|

|

Office of Labor-Management Standards (OLMS)

|

||||||

Conducting Audits in Small Unions — A Guide for Trustees

Table of Contents

A Message to Trustees

Chapters

Figures

References

A Message To Trustees

This Guide features a 10-step audit designed to help Trustees from small unions carry out their duties. For purposes of this Guide, a small union is considered to be one with annual receipts of less than $50,000. Trustees from larger unions with more complex recordkeeping systems may also find this Guide helpful.

The Office of Labor-Management Standards (OLMS) of the U.S. Department of Labor’s Employment Standards Administration has prepared this Guide to further the aims of the Labor-Management Reporting and Disclosure Act of 1959, as amended (LMRDA). More commonly known as the Landrum-Griffin Act, the LMRDA has several provisions designed to promote the financial integrity of unions, including those pertaining to financial reporting, recordkeeping, bonding, and loans. The LMRDA applies to unions which represent private sector employees and U.S. Postal Service employees. The Civil Service Reform Act of 1978 (CSRA) has similar provisions which apply to most unions which represent federal government employees.

Your Role

As an elected or appointed Trustee you will play a key role in making sure that your union’s funds and other assets are properly accounted for and used solely for the benefit of your union and its members. Few tasks could be more critical to the well-being of any organization.

Your specific duties and responsibilities may be outlined in your union's constitution and bylaws or otherwise defined by your parent body. However, your primary task as a Trustee is to ensure that all union resources (money/assets) are used for legitimate union purposes as authorized by your membership in accordance with your constitution and bylaws. In addition, you should ensure that your union is properly submitting per capita taxes to its parent body and is complying with legal requirements for financial reporting, recordkeeping, bonding, and loans.

What’s in this Guide

This Guide is designed to be an easy-to-use reference based on the law and regulations as well as the knowledge and experience of OLMS staff. It will take you step by step through the audit process, help you identify your responsibilities during each step, and provide suggestions to make your job easier. Most of the seven chapters in the Guide refer to Figures (such as an audit planner, a financial records request, a questionnaire, worksheets, and an audit report) relating to the topics discussed. A fictitious union (Factory Workers Local 888) is used in several of the Figures to illustrate recommended procedures. A general overview of the way many unions maintain their financial records, a list of common financial terms and their meanings, and a four-page Checklist for Conducting Audits in Small Unions which summarizes the contents of this Guide are included as References at the end of this publication.

We realize that unions operate differently, using different constitutions and bylaws and audit procedures, and that Trustees and audit officials have varying degrees of responsibility. For example, some unions want a greater day-to-day financial role for Trustees (requiring that they sign all vouchers or co-sign checks) while others want only periodic reviews of financial records. Likewise, some unions have both Trustees and Audit Committees. Therefore, not all information in this Guide will apply to all unions. You should disregard the parts of the Guide that do not apply to you and consider the other parts as a supplement to the practices and procedures specified by your parent body.

Who Should Use this Guide

This Guide should be used by the union officials responsible for conducting audits (periodic examinations of local financial records). The general term “Trustee” is used in this Guide to refer to those individuals elected or appointed to serve in this capacity, or a similar capacity, whether for a full term or a specific record examination. Although the Guide covers the “basics” and is geared primarily to officials with little or no experience in conducting an audit, it can be helpful to more experienced officials as well.

How to Use this Guide

Trustees or other audit officials should become familiar with the contents of this Guide as soon as possible after being elected/selected. An initial review will provide an overview of the entire audit process and point out all the steps involved in conducting a meaningful examination of your union’s financial records.

You are not expected to remember all the procedures for conducting an audit after your first review of this Guide. Instead, before each step of your audit re-read the applicable chapter to refresh your understanding of what should be done. Refer to the Guide frequently during the audit process. Although we have tried to include all necessary information, the Guide does not specifically address every situation that may develop. Some record examinations may involve complex or unusual issues requiring you to seek further assistance.

Seeking Assistance

If you need advice or have questions about your responsibilities or provisions of your union’s constitution and bylaws, you should contact your union’s officers or parent body for help. In addition, OLMS staff in the field offices referred to at the end of this Guide can answer your questions about the LMRDA, related regulations, and this Guide.

Getting Started

Now that you are familiar with the purpose and contents of this Guide and how best to use it, it’s time to get started. Read Chapter 1 and begin preparing for your audit.

As you begin an audit of your union’s financial records your job as a Trustee may seem intimidating, particularly if you have never conducted an audit or are unfamiliar with your union’s books and records. However, if you think of the audit process as a series of separate steps and understand your responsibilities for each step, the entire process becomes more manageable. At this early stage preparation is very important since good planning and organization are key ingredients to conducting a meaningful audit. This chapter outlines the first steps you should take to prepare for your audit, including meeting with other Trustees to determine specific responsibilities, reviewing prior audit records and results, obtaining certain information from the principal financial officers of your union, and scheduling important audit activities.

Determining Responsibilities

The best way to get started is to review your union’s constitution and bylaws to determine your specific responsibilities as a Trustee. At least one week before the audit you should discuss your roles with the other Trustees either in person or by telephone and select a chairperson or team leader if one is not already designated. If none of the Trustees has ever conducted an audit, you should consider contacting members who have served as Trustees in prior years to discuss their experiences, both positive and negative. You may also wish to contact your parent body, as needed, to seek advice or information about your duties.

Gathering Materials

After determining your general responsibilities, you should obtain and review the following:

You should also review Figures 1, 2, 3, and 4 which may be adapted for use in your audit.

Meeting with Principal Officers

Before the audit begins, you and your fellow Trustees should meet with the principal financial officers of your union to:

It is important that you obtain this information early in the process and deal with the principal financial officers “up-front” in order to avoid any later misunderstandings or problems.

Scheduling the Audit

After talking to the principal financial officers, you should meet as a group to make some important decisions. First, decide the time frame (annual, semiannual, quarterly) that your audit will cover. This may be governed by your parent body constitution or local bylaws.

