EU and U.S. Organic Markets Face Strong Demand

Under Different Policies

Carolyn

Dimitri

Lydia

Oberholtzer

David Sparer; courtesy of My Organic Market

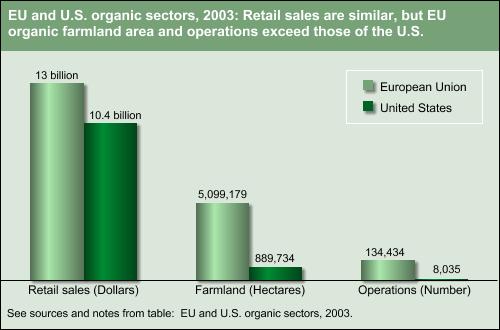

Organic markets in the European

Union member states and the U.S. are nearly the

same size in terms of retail sales. At the same

time, their farm sectors differ significantly, with

the EU-15 member states having more organic farmland

and more organic operations than the U.S. (see “EU

and U.S. Organic Sectors”). The U.S. and

EU Governments have also adopted markedly different

policy approaches to the organic sector. The EU

actively promotes the growth of the organic sector

with a wide variety of policies designed to increase

the amount of land farmed organically, including

government standards and certification, conversion

and support payments for organic farmers, targets

for land under organic management, and policies

supporting research, education, and marketing. The

U.S. largely takes a free-market approach: its policies

aim to facilitate market development through national

standards and certification and federally funded

grants that support research, education, and marketing

for organic agriculture.

The policy approaches adopted by

the two regions are the result of the inherently

dissimilar perspectives and histories that the EU

and U.S. governments have concerning agriculture,

the environment, and by extension, organic agriculture.

From the perspective of many EU countries, organic

agriculture delivers environmental and social benefits

to society, and is regarded as an infant industry

requiring support until it is able to compete in

established markets. This view of organic farming

as a provider of public goods affords an economic

rationale for government intervention in the market.

The U.S. Government’s approach, while acknowledging

organic agriculture’s positive impact on environmental

quality, treats the organic sector primarily as

an expanding market opportunity for producers and

regards organic food as a differentiated product

available to consumers. In such cases, government-devised

standards and labels facilitate market transactions

and allay consumer concerns about product identity.

EU

and U.S. Organic Sectors

The EU-15 countries (the countries that

made up the EU prior to entry of 10 new

countries in May 2004) are the focus of

this article because much of the data on

organic agriculture is on these countries.

All references to the EU in this article

refer to the EU-15: Austria, Belgium, Denmark,

Finland, France, Germany, Greece, Ireland,

Italy, Luxembourg, the Netherlands, Portugal,

Spain, Sweden, and the United Kingdom.

The EU and the U.S. together accounted for

95 percent of the $25 billion in world retail

sales of organic food products in 2003.

In 2003, retail organic sales in the EU,

at almost $13 billion (€10 billion),

exceeded the $10.4 billion (€8 billion)

of U.S. sales. However, per capita retail

sales were nearly equal, approximately $34

in the EU and $36 in the U.S.

The European organic markets are more mature

than the U.S. market. The EU’s organic

sector—particularly Western Europe—had

the fastest worldwide growth in the 1990s.

Growth in organic retail sales, however,

has slowed in some countries, with recent

growth rates across the EU averaging 7.8

percent per year. Forecasts of annual growth

for organic sales in the next few years

range from 1.5 percent for Denmark to 11

percent for the United Kingdom. U.S. organic

retail sales increased equally rapidly in

the 1990s, averaging 20 percent per year,

continued that pace well into 2005, and

are predicted to grow 9-16 percent per year

through 2010.

Certified organic land in the EU rose from

2.1 million hectares (5.2 million acres;

0.405 hectares = 1 acre) in 1997 to 5.1

million hectares in 2003, about 4 percent

of total agricultural area. U.S. organic

lands increased from 549,406 hectares in

1997 to 889,734 hectares in 2003—or

0.24 percent of all agricultural lands.

