|

|||||||||||||||

A RECORD OF ECONOMIC SUCCESS—BUT CHALLENGES AHEAD

|

|||||||||||||||

|

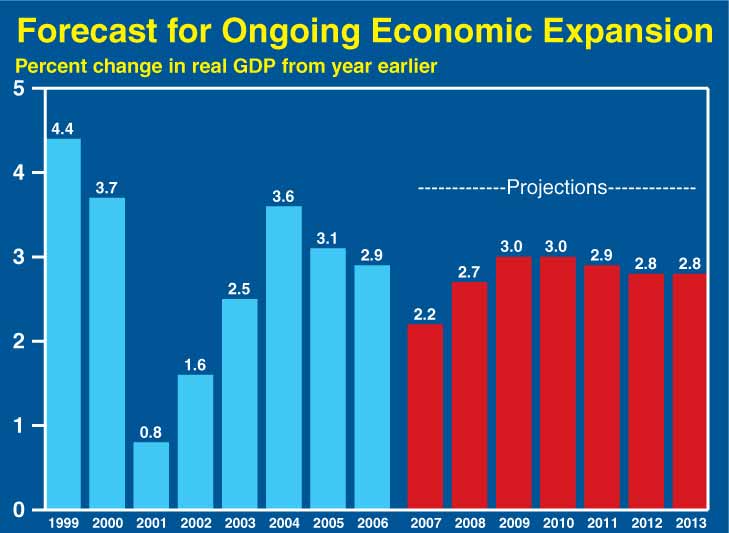

Looking back, the sustained economic expansion of the past six years generated strong growth of Federal receipts, which, together with the President’s ongoing efforts to restrain the growth of Federal spending, produced significant reductions in the Federal budget deficit in recent years. With the policies proposed in this Budget and a projection of continued economic growth following a near-term slowdown (see chart)—the Federal budget is on a path to balance.

Looking forward, sustained economic growth—and the ability of the economy to overcome future challenges—should not be taken for granted. Whether the challenges are the uncertainties about the short-run cyclical performance of the economy, or the projected long-run entitlement spending burden, it is of fundamental importance for pro-growth and strong security policies to be maintained. Such policies include preserving the underlying low-tax environment; maintaining domestic security and defense policies to provide for a safe environment for our country and its economy; restraining growth in Government spending; reducing burdensome regulatory policies; and furthering pro-growth trade, energy, and environmental policies. A positive environment for small businesses, research and development, entrepreneurial activity, efficient use of capital, and proper returns for prudent risk-taking promotes technology and productivity gains. Solid and sustained economic performance is a necessary foundation for a sound fiscal environment and for advancing Americans’ standards of living.

A RECORD OF SUCCESS

Over the past seven years, the economy has faced numerous challenges, including the collapse of the stock market bubble from the late 1990s and the related economic slowdown and recession of 2000–2001; the terrorist attacks of September 11, 2001, and continuing efforts of the terrorists; corporate scandals; Hurricane Katrina and the severe hurricane season of 2005; and recently, rising oil and energy prices, declines in the housing market, and financial and credit market disruptions. Facing these challenges, the President and his Administration have continuously worked to adopt and maintain pro-growth policies. In 2001 the President, working with the Congress on a bipartisan basis, enacted the largest tax cut since the Reagan Administration. The tax cut doubled the Child Tax credit, cut the marriage penalty, and lowered individual income tax rates. These tax changes, combined with an aggressive monetary response by the Federal Reserve, countered the recession then underway and subsequently helped the economy weather the effects of the September 11th terrorist attacks.

The 2001 tax cuts helped stabilize the economy, but it remained weak in the face of the declining stock market and corporate accounting scandals that rocked business and investor confidence. So the President pressed for additional tax relief in 2002 and again in 2003, including provisions to encourage business investment in new plant and equipment and an historic reduction in the capital gains and dividend tax rates. The President has continued to urge the Congress to extend and preserve the tax relief.

The pro-growth policies have been successful, as demonstrated by the sustained economic expansion, growth in productivity, ongoing jobs gains, and low unemployment:

|

-

Through the third quarter of 2007, the U.S. economy experienced six years of uninterrupted growth, during which real gross domestic product (GDP) grew at an average annual rate of 2.8 percent; growth over the past four quarters was 2.8 percent, as well.

