|

|

|

|

|

||||

|

|||

| Setup Instructions |

| Rural

Ambulance Service Budget Model U.S. Department of Health and Human Services Health Resources and Services Administration Office of Rural Health Policy This document was prepared under HRSA contract # 250-03-0022, U.S. Department of Health and Human Services, Health Resources and Services Administration, Office of Rural Health Policy. Printer-Friendly Acrobat Version (985 kb) Contents

QuickBooks Easy Step Interview APPENDIX A: REMSTTAC Stakeholders' Group We are very pleased to offer you the Rural Ambulance Service Budget Model. This budgeting and financial management tool is an important part of the financial toolkit under development for rural ambulance services and rescue squads that do not have the resources to purchase such tools themselves. We recognize that rural ambulance services are an essential component of rural health care systems. Budgeting and financial management is but one of the many challenges facing rural Emergency Medical Services (EMS) agencies in the United States today. Rural EMS agencies also face such issues as recruitment and retention of qualified, trained human resources; increasing education and training requirements; increasing cost of equipment and increasing funding challenges, to name a few. With capital and operating costs increasing and reimbursement decreasing, management of limited financial resources is becoming a more important component of rural ambulance service management and governance. The Rural Ambulance Service Budget Model provides a management tool that enables a service to enter known financial information into a simple, yet elegant preprogrammed spreadsheet. Once information is entered into the model, a budget is automatically calculated that can be exported into off the shelf accounting software and monthly budget versus actual results can be used to better manage limited funds and plan for improved financial management of the service. This publication was developed by the Federal Office of Rural Health Policy, Health Resources and Services Administration in cooperation with the Rural Emergency Medical Services and Trauma Technical Assistance Center. It is hoped that this Rural Ambulance Service Budget Model will serve as a valuable tool for rural ambulance services and provide for better informed fiscal management in the challenging realm of out of hospital health care. Please see the special note on the following page concerning the ongoing availability of this document.

A special note to the reader: In FY 2000, Congress funded the Trauma and EMS Program within the Department of Health and Human Services, Health Resources and Services Administration (HRSA) to foster the development of appropriate, modern systems of such care. Ten percent of the funding provided for that program was earmarked for "rural" trauma and EMS and was administered by HRSA's Office of Rural Health Policy (ORHP). In FY 03, ORHP established the Rural Emergency Medical Services and Trauma Technical Assistance Center (REMSTTAC). This product represents one of the deliverables identified in the REMSTTAC contract. Congress zeroed out the HRSA Trauma and EMS Program in FY 05 and ORHP, therefore, lost the resources necessary to continue REMSTTAC. However, as part of ORHP's ongoing commitment to rural EMS, this and other products will continue to be available from two sources. These include the Critical Illness & Trauma Foundation (www.citmt.org) [not a government Web site], the parent organization of the previously funded REMSTTAC, and the Rural Assistance Center (www.RAConline.org) [not a government Web site] In the early stages of the development of the Rural EMS and Trauma Technical Assistance Center (REMSTTAC) a diverse group of stakeholders were brought together to provide input and direction regarding how the TA center might best meet the needs of its constituency groups. These three groups are broadly defined as:

In developing and prioritizing the REMSTTAC scope of work, the stakeholder group recommended the development of a financial tool kit that would provide specific financial and budgeting tools to rural EMS agencies and organizations that may be managed by volunteer EMS providers or others with limited experience or training in the financial and budgeting aspects of public, private or not-for-profit organizations. As cited in the Rural and Frontier EMS Agenda for the Future (2005), many rural and frontier EMS services "have no expertise or infrastructure for collecting fees or maintaining the business functions." The need for this toolkit has been further validated through a series of "town hall" meetings conducted in the intermountain west and New England States with representation from local EMS leadership. In response to this direction, a task group was organized within REMSTTAC to develop tools for this financial tool kit. The task group, coordinated by a REMSTTAC staff person, includes a business/financial consultant and representatives of: the National Association of State EMS Officials, the Rural Health Resource Center and the National Association of Emergency Medical Technicians (EMTs). In addition to the considerable knowledge and expertise of these task group members, tasks and priorities are reviewed by the entire stakeholder group. Their input and direction guides the work of the task group. The task group and stakeholders identified the following priorities for toolkit development:

The Sample Chart of Accounts represents the first drawer in the Financial Toolkit. It provides a bookkeeping and accounting framework for rural EMS services and is consistent with generally accepted accounting principles. It is organized as follows:

Some EMS services may not need all the items shown in the sample Chart of Accounts. Others may find the need to add accounts. Either way, the sample provides a model with the most commonly used accounts in the accounting structure of a rural EMS organization.

