many of those who might typically have applied for FHA

loans instead opted for subprime loans. In addition, FHA loan levels

were often not competitive in many real estate markets. Consequently,

HUD-OIG witnessed a parallel decline in FHA mortgage

fraud investigations. Recently, FHA has made several significant

changes in its SF loan

program, including substantially increasing loan levels in high-cost

areas, and making efforts to have those currently holding subprime

loans, or facing foreclosure, to refinance those loans with FHA.

As a result, the FHA market share is expected to increase, with

a parallel increase anticipated for HUD-OIG’s investigative

case load.18

HUD-OIG’s top 10 mortgage fraud states based on investigations

opened during FY 2007 included Ohio, Maryland, Illinois, Georgia,

Texas, Virginia, California, North Carolina, Michigan, and New

York, respectively. Also, the top 10 state for pending investigations

during the same time period included California, Illinois, Texas,

Maryland, Ohio, Georgia, New York, Colorado, Florida, and Missouri.19

Mortgage Asset Research Institute

During 2007, Florida, Nevada, Michigan, California, Utah, Georgia,

Virginia, Illinois, New York, and Minnesota were MARI’s top

10 states for reports of mortgage fraud across all SF loan types (see

figure 12).20 MARI maintains the Mortgage Industry Data Exchange

(MIDEX) database which contains incidents of alleged mortgage fraud/misrepresentations

from hundreds of mortgage industry entities including Fannie Mae,

Freddie Mac, HUD, mortgage insurers, and numerous lenders. MARI

annually releases a report to the mortgage industry highlighting

the geographical distribution of mortgage fraud based on MIDEX

submissions. Individual states are ranked using the MARI Fraud

Index (MFI). The MFI is an indication of amount of mortgage fraud

found through MIDIX subscriber fraud investigations in various

geographical areas within a particular year relative to the amount

of loans originated. New states added to MARI’s top 10 for

2007 included Utah and Virginia.

Figure 12: MARI’s Top 10 States for 2007 Reported Fraud

in Single Family Loan Types

| Figure 12: MARI’s Top 10 States for 2007

Reported Fraud in Single Family Loan Types |

| State |

MFI Rank 2007 |

MFI Rank 2006 |

Florida |

1 |

1 |

Nevada |

2 |

6 |

Michigan |

3 |

3 |

California |

4 |

2 |

Utah |

5 |

11 |

Georgia |

6 |

4 |

Virginia |

7 |

14 |

Illinois |

8 |

8 |

New York |

9 |

9 |

Minnesota |

10 |

5 |

Interthinx® Interthinx® is a provider of proven risk mitigation and regulatory

compliance tools for the financial services industry. Data from

Interthinx® fraud detection tools (DISSCO and FraudGUARD?) include

nearly 2 million loan applications from more than 2,000 mortgage

originators and loan purchasers nationally. Loans are flagged for

possible fraudulent activity and scored as “Investigate” or “Critical

Risk” if they demonstrate high impact variances in employment/income,

identity, occupancy, straw-buyer, property valuation, or property

flipping. More than 22 percent of loans submitted to the Interthinx® mortgage fraud detection tools during 2007 had at least one high

impact variance in one of these categories. The top 10 states for

possible fraudulent activity based on 2007 loan application submissions

to Interthinx® were New Jersey, Michigan, Maryland, Florida, Illinois,

New York, Georgia, Arizona, Connecticut, and Ohio, respectively.21

Federal National Mortgage Association (Fannie Mae)

As of December 2007, the top 10 markets (by zip code area) for

mortgage loan misrepresentations according to Fannie Mae included

Minneapolis, Minnesota; Atlanta, Georgia; Detroit, Michigan; Memphis,

Tennessee; St. Paul, Minnesota; Pompano Beach, Florida; Miami,

Florida; Fort Myers, Florida; Houston, Texas; and Dearborn, Michigan.22

Fannie Mae is the nation’s largest mortgage investor. To

aid in mortgage fraud prevention and detection, the company publishes

a mortgage fraud newsletter that includes information concerning

misrepresentations discovered in loan files. Loans originated in

2006 through 2007 and reviewed by Fannie Mae through December 2007

were used to formulate a geographic top 10 list by zip code area

for concentrated mortgage loan misrepresentations (see figure

13).