-

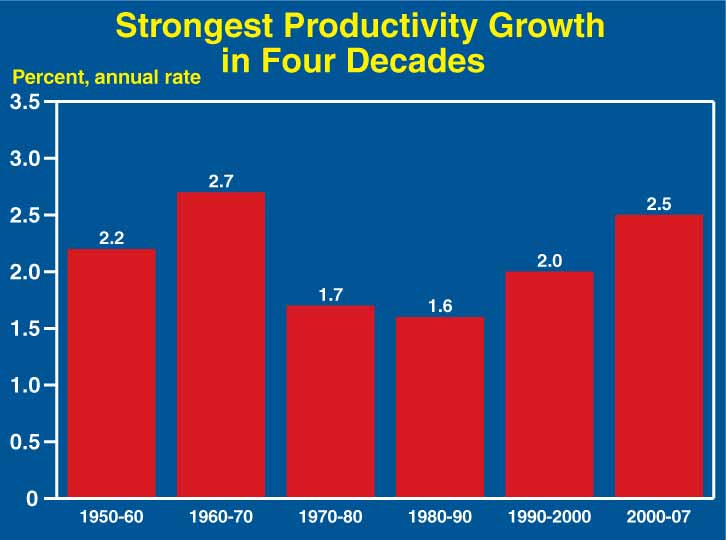

So far this decade, labor productivity growth—the increase in output per labor hour—has averaged 2.5 percent, well above the average growth rates during the decades of the 1970s, 1980s, and 1990s. Labor productivity growth ultimately is the basis for improving the standard of living of the Nation’s workers and households.

-

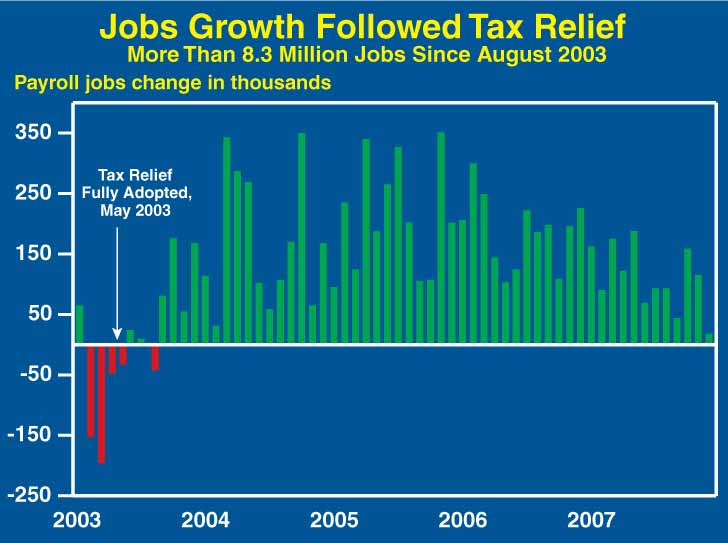

Since August 2003, nonfarm payroll employment registered a total gain of more than 8.3 million jobs (including the effects of the preliminary estimates of the annual benchmark revision), with 1.3 million added during 2007. This is the longest sustained period of jobs gains on record, with total employment growth being better than all other major industrialized nations combined.

|

-

The unemployment rate ended 2007 at 5.0 percent in December, well below the average rates in each of the past three decades. The unemployment rate has risen slightly over the past year, but the Administration forecast assumes it will flatten out at around 4.8 percent in coming years—at a still-low level by historical standards.

Americans’ wages, incomes and wealth also rose during the expansion:

-

Real after-tax per capita personal income has increased by more than $3,500 in today’s prices—an increase of more than 11 percent—since January 2001.

