Agricultural Contracting: Trading Autonomy for

Risk Reduction

Nigel

Key

James

MacDonald

Corbis

Farming is a risky business. Sharp

changes in farm production or farm prices, driven

by the vagaries of weather and disease, sudden shocks

to export markets, or the introduction of new technologies,

can lead to striking changes in a farmer’s

income in a short period of time. Agricultural contracts

can shift such risks from farmers to contractors,

and facilitate farm expansion. For these reasons,

more and more farm output is being produced under

contract. But farmers who contract often give up

something they prize—the autonomy that comes

with making management decisions.

Agricultural contracts are agreements

between farmers and their commodity buyers that

are reached before harvest or the completion of

a livestock production stage. They govern the terms

under which products are transferred from the farm,

and might specify the date of delivery, product

price, and required production practices. Contracts

create closer linkages between farmers and specific

buyers, and may afford the contractor (buyer) greater

control over agricultural production decisions.

The growth in contracting has come

largely at the expense of spot (or cash) markets,

where farmers retain full autonomy and receive prices

based on prevailing market conditions and product

attributes at the time of sale. In the case of hogs,

the risk reduction provided by contracts is valuable

to risk-averse farmers, who seek to avoid widely

fluctuating input and output prices. But hog farmers

also appear to value autonomy highly—ERS research

shows that a moderately risk-averse producer would

need to be paid a price premium of nearly 12 percent

to give up the autonomy of independent production.

Recent Trends in Contracting

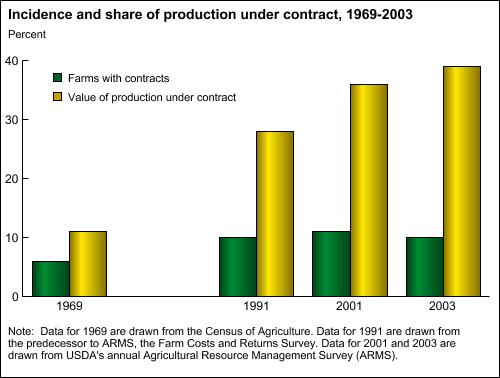

While the share of farms that

contract has remained steady, the share of production

under contract has grown. In 2003, only 1 in 10

U.S. farms held a contract—a share that has

remained stable since at least 1991. However, contracts

covered 39 percent of the value of agricultural

production in 2003, up from 11 percent in 1969,

28 percent in 1991, and 36 percent in 2001. Large

farms are far more likely to use contracts. Only

6 percent of small farms (sales under $250,000)

used contracts in 2003, compared with more than

60 percent of very large farms (at least $500,000

in sales). In turn, contracts covered 20 percent

of production from small farms and just over half

of all production from very large farms.

The trends toward contracts and

production on larger farms are parallel: family

farms with at least $500,000 in real sales (2003

dollars, adjusted for inflation) accounted for 45

percent of production by 2003, up from 32 percent

in 1989 (nonfamily farms held another 14 percent,

up from 6 percent in 1989). In the early 1990s,

contracts covered a quarter of crop production and

a third of livestock production; by 2003, they covered

31 percent of crop production and 47 percent of

livestock production (see “Production

and Marketing Contracts Defined”). Almost

all (96 percent) contract crop production is covered

by marketing contracts; production contracts are

common only for crops grown for seed and for some

vegetable and flower production. By contrast, production

contracts covered 71 percent of contract livestock

production, where absentee contractors can exercise

much more effective control over genetics and production

decisions.

Contracts offer several advantages to food buyers.

First, they can be used to ensure uniformity in

commodity attributes, stabilize production volumes,

and induce the spread of improved varieties, leading

to reduced production and processing costs and lower

consumer prices. Second, because contracts are frequently

used to coordinate the production of differentiated

products (such as high-oil corn, branded lean beef,

or organic produce), they can expand the variety

of food and agricultural products.

Contracts can have subtle and far-reaching impacts

on farmers and the organization of farming. Here,

we focus on the effects of contracting on a farmer’s

income risk, and the associated impacts on farm

structure and farmer autonomy.