The Rural Ambulance Service Budget Model (RASBM) fills a very large drawer in the REMSTTAC Financial Toolkit. The Budget Model is a customized Microsoft Excel® spreadsheet. Part of the Microsoft Office® software family, Excel® is commonly available to most computer users and is often bundled on computers marketed in the U.S. Where Excel® is not already installed on a personal computer; the software can be purchased inexpensively from most office supply stores or on-line software vendors. If you have other spreadsheet software REMSTTAC will assist you in the conversion or importation of this template. This tool was developed to assist rural ambulance services in establishing an annual budget. It also helps calculate the value of services donated to the ambulance service by another entity and the value of donated services provided by the ambulance staff to the community. Why should you prepare and use a budget?

A budget is a record and forecast of all cash sources and cash expenditures.

Maintaining a budget allows you to estimate future needs and profits

and to plan for managing any discrepancies. At minimum, your budget

should track the expenses of running your service compared to the

money generated. A detailed budget will allow you to do much more

than simply track revenue and expenses; it will provide the framework

for quantifying the overall value of your ambulance service. This

becomes especially important when seeking community support, reporting

to oversight boards or committees, and in applying for grants or

loans. The Rural Ambulance Service Budget Model provides step-by-step

instructions for organizing important data regarding your service.

The first step in using this REMSTTAC Budget Model is to copy the .xls file from the enclosed CD ROM onto your computer hard drive. This file should reside in the directory on your hard drive where other Excel® spreadsheet files are maintained. Do not attempt to fill in your service information on the file on the CD ROM. DISCLAIMER: The rural EMS industry is widely diverse and this budget model will not be appropriate for, nor was it intended to serve, all ambulance services. Ambulance services are encouraged to engage the services of a professional accountant as necessary. The REMSTTAC Budget Model and its associated Chart of Accounts are the first of several drawers in the Financial Toolkit to be developed. Additional tools under consideration are:

We welcome your feedback on the REMSTTAC Budget Model and associated Tutorial. You may contact us at: Rural Ambulance Service Budget Model

Congratulations! You've taken an important first step in deciding to use the budget model tool provided by the Department of Health and Human Services, Health Resources and Service Administration's Office of Rural Health Policy (ORHP). This product was developed by the Rural Emergency Medical Services & Trauma Technical Assistance Center (REMSTTAC) under a previous contract with ORHP. This tool was developed to assist rural ambulance services in establishing an annual budget. It also provides some utility in demonstrating the value to a community for services donated to the ambulance service by another entity (such as dispatch functions provided free by the sheriff), and the value of donated services provided by the ambulance staff to the community (such as the value of volunteer labor contributions). The tool is one of a series of "EMS Management Tools" being produced. The model will also give you the ability to upload our national standard EMS Chart of Accounts and the budget you develop directly into the Intuit's QuickBooks® program. QuickBooks® is a proprietary accounting program that can help you manage your finances, print reports, provide payroll functions, and more. We chose QuickBooks® to provide an interface because Intuit supports it fully on-line and provides comprehensive help and training. The rural EMS industry is widely diverse and this budget model will not be appropriate for, nor was it intended to serve, all ambulance services. Ambulance services are encouraged to engage the services of a professional accountant as necessary. This model consists of a series of visible and hidden rows and columns. It is designed to be completed sequentially; however it is possible to start one section, skip part, and then return. Green areas of the worksheet are always fine to fill in. Yellow areas provide caution or an either/or Statement. Filling in red sections, or any section on the budget page will override formulas. Do so with caution and monitor the effect on the rest of the model. These areas should be changed only by those with strong expertise in spreadsheet design and use. First, print the document included in this package called "Budget Model Worksheet.doc". Keep it handy: we'll be filling it in as you move along in this tutorial. Next, open the budget model by double clicking on the "Budget Model.xls" file. The first page you see is the Demographics page.

