|

|

|

|

www.dol.gov

|

| November 4, 2008 DOL Home > About DOL > 2006 PAR > Management's Discussion & Analysis |

|

DOL Annual Report, Fiscal Year

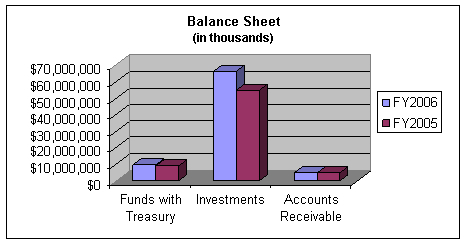

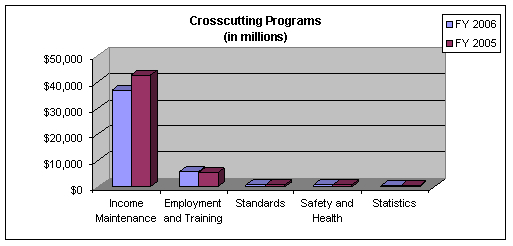

2006 Management's Discussion & Analysis Financial Section Improving Financial Performance Through Transparency  Over the past fiscal year, the Department has also worked on enhancing its managerial cost accounting system, Cost Analysis Manager (CAM). The Department's success in implementing a Department-wide managerial cost accounting system was highlighted in the Government Accountability Office's (GAO) Survey of Managerial Cost Accounting Practices at Large Federal Agencies. In addition, the Department was praised for its efforts in making managerial cost accounting information readily available at a hearing before the U.S. House of Representatives on September 21, 2005. CAM is an indispensable tool for improving program performance. It improves accountability and transparency for how well tax dollars are spent. In FY 2005, the Department reported in its Performance and Accountability Report the cost of its Department-wide performance goals. This year, it is providing cost information on more than half of its Department-wide performance indicators. When fully implemented, the new system will be a strategic asset for the Department allowing, managers to create customized reports online at their desktops to meet their management needs in real time. LEAP is currently being hosted by a Shared Service Provider (SSP). This SSP was selected in Q2 FY 2006, and the SSP hosting of LEAP started in Q4 FY 2006. For Q1 FY 2007, LEAP is scheduled to complete the configuration of the Oracle Federal Administrator (Budget Execution) module for internal reporting and evaluation purposes. The Department is the first Federal agency to deploy an-end-to end web based electronic travel management system, which was completed on September 30, 2006. Now, DOL employees have the advantage of being able to assess their travel system 24-hours a day/7 days a week to enter travel authorizations, book travel reservations, and complete their travel vouchers. The system is accessible from the office, home, or while on the road. E-Gov Travel is totally paperless and affords DOL employees the ease of taking advantage of the latest technology while providing cost savings. The Debt Collection Improvement Act of 1996 (DCIA) designated the Department of the Treasury as the central agency for collection of Federal debts over 180 days delinquent. The Department cross-services all delinquent debts in accordance with this statute. Debt management accounts for a relatively small part of our financial management activity. The majority of debts managed by the Department relate to the assessment of fines and penalties in our enforcement programs. During FY 2006, the Department referred $84.2 million, which represents 79 percent of all eligible delinquent debt, to Treasury for collection. The Department continues to monitor and aggressively pursue its debt greater than 180 days old. The Department continues to make improvements in its efforts to meet guidance and regulations outlined in the Prompt Payment Act. The Prompt Payment Act requires Executive agencies to pay commercial obligations within discreet time periods and to pay interest penalties when those time constraints are not met. In FY 2006, of approximately $1.2 billion in gross payments, $452,000 was paid in interest fees and penalties. Additionally, during FY 2005, there were over 73,000 payments made to vendors and travelers. Of this amount, 2,476 invoices were paid late, resulting in only 3% of the total payments incurring interest penalties. These results represent significant improvements from the prior year. The Department continues to work aggressively with its agencies to increase the number of vendors receiving payments through electronic fund transfer (EFT). The percentage of vendors receiving EFT payments increased by 7% to 95%. ESA benefit and medical programs, although increasing in EFT payments, continue to remain low. Analysis of Financial Statements The principal financial statements summarize the Department's financial position, net cost of operations, and changes in net position, provide information on budgetary resources and financing, and present the sources and disposition of custodial revenues for FY 2006 and FY 2005. Highlights of the financial information presented in the principal financial statements are shown below. Financial Position Net Cost of Operations Income Maintenance programs continue to comprise the major portion of costs. These programs include costs such as unemployment benefits paid to individuals who are laid off or out of work and seeking employment as well as payments to individuals who qualify for disability benefits due to injury or illness suffered on the job. Employment and Training programs comprise the second largest cost. These programs are designed to help individuals deal with the loss of a job, research new opportunities, find training to acquire different skills, start a new job, or make long-term career plans. Statement of Budgetary Resources Limitations on the Principal Financial Statements Management Assurances The Department committed significant resources in implementing the requirements outlined in the revised OMB Circular A-123, Management's Responsibility for Internal Controls. The Department's implementation leveraged and improved upon existing successes in financial management, including the Quarterly Financial Management Certification program, which requires managers at all levels to attest to the adequacy of effective management controls over program resources, financial systems, and financial reporting. The Department's approach to the A-123 requirement is compliance at managed cost, sustainability by reducing compliance mindset and reliance on outside parties to discover errors and problems, and improvement in effectiveness and efficiency of agency programs. SECRETARY OF LABOR