Next, decide when you want to begin the audit. If you have decided to review your union’s records for an entire year, then you may want to begin your audit shortly after your union’s annual financial report (LM-3 or LM-4) has been submitted to OLMS. This will ensure that your audit does not interfere with the ongoing operations of your union. You could also compare your own findings regarding the finances of your union with the information on the LM report.

Finally, develop a detailed plan which lists all the important phases of the audit or you may spend a lot of time and energy and still not get the job done right. This plan can be used to show your progress as you work your way through the 10-step audit and to identify specific responsibilities for each Trustee. A sample audit planner is provided as Figure 1.

Requesting Records

Your next task will be to create a list of financial records needed for your 10-step audit and provide this to the principal financial officers of your union. Otherwise, certain records such as membership meeting minutes may not be available when needed. A sample letter requesting financial records is provided as Figure 2. Feel free to modify this letter to conform with the records used in your union.

Financial records cannot be examined efficiently without some explanation of how they tie together. If you are not completely familiar with how your union’s financial records are maintained, consider creating a short questionnaire for the principal financial officers so that everyone has a common understanding. Figure 3 can be modified for this purpose. A completed version of this questionnaire is provided as Figure 4 to illustrate the type of information that should be obtained including any applicable constitutional provisions.

Two References at the end of this Guide should be reviewed by first-time Trustees before beginning an audit. Understanding Union Financial Records provides helpful illustrations of the types of financial records maintained by many unions and Union Financial Definitions provides easy to understand explanations of the financial terms used throughout this Guide. Use these References as needed during the audit.

Small unions may have hundreds of financial transactions every year. It would take a considerable amount of time to examine each of these transactions in detail. The next four chapters describe a 10-step audit which concentrates on reviewing key financial areas and is specifically designed to save you time, yet still provide for a meaningful, systematic review of your union’s financial books and records. The 10-step audit is not a “traditional” audit, but rather a limited, focused review of financial records that was developed for use by Trustees from small unions with little or no financial training or experience. It is modeled after techniques successfully used by OLMS.

Audit Objectives

The 10-step audit, summarized below, has four primary objectives:

Audit Design

The 10-step audit focuses on four major areas: disbursements, receipts, assets, and compliance with the requirements of the Labor-Management Reporting and Disclosure Act (LMRDA), as outlined below:

10-Step Audit

Optional Steps

In addition to these ten audit steps, Chapters 3-5 include eight optional steps for disbursements, four optional steps for receipts, and three optional steps for assets. These optional steps were designed to give you the flexibility to tailor your audit to the specific circumstances of your union and to make your audit as meaningful as possible. They are particularly recommended for use by Trustees in larger unions.

Audit Tips

|

You will probably issue an audit report to document your work. If your parent body requires that you submit a standard audit report form that outlines the financial condition of your union, you should collect necessary information for this report as you complete the audit steps described in Chapters 3-6 of this Guide. |

Like any organization, your union must spend money to operate. Most unions have a checking account which is used to make disbursements. Typical disbursements from your union’s checking account might include payments for per capita taxes, hall rentals, office supplies, and lost time to officers. Members expect that when their union spends money it will be for legitimate union purposes and that these expenditures will be properly authorized. Documents, such as your union’s constitution, minutes of meetings, bills, and vouchers, will help you determine why disbursements were made and whether they were authorized by your membership in accordance with your constitution and bylaws.

Confirming that established disbursement practices are being followed is essential to ensuring that your union’s funds are being handled responsibly on behalf of all members. Audit Steps 1 and 2 are designed to provide a simple but effective method for examining your local’s disbursements. They will assist you in determining whether payments were for approved, legitimate union business. In addition, they will enable you to determine if payments were properly recorded in your union’s records, allowing for accurate financial reporting to the members of your union, your parent body, and various government agencies.

To complete Audit Steps 1 and 2, as well as any optional steps you may select, you will need the following for the audit period: bank statements; cancelled checks; disbursements journal (or check stubs if a journal is not maintained); minutes of membership and Executive Board meetings; and all documents in support of disbursements such as bills, invoices, and vouchers. In addition, you will need any financial forms provided by your parent body. First-time Trustees may want to review the References “Understanding Union Financial Records” and “Union Financial Definitions” at the end of this Guide before beginning Audit Steps 1 and 2.

|

Step 1 |

Trace Cancelled Checks to the Bank Statements and Disbursements Journal

By completing Audit Step 1 you should be able to confirm the reliability and completeness of your union’s disbursements records.

If no discrepancies are noted during Audit Step 1, proceed to the next step. However, if you find any questionable items or have some areas of concern, refer to “Common Problems and Solutions” and “Significant Discrepancies” at the end of this chapter.

|

Step 2 |

Scan the Disbursements Journal and Record Unusual Entries

By completing Audit Step 2 you should be able to determine whether the checks issued from your union’s bank account were for legitimate union purposes.

If you find any questionable items or have some areas of concern while conducting Audit Step 2, refer to “Common Problems and Solutions” and “Significant Discrepancies” at the end of this chapter.

Optional Steps

As time allows, consider conducting one or more of the following optional steps or proceed to Audit Step 3. Some of these optional steps may be required by your parent body.

This is not an exhaustive list of optional audit steps. Based on your union’s recordkeeping system and any parent body requirements, you may choose to review other areas of disbursements.