(Click on Image to see full-size image) Spreadsheets are organized into columns and rows. Columns are identified by letters (A to Z and then AA to ZZ, and so on). Look at the words "Test Ambulance Service" above, (they are at the top of the yellow area). The area those words appear in is called a cell. The reference for that cell is B6. That is because those words appear going across the top in column B and going down to row six. The cell reference for the words "I am preparing a budget for the year:" is A19. The words in cell C7 are "on all subsequent worksheets". Now look at the bottom of the graphic. Under the number for row 31 you see a group of four arrows pointing left or right and then seven words: QuickBooks, Demographics, Vehicles, Building, Other Capital, Staffing and Training. (Your spreadsheet program may display some, all, or all of these plus others.) These are tabs. We're working on the Demographics tab right now. To switch to the Vehicles tab, click on the word Vehicles and that tab will be displayed. If you need more assistance in learning about spreadsheets, please refer to the Help function on your spreadsheet program. What this tab does: The transport and miles information you enter on this page will become important as you get to the final steps of the model. You will use them to help determine what you will need to set your rates at in order to cover your costs.

(Click on Image to see full-size image) On this tab you will enter the name and other information about your ambulance service. In cell B15, enter the number of emergency ambulance runs your service performed last year that resulted in a bill being sent. Do not include responses that did not result in a bill. In cell B16, follow the same procedure to record the number of non-emergencies. In cell B17, enter the total number of miles billed. Try to be accurate with these numbers, they are important later. STOP - IT IS TIME TO SAVE YOUR WORK. This is the first save of your work. To save your file to your hard drive, click on File and then Save-As. Choose a location on your computer to save your work. Rename the file if you would like. We'll have you save your data frequently as you work through this tutorial, always to the same place. Also, if you take a break, when you come back to continue working, be sure to open the saved spreadsheet from your hard drive, not the template version you opened to begin this tutorial. Now it's time to move to the Vehicles tab. What this tab does: The information you enter on this page feeds necessary information to your final budget. For vehicles you lease, it will transfer the lease costs into your budget. For vehicles you purchase, it will set up depreciation. Depreciation is an important part of your final budget. By depreciating over time, you will be saving money in the bank to replace your vehicles when their useful life is exhausted. Since the cost of vehicles will increase over time, depreciation alone will not produce enough cash to meet the increased price when replacement is necessary. You will need to supplement depreciation with either cash reserves, or funds produced another way.