-

During 2007, despite heightened volatility, values of corporate equities still registered gains, with the Dow up 6.4 percent and the S&P 500—a key measure for many retirement stock funds—up 3.5 percent for the year. At year-end, the Dow was up more than 70 percent since late 2002; the NASDAQ was up more than 100 percent over the same time period.

|

-

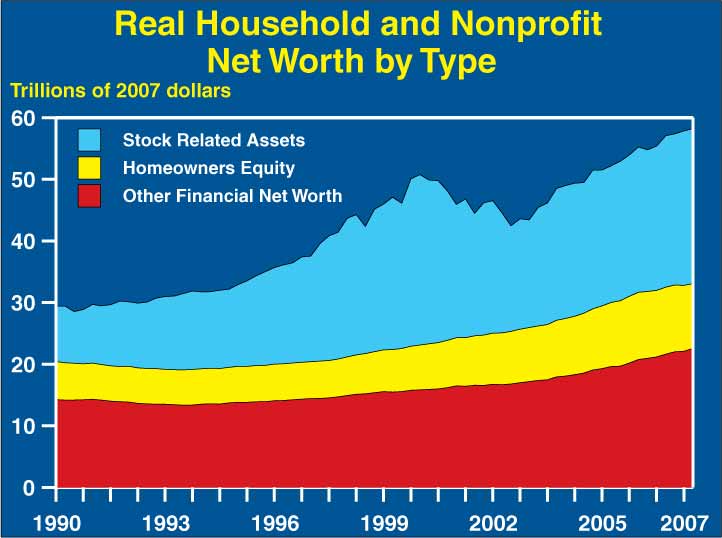

Household wealth increased 7.3 percent over the past year, and stood at $58.6 trillion at the end of the third quarter. Nearly 30 percent of the Nation’s net worth has been added since the 2003 tax cuts. Even with the moderation in the value of real estate assets, the value of real net worth continued to rise through the third quarter of 2007 reflecting gains in other assets.

The Nation also has experienced solid gains from international trade; real exports increased by 10.3 percent over the past four quarters while real imports rose 1.7 percent, resulting in a $101 billion reduction in the annualized real trade deficit over that period.

SHORT-RUN CHALLENGES

Although the economy has experienced solid growth over the past six years, risks remain as the economy currently faces significant headwinds. Economic expansions do not end simply because they have continued for a long period of time. Significant slowdowns or declines in economic activity occur because of external shocks, large imbalances that must be corrected, or reactions to policy changes. For example, the economic slowdown and recession of 2000–2001 occurred in large part because of the correction to the excessive valuation of the stock market of the late 1990s and the related excess investment in technology assets at the time. Although the current expectation is for ongoing growth, the economy is working off the housing sector imbalance and is burdened by higher oil and energy prices. At the same time, and on a positive note, the improvement in real net exports made a positive contribution to real GDP growth of 0.9 percentage point on average for the four quarters ending in the third quarter of 2007—roughly offsetting the –0.9 percentage point effect on real GDP growth from the decline in real residential investment. Recognizing the mixed economic signals and the risks to short-term economic growth, the President called for the quick adoption of an effective growth package of broad-based tax relief to boost consumption and investment and to help keep instability and uncertainty from causing additional harm to the overall economy.

Helping Americans Weather the Housing Downturn

The Administration has aggressively pursued policies to help deal with current challenges. Facing declines in housing markets of the past two years, the Administration has made proposals for modernization of the Federal Housing Administration (FHA) and for expanded refinancing opportunities through new uses and increased allowances for tax-exempt State and local bonds; implemented efforts to promote additional refinancing opportunities through FHASecure; expanded cooperation with private-sector groups through the HOPE NOW alliance; and worked to help borrowers and lenders reach voluntary agreements for alleviating interest rate resets. The Administration also worked with the Congress to adopt temporary tax relief for homeowners who face additional tax liability from mortgage debt cancelled by their lenders. These policies are intended to help provide transition relief—without any direct costly “bailout” from the Federal Government for individuals or institutions that had taken on excessive speculative risk and without interfering with the effective functioning of the free market. As such, the policies provide targeted assistance while avoiding longer-run costs from a perception of the Government bearing the cost of risky speculation or reckless financial decisions (what economists call “moral hazard”). Even with such efforts, the correction to the housing imbalance and the related financial market difficulties are having adverse effects on the performance of the economy in the short run.

Addressing America’s Oil Dependence

Though inflation is relatively low by historical standards, it remains a challenge, especially in the face of higher food and energy prices. Although high energy prices likely will continue to be a challenge in the short run, the Administration’s energy strategy is directed at promoting energy security by improving efficiencies, increasing domestic oil production, pursuing alternatives to oil, taking advantage of new technologies, and increasing the Strategic Petroleum Reserve. The President set a Twenty in Ten goal of cutting U.S. consumption of gasoline by 20 percent over the next 10 years, and the Congress responded by passing legislation that takes a significant step toward this goal.