Thus, in 2003, the EU had over five times

the amount of organic farmland as the U.S.,

while the U.S. had three times as much total

agricultural land.

|

EU and U.S. Adopt Organic Agriculture Standards

and Certification

Both the EU and U.S. have established

organic food standards, as well as systems that

certify operations as organic. Such standards reduce

transaction costs by ensuring that attributes of

organic food do not have to be specified for each

transaction. They also resolve an information problem

since a product’s “organic” status

is unobservable to buyers, whereas the producer

has knowledge of the production and handling methods.

Certification is a process providing third-party

assurance that a product was raised, processed,

and distributed appropriately, and meets the official

organic standards. Thus, standards and certification

work in tandem. Certification also reduces opportunistic

behavior (such as falsely claiming a product is

organic) by creating a specific enforcement system.

In the U.S., penalties are clearly outlined for

firms that use the organic label inappropriately,

while the EU leaves enforcement up to individual

member states.

In the EU, labeling of organic plant products is

governed by EU Regulation 2092/91 (enacted in 1993);

organically managed livestock is governed by EU

Regulation 1804/99 (enacted in 2000). The regulations

set minimum rules for production, labeling, and

marketing for the whole of Europe, but each member

state is responsible for interpreting and implementing

the rules, as well as enforcement, monitoring, and

inspection. EU labeling of organic products is complex

because some member states have public labels, while

private certifiers in other member states have their

own labels, some well known to the public (e.g.,

KRAV in Sweden, Skal in the Netherlands, or the

Soil Association in the UK). In addition, the EU

introduced a voluntary logo in 2000 for organic

products that could be used throughout the EU by

those meeting the regulation. So far, few companies

are using the logo. Most recently, in December 2005,

the European Commission made compulsory the use

of either the EU logo or the words “EU-organic”

on products with at least 95 percent organic ingredients.

In the U.S., the 1990 Organic

Foods Production Act (OFPA) required that USDA establish

national standards for U.S. organic products. The

three goals of OFPA were to (1) establish standards

for marketing organically produced products, (2)

assure consumers that organic products meet a consistent

standard, and (3) facilitate interstate commerce.

The legislation targeted environmental quality by

requiring that an organic production plan pay attention

to soil fertility and regulate manure application

to prevent water contamination. It also included

environmental and human health criteria to evaluate

materials used in organic production. Along with

the USDA organic logo, the USDA National Organic

Standards (NOS) were implemented on October 21,

2002, replacing the prior patchwork system of State

organic standards.

Both the EU and U.S. rely on accredited agents to

certify organic farmers and handlers. The EU system

is more complicated, largely because member states

have some latitude as to how they approve and supervise

certifying entities, resulting in a great deal of

diversity among the states. A national authority

from each member state certifies that organic products

comply with EU law. These bodies, in turn, approve

other entities that are allowed to certify organic

production and handling processes. Most member states

have government-approved private certification bodies,

but some have public member state certification.

In addition, some member states and certifiers have

additional public or private standards, as well

as standards for products not covered under the

EU Regulation, such as fish and nonfood agricultural

products. Some certifiers require stricter standards

than those of the EU legislation. As a result, not

all EU certificates are acceptable to each certification

body. In contrast, in the U.S., agents are accredited

by USDA to carry out organic certification, and

the certification process is well defined so that

all farmers and handlers are certified according

to the same standard.