| Figure 13: Fannie Mae Top 10 Zip Code Markets

for Misrepresentations |

| Rank for Number of Misrepresentations |

Top 10 Zip Code Markets

(first three digits

of zip code) |

Type of Misrepresentation |

1

|

Minneapolis, Minnesota (554)

|

Credit and SSN

|

2

|

Atlanta, Georgia (303)

|

Credit and Income

|

3

|

Detroit, Michigan (482)

|

Credit and Value/Property

|

4

|

Memphis, Tennessee (381)

|

Income and Assets

|

5

|

St. Paul, Minnesota (551)

|

Credit and SSN

|

6

|

Pompano Beach, Florida (330)

|

Income and Credit

|

7

|

Miami, Florida (331)

|

Income and Assets

|

8

|

Fort Myers, Florida (339)

|

Credit and Occupancy

|

9

|

Houston, Texas (770)

|

Income and Credit

|

10

|

Dearborn, Michigan (481)

|

Credit and Income

|

Delinquency, Default, and Foreclosure: Results of Fraud

BasePoint Analytics, a fraud analysis and consulting service,

analyzed more than 3 million loans and found that between 30 and

70 percent of early payment defaults (EPDs) are linked to significant

misrepresentations in the original loan applications.23 Radian Guaranty,

Inc. is a leading provider of mortgage insurance which protects

lenders against loan default. Statistics maintained by the company

indicated that Florida, California, Michigan, Texas, Ohio, Illinois,

Georgia, New York, Pennsylvania, and New Jersey, respectively were

the top 10 states for the percentage of EPDs as of 31 December

2007.24 Radian Guaranty, Inc. also ranked more than half of these

states in their top 10 for percent of mortgage frauds uncovered,

which suggests that EPDs are potential fraud indicators. As of

31 December 2007, Radian Guaranty, Inc.’s top 10 states for

percent of overall frauds uncovered included Michigan, Georgia,

Texas, Ohio, California, Indiana, Colorado, Illinois, Missouri,

and Minnesota, respectively (see figure 14).25

Figure 14: Radian Guaranty, Inc. Top States for

EPDs and Mortgage Fraud

(States in both columns are bold text) |

| Rank |

Radian Guaranty, Inc.

Top States for EPDs |

Radian Guaranty, Inc.

Top Mortgage Fraud States |

1

|

Florida

|

Michigan

|

2

|

California

|

Georgia

|

3

|

Michigan

|

Texas

|

4

|

Texas

|

Ohio

|

5

|

Ohio

|

California

|

6

|

Illinois

|

Indiana

|

7

|

Georgia

|

Colorado

|

8

|

New York

|

Illinois

|

9

|

Pennsylvania

|

Missouri

|

10

|

New Jersey

|

Minnesota

|

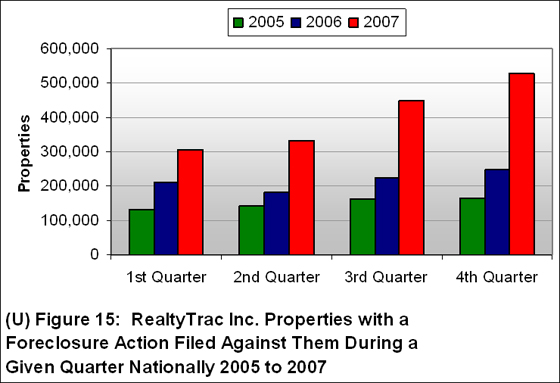

During 2007, there were more than 2.2 million foreclosure filings

reported on approximately 1.29 million properties nationally, up

75 percent from 2006. More than 1 percent of all US households

were in some stage of foreclosure, including default notices, auction

sale notices, and bank repossessions, up from 0.58 percent in 2006.26

Properties in some stage of foreclosure for 2007 surpassed 2006

figures for all four quarters (see figure 15). The top 10 states

for percent of households in some stage of foreclosure during 2007

were Nevada (3.376 percent), Florida (2.002 percent), Michigan

(1.947 percent), California (1.921), Colorado (1.919), Ohio (1.797),

Georgia (1.566), Arizona (1.516), Illinois (1.250), and Indiana

(1.027).27

Emerging Schemes

The downward trend in the housing market provides an ideal climate

for mortgage fraud perpetrators to employ a myriad of schemes suitable

to a down market. Several of these schemes have emerged with the

potential to spread as the recent rise in foreclosures, depressed

housing prices, and decreased demand place pressure on lenders,

builders, and home sellers. As lending practices tighten, in response

to the subprime lending crisis, fewer loans will be originated.