Common Problems and Solutions

Even the best maintained disbursements records may have some problem areas. Frequently encountered problems are listed below with suggestions on how to resolve them:

Problem: |

Cancelled checks are not available. |

Solution: |

Ask officers to obtain copies from the bank. |

Problem: |

Bank statements indicate checks have been returned for non-sufficient funds (NSF). |

Solution: |

Determine when the first NSF (“bounced”) check was returned by the bank. Look for delayed deposits during the period. Ask officers for an explanation of the NSF checks and, if necessary, suggest that the disbursements records be properly noted. |

Problem: |

The disbursements journal entries do not match the corresponding information on the bank statements or on the cancelled checks. |

| Solution: |

Determine the reason for the discrepancies. Ask officers for an explanation, such as failure to reconcile the disbursements journal with the related monthly bank statements and, if necessary, suggest that the principal financial officers correct the records. |

Problem: |

No records to support disbursements exist. |

Solution: |

Review minutes for approval and, if necessary, ask officers about the payments. |

Problem: |

The union does not maintain a disbursements journal. |

Solution: |

Review check stubs and/or check register. |

Significant Discrepancies

The situations listed below may suggest that your union’s financial records are unreliable or that union funds have been misused:

If you detect a serious problem in your union’s records or a possible misuse of union funds, contact your parent body or the nearest OLMS office for assistance.

Parent Body Requirements

Note any additional audit procedures or standard audit forms relating to disbursements which your parent body requires you to use:

Local unions receive most of their money from their members in the form of dues payments. A common method of paying union dues is through dues checkoff. In this arrangement the employer periodically withholds the amount of dues from members’ wages and sends the money collected to the union or its parent body. In other instances, members pay their dues directly to the union. Generally these payments are deposited into the union’s checking account. Members entrust their dues money to the responsible union representatives and expect that the funds paid in will be available for the union to draw upon for authorized union activities. Ensuring that all of the money received by your union has been deposited into your union’s bank account is a key component to a successful audit. Audit Steps 3 and 4 will help you trace the receipts of your union into your union’s bank account and verify that receipts from all sources have been recorded and deposited.

To complete Audit Steps 3 and 4, as well as any optional steps you may select, you will need the following for the audit period: bank statements; deposit slips; receipts journal (or other records if a journal is not maintained); all documents which identify the source of your union’s receipts, such as employer checkoff statements; individual dues receipts; and member ledger cards. In addition, you will need any financial forms provided by your parent body. First-time Trustees may want to review the References “Understanding Union Financial Records” and “Union Financial Definitions” at the end of this Guide before beginning Audit Steps 3 and 4.

Trace Employer Dues Checkoffs to the Receipts Journal and Bank Statements

By completing Audit Step 3 you should be able to confirm that employer checkoff receipts are properly recorded in your union’s receipts records and deposited into your union’s bank account.

The following Alternate Step 3 must be substituted for Step 3 above only if all members’ payments to the union (for dues, working dues, fees, etc.) are made directly to union officers or employees and not through employer checkoff.

|

Alternate Step 3 |

Trace Direct Dues Payments to the Receipts Journal and Bank Statements

By completing Alternate Audit Step 3 you should be able to confirm that cash and checks for dues paid directly to the union by members are properly recorded in your union’s receipts journal and deposited into your union’s bank account.

If no discrepancies are noted during Audit Step 3 or Alternate Audit Step 3, proceed to the next step. However, if you find any questionable items or have some areas of concern, refer to “Common Problems and Solutions” and “Significant Discrepancies” at the end of this chapter.

Confirm That Receipts from All Other Sources Have Been Properly Recorded and Deposited

By completing Audit Step 4 you should be able to determine whether non-dues money coming into your union has been properly recorded in your union’s receipts records and deposited into your union’s bank account.

Make sure the amounts and frequency of these entries seem appropriate.

If you find any questionable items or have some areas of concern while conducting Audit Step 4, refer to “Common Problems and Solutions” and “Significant Discrepancies” at the end of this chapter.

Optional Steps

As time allows, consider conducting one or more of the following optional steps or proceed to Audit Step 5. Some of these optional steps may be required by your parent body.

This is not an exhaustive list of optional steps. Based on your union’s recordkeeping system and any parent body requirements, you may choose to review other areas of receipts.

Common Problems and Solutions

As with your union’s disbursements records, you may have encountered some difficulties while completing Audit Steps 3 and 4. Even the best kept receipts records may have some problem areas. Frequently encountered problems are listed below with suggestions on how to resolve them:

Problem: |

Bank records are not available. |

Solution: |

Ask officers to obtain copies from the bank. |

| Problem: |

Original checkoff records are not available. |

| Solution: |

Ask officers to obtain copies from the employer. |

Problem: |

Other original receipt records are not available. |

Solution: |

Ask officers for an explanation. |

Problem: |

The receipts journal entries do not match corresponding information on the bank statements or deposit slips. |

Solution: |

Determine the reason for the discrepancy. Ask officers for an explanation, such as failure to reconcile the receipts journal with the related monthly bank statements, and, if necessary, suggest that the principal financial officers correct the records. |

Problem: |

The entire amount of the checkoff check is not deposited into your union’s primary account. |

| Solution: |

Look at the other bank accounts for deposits of the remainder of these funds. Ask officers for an explanation of the disposition of these funds. |

Significant Discrepancies

As with the review of your union’s disbursements records, you might have reasons to doubt the accuracy of the union’s receipts records. The situations listed below may suggest that your union’s financial records are unreliable or that union funds have been misused:

If you detect a serious problem in your union’s records or a possible misuse of union funds, contact your parent body or the nearest OLMS office for assistance.

Parent Body Requirements

Note any additional audit procedures or standard audit forms relating to receipts which your parent body requires you to use:

When auditing assets, keep in mind that your union not only has money in its bank accounts, which may be in the form of a checking account, a savings account, or a certificate of deposit (liquid assets), but it may also own various types of equipment, such as a computer, a photocopier, or a file cabinet (fixed assets). The value of these assets must be included and accounted for during your audit. Both liquid assets and fixed assets might be overlooked during your audit unless your union keeps accurate and reliable records. Audit Steps 5 and 6 will help you identify, account for, and determine the total value of your union’s liquid and fixed assets. By completing these audit steps you will ensure that your union has an accurate, current inventory of all your union’s liquid and fixed assets, which can easily be updated as the need arises.