EU and U.S. organic sectors, 2003 |

Country |

Retail sales |

Organic operations |

Organic land |

Farmland under organic production |

|

Million euros |

Number |

Hectares |

Percent |

Austria |

400 |

19,056 |

328,803 |

9.7 |

Belgium |

300 |

688 |

24,000 |

1.7 |

Denmark |

339 |

3,510 |

165,146 |

6.1 |

Finland |

212 |

5,074 |

159,987 |

7.2 |

France |

1,578 |

11,377 |

550,000 |

1.9 |

Germany |

3,100 |

16,476 |

734,027 |

4.3 |

Greece |

21 |

6,028 |

244,455 |

6.2 |

Ireland |

40-50 |

889 |

28,514 |

0.7 |

Italy |

1,400 |

44,039 |

1,052,002 |

6.9 |

Luxembourg |

NA |

59 |

3,002 |

2.4 |

Netherlands |

395 |

1,522 |

41,865 |

2.2 |

Portugal |

NA |

1,507 |

120,729 |

3.2 |

Spain |

144 |

17,028 |

725,254 |

2.8 |

Sweden |

420 |

3,562 |

225,776 |

7.4 |

United Kingdom |

1,607 |

4,017 |

695,619 |

4.4 |

European Union1 |

9,966 |

134,434 |

5,099,179 |

3.9 |

U.S.2 |

8,047 |

8,035 |

889,734 |

0.2 |

| NA = Not available.

Note: U.S. retail sales dollars were converted

to euros using an exchange rate of $1.29 =

€1.00, May 2005.

1Some EU land numbers are provisional.

All EU hectares and farms are for certified

organic and in-conversion land. Numbers for

Sweden do not reflect the substantial hectares

that are managed organically but not certified.

In Sweden, these lands are given governmental

support payments as recognition by Sweden

and increasingly other Scandinavian countries

that financially supporting organic land management

for environmental gain does not necessarily

need to be linked to the marketing of organic

food, for which certification is a legal requirement.

In Sweden, these lands accounted for another

180,000 hectares and an estimated 12,500 farms

in 2003.

2The U.S. reports certified organic

acreage, which has been converted to hectares

(1 acre = 0.405 hectares). The U.S. does not

report farms or acreage in transition to organic

production, as does the EU, and does not report

subcontracted organic growers.

Sources: Various sources, cited in Market-Led

Versus Government-Facilitated Growth: Development

of the U.S. and EU Organic Agricultural Sectors,

by Carolyn Dimitri and Lydia Oberholtzer,WRS-05-05,USDA,

Economic Research Service, August 2005, available

at: www.ers.usda.gov/publications/wrs0505/.

U.S. operation and land numbers for 2003 are

available at: www.ers.usda.gov/data/organic/

|

The EU, Unlike the U.S., Subsidizes Organic Production

European governments (including

countries not in the EU, such as Switzerland) support

organic agriculture through green payments (payments

to farmers for providing environmental services)

for converting to and continuing organic farming.

The economic rationale for these subsidies is that

organic production provides benefits that accrue

to society and that farmers lack incentives to consider

social benefits when making production decisions.

In such cases, payments can more closely align each

farmer’s private costs and benefits with societal

costs and benefits. EU green payments partly compensate

new or transitioning organic farmers for any increase

in costs or decline in yields in moving from conventional

to organic production, which takes 3 years to complete.

EU support for organic agriculture falls under the

EU’s general agri-environment program that

is part of the Common Agricultural Policy (CAP).

The EU commission establishes the general framework

and co-financing, and each member state chooses

a set of policies from this menu of measures. The

1992 CAP reform (EC Regulation 2078/92) provided

the policy framework for EU member states to support

organic farming, and many of the payments currently

granted were implemented under this reform, dating

back to 1994. More recently, under Agenda 2000,

these measures were included in the rural development

program (Rural Development Regulation No. 1257-99),

a CAP reform carried out from 1999 to 2001. In 2001,

the EU-15 spent almost €500 million ($559 million;

the average annual exchange rate for 2001 was $1

= €0.895) on organic lands under the two measures,

with organic farms receiving average payments of

€183-€186 ($204-$208) per hectare, compared

with €89 ($99) per hectare paid to conventional

farms.