Perpetrators will seek alternative methods of defrauding mortgage

loan products. Identity theft is historically a popular tool for

use in mortgage fraud schemes. As financial institutions begin

to enforce higher lending standards, the identities of individuals

with good credit will increase in value to perpetrators. As such,

individuals with good credit will likely be at a more significant

risk for identity theft and mortgage fraud schemes, and the continued

vulnerability of identifying information will allow perpetrators

the accesses necessary to commit such schemes.

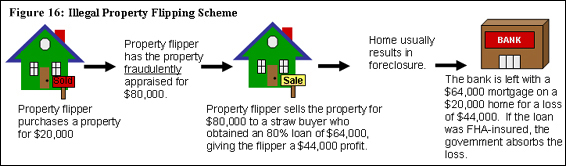

Builder-Bailout Schemes

Builders are employing builder-bailout schemes to offset losses

and circumvent excessive debt and potential bankruptcy as home

sales suffer from escalating foreclosures, rising inventory, and

declining demand. Builder-bailout schemes are common in any distressed

real estate market and typically consist of builders offering excessive

incentives to buyers, which are not disclosed on the mortgage loan

documents. Builder-bailout schemes often occur when a builder or

developer experiences difficulty selling their inventory and uses

fraudulent means to unload it. In a common scenario, the builder

has difficulty selling property and offers an incentive of a mortgage

with no down payment. For example, a builder wishes to sell a property

for $200,000. He inflates the value of the property to $240,000

and finds a buyer. The lender funds a mortgage loan of $200,000

believing that $40,000 was paid to the builder, thus creating home

equity. However, the lender is actually funding 100 percent of

the home’s value. The builder acquires $200,000 from the

sale of the home, pays off his building costs, forgives the buyer’s

$40,000 down payment, and keeps any profits. If the home forecloses,

the lender has no equity in the home and must pay foreclosure expenses.

Seller Assistance Scams

Mortgage fraud perpetrators are exploiting the depreciating housing

market by assisting sellers and providing buyers to conduct property

sales that are based on inflated appraisals. In a typical seller

assistance scam, a perpetrator solicits an anxious seller or his

real estate agent and offers to find a property buyer. The perpetrator

negotiates the amount that the property seller is willing to accept

for the home. The perpetrator then hires an appraiser to inflate

the property’s value. The property is sold at the inflated

rate to a buyer who is recruited by the perpetrator. The buyer

takes out a mortgage for the inflated amount. The seller then receives

the asking price for the home, and the perpetrator pockets a “servicing

fee,” the difference between the home’s market value

and the fraudulently inflated value. When the mortgage defaults,

the lender forecloses on the house, but is unable to sell it for

the amount owed as a result of the inflated value.

Seller assistance programs may be easily perpetrated in any

depressed market where sales of homes have languished and sellers

are motivated. The current instability in the housing market and

mortgage industry has created an ideal environment for perpetration

of this fraud. Seller assistance schemes eliminate the need for

the two property transactions that are required for illegal property

flipping, which involves first purchasing and then selling a property.

Some industry sources have coined the phrase “cash back purchase” or “one

transaction flip” to describe the scheme because it eliminates

the need for two property transactions to generate a profit.

Short-sale Schemes

Figure 17: Example of a fraudulent short sale:

Perpetrator

of a short-sale scheme; Perpetrator

of a short-sale scheme;

Perpetrator recruits a straw buyer to purchase a property. Perpetrator recruits a straw buyer to purchase a property.

Perpetrator has straw buyer secure a mortgage for 100% of

the property’s value. Perpetrator has straw buyer secure a mortgage for 100% of

the property’s value.

Perpetrator may have a straw buyer refinance the home and

obtain $30,000 for “repairs.” Perpetrator may have a straw buyer refinance the home and

obtain $30,000 for “repairs.”

Perpetrator pockets the $30,000. No repairs are made.

No payments are made so the mortgage will default.

Straw buyer informs the lender that the home will foreclose

and recommends the perpetrator as a potential buyer in a

short sale.

Perpetrator approaches lender prior to foreclosure and offers

to pay less for the home than would otherwise be received

in a competitive foreclosure sale.

Lender agrees to the short sale not knowing that the mortgage

payments were deliberately not made to create this short-sale

situation.