To complete Audit Steps 5 and 6, as well as any optional steps you may select, you will need the bank statements, receipts and disbursements journals for the audit period (or check stubs if journals are not maintained), any inventory of fixed assets prepared prior to your audit, and any forms provided by your parent body.

Identify All Bank Accounts, Verify Their Ending Balances, and Review Withdrawals/Transfers

By completing Audit Step 5 you should be able to identify the bank accounts maintained by your union during the audit period, determine the total amount of money in these accounts, and verify that withdrawals from these accounts were used for legitimate union purposes.

If no discrepancies are noted during Audit Step 5, proceed to the next step. However, if you find any questionable items or have some areas of concern, refer to “Common Problems and Solutions” and “Significant Discrepancies” at the end of this chapter.

Inventory Fixed Assets

By completing Audit Step 6 you should be able to identify the fixed assets owned by your union and verify the location of these assets.

If you find any questionable items or have some areas of concern while conducting Audit Step 6, refer to “Common Problems and Solutions” and “Significant Discrepancies” at the end of this chapter.

Optional Steps

As time allows, consider conducting one or more of the following optional steps or proceed to Audit Step 7. Some of these optional steps may be required by your parent body.

This is not an exhaustive list of optional steps. Based on your union’s recordkeeping system and any parent body requirements, you may choose to review other areas of your union’s assets.

Because small unions typically do not incur significant liabilities (debts), the 10-step audit does not address this area. However, if your union has significant liabilities such as delinquent taxes or unpaid bills, you may want to review them as time permits.

Common Problems and Solutions

You may encounter some obstacles as you inventory your union’s assets. These may range from poor recordkeeping to a question on how best to record the value of an asset. Two frequently encountered problems are listed below with suggestions on how to resolve them:

Problem: |

Bank statements are not available. |

Solution: |

Ask officers to obtain copies from the bank. |

Problem: |

The entire amount of a withdrawal from the union’s savings account is not deposited into your union’s checking account. |

Solution: |

Look at the other bank accounts for the deposit of the remainder of these funds. Ask officers for an explanation of what happened to these funds. |

Significant Discrepancies

It is easy to lose track of a fixed asset, or sometimes even a bank account, if accurate records are not maintained. The situations listed below may suggest that your union’s financial records are unreliable or that union funds or assets have been misused:

If you detect a serious problem in your union’s records or a possible misuse of union funds or assets, contact your parent body or the nearest OLMS office for assistance.

Parent Body Requirements

Note any additional audit procedures or standard audit forms relating to assets which your parent body requires you to use:

In 1959, Congress passed the Labor-Management Reporting and Disclosure Act, as amended (LMRDA). The LMRDA has at least ten provisions designed to promote the financial integrity of unions which are outlined in Figure 10. Four of these provisions will require special attention during the course of your audit. Essentially, they require that unions file annual financial reports with OLMS, maintain records that are sufficient to clarify or support the information shown on these reports, secure adequate bonding to provide protection against losses due to fraudulent or dishonest actions, and restrict the amounts of loans made to officers and employees. Audit Steps 7 through 10 will help you determine whether your union is complying with the LMRDA’s requirements for financial reporting, recordkeeping, bonding, and loans.

Confirm That the LM Annual Financial Report for the Latest Completed Fiscal Year Was Filed on Time

The LMRDA requires unions to submit an annual financial report (an LM report) to OLMS within 90 days after the end of their fiscal year. Unions with annual receipts more than $200,000 must file an LM-2 report. Unions with annual receipts less than $200,000 may file a shorter LM-3 report. Unions with annual receipts less than $10,000 may file an abbreviated LM-4 report.

Determine Whether Financial Records Were Properly Maintained

The LMRDA requires unions to keep financial records for five years after the applicable LM reports are filed which are sufficient to clarify or verify the information shown on these reports, as explained in Figure 11.

Ensure That All Officers and Employees Who Handle Funds Are Adequately Bonded

The LMRDA requires that all unions with property and annual receipts greater than $5,000 secure a bond for at least 10% of the receipts and assets handled by union officers and employees during the prior fiscal year to ensure against losses resulting from fraudulent or dishonest acts. If bonding is required, your union should have a bonding certificate, or other proof of bonding, which indicates the total amount recoverable if a loss of union funds occurs. Many parent bodies obtain coverage for their affiliate unions.

Confirm That No Officers or Employees Were Loaned More than $2,000 by Your Union

The LMRDA places certain restrictions on the type and amount of loans that can be made by a union. The law provides that loans made to a union officer or union employee may not exceed $2,000 in total indebtedness at any time, and all loans must be reported on the appropriate LM report. Your parent organization may also have restrictions or prohibitions regarding loans.

Parent Body Requirements

Note any additional audit procedures or standard audit forms relating to financial reporting, recordkeeping, bonding, and loans which your parent body requires you to use:

By now you have spent a lot of time and energy examining your union’s books and records to complete your 10-step audit. Your fellow members and your parent body will be very interested in what you found. But first you must review your findings, resolve any loose ends, decide how to document your work, and report your findings. In many respects, wrapping up is the most important part of your audit.

Taking Stock

Until now, you and the other Trustees may have been looking at your union’s receipts, disbursements, and assets on an individual basis rather than as a group. Now you must get together to:

Meeting with Principal Officers

Unless significant discrepancies have been detected in the union’s records and parent body or other assistance has been requested to help resolve these issues, you should meet with the principal financial officers of your union to discuss your preliminary findings, resolve any remaining concerns, and recommend changes to improve compliance with LMRDA requirements and adherence with sound internal financial controls and with parent body financial practices and procedures.

Reporting Your Findings

At this point, your union’s members and parent body probably want to know what the general financial condition of your organization is, whether your audit disclosed any problems and, if so, how they were resolved. If your union has standard forms to document your work and report your findings to the membership, fill them out. Otherwise, you may want to review the sample audit report shown as Figure 14 which can be modified to better suit your situation.