Statement of Qualified Assurance Federal Managers' Financial Integrity Act DOL conducted its assessment of the effectiveness of internal control over the effectiveness and efficiency of operations and compliance with applicable laws and regulations in accordance with OMB Circular A-123, Management's Responsibility for Internal Control. Based on the results of this evaluation, DOL identified 7 significant deficiencies in 2 non-financial systems which are required to be reported as material weaknesses in its internal control over the effectiveness and efficiency of operations and compliance with applicable laws and regulations as of September 30, 2006. Other than the exceptions noted below, the internal controls were operating effectively and no other material weaknesses were found in the design or operation of the internal controls. DOL is also in conformance with Section 4 of FMFIA. In addition, the DOL conducted its assessment of the effectiveness of internal control over financial reporting, which includes safeguarding of assets and compliance with applicable laws and regulations, in accordance with the requirements of Appendix A of OMB Circular A-123. Based on the results of this evaluation, DOL can provide reasonable assurance that its internal control over financial reporting as of June 30, 2006 was operating effectively and no material weaknesses were found in the design or operation of the internal control over financial reporting. Federal Financial Management Improvement Act of 1996

Disclosure of Federal Information Security Management Act (FISMA) Significant Deficiencies The Federal Information Security Management Act (FISMA) requires the Department of Labor (DOL), Office of Inspector General (OIG), to perform annual independent evaluations of the DOL information security program and practices based upon audits of a subset of DOL's identified major information systems. The objective of the audits is to determine if security controls over the systems were in compliance with FISMA requirements. Based on the audits performed during FY 2006, the OIG identified 7 significant deficiencies in 2 non-financial systems in the following security control areas:

To address the significant deficiencies in the security of the data, the OIG recommended that DOL document and implement procedures and processes to ensure that:

In its response to the audit reports, DOL generally concurred with the findings and recommendations and has already taken corrective actions to address several of the recommendations associated with these deficiencies and is in the process of taking corrective actions to address the remaining recommendations. IPIA Compliance Improved financial performance through the reduction of improper payments continues to be a key financial management focus of the Federal government. At Labor, developing strategies and the means to reduce improper payments is a matter of good stewardship. Accurate payments lower program costs. This is particularly important as budgets have become increasingly tight. Over the past several years, identifying and reducing improper payments has been a major financial management focus of the Federal Government. A PMA key component is to improve agency financial performance through reductions in improper payments. OMB originally provided Section 57 of Circular A-11 as guidance for Federal agencies to identify and reduce improper payments for selected programs.12 The Improper Payments Information Act of 2002 (IPIA) broadened the original erroneous payment reporting requirements to programs and activities beyond those originally listed in Circular A-11. IPIA defines improper payments as those payments made to the wrong recipient, in the wrong amount, or used in an improper manner by the recipient. IPIA requires a Federal agency to identify all of its programs that are risk susceptible to improper payments. It also requires the agency to implement a corrective action plan that includes improper payment reduction and recovery targets. The act also requires the agency to report annually on the extent of its improper payments and the actions taken to increase the accuracy of payments. To coordinate and facilitate the Department's efforts under IPIA, the Chief Financial Officer (CFO) is the Erroneous Payment Reduction Coordinator for the Department. OCFO works with program offices to develop a coordinated strategy to perform annual reviews for all programs and activities susceptible to improper payments. This cooperative effort includes developing actions to reduce improper payments, identifying and conducting ongoing monitoring techniques, and establishing appropriate corrective action initiatives. Methodology FY 2006 benefit programs with FY 2005 outlays totaling less than $200 million were deemed to be low risk, unless a known weakness existed in the program management based on reports issued by oversight agencies such as the Department's Inspector General (IG) and/or the U.S. Government Accountability Office (GAO). Hence, these benefit programs were not statistically sampled. For benefit programs with outlays greater than $200 million, the Department conducted sampling to determine their improper payment rates. This sampling included FECA, UI, Black Lung Disability Trust Fund, and Energy Employees Occupational Illness Compensation Fund. UI was the only program determined to be susceptible to risk13 as a result of this approach. However, the Department is also reporting on FECA's improper payment rate since it is required per OMB guidance. As mentioned earlier, the Department used a separate methodology to assess the risk of improper payments in grant programs except for Job Corps which was sampled. The Department analyzed all FY 2004 Single Audit Reports14 to identify questioned costs, which were used as a proxy for improper payments, and to estimate an approximate risk for each of the Department's grant programs. The improper payment rate was determined by calculating the projected questioned costs and dividing this total projection by the corresponding outlays.15 All error rates were determined to be well below the 2.5 percent threshold; therefore, no grant programs were determined to be susceptible to risk as a result of this approach. However, like FECA, the Department is reporting on WIA's improper payment rate since it is required per OMB guidance, even though its improper payment rate is well below the 2.5 percent threshold. Challenges for IPIA Compliance Two factors appear to account for most of the increase in the overpayment rate from 9.3% a year earlier as the table below shows:

The Department has obtained authority to require states to use the NDNH to improve their BAM estimates of overpayments due to workers who return to work but continue claiming benefits. When this NDNH crossmatch requirement becomes mandatory in January 2008, we estimate that it will raise the measured BAM annual report and operational rates by 0.5 to 0.75 percentage points. Without the effects of these two elements, we estimate that the Annual Report rate would have been about 9.5% instead of 10.0%, and the operational rate 5.3% instead of 5.6%. Because both estimates are sample-based, they are subject to the usual sampling variation. The 95% confidence intervals are 10.0% +/- 0.54 percentage points for the Annual Report rate and 5.63% +/- 0.44 percentage points for the operational rate. Furthermore, meeting improper payment reduction and recovery targets of programs such as UI and WIA are contingent upon the cooperation and support of State agencies and other outside stakeholders who are intricately involved in the day-to-day management of these programs' activities. Accomplishments and Plans for the Future The Department's analytical studies indicate that earlier detection of recoverable overpayments is the most cost-effective way to address improper payments. Early detection allows agencies to stop payments before a claimant who has returned to work can exhaust benefits and to recover these overpayments more readily. The Department estimates that the forty-five states that crossmatch UI beneficiaries with the SNDH or the NDNH instead of UI wage records prevented approximately $75 million of overpayments in each of the past two fiscal years. Last year, three states participated in a pilot study initiated by the Office of the Chief Financial Officer and the UI program to determine whether a cross-match using the NDNH is more effective than the SDNH in identifying individuals no longer eligible to receive UI benefits. The results of this pilot showed that because the NDNH includes records for out-of-state employers, Federal agencies, and multi-state employers that report all of their new hires to a single state, it detects improper payments more effectively than the SDNH. The Department has provided states with funds to implement these NDNH cross-matches; as of 10/30/06, twenty-two states have implemented the NDNH crossmatch, twelve states have signed the computer-matching agreement with HHS that is the prelude to connecting with the NDNH, and seventeen are in the planning process. Seven States were awarded special FY 2006 supplemental funds to implement NDNH. In FY 2005, the Department began providing States funds to conduct Reemployment and Eligibility Assessment (REAs) with UI beneficiaries. These assessments reduce improper payments both by speeding claimants' return to work and by detecting and preventing eligibility violations. Twenty states received funds to continue REAs during FY 2006; these REAs are estimated to return about $66 million to the UI trust fund. An impact evaluation of nine states' REA programs is scheduled for March 2007.

12Section 57 identified Unemployment Insurance (UI), Federal Employees' Compensation Act (FECA), and Workforce Investment Act (WIA) as programs required to report annual erroneous payments.

|

|

||||||||||||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||||||||||||