THE LONG-RUN CHALLENGE

The President’s tax relief policies will continue to promote growth in the years ahead by reducing the inherent biases in our Federal tax system against work, saving, investment, economic risk-taking, and entrepreneurship. Along with the tax cuts, other policies of this Administration will continue to strengthen our economy over the longer-run outlook. For example, the Administration has:

-

Worked to provide sufficient resources for defense and homeland security, a necessity for establishing a safe environment for promoting economic security and growth in standards of living.

-

Limited the regulatory burden Americans face while preserving protections for workers and consumers.

-

Promoted American exports by actively working to open new markets with free trade agreement (FTA) negotiations in Latin America, Asia, the Middle East, and Africa. In the last six years the Administration has secured congressional approval of new free trade agreements with 13 countries and concluded FTA negotiations with three additional countries.

-

Put in place policies to restrain excessive health care inflation through market-based reforms in Medicare and through the market discipline resulting from the enactment and growing popularity of Health Savings Accounts.

-

Advanced the American Competitiveness Initiative, to build on our successes and remain a leader in science and technology through increasing investment in research and development, strengthening education, and encouraging entrepreneurship.

Efforts must continue to sustain, improve, and build on these policies, and to address long-term national issues such as access to affordable health care and reform of our important, yet currently unsustainable, entitlement programs. The long-run entitlement outlook, in particular, is very problematic. On this, the President also has taken the lead, advocating Social Security reform, and proposing savings in mandatory programs, including changes to Medicare that would resolve nearly one-third of the long-run unfunded obligation. Congress has not yet risen to the challenge.

The Administration also has advocated fundamental tax reform to make the tax code even more efficient and pro-growth. The U.S. Treasury recently put forward a review of potential approaches for reform of the U.S. business tax system to help promote a more competitive economic environment for U.S. businesses. Policies that foster the country’s entrepreneurial spirit and reward the ingenuity that plays such a critical role in developing new technologies and generating productivity gains provide the ultimate improvements in standards of living.

Some argue that taxes are not high enough and should be increased to deal with the budget challenges we face, both in the short run and the long run. A higher and growing tax burden and excessive spending increases are the wrong formula for economic growth. Americans are not under-taxed. The overall tax burden for the economy is at a high level by historical standards. The total tax burden, including Federal, State and local government as a whole, shows that more than one-third of all the income in the economy (“national income”) is being paid to government. Further, without reform or active management to reduce taxes on an ongoing basis, biases in the tax code tend to push that burden ever higher over time.

|

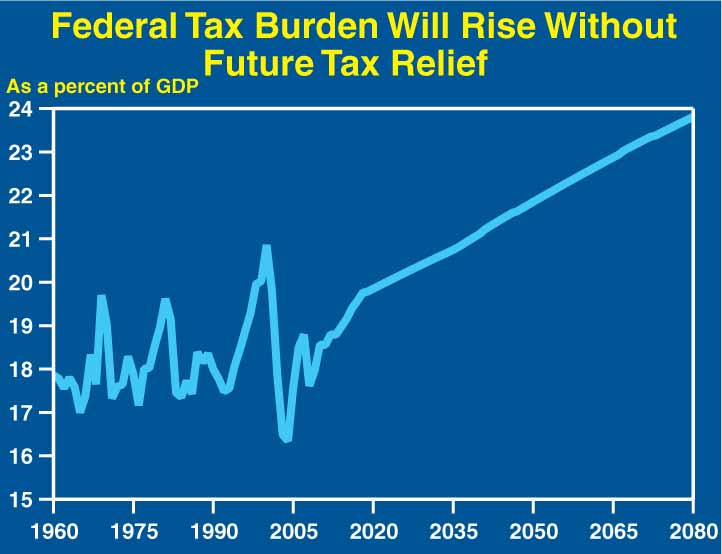

At the Federal level, taxes were at 18.8 percent of GDP in 2007—above the 40-year historical average of 18.3 percent. Even with the extension of the President’s tax relief, the tax burden is projected to rise over time, in part because of “real bracket creep”—the tendency for real growth in wages and salaries to push taxpayers into higher tax brackets (tax brackets are only indexed for inflation and not real wage gains); the accompanying chart shows the projected Federal tax burden rising steadily over time, to more than 20 percent of GDP by 2030 and nearly 24 percent of GDP by 2080. That burden would be even higher if the President’s tax relief were not extended. The ongoing tendency for the tax burden to rise over time further reveals the importance of not only extending the President’s tax relief but also providing for future tax policies that limit the increase in the tax burden.