Production

and Marketing Contracts Defined

ERS analyses distinguish production contracts

from marketing contracts. Under a production

contract, the farmer provides services to

the contractor, who usually owns the commodity

under production. For example, contractors

in poultry production usually provide chicks

to the farmer, along with feed and veterinary/transportation

services. The farmer then raises the chicks

to maturity, whereupon the contractor transfers

them to processing plants. Contractors often

provide detailed production guidelines,

and farmers retain far less control over

production decisions. The farmer’s

payment resembles a fee paid for the specific

services provided, instead of a payment

based on the market value of the product.

Marketing contracts focus on the commodity

as it is delivered to the contractor, rather

than the services provided by the farmer.

They specify a price or a mechanism for

determining the commodity’s price,

a delivery outlet, and a quantity to be

delivered. The pricing mechanisms sometimes

limit a farmer’s exposure to price

risks, and they often specify price premiums

to be paid for commodities with desired

levels of specified attributes (such as

oil content in corn, or leanness in hogs).

The farmer retains control over major management

decisions and hence retains more autonomy

than is available under production contracts.

A forward marketing contract, frequently

used in grain and livestock production,

typically establishes a base price before

harvest and provides for delivery of a given

quantity of a good within a specified time.

A futures contract is an agreement to trade

a commodity with specified attributes at

a specified time. Futures are distinguished

from generic forward contracts in that they

contain standardized terms, trade on a formal

exchange, and are regulated by overseeing

agencies.

|

Income Risks in Agricultural

Production

Income from farming is risky.

Price risks arise from unanticipated changes in

output or input prices, while yield (production)

risks result from unpredictable events (like drought,

flood, pest infestations, or disease) that affect

the quantity of production.

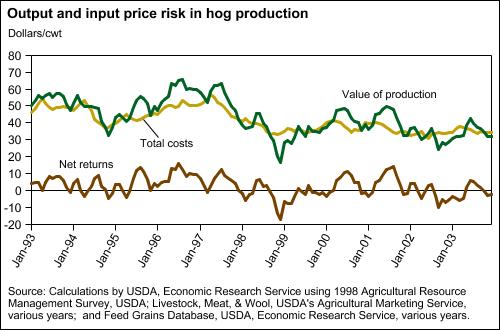

The hog market provides a striking example of price

risks, as embodied in average prices for finished

hogs (the value of production per hundredweight

(cwt)), total costs, and net returns for a typical

independent feeder-to-finish producer from 1993

to 2003. Feeder hogs usually weigh about 50 pounds,

while finished hogs usually weigh about 250 pounds.

Prices for finished hogs ranged from over $65/cwt

to less than $17/cwt (in 1998 dollars) from 1993

to 2003, and usually varied by $10-15 during any

given year. Costs, largely driven by fluctuations

in feed and feeder pig prices, ranged from $30/cwt

to $55/cwt, and fluctuated widely during any single

year. Consequently, net returns varied widely over

1993-2003: farmers who added 200 pounds per hog

earned up to $32 per hog, but also could have lost

as much as $35. With most production now on farms

marketing more than 5,000 hogs a year, these fluctuations

imply substantial income risk.

Risk can reduce farm production and efficiency and

lower farm household income. Years with low returns

(such as 1998-99) can lead to farm business failure

and to financial stress for households without income

from other farm enterprises or off-farm work. Banks

may be reluctant to advance credit to businesses

in extremely risky markets, or during downturns.

Greater price risks require farmers to devote more

time and effort to marketing decisions that could

otherwise be devoted to farm production or family.

Farm operator households can limit their exposure

to risks by altering production techniques, diversifying

the farming operation, combining on-farm and off-farm

work, or by using contracts that shift risks to

buyers.

Contracts Can Reduce

Farmers’ Risks

Since contract fees are usually

not tied to market prices, production contracts

can eliminate most or all of the output price risk

facing farmers. Production contracts can also largely

eliminate input price risks, because contractors

provide the inputs that comprise most of the operating

expenses. In 2003, contractors provided inputs representing

over 80 percent of operating expenses under broiler

production contracts, and over 70 percent of operating

expenses under hog production contracts. Contracts

could also eliminate production risk; however, most

hog and poultry production contracts retain some

production risk because they typically adjust base

payments to reflect feed efficiency and death losses.