| EU agri-environmental

support and organic farming, 2001 |

|

|

Organic

land supported under agri-environmental programs1 |

|

|

Average

support premium for organic land |

| Country |

1992 CAP

reform |

Agenda 2000

|

Share of organic land

in policy support programs |

Public support of organic

land under 1992 CAP reform |

1992 CAP

reform |

Agenda 2000

|

| |

Hectares |

Percent

|

Thousand

euros |

Euros/hectare |

| Austria

|

36,193

|

210,833 |

89 |

67,905

|

211 |

286 |

| Belgium

|

13,032

|

3,616 |

74 |

3,416

|

187 |

269 |

| Denmark

|

79,731

|

78,347 |

94 |

16,377

|

137 |

199 |

| Finland

|

23,948

|

113,631 |

93 |

3,402 |

141 |

117 |

| France

|

54,727

|

82,508 |

33 |

23,951 |

196 |

188 |

| Germany

|

278,884

|

254,715 |

84 |

84,477 |

154 |

163 |

| Greece

|

4,928

|

10,614 |

50 |

17,505 |

401 |

445 |

| Ireland |

13,691

|

NA |

46 |

1,848

|

135 |

NA |

| Italy |

351,113

|

101,134

|

37 |

158,898 |

361 |

318 |

| Luxembourg

|

736 |

1,224 |

98 |

328 |

158 |

173 |

| Netherlands |

8,140

|

14,593 |

63 |

4,446

|

266 |

156 |

| Portugal |

26,970

|

90 |

38 |

3,779 |

137 |

111 |

| Spain |

142,591

|

112,554 |

53 |

14,544 |

69 |

195 |

| Sweden2 |

81,067

|

349,562 |

113 |

69,018 |

153 |

162 |

| UK |

285,633

|

122,330

|

60 |

27,591 |

42 |

45 |

| European

Union |

285,633

|

122,330 |

60 |

27,591 |

42 |

45 |

| NA = Not available.

1Organic support falls under EC

Regulation 2078/92, the agri-environmental

program of the 1992 Common Agricultural Policy

reform. After 1999, organic farming support

was part of Rural Development Regulation 1257/97,

under Agenda 2000.

2Sweden’s 113 percent signifies

that there is more policy-supported organic

land than certified area, reflecting the country’s

policy of supporting uncertified organically

managed lands (see note to table: EU and U.S.

organic sectors, 2003, on page 15).

Sources: Various sources, cited in Market-Led

Versus Government-Facilitated Growth: Development

of the U.S. and EU Organic Agricultural Sectors,

by Carolyn Dimitri and Lydia Oberholtzer,

WRS-05-05, USDA, Economic Research Service,

August 2005 |

Many EU Member States Set Targets

for Organic Land . . .

Many EU member states have established

targets for the share of farmland under organic

production in their organic farming action plans.

The EU governments use targets to convey their level

of commitment to growth in the organic sector. Some

countries have selected relatively attainable targets,

while others have chosen more ambitious ones. For

example, in 1995, Denmark announced a target of

7 percent of farmland certified as organic by 2000

and nearly reached this goal with 6 percent. Denmark’s

goal of having 12 percent of farmland certified

as organic by 2003, however, fell short. In response

to the 2000 Bovine Spongiform Encephalopathy (BSE)

crisis, Germany set a target of certifying 20 percent

of farmland as organic by 2010, a number that may

be hard to reach since only 4 percent of land was

in organic production in 2003.

. . . and Higher Funding for Research

Public funding of organic-related

research and programs is increasing in both the

EU and U.S., although European governments are financing

more programs with a broader range. European funding

supports innovation in production techniques, food

processing, food marketing, and food retailing,

and is estimated at €70-€80 million annually

from 2003 to 2005. Germany, the Netherlands, Switzerland,

and Denmark accounted for 60 percent of this. In

fiscal year 2005, the U.S. Government made approximately

$7 million available exclusively for organic programs,

including a certification cost-share program and

$4.7 million for a research grant program. This

amount is supplemented by other programs that benefit

organic producers, including funding for organic

research and technical assistance by Federal, State,

and local agencies that focus on organic agriculture.