Completion of the 10-step audit allows you to make some broad statements about the financial books and records of your union. For example, if no significant problems for the audit period were uncovered, you can say your audit indicates:

Any additional findings or recommendations can be incorporated in your report as shown in Figure 14. If the 10-step audit has verified the accuracy of your union’s books and records it should also be relatively easy to create a balance sheet like that found in this figure to report the general financial condition of your union.

Once you have decided what to say and how to say it, you should probably select a spokesperson to respond to any questions. Your audit report should then be submitted to your Executive Board, membership, and parent body, as applicable. Copies of your report could also be posted on union bulletin boards or cited in your union’s newsletter.

| A Final Word from OLMS Now that you have completed your audit, we would like to say “thanks.” In your role as a Trustee, you have helped to ensure that your union’s funds and other assets are safeguarded and expended appropriately for the benefit of your union and its members. As a final step, you should place a copy of your audit report and all related work papers, notes, etc., in a folder for use by your union’s Trustees when the next audit is conducted. Be sure to include a copy of this publication which we hope you found helpful in fulfilling your important responsibilities as a Trustee. |

Figures

Audit Planner |

|

|---|---|

| Date Completed |

Activity |

Chairperson selected. (Chapter 1) |

|

Constitution/bylaws and other governing documents reviewed. (Chapter 1) |

|

Latest audit report and LM annual financial report reviewed. (Chapter 1) |

|

Initial meeting with principal financial officers to make arrangements for audit held. (Chapter 1) |

|

Time frames for audit determined. (Chapter 1) |

|

Principal financial officers notified of audit starting date and records needed. (Chapter 1) |

|

Financial Questionnaire prepared if necessary. (Chapter 1) |

|

Disbursements reviewed. (Chapter 3) |

|

Receipts reviewed. (Chapter 4) |

|

Assets examined. (Chapter 5) |

|

Latest LM annual financial reporting confirmed. (Chapter 6) |

|

Recordkeeping reviewed. (Chapter 6) |

|

Bonding coverage confirmed. (Chapter 6) |

|

Loan analysis completed. (Chapter 6) |

|

Audit Report completed. (Chapter 7) |

|

Audit Report to parent body and membership submitted. (Chapter 7) |

|

Letter Requesting Access to Financial Records January 10, 2001 Treasurer Richard Roe Dear Mr. Roe: As you know, the Trustees plan to start our quarterly audit of Local 888’s financial books and records on Saturday, January 20, 2001 at the union hall at 8:00 a.m. Please make available the latest Trustee Audit Report, the latest LM annual financial report, and the following records for the period October 1, 2000 - December 31, 2000:

If we need any additional records or information, we will let you know. Your cooperation is greatly appreciated. Sincerely, John Smith |

Financial Questionnaire |

|||

|---|---|---|---|

1. What sources of receipts does the union have? |

|||

Yes |

No |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. How is this money recorded in the union’s financial records?

|

|||

3. Who is responsible for making these entries in the union’s financial records?

|

|||

4. What kinds of receipts records are maintained? |

|||

Yes |

No |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5. Where is the union’s money kept on deposit? |

|||

Type of Account |

Bank |

Account Number |

|

|

|||

6. Does the union have any investments such as stocks or bonds? If so, list.

|

|||

7. Does the union have an inventory of fixed assets showing date of purchase and cost?

|

|||

8. Does the union have a safe or safe deposit box? If so, specify location/contents.

|

|||

9. Are all disbursements made by check?

|

|||

10. What kinds of disbursements records are maintained?

|

|||

Yes |

No |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11. How are disbursements approved, made, and recorded in the union’s financial records?

|

|||

12. Did any special situations occur (salary increases, convention expenses, financial support from parent body, office break-in and related insurance claims, etc.) during the audit period?

|

|||

Key Constitutional Provisions Officer Duties: Officer Entitlements: Spending Authorization: Other: |

|||

Completed Financial Questionnaire Factory Workers Local 888 |

|||

|---|---|---|---|

1. What sources of receipts does the union have? |

|||

Yes |

No |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. How is this money recorded in the union’s financial records?

|

|||

3. Who is responsible for making these entries in the union’s financial records?

|

|||

4. What kinds of receipts records are maintained? |

|||

Yes |

No |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5.Where is the union’s money kept on deposit? |

|||

Type of Account |

Bank |

Account Number |

|

Checking Account Savings Account Certificate of Deposit Money Market Other: |

National City |

2215607 |

|

6. Does the union have any investments such as stocks or bonds? If so, list.

|

|||

7. Does the union have an inventory of fixed assets showing date of purchase and cost?

|

|||

8. Does the union have a safe or safe deposit box? If so, specify location/contents.

|

|||

9. Are all disbursements made by check?

|

|||

10. What kinds of disbursements records are maintained? |

|||

Yes |

No |

||

|

|||

|

|||

|

|||

|

|||

|

|||

|

|||

|

|||

|

|||

|

|||

|

|||

11. How are disbursements approved, made, and recorded in the union’s financial records?

|

|||

12. Did any special situations occur (salary increases, convention expenses, financial support from parent body, office break-in and related insurance claims, etc.) during the audit period?