(Click on Image to see full-size image) Let's make this friendly for you first. Click on cell A16 and replace the words "Ambulance #1" with terminology that is familiar to you. Call it Unit 101, Squad 54, or whatever label will help you recognize this as your primary ambulance. If you have more than one ambulance, replace the text in A17 through A25 similarly. If you are LEASING any of these ambulances, enter the monthly lease amount in the yellow area on the same row as that vehicle. For leased vehicles, you will not complete columns C to G. For all vehicles - LEASED AND OWNED - fill in columns K (Vehicle License), L (Vehicle Registration) and M (Insurance). In column K, fill in the amount paid in vehicle licensing fees from your State EMS agency, if any, for all vehicles. The amount should be an annual amount, so if the State charges you once every two years, divide the total by two and enter that amount. Column L is for vehicle registration and license plates from your State vehicle licensing bureau, if any, for all vehicles. Enter an annual amount. Column M is for one year of vehicle insurance. Fill in the annual amount for each of the ambulances. If you LEASE your vehicles follow the same process as above for any non-ambulances you might have, using rows 32-36. Then, you're done with this tab, unless you also own some of your vehicles. We'll use columns C to G for vehicles you OWN (or are making loan payments). If you normally replace your vehicles based on a specific number of years, enter the number of years in cell G10. If you normally replace vehicles when their mileage hits a specific level, enter the target number of miles in G11. Do NOT put values in both cells, but also make sure you fill in one of them. If you don't follow either of these replacement milestones, pick one and estimate a number for it. For each owned ambulance enter the following information: Cell C16 (through C25) - the year the ambulance was acquired. Cell D16 (through D25) - the cost of the vehicle the year it was purchased. Cell E16 (through E25) - the cost of any capital equipment you purchased with the ambulance. Many ambulance services will purchase new stretchers, mobile radios, defibrillators and other capital equipment each time they purchase an ambulance. If you follow this process, enter the total value of capital items that are purchased with the vehicle. Capital is commonly defined as those items that cost more than $500 and have a useful life exceeding one year. It is important to keep track of what equipment is represented in this figure. It will roll into the total vehicle depreciation calculation; therefore, it should not be listed again later with other capital equipment. Cells F16 and G16 (through F25 and G25) - if you entered a number of years in cell G10, you do not need to fill in these numbers; your depreciation will be calculated based on the number of years the vehicle is in service. If you entered a number of miles in G11, then you need to complete F16 and G16. In F16, enter the odometer reading of your vehicle at the beginning of the previous 12 month period and the odometer reading at the end of the 12 month period. Since you replace your vehicles based on miles driven, depreciation will be calculated based on the total number of miles driven last year. Complete the same information on rows 32-36 for all non-ambulances you own or lease. STOP - IT IS TIME TO SAVE YOUR WORK. Click on File and then Save. Now it's time to move to the Building tab. What this tab does: The Buildings tab will record rent and mortgage information. It sets up depreciation for buildings owned by the ambulance service. In addition, it estimates the value of space donated for your use. Pay attention to donated space for two reasons: first, it will help you understand the value of the donation, and secondly, you can publicly report the value of the donation.

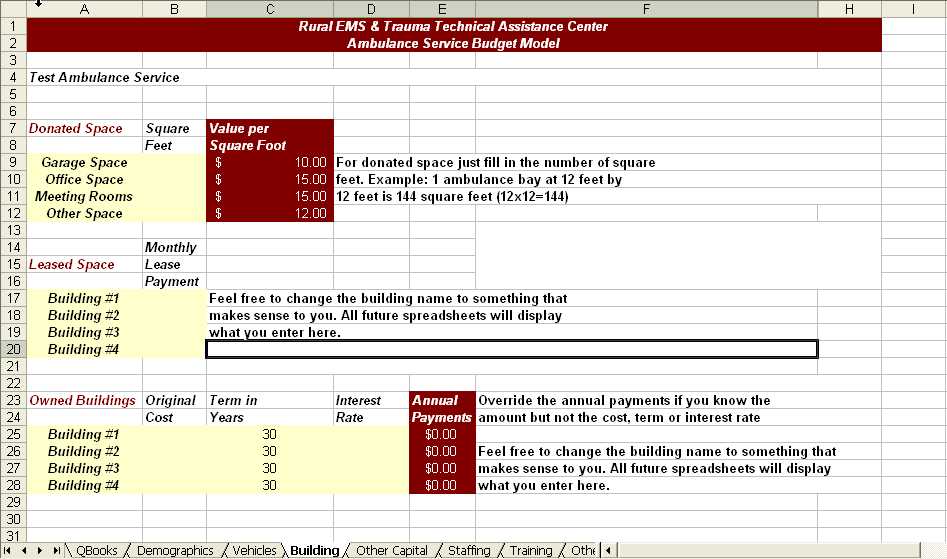

(Click on Image to see full-size image) Rows 7-12 are for donated space. For each category of space, enter the number of square feet in column B. Column C has some default square footage price estimates. If you know a specific value for your area, you can override these numbers with actual values. Rows 14-20 are for lease payments made for space you occupy but don't own. Enter your monthly lease payment for each building. Rows 23-28 are for buildings you own. If you know the original cost, interest rate and mortgage term, enter those values and the annual payment amount will be automatically calculated. As an alternative, if you know the annual mortgage cost, you can just type it into the red area. NOTE: for owned buildings, enter ANNUAL information and for leased buildings, enter MONTHLY lease payments. STOP - IT IS TIME TO SAVE YOUR WORK. Click on File and then Save. Now it's time to move to the Other Capital tab. What this tab does: The Other Capital tab collects information to set up depreciation for capital items that are not included on the Vehicles tab. Capital items are those that cost over $500 and have a useful life that exceeds one year.