Empirical analyses confirm that hog and poultry

production contracts can greatly reduce risk. Some

studies compared actual contract and independent

production, while others compared contract production

with simulated independent producers using the same

technology but facing price fluctuations for inputs

and outputs. The studies found that price risk caused

most of the income risk, that contracts can reduce

90 percent or more of price risk, and that some

contracts can substantially reduce yield risk.

Marketing contracts can also greatly reduce a farmer’s

output price risks. Forward marketing contracts,

frequently used in grain and livestock production,

establish a base price before harvest and commit

the farmer to delivery of a given quantity within

a specified time. Forward contracts can set an exact

price, or they can set a “basis” price,

tying a contract price to a price in the futures

market, plus or minus a specified amount (the basis).

Farmers can then offset the price fluctuations in

the contracted crop by hedging with the purchase

of a futures contract, thus eliminating price risks.

Marketing contracts can also mitigate risks from

input prices and yields. Product payments can be

based in part on input prices. Some crop contracts

commit farmers to deliver the production from a

particular acreage rather than an outright quantity.

Under such acreage contracts, the producer still

obtains revenue only from the amount delivered,

but does not have to make up production shortfalls

by buying in the cash market to fulfill contract

terms.

Contracts, Risk, and

Farm Structure

Contract producers in any given

commodity tend to be much larger than independent

producers. Recent research suggests that contracts

can facilitate farm expansion, partly through risk

reduction.

By reducing price risks, production and marketing

contracts can make it easier for farmers to obtain

credit and thus expand operations. Banks lend more

to contract producers than to independent producers,

even when producers have the same amount of financial

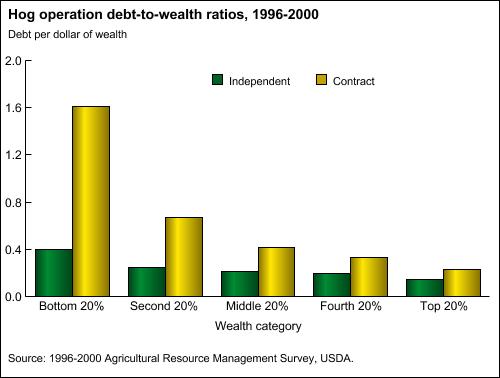

wealth. Because contract producers can call on greater

financial resources, they can generate significantly

more production than independent producers who have

similar levels of wealth. For example, among the

least wealthy farmers, contract producers are able

to obtain $1.60 in loans for every $1.00 in wealth,

while independent producers from the same wealth

group borrow $0.40. Production contracts almost

eliminate the need for short-term credit to finance

operating expenses, thereby allowing the farm to

redirect some borrowing to other farm activities.

Since very large farms tend to be operated by households

that derive most of their income from farming, contracts

also serve to reduce household income risks from

operating at such a large scale. As a result, expanding

use of contracts may be one factor driving the shift

of production to larger farms.

Since risk reduction benefits farmers, we would

expect them to pay something for it; that is, we

would expect them to accept contracts offering lower

returns than they could expect from independent

production. However, our research shows that contract

production (lower risk) frequently yields higher

returns than independent production (greater risk),

even when contract and independent operations produce

very similar products. At first glance, this suggests

either that farmers do not value risk reduction

or that contract operations produce output of superior

quality. A more plausible explanation is that contracts

force farmers to give up their highly prized autonomy—and

farmers must be paid to do that.

Autonomy Matters to

Farmers

Farmers may derive satisfaction

from noncontract production because it offers independence,

a sense of responsibility, and pride from self-determination

in farm management. Farmers who value such independence

would need to be compensated by contractors in order

to give up the satisfaction from independent production.

ERS recently investigated the tradeoff that hog

farmers make between risk reduction offered by contracts

and loss of autonomy. The evidence suggests that

farmers place great value on both autonomy and risk

reduction. A risk-averse farmer is willing to accept

a lower average income in exchange for less income

variability. Comparing the variation in net returns

under independent and contract hog production, we

estimate that the risk reduction offered through

a typical production contract was worth about $2.61/cwt

to a moderately risk-averse farmer, or 4.9 percent

of the average price for market hogs during the

1990s.