|

|||

Key Constitutional Provisions Officer Duties: Article 40, Section 1-12 — The President shall sign all vouchers and countersign all checks issued by Treasurer. Recording Secretary will sign all vouchers and keep minutes of meetings. Treasurer will receive all income, issue receipts, make deposits, write checks, maintain a property inventory, and prepare monthly financial report for membership meetings. The Trustees shall audit the records quarterly using forms provided by the International. They will confirm that all funds are deposited and that the financial officers are bonded. They will issue a report to the local with a copy to the International. If inaccuracies appear the General Secretary Treasurer has the authority to conduct an audit and, if necessary, schedule a hearing. Officer Entitlements: Article 50, 51 — Lost time will be paid only when official union business requires that a member forfeit salary from his employer. Travelers are entitled to reimbursement for the actual cost of lodging and transportation and a meal allowance of $30/day. Officers are entitled to salaries specified in the local bylaws. Spending Authorization: Article 46 — All disbursements must be approved by the membership. Other: Article 6, 48 — Per capita taxes will be paid on the fifteenth of each month. The International will provide bonding coverage for all local officers and employees who handle funds. |

|||

Disbursements Reconciliation Worksheet |

||

|---|---|---|

Month |

Disbursements Per Union(1) |

Disbursements Per Bank(2) |

October |

$2,397.22 |

$2,614.82 |

November |

2,056.19 |

2,731.53 |

December |

3,199.32 |

2,680.32 |

Total |

$7,652.73 |

$8,026.67 |

(3)Plus Service Charges |

+88.20 |

N/A |

(4)Less Outstanding Checks |

N/A |

-312.09 |

Plus Service Charges |

+ 88.20 |

N/A |

(4)Less Outstanding Checks |

N/A |

-312.09 |

(5) Plus Outstanding Checks |

N/A |

+526.35 |

Less Transfers |

N/A |

-500.00 |

(7)Adjusted Total |

$7,740.93 |

$7,740.93 |

Notes

|

||

Receipts Reconciliation Worksheet |

||

|---|---|---|

Month |

Receipts Per Union(1) |

Receipts Per Bank(2) |

October |

$2,796.50 |

$2,938.55 |

November |

2,566.80 |

2,832.45 |

December |

2,724.35 |

2,602.25 |

Total |

$8,087.65 |

$8,373.25 |

(3)Plus Interest |

+37.60 |

N/A |

(4)Less Outstanding Checks |

N/A |

-398.00 |

(5)Plus Outstanding Deposits |

N/A |

+650.00 |

Less Transfers |

N/A |

-500.00 |

(7)Adjusted Total |

$8,125.25 |

$8,125.25 |

Notes

|

||

Liquid Assets Inventory |

||

|---|---|---|

Account No. 1 |

||

Name of Account |

General Fund |

|

Location of Account |

National City |

|

Type of Account |

Checking Account |

|

Account Number |

2215607 |

|

Balance per Bank Statement |

|

$1,378.11 |

Balance per Bank Statement |

|

$1,378.11 |

Account No. 2 |

||

Name of Account |

General Fund |

|

Location of Account |

National City |

|

Type of Account |

Savings Account |

|

Account Number |

2215608 |

|

Balance per Bank Statement |

|

$2,510.50 |

Account No. 3 |

||

Name of Account |

General Fund |

|

Location of Account |

First Federal |

|

Type of Account |

Certificate of Deposit |

|

Account Number |

1607126 |

|

Balance per Bank Statement |

|

$1,500.00 |

Total Ending Balance |

|

$5388.61 |

Fixed Assets Inventory |

|||

|---|---|---|---|

Item |

Location |

PurchaseDate |

Cost or CurrentValue |

1.Filling Cabinet |

Office |

1/7/75 |

$150.00 |

2.Typewriter |

Recording Secretary's Home |

8/16/95 |

$250.00 |

3.Desk |

Office |

1/7/75 |

$241.00 |

4.Chairs(4) |

Office |

11/5/91 |

$295.00 |

5.Photocopier |

Office |

2/12/94 |

$300.00 |

|

|

Total |

$1,195.00 |

| "Note: No fixed assets were sold, donated, or otherwise disposed of during the audit period. |

|||

Ending Bank Balance Reconciliation Worksheet |

|||

|---|---|---|---|

Ending Balance Per Bank: |

|

|

$1,378.11 |

Plus Outstanding Deposits: |

Christmas Raffle |

|

+650.00 |

|

|

|

$2,028.11 |

Less Outstanding Checks: |

1701 |

50.10 |

|

|

1704 |

450.00 |

|

|

1709 |

26.25 |

|

|

|

|

-526.35 |

Adjusted Bank Balance: |

|

|

$1,501.76* |

*This amount should agree with the figures shown in the union records. If significant discrepancies are detected, double-check the figures and, if necessary, seek an explanation from the principal financial officers. |

|||

|

LMRDA Requirements Relating to Union Funds The Labor-Management Reporting and Disclosure Act of 1959, as amended (LMRDA), establishes a number of requirements relating to the handling and reporting of union funds: Reports — Unions must file annual financial reports with the Office of Labor-Management Standards (OLMS) on one of three forms depending on the reporting union’s total annual receipts. Unions with $200,000 or more in receipts and those in trusteeship must file the Form LM-2. Unions with less than $200,000 in total annual receipts which are not in trusteeship may file the shorter Form LM-3 and unions with less than $10,000 in total annual receipts which are not in trusteeship may file the abbreviated Form LM-4. The reports are public information and are available from OLMS for any person to examine or purchase copies. Records — Unions must retain the records necessary to verify the annual financial reports (Form LM-2/3/4) for at least five years after the reports are filed and must permit members to examine the records for just cause. Bonding — In unions with more than $5,000 in property and annual receipts, officers and employees who handle union funds or property must be bonded to provide protection against losses by acts of fraud or dishonesty on their part. Fiduciary Responsibility — Union officers have a duty to manage the funds and property of the union solely for the benefit of the union and its members in accordance with the union’s constitution and bylaws. Embezzlement — A union officer or employee who steals or otherwise misappropriates union funds or other assets commits a federal crime punishable by a fine and/or imprisonment. Loans — A union may not have outstanding loans to any one officer or employee at any time that in total exceed $2,000. Fines — A union may not pay the fine of any officer or employee convicted of any willful violation of the LMRDA. Elections — Union funds or other assets may not be used to promote the candidacy of any candidate in an election of union officers. Trusteeships — If a union is in trusteeship, no funds of the union can be transferred to its parent body other than the normal per capita tax and assessments payable by subordinate bodies not in trusteeship. Office Holding/Employment Prohibition — Persons convicted of certain crimes may not hold union office or employment for up to 13 years after conviction or after the end of imprisonment. If you have any questions about the LMRDA, contact the nearest OLMS office for assistance. |