Economists long have recognized that higher taxes—and higher income tax rates, in particular—impose costs on the economy from the forgone value of production and income that is lost and the distortion of incentives. For the long-term U.S. economic outlook, the large tax increases required to deal with projected entitlement spending would threaten economic growth and, ultimately, the ability of the economy to generate growth in standards of living and in revenues. Such concerns underscore the importance of curbing increases in long-term entitlement spending, rather than attempting to rely on tax increases to resolve the challenge.

THE ECONOMY AND THE BUDGET: REDUCING THE DEFICIT

In February 2004, the President’s Budget forecasted a deficit for 2004 of 4.5 percent of GDP, or $521 billion. Even coming out of a recession and in time of war, that was a significant fiscal shortfall, and the President rightly determined it needed to be addressed. He set a goal of cutting the deficit in half by 2009, which was achieved three years ahead of schedule. Upon completing this goal, the President set a new goal for the Nation in January 2007: balancing the budget. The policies contained in this Budget represent the next steps toward meeting that goal.

Significant deficit reduction is not easy. On the receipts side, governments face the choice of pursuing pro-growth policies to generate higher tax receipts, or raising taxes and thereby sacrificing some of their economic growth. This Administration chose to pursue pro-growth policies, which have worked. Along with steady growth in output and incomes, there has been remarkable growth in Federal tax receipts. In 2005, tax receipts rose 14.5 percent, the largest one-year growth in receipts since 1982. Tax receipts rose another 11.8 percent in 2006, and 6.7 percent in 2007.

Restraining spending growth is the other side of successful deficit reduction. Since the September 11th terrorist attacks, the President’s Budgets have provided the necessary funding for prosecuting the Global War on Terror and for homeland security needs, while calling for increasing restraint in non-security discretionary spending and significant reductions in mandatory spending. The 2009 Budget continues this emphasis on fiscal discipline. Non-security discretionary spending growth is at less than 1 percent, total discretionary spending grows less than the growth of nominal GDP, and the Budget proposes more than $200 billion in mandatory savings over five years.

Strong receipts growth and spending restraint produced substantial improvement in the deficit, with the deficit declining by $250 billion over the past three years. At just 1.2 percent of GDP, this deficit was well below the 40-year average of 2.4 percent of GDP. In addition, the Federal debt held by the public ended 2007 at 36.8 percent of GDP, lower than the average for the 1990s and only marginally higher than the 35.6 percent 40-year average. As a percentage of output, U.S. net Government debt compares favorably to other major countries: it is below the G-7 average, and lower than for Germany, Italy, and Japan.

The progress in reducing the deficit and toward achieving a balanced budget would not be possible without the Administration’s pro-growth economic policies. By reducing the deficit through spending restraint and growth-generated revenue increases, the Administration has shown the great strides that can be made toward fiscal discipline without raising taxes. Nonetheless, challenges will continue in coming years to maintain the budget on a path to balance as pressures for higher deficits will persist.

Looking forward, we cannot take economic growth for granted. It is of fundamental importance to continue to adopt and maintain sound pro-growth policies that reward work and prudent risk-taking. The pro-growth tax cuts enacted in 2001 and 2003, currently scheduled to expire at the end of 2010, should be made permanent as proposed in this Budget to ensure continued economic growth. The tax cuts helped boost our economy out of recession and will continue to provide beneficial incentives, and future economic growth will help to generate the resources needed to address the very real problems the country will face from the unsustainable growth in Medicare, Medicaid, and Social Security spending. The right policy setting—a low-tax environment, spending restraint, defense and domestic security, efficient regulation, and market-oriented trade, energy and environmental policies—is the best foundation for ensuring an expanding economy, a sustainable fiscal outlook, and ongoing gains in Americans’ standards of living.

| Federal Register | Jobs at OMB | FOIA | OMB Locator | USA.gov | Accessibility | Privacy Policy | Site Search | Help |