Perpetrator sells the property at actual value for a profit,

or has the property artificially inflated to conduct an illegal

property flip.

|

Short-sale schemes are desirable to mortgage

fraud perpetrators because they do not have to competitively bid

on the properties

they purchase, as they do for foreclosure sales. Perpetrators also

use short sales to recycle properties for future mortgage fraud

schemes. Short-sale fraud schemes are difficult to detect since

the lender agrees to the transaction, and the incident is not reported

to internal bank investigators or the authorities. As such, the

extent of short sale fraud nationwide is unknown. A real estate

short sale is a type of pre-foreclosure sale in which the lender

agrees to sell a property for less than the mortgage owed. In a

typical short sale scheme, the perpetrator uses a straw buyer to

purchase a home for the purpose of defaulting on the mortgage.

The mortgage is secured with fraudulent documentation and information

regarding the straw buyer. Payments are not made on the property

loan so that the mortgage defaults. Prior to the foreclosure sale,

the perpetrator offers to purchase the property from the lender

in a short-sale agreement. The lender agrees without knowing that

the short sale was premeditated. The mortgage owed on the property

often equals or exceeds 100 percent of the property’s equity (see figure17).

Foreclosure Rescue Scams

As in 2006, foreclosure rescue scams continued to be problematic

in 2007. Escalating foreclosures provide criminals with the opportunity

to exploit and defraud vulnerable homeowners seeking financial

guidance. The perpetrators convince homeowners that they can save

their homes from foreclosure through deed transfers and the payment

of up-front fees. This “foreclosure rescue” often involves

a manipulated deed process that results in the preparation of forged

deeds. In extreme instances, perpetrators may sell the home or

secure a second loan without the homeowners’ knowledge, stripping

the property’s equity for personal enrichment.

Identity Theft Used to Drain Home Equity Lines of Credit

HELOC Vulnerabilities

HELOCs differ from standard home equity loans because the homeowner

may borrow against the line of credit over a period of time using

a checkbook or credit card. They are aggressively marketed by

lenders as an easy, fast, and inexpensive means to obtain funds.

As such, an individual may open a HELOC account much like they

do a credit card. The funds may not be accessed for an extended

period of time, and the account balance may not be regularly

verified. |

Stolen customer identification information is

being used to compromise Home Equity Lines of Credit (HELOC) accounts.

To facilitate this

scheme, perpetrators pose as customers to establish HELOC Internet

account services and manipulate customer account verification

processes, including rerouting telephone calls, forging signatures,

using

passwords, and reciting recent account history. For example,

a perpetrator uses the account holder identification information

to contact a financial institution and request an advance of

funds

on a HELOC account. Once the advance is granted, the perpetrator

sends a facsimile to the financial institution requesting that

the funds be wire transferred to another account. On receipt

of the facsimile request, the financial institution contacts the

account

holder using the telephone number on record to verify the transaction.

However, the call is unknowingly forwarded to the perpetrator

who verifies the account holder’s information to complete

the wire transfer.

FBI Response As mortgage fraud crimes escalate, the burden on federal law enforcement

increases. With the anticipated upsurge in mortgage fraud cases,

the FBI employed additional strategies to proactively address the

crime problem. The FBI works with the Department of Justice (DOJ)-Mortgage

Fraud Working Group on a number of mortgage fraud related issues,

including the creation and finalization of standard loss valuation

criteria associated with mortgage fraud violations, and assisting

the banking industry with the construction of a centralized repository

of mortgage-related documentation.

The FBI also held a mortgage fraud summit with FBI Supervisory

Special Agents to address the most severe mortgage fraud problems

nationally. Currently the FBI has mortgage fraud working groups

or task forces in 32 field divisions, including Anchorage, Albuquerque,

Atlanta, Buffalo, Charlotte, Chicago, Cincinnati, Cleveland, Detroit,

Dallas, Denver, El Paso, Honolulu, Houston, Indianapolis, Jackson,

Kansas City, Louisville, Memphis, Miami, Minneapolis, Milwaukee,

Portland, Pittsburgh, Philadelphia, Phoenix, Sacramento, San Diego,

San Francisco, Salt Lake City, Tampa, and Washington, DC. The FBI

continues to encourage the use of undercover operations as an effective

technique to address mortgage fraud.

The FBI continues to work closely with its government and

industry partners to ensure that pertinent data is shared in a

timely fashion. Efforts are ongoing to educate the American public

regarding mortgage fraud crimes and perpetrators. Analytical products

are routinely disseminated to a wide audience. Working groups and

task forces remain ideal forms from which to coordinate multi-agency,

multi-jurisdictional investigations into mortgage fraud matters.

|