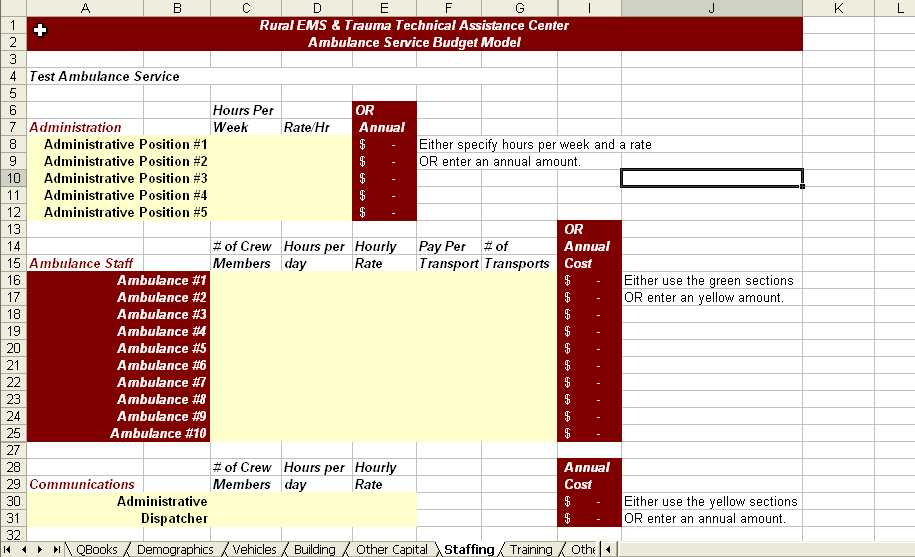

(Click on Image to see full-size image) The Other Capital tab has 4 categories common capital equipment: communications, patient care, mechanic and office equipment. If you have equipment that doesn't fit into one of these categories, you'll have to make it fit somewhere. Use one of the "other" categories on rows 12, 17 or 25. Type over the word "other" to remember what equipment you placed there. In each category, enter the purchase cost of the item(s) purchased. Feel free to change the number of years in the "Years Useful Life" columns. If you included your stretcher(s) or defibrillator(s) as equipment on the vehicle tab, do not enter them here. STOP - IT IS TIME TO SAVE YOUR WORK. Click on File and then Save. Now it's time to move to the Staffing tab. What this tab does: The Staffing tab collects information about how you staff your ambulance service and will estimate your salary costs for next year.

(Click on Image to see full-size image) Let's make this friendly for you. If you have

administrative staff, type over the label Administrative Position

#1 in cell A8 with either the name or job classification for the

person filling the role. If you have more than one administrative

position (billing, secretary, etc.) do the same on A9 to A12. Example: ABC ambulance service staffs one

ambulance 24 hours a day with two full-time staff. They have a second

ambulance which uses on-call staff that are each paid $2 per hour

while on call, and $20 per run. On their 500 billable runs, the

full-time staffed ambulance completes 450 and volunteers complete

the other 50. In cell F16 you will enter the average pay rate of the full-time staff. If your staff are paid different hourly rates depending on their longevity with the service, simply add up all of their pay rates and divide by the number of employees and this will give you the average hourly rate. The typical ambulance service will pay some overtime during the course of the year. Estimate the number of overtime hours and fill in the blocks below. Use that result as the Hourly Rate for cell F16.

In cell D16 enter "2" for the

volunteers that are on call. In cell E16 enter 24. In cell F16 enter

"2" for the $2 per hour call time. In cell G16 enter 20

for the per-run stipend and in cell H16 enter 50 - the number of

transports completed by the volunteers. STOP - IT IS TIME TO SAVE YOUR WORK. Click on File and then Save. Now it's time to move to the Training tab. What this tab does: The Training tab collects information about your ongoing education costs.

