Released on February 27, 2008

(Next Release on March 5, 2008)

Coming Attractions

Now that the Academy Awards for 2007 have been handed out, movie fans are turning their attention to coming attractions for 2008. One film that may stir some excitement is the next installment of the Indiana Jones series, opening in time for Memorial Day weekend. Coincidentally, for the past several years, consumers have seen the first price peak for gasoline occur in time for Memorial Day weekend, as well. Should consumers expect this year to be any different?

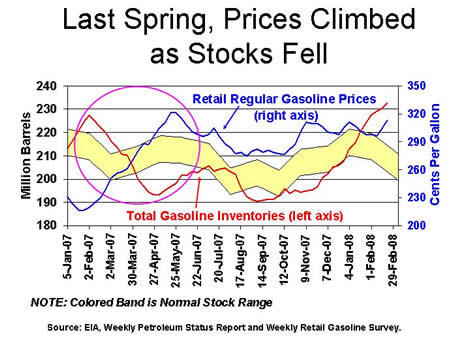

First, let’s turn back to spring 2007 to review the events leading up to the summer driving season. Data for the week ending February 23, 2007 showed gasoline inventories at 220.2 million barrels, 2.0% above the 5-year average. Gasoline demand was relatively strong, with the 4-week average level 1.3% higher than the same period in 2006 (based on weekly-to-weekly data), albeit relative to a 2006 comparable period that may have still reflected the aftermath of the devastating hurricanes in 2005. At this time last year, gasoline prices were about 75 cents lower than they are now. However, during 12 consecutive weeks from February to April, total gasoline inventories were drawn down by more than 34 million barrels, the largest such decline over a 12-week period in EIA’s data history. These stockdraws began with the seasonal sell-off of winter grade gasoline, which at the end of the winter may be sold at a discount to move it out of primary storage to make room for summer grade gasoline. However, stocks then continued to fall as a large amount of refinery capacity went off-line for both planned maintenance and unexpected outages. This longer- and deeper-than-normal refinery turnaround season, as well as low import levels, pushed gasoline inventories from well above the average range to well below it. These tight supplies pushed the national average price for regular gasoline to a nominal high of 321.8 cents per gallon on May 21, 2007.

The situation this year differs from that of 2007 in several key respects. While seasonal stockdraws are expected in the next few weeks, gasoline inventories currently stand at 232.6 million barrels, or about 12 million barrels higher than this time last year and almost 8% above the 5-year average. And as was discussed in last week’s This Week in Petroleum, it is expected that refinery outages this spring will not be as numerous or long-lasting as last year, while imports of gasoline remain around year-ago levels. Additionally, gasoline demand growth has softened in response to a struggling economy and gasoline prices averaging above $3 per gallon all fall and winter. In fact, the current 4-week average for gasoline demand is 1.1% lower than this time last year.

While gasoline stocks and likely refinery availability appear to have improved relative to the year-ago situation, there is still, unfortunately, another key element to consider: crude oil prices. Crude oil prices are currently around $100 per barrel compared to prices around $60 per barrel for the same period last year. The $40 per barrel crude oil price difference is equivalent to 95 cents per gallon, which significantly exceeds the 75 cent gasoline price difference from the same period last year. This suggests that gasoline prices could rise still more if crude oil prices do not fall from current levels. Although EIA does expect that crude oil prices may gradually decrease over the course of 2008 while the global oil supply-demand balance loosens, significant uncertainty surrounds this forecast. However, taking both gasoline market conditions and crude oil prices into account, it is still likely that we will see gasoline prices peaking at a higher level this spring and summer than we did in 2007. Such an outcome would not be a very happy ending for American consumers, and consumers may decide to enjoy more of their movies from home.

Residential Heating Fuel Prices See Further Increases

Residential heating oil prices increased solidly during the period ending February 25, 2008, the 21st week of the survey this season. For the second week in a row, the average residential heating oil price set a nominal high record with an increase of 6.6 cents last week to reach 346.1 cents per gallon, which was an increase of 100.8 cents from the 21st reporting period last year ending February 19, 2007. Wholesale heating oil prices gained 12.1 cents to reach 286.3 cents per gallon, which was an increase of 107.5 cents compared to last year.