|

LMRDA Recordkeeping Requirements Section 206 of the Labor-Management Reporting and Disclosure Act of 1959, as amended (LMRDA), outlines the general recordkeeping requirements for unions. The Office of Labor-Management Standards (OLMS) finds that about thirty-five percent of the unions audited by OLMS failed to maintain adequate records. The overwhelming majority of these violations were unintentional; the responsible union officials often did not understand what specific records had to be kept for the required five-year period. However, because of the wide diversity of recordkeeping systems used by international and national unions and their affiliates, it is not possible for OLMS to precisely define what records must be maintained by every union. As a general rule, all types of records used in the normal course of doing business must be maintained by unions for five years. This includes such financial records as receipts and disbursements journals, cancelled checks and check stubs, bank statements, dues collection receipts, per capita tax reports, vendor invoices, and payroll records. OLMS has found that, for the most part, unions do maintain these types of basic financial records but often fail to keep other records which help explain or clarify financial transactions such as:

All types of financial records and other related records that clarify or verify financial transactions must be maintained for five years after the applicable LM reports are filed. If the principal financial officers or Trustees have any questions about recordkeeping responsibilities, the union records in question should be retained or advice from the nearest OLMS field office should be sought. |

|

|||||||||||||||||||||||||||||||||||

|

Internal Financial Controls Section 501 of the LMRDA outlines the general fiduciary responsibilities for officers and employees of unions. Union officials occupy positions of trust and therefore must ensure that the union’s funds and other assets are used solely for the benefit of the union and its members. Unfortunately, if a union or other organization does not have an adequate system of internal financial controls, some individuals may use or be tempted to use some of the organization’s funds for their own purposes or become careless and mix the organization’s money with their own. To prevent, or at least deter, the misuse or embezzlement of their funds, most organizations including corporations, banks, international unions, etc., establish internal controls over the handling of their finances. Adequate and effective internal controls require a separation of functions and responsibilities among a number of individuals who are actively involved in handling the union’s finances and who provide a system of “checks and balances” over each other’s activities. An entirely adequate system of internal controls is not always possible in small unions which employ no more than one full-time or part-time officer or employee to handle the union’s financial affairs and cannot afford the services of an independent accountant. However, some effective internal controls can usually be established even in one- person operations. For example, union executive boards or other governing bodies should consider taking the following actions to safeguard union funds by requiring that:

Although establishment of internal financial controls will not absolutely prevent misuse or embezzlement of union funds, internal controls such as those listed above will deter most individuals from misusing union funds. Trustees and other union officers who have further questions about internal financial controls should seek the advice of their parent body or the nearest OLMS field office. |

|

||||||||||||||||||||||||||||

References

Understanding Union Financial Records

Unions receive money, deposit it into bank accounts, and spend it for a variety of reasons. The LMRDA requires that records of every union financial transaction be maintained and that summaries of these transactions be reflected on the Labor Organization Annual Report (LM-2, LM-3, or LM-4). Typical receipts, disbursements, assets, and liabilities records maintained by Factory Workers Local 888, a fictitious union, are described below.

Receipts

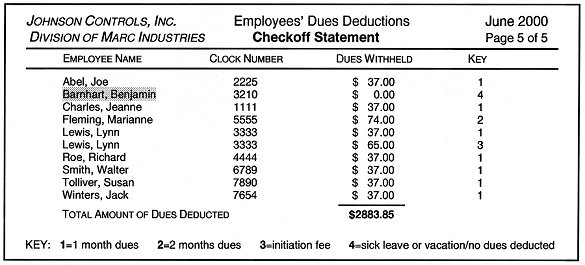

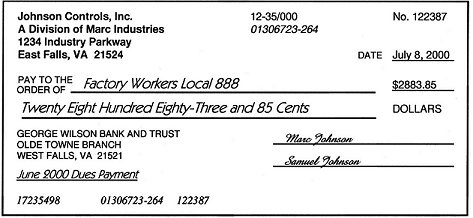

Unions obtain their funds chiefly from dues paid by union members. Other sources may include fees, assessments, interest, and dividends. All funds going into a union are referred to as "receipts." Receipts records generally consist of dues checkoff statements and individual dues receipts issued to members who pay their dues directly to the union. The checkoff statement which is sent by the employer along with the dues check should be retained in your union records. A typical checkoff statement and check are illustrated below:

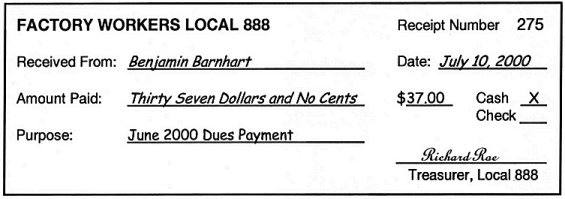

In this checkoff statement you will notice that dues were not deducted for Benjamin Barnhart for the month of June. He must pay his dues directly to the union's Treasurer.