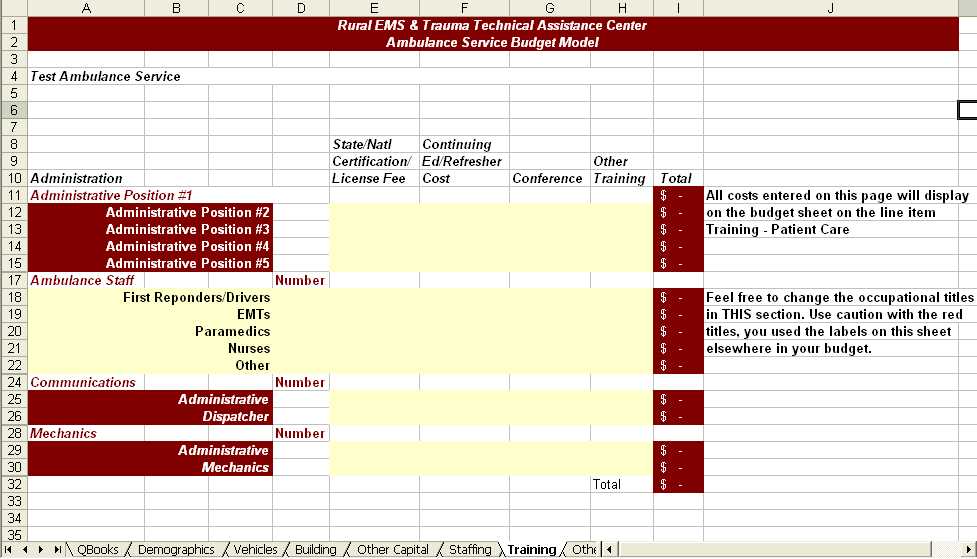

(Click on Image to see full-size image) The amounts entered into this tab should be ANNUAL amounts per person. Many States require certification/licensure renewal every two or three years. If your service pays these fees or reimburses staff for them, divide the fee paid by the number of years the certificate/licensure is valid. See an example on the Budget Model Worksheet for how to calculate this result. The example is based on a State certification/licensure fee of $40 for fours years and a National Registry fee of $25 for two years. Use a similar process to calculate the annual cost of refresher courses if your service pays for them. If your service pays for conference attendance, include the average cost of conference registration plus travel expenses in column G. If there is other training that you pay for (for example ACLS or PALS courses), report an average ANNUAL amount that includes reimbursed travel costs. For example, let's say you pay a registration fee of $150 and reimburse on average $50 in travel related costs for ACLS. Since the refresher course is every two years, the cost per two year cycle per person is $200. However, you should report the ANNUAL cost per person ($100). STOP - IT IS TIME TO SAVE YOUR WORK. Click on File and then Save. Now it's time to move to the Other Expenses tab. What this tab does: This tab collects information about expenses that have not been recorded elsewhere on any tabs.

(Click on Image to see full-size image) This tab requires some detective work on your part. You will need to go through your records from last year to determine the total amounts paid for these various categories. The tab is organized into six different sections: patient care expenses, dispatch expenses, administrative expenses, interest expense, building expenses, and vehicle expenses. DO NOT CHANGE THE ACCOUNT NUMBERS OR DESCRIPTIONS ON THIS TAB. They are part of a national standard EMS Chart of Accounts. If you don't see a category that matches they way you have previously recorded your expenses, you'll need to find the best fit. If you use QuickBooks® or some other proprietary software, you can set-up sub-accounts to these categories later to match the way you keep track of expenses. On the Budget tab that follows this one, some benefit costs will be automatically calculated for you, using an average benefit rate of 30 percent of salary. If you don't want to use this average rate and you know the actual costs of the red areas in column C, fill in the actual amount in the benefits cells under patient care, dispatch and administration in column C. Change the (0.3) in the formula to reflect your actual benefit percentage. STOP - IT IS TIME TO SAVE YOUR WORK. Click on File and then Save. Now it's time to move to the Budget tab. What this tab does: This tab displays the calculations and amounts entered on all previous tabs. It also demonstrates the value of contributed items, either by other agencies to yours, or by your volunteer staff. It uses an inflation factor to increase your budget amounts from last year to the current year.