Consumers in Both Regions Drive

Market Growth

In many ways, development of the

EU and U.S. organic markets has followed a similar

path. In the early days, the organic sectors were

supply driven and organic products were introduced

by farmers. More recently, consumers have been the

driving market force in both regions. Studies indicate

that most European consumers have shifted from buying

organic food for altruistic reasons to more self-interested

reasons, such as food safety and health. Ranking

behind these are taste, nature conservation, and

animal welfare. Similarly, U.S. consumers 20 or

more years ago bought organic food because of their

concern for the environment. In 2002, according

to national surveys, two-thirds of U.S. consumers

cited health and nutrition as a reason for buying

organic, followed by taste, food safety, and the

environment.

Consumers in both regions offer similar reasons

for why they do not purchase organic food. In Europe,

the main factors include high prices, poor product

distribution, little obvious difference in quality,

lack of information on the nature of organic products,

and doubts about the organic integrity of the items.

In the U.S., according to consumer surveys, price

leads the list of barriers to purchasing organic

products, followed by availability of organic products.

Despite these factors, retail sales are growing

rapidly in both regions.

In 2003, U.S. organic food sales were distributed

almost evenly between natural product/health food

stores (47 percent) and conventional retail stores

(44 percent), with direct sales and exports accounting

for 9 percent. This is a significant shift from

1998, when corresponding sales were 63 percent,

31 percent, and 6 percent. As in the U.S., mainstream

European supermarkets in some countries stock a

wide range of organic products. However, the main

type of retail channel for organic food varies across

countries. Over 85 percent of organic products are

sold through general food shops in Denmark; in Luxembourg

and Greece, organic foods are primarily sold through

other stores (e.g., organic/health food stores,

bakers, and butchers). In a number of countries,

including Ireland, Italy, France, Belgium, the Netherlands,

and Germany, sales are more evenly divided between

supermarkets and other stores.

Although the organic market is growing in both the

EU and the U.S., there are some problems with the

flow of products to market. In Europe, the organic

dairy and livestock industries, in particular, have

grown rapidly over the last decade, and in some

cases have outpaced the capacity of the market and

distribution channels. Organic milk supplies in

some regions were large enough to reduce organic

prices, causing some producers to exit the sector

because they were unable to turn a profit. The milk

glut, however, appeared to be giving way to shortages

in the UK, as demand continues to grow and supply

has declined. The U.S. organic food market was formerly

supply constrained, but now seems better able to

meet consumer demand, especially for fresh produce.

In the dairy market, however, with demand increasing

rapidly, suppliers are struggling to provide enough

organic milk to satisfy demand at current prices.

EU CAP Reform Renews Support for

Organic Farming

In June 2004, the European Commission

adopted an Action Plan for Organic Food and Farming,

with 21 policy actions aimed at facilitating ongoing

developments in the organic sector. The actions

are focused on three main areas: information development

e.g., increasing consumer awareness, improving statistics

on organic production and demand); encouraging member

states to apply a more coherent approach and to

make better use of the different rural development

measures; and improving/reinforcing the EU’s

organic farming standards and import/inspection

requirements.

The 2003-04 CAP reforms partially

shift agricultural policy toward a market-driven

policy and convert the current system of direct

payments to a single-farm payment independent of

the volume of production. The single-farm payments

began in 2005, with member states having discretion

in implementing them. The farm payment will require

cross-compliance with a wide range of standards,

including environmental, food safety, animal welfare,

and occupational health/safety. While the impact

on organic agriculture is still unknown, the overall

changes are expected to favor an expansion of organic

farming.

Market-Led Versus

Government-Facilitated Growth: Development of the

U.S. and EU Organic Agricultural Sectors, by

Carolyn Dimitri and Lydia Oberholtzer, WRS-05-05,

USDA, Economic Research Service, August 2005.

The ERS Briefing Room

on Organic Farming and Marketing.

|