Pensions

Over the past few decades, there has been a shift in the types of pensions offered

by employers from defined benefit only (in which a specified amount is typically

paid as a lifetime annuity) to defined-contribution only (in which the amount of

future benefit varies depending on contributions and investment earnings).

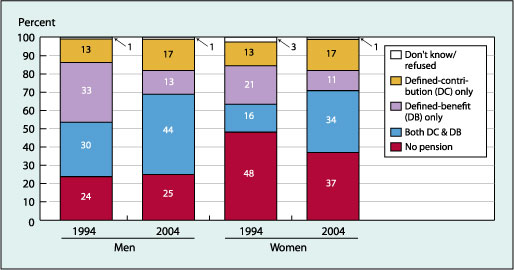

Chart 6. Percentage of people aged 55–64 who participated in a pension plan with an employer during their worklife, by pension type and sex, 1994 and 2004

Note: The measurement of pension participation reflects a report that

the person participated in a pension plan in the original or any subsequent interview

or in past jobs. Subsequently, some will have left the job and transferred the pension

money out of the pension plan to an Individual Retirement Account, an annuity, or

other uses. See Appendix B for description of the Health and Retirement Study.

Source: Health and Retirement Study.

- Between 1994 and 2004, the lifetime pension participation

of men remained stable at about 75 percent; the type of pension plans they participated

in changed.

- Between 1994 and 2004, the percentage of men aged 55–64 who

participated only in a defined benefit plan decreased from 33 percent to 13 percent,

the percentage who participated only in a defined-contribution plan increased from

13 percent to 17 percent, and those who participated in both defined-benefit and

defined-contribution plans increased from 30 percent to 44 percent.

- The percentage of women aged 55–64 who have not participated

in a pension decreased from 48 percent in 1994 to 37 percent in 2004.

- Women also experienced a shift in the type of pension they

have. Between 1994 and 2004, the percentage of women aged 55–64 who participated

in only a defined-benefit plan fell by one-half from 21 percent to 11 percent, the

percentage who participated in only a defined-contribution plan increased from 13

percent to 17 percent, and those who participated in both defined-benefit and defined-contribution

plans more than doubled from 16 percent to 34 percent.

Last Modified: 12/31/1600 7:00:00 PM