(Click on Image to see full-size image) About the patient care section: If you elected to fill in the red cells in the previous tab for benefits you should make the amount in cell C11 "0." Otherwise, benefits will be reported twice. If your total employee salaries do not equate to at least $10 per hour for two people, cells F10 and F11 will report an amount that volunteers contribute. This number can be a powerful tool for you as you report the estimated dollar value you provided to the community through the volunteers' service. Feel free to change the Percent Inflation on any or all of the rows in column D to match your particular circumstances. Column G is calculated by taking the actual or estimated information in column C times the inflation factor in column E for that row. About the dispatch section: Many ambulance services do not operate their own dispatch centers; the service is dispatched by the police or sheriff's departments. If you haven't reported an amount equivalent to $15 per hour, 24 hours a day in dispatch salaries, this sheet will estimate the value that your dispatch center provides to you. If you elected to fill in the red cells in the previous tab for benefits you should make the amount in cell C24 "0." About the administrative section: Many ambulance services have part-time managers. If you have not reported at least $15 per hour for 40 hours per week in administrative payroll costs, this sheet will report the value of the contribution to the service by your management staff. If you elected to fill in the red cells in the previous tab for benefits you should make the amount in cell C36 zero.

(Click on Image to see full-size image) About the building section: Cell E24 will report the annual value given to the ambulance service for donated space that was reported on the building tab.

(Click on Image to see full-size image) Row 87 provides a total of your expenses from last year, the value added to the service by donated space or dispatch, the value provided to the community by volunteers, and budget amounts for next year that are based on this year's budget plus an inflation factor. When you're satisfied the amounts are correct, you should print this page. STOP - IT IS TIME TO SAVE YOUR WORK. Click on File and then Save. Now it's time to move to the Rate Study tab. What this tab does: This tab allows you to see the effect of varying base and mileage changes, based on the percentage of collections of your service.

(Click on Image to see full-size image) This tab is a tool for you to estimate what your charges will need to be in order to recoup your cost of providing service. The number of emergency calls, non-emergency calls, and billed miles reported on the demographics tab are displayed in cells B10, B20 and B30. Note: in order to provide you with an example, we have used 500 emergency trips, 200 non-emergency trips and 9,000 billable miles. When you open this sheet, the numbers you entered on the demographics page will be displayed. In order to use this sheet, you will need to ask your billing clerk or billing company what your average percentage of collections are. If you bill $100,000 annually and collect $70,000, then your collection percentage is 70 percent. We'll use this as an example. In this example, if you bill a $250 base rate for your 500 emergencies, you would collect roughly the amount in cell C14 ($87,500). For 200 non-emergencies charged at a $250 base rate you would collect the amount in cell C24 ($35,000). For 9,000 billed miles at $9 per mile, you would collect the amount in cell C34 ($56,700). Your total collections for 500 emergencies, 200 non-emergencies and 9,000 billed miles would be $179,200. STOP - IT IS TIME TO SAVE YOUR WORK. Click on File and then Save. You can use this sheet to test various rates and collection percentages. We have provided space for you to add these three collections amounts on the Budget Model Worksheet. If you need to adjust the rates up or down for any or each of the categories, simply change the numbers in cells C10, C20 and C30. Each column D through M on row 10 increases the base rate by $50. If you want to see what a base rate of $100 would collect, change C10 to $100. Then D10 will automatically convert to $150, E10 to $200 and so on. STOP - IT IS TIME TO SAVE YOUR WORK. Click on File and then Save. Congratulations! You have finished your

own budget based on the Budget Model. We would appreciate hearing

from you about your experience using this tool, what you did with

it when you were finished, and ways we can enhance it in the future.