The average residential propane price rose by 3.0 cents, attaining the mark of 258.0 cents per gallon, which was a new nominal all-time high price record. This was an increase of 55.5 cents compared to the 202.5 cents per gallon average for the same period last year. Wholesale propane prices skyrocketed up 29.9 cents, from 147.5 to 177.4 cents per gallon. This was an increase of 72.0 cents from the February 19, 2007 price of 105.4 cents per gallon.

Highway Diesel at Highest Price in History

Gasoline prices continued their upward climb, increasing in all regions of the U.S. The national average retail price for regular gasoline jumped 8.8 cents to 313.0 cents per gallon as of February 25, 2008. This was an increase of 74.7 cents above the price a year ago. Prices on the East Coast rose by 10.2 cents to 314.8 cents per gallon, 81.1 cents per gallon above last year. In the Lower Atlantic, the average price rose by 11.5 cents to an all-time high of 315.3 cents per gallon, surpassing the previous record set September 5, 2005. The Midwest had the smallest increase of any region, moving up by 3.4 cents to 308.0 cents per gallon. This was 71.0 cents per gallon more than last year. The Gulf Coast price rose by 11.5 cents to 305.6 cents per gallon, 82.2 cents per gallon higher than the price a year ago. Although the price in the Rocky Mountains increased by 9.2 cents, at 305.1 cents per gallon, it was the lowest of any region. Once again, prices on the West Coast remained the highest on a regional basis. The price shot up by 12.8 cents to 326.5 cents per gallon, 60.1 cents above the price last year. In California, the average price for regular grade surged by 13.7 cents to 332.8 cents per gallon, 53.2 cents above the price a year ago.

Soaring to 355.2 cents per gallon, the U.S. average retail diesel price rose sharply to the highest point ever, topping the previous record by almost 11 cents. This was a jump of 15.6 cents from the previous week and 100.1 cents above the price a year ago. On a regional basis, aside from the Rocky Mountains, prices also reached all-time record levels. Prices on the East Coast rose the most of any of the five regions, surging up by 16.4 cents to 360.8 cents per gallon. This raised the price by 108.2 cents per gallon above the price last year. In the Midwest, the price was up by 16.0 cents to 352.5 cents per gallon, an increase of 100.2 cents from a year ago. The price in the Gulf Coast area increased by 14.3 cents to 351.0 cents per gallon which was 101.3 cents above the level a year ago. Once again, the price in the Rocky Mountains was the lowest of any region last week, moving up by 12.3 cents, to 347.3 cents per gallon, 90.5 cents above the price a year ago. On the West Coast, the average price increased by 15.5 cents to 360.9 cents per gallon, 81.9 cents above the price a year ago. In California, the average price shot up by 16.1 cents to 367.2 cents per gallon, 76.1 cents higher than last year.

Cold Weather Lowers Propane Inventories

A fresh round of cold temperatures lowered propane inventories last week by 2.4 million barrels, leaving the Nation’s primary supply of propane at an estimated 31.6 million barrels as of February 22, 2008. With last week’s decline, total propane inventories continued to track well within the normal range for this time of year. All regions reported declines last week, leading with 1.1 million barrels in the Gulf Coast region with the Midwest following in second with 1.0 million barrels. East Coast inventories were partially offset by strong imports last week but still fell by 0.2 million barrels, while the combined Rocky Mountain/West Coast region moved only slightly lower by 0.1 million barrels during this same time. Propylene non-fuel inventories were unchanged at 2.4 million barrels but accounted for a higher 7.5 percent share of total propane/propylene inventories from the prior week’s 7.0 percent share.

Text from the previous editions of “This Week In Petroleum” is now accessible through a link at the top right-hand corner of this page.

| Retail Prices (Cents Per Gallon) | |||||||

|

|

||||||

|

|

||||||

| Retail Data | Changes From | Retail Data | Changes From | ||||

| 02/25/08 | Week | Year | 02/25/08 | Week | Year | ||

| Gasoline | 313.0 | Heating Oil | 346.1 | ||||

| Diesel Fuel | 355.2 | Propane | 258.0 | ||||

| Spot Prices (Cents Per Gallon) | |||||||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||||||

| Stocks (Million Barrels) | |||||||

|

|

||||||

|

|

||||||

| Stocks Data | Changes From | Stocks Data | Changes From | ||||

| 02/22/08 | Week | Year | 02/22/08 | Week | Year | ||

| Crude Oil | 308.5 | Distillate | 120.0 | ||||

| Gasoline | 232.6 | Propane | 31.583 | ||||