To estimate the value farmers place on autonomy,

we used USDA’s Agricultural Resource Management

Survey of hog producers to estimate the difference

in net returns between contract and independent

production. If risk reduction was the only factor

influencing farmers, we would expect contractors

to offer lower prices to contract producers, and

contract producers would realize lower returns from

hog production than independents. But instead, our

estimates indicate that for moderately risk-averse

farmers, the expected return from contract production

exceeded the expected return under independent production

by $3.68/cwt. Since we might expect hog farmers

to willingly give up $2.61/cwt for the risk reduction

provided by a contract, and we find that they instead

receive a premium of $3.68/cwt to accept a contract,

the difference between the two estimates ($6.29

per cwt) reflects the value of autonomy.

| Estimated

risk and autonomy premia by degree of risk

aversion for hog farmers |

| |

Risk

premium |

Autonomy

premium |

| Degree

of risk aversion |

Dollars/cwt |

Percent

of average price |

Dollars/cwt |

Percent

of average price |

| Risk-neutral |

0.00

|

0.0 |

3.68

|

6.8 |

| Moderately

risk-averse |

2.61

|

4.9 |

6.29 |

11.7 |

| Strongly

risk-averse |

5.22

|

9.7 |

8.90 |

16.6 |

|

Notes: The average price for

1988-1997 was $53.75 per hundredweight (cwt)

gain in 1998 dollars. The risk premium is

the value that a farmer would be willing to

pay for the risk reduction provided by a contract.

The autonomy premium is the value that a farmer

would have to be paid to give up independence

in decisionmaking. |

Farmers are not unique in valuing

autonomy highly; other studies have demonstrated

individuals’ willingness to pay for the opportunity

to be self-employed and make management decisions.

For example, a recent study of nonagricultural employment

found that individuals were willing to give up about

35 percent of their income in order to be self-employed

rather than to be paid employees.

Looking Ahead

Farm production is shifting from

smaller to larger family farms and from spot markets

to contracts. Technological developments may underlie

much of the shift to larger farms, but expanded

use of production and marketing contracts supports

that shift by reducing financial risks for farm

operators. For farm operators, contracts provide

benefits from reduced risks, but also impose costs

from loss of managerial control and reduced autonomy.

However, the gains to contractors

from contract production have been substantial enough

to support the additional compensation that must

be offered to farmers to surrender some of their

autonomy under contracts. With substantial gains

to contractors, continued expansion of contracting

is likely, with its associated implications for

farm size and for farm operator risks and returns.

In some commodities, that expansion may build on

itself and accelerate: as spot markets in some commodities

become quite thin, even producers who would prefer

to farm independently and use spot markets may seek

contract alternatives. In turn, USDA price reporting

systems, traditionally based on spot market transactions,

may need reconfiguring to deal with markets in which

most transactions occur through contracts.

Agricultural Contracting

Update: Contracts in 2003, by James MacDonald

and Penni Korb, EIB-9, USDA, Economic Research Service,

January 2006

"How Much Do Farmers Value Their Independence?”

by Nigel Key, Agricultural Economics 33(2005):

117-126

Contracts, Markets,

and Prices: Organizing the Production and Use of

Agricultural Commodities, by James MacDonald

et al., AER-837, USDA, Economic Research Service,

November 2004

"Agricultural Contracting and the Scale of

Production,” by Nigel Key, Agricultural

and Resource Economics Review, Vol. 33, No.

2 (October 2004), pp. 255-271

Did

the Mandatory Requirement Aid the Market? Impact

of the Livestock Mandatory Reporting Act, by

Janet Perry, James MacDonald, Ken Nelson, William

Hahn, Carlos Arnade, and Gerald Plato, LDP-M-135-01,

USDA, Economic Research Service, September 2005

"Losing

Under Contract: Transaction-Cost Externalities and

Spot Market Disintegration," by Michael

J. Roberts and Nigel Key, Journal of Agricultural

& Food Industrial Organization, Vol. 3, No.

2, Article 2, 2005

|