To provide comments, please e-mail info@remsttac.org

or telephone us at (866) 587-6370. Whether or not you export your data to QuickBooks® you have taken a very important step in planning for the financial future of your Agency. By exporting your data to QuickBooks® or another off-the-shelf accounting software system, you will be able to follow the financial performance of your ambulance service on a monthly basis. Tracking expenditures and revenues monthly better enables you to anticipate future needs and plan for addressing them. Maintaining a detailed budget will also provide you with persuasive data to share with others when you need to demonstrate the value and needs of your ambulance service. QUICKBOOKS EASY STEP INTERVIEW There is one tab in the Budget Model that you haven't used yet. This tab contains the and budget information you've just completed, which can be imported into QuickBooks®. This information is formatted for QuickBooks® Pro 2006. Whether it will import into other versions of QuickBooks® is unknown. We will provide you with a step by step example of importing this data that assumes you just purchased QuickBooks® and are starting from scratch. After installing QuickBooks®, start the program. Follow the prompts in the program. You will see the following screen. (Click on Image to see full-size image) Fill in the appropriate information and click Next.

Select "(No Type)" on the left side and click Next.

Choose either the default place to save your file or another location on your hard drive and click save.

(Click on Image to see full-size image) Click "Begin Using QuickBooks" in the lower right corner. If some Alerts pop up, click "Mark As Done" or "Remind Me Again" if you want to be reminded. Now go back to your Budget Model spreadsheet. You'll see this in the lower left corner of the sheet:

(Click on Image to see full-size image) Just above where it says "Ready" click the first arrow on the left side.

Then you will see the first few tabs in the spreadsheet.

Click on the QuickBooks tab, and you should see this:

(Click on Image to see full-size image) We need to save this tab in a format that QuickBooks can recognize. To do that, we're going to save a duplicate of your budget model under a different name and format.

(Click on Image to see full-size image) Now change the "Save as type" in the center on the bottom to TEXT. Also, rename the file to QuickBooks.iif.

Now click Save. You may now see two dialogue boxes, one informing you that only the current sheet can be saved and the other that some features of Excel may not be available in this format. Click YES to both dialogue boxes. Back to QuickBooks. Click on File, then Utilities, then Import, then IIF files.

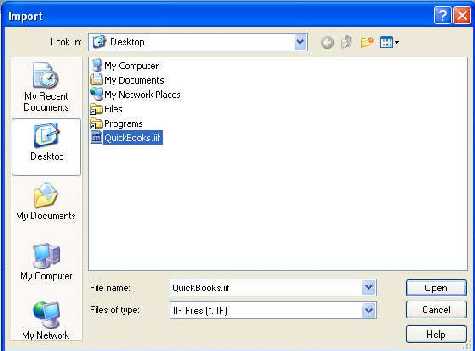

(Click on Image to see full-size image) Now click on Desktop on the left and select the QuickBooks.iif file you previously saved.

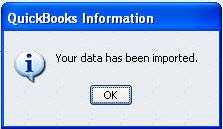

(Click on Image to see full-size image) Click Open. After the budget is imported you will see the following:

Congratulations! You are finished with this tutorial. Please refer to the extensive in-product and on-line support for QuickBooks. Thank you for using the budget model. We're interested

in your feedback on the use and utility of this product. If you

have comments or suggestions for improvement, please contact us

at: Health Resources and Services Administration,

Office of Rural Health Policy APPENDIX A: REMSTTAC STAKEHOLDERS GROUP Jane Ball, Executive Director Eli Briggs, Policy & State Affairs Manager Bethany Cummings Drew Dawson, Chief, EMS Division Tom Esposito, Medical Director Blanca Fuertes, Project Officer Grant Gray, Representative Christian L. Hanna, Rural Site Director Bob Heath, EMS Education Coordinator Marilyn Jarvis, Assistant Director for Continuing

Education Fergus Laughridge, Program Manager Tami Lichtenberg, Program Manager Patrick Malone, Director N. Clay Mann, Professor, Associate Director of

Research Evan Mayfield, CDC Public Health Advisor Charity Moore, Research Assistant Carol Miller, Executive Director Daniel Patterson, AHRQ-NRSA Post-Doctoral Research

Fellow Davis Patterson, Research Associate Kristine Sande, Project Director Dan Summers, Director of Education Chris Tilden, Interim Director Robert K. Waddell II, Secretary /Treasurer Bill White, President Gary Wingrove, Program Development Jill Zabel, Healthcare Consulting |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

![]()

Go to:

Top

| HRSA | HHS

| Disclaimer | Accessibility

| Privacy