When dues are paid directly to the union, the member is usually given an individual dues receipt. The original receipt should be given to the dues paying member. A duplicate (carbon copy) of the receipt should be kept in a bound book and retained in your union's receipts records. An individual dues receipt for Benjamin Barnhart is illustrated below:

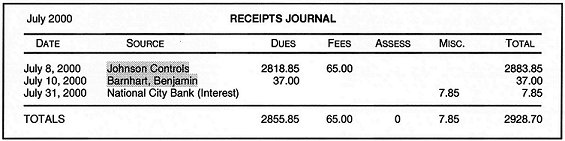

All receipts should be posted in your union's financial records (receipts journal, checkbook register, and/or check stubs). To keep track of receipts, many unions rely on a receipts journal. Note that the checkoff check from Johnson Controls and the direct dues payment from Benjamin Barnhart are posted in the illustration below:

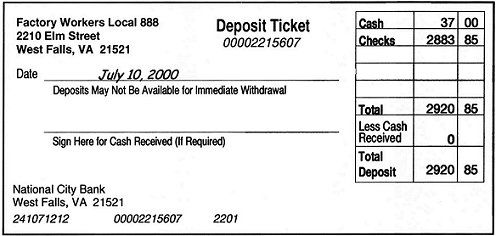

Once receipts are recorded in your union's financial records, a bank deposit slip like that shown below should be prepared and a duplicate retained by your union. Note that this deposit slip only shows the total amount of the checks and cash recorded in the receipts journal above.

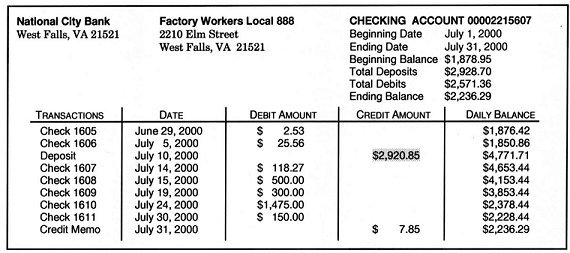

All deposits will be reflected on your union's monthly bank statements. In the following illustration, you will see a deposit made on July 10, 2000 in the amount of $2,920.85. The union financial records explaining this deposit consist of the receipts journal, duplicate deposit slip, direct pay receipt, and checkoff statement.

Disbursements

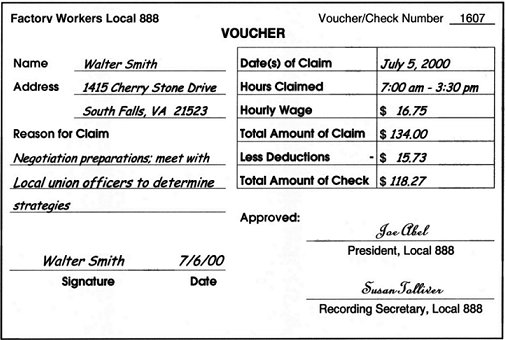

Unions spend money for a variety of reasons like per capita tax payments, lost wages, expenses, office supplies, or postage. Prior to disbursing money, many unions require that a voucher be completed. Frequently other documents such as bills and invoices supporting the claim are stapled to the voucher. An example of a voucher is shown below:

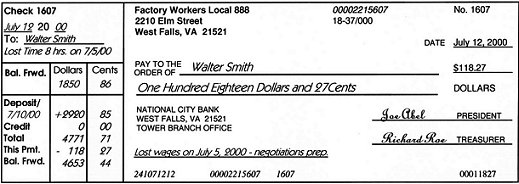

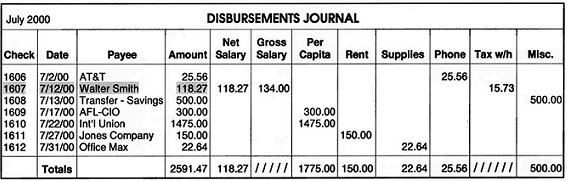

The following check is payable to Walter Smith, who has submitted the voucher shown above, for payment of lost time. Smith is the payee on the check illustrated below. The check is signed (or approved) by President Joe Abel and Treasurer Richard Roe. They are the signatories of this check. When this check is negotiated, Walter Smith will sign his name on the back of the check showing that he received the proceeds from this check. His signature is referred to as an endorsement and he is considered to be the endorser. After a check is charged to the union's account, the cancelled checks for the month are generally returned to the union along with the monthly bank statement. The amount of the check will be posted on the bank statement and on the bottom right-hand corner of the check as shown below. The check stub, to the left of the check, provides additional information (lost time hours) about this transaction.

A record of every check the union issues must be maintained. The checkbook register and/or check stubs often function as a disbursements journal, or a listing of all checks written. Some unions also keep a separate disbursements journal so that they can allocate similar kinds of disbursements into separate columns. This makes it easier to calculate how much money is being spent for similar purposes. An example of a disbursements journal page is shown below. Note that the check to Walter Smith is shown in this illustration:

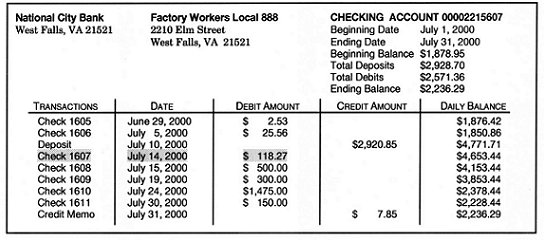

All cancelled checks will be reflected on your monthly bank statements. These statements will generally identify the check numbers and the amounts of the checks which were charged against your union's account during the month. In the following illustration, check number 1607 to Walter Smith for $118.27 was negotiated and charged against the union's account on July 14, 2000. The voucher (and any attached documents), check stub, disbursements journal, and cancelled check all explain (or support) the disbursements shown on these bank statements. Many unions require that all disbursements be approved by their members. In these instances, the membership meeting minutes may provide further details regarding the purpose of these disbursements.

Assets

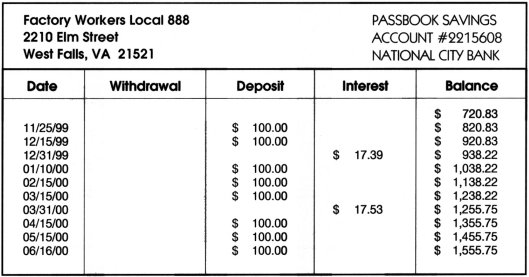

Unions retain both liquid (cash, or easily convertible to cash) and fixed (furniture, computers, etc.) assets. The assets of most concern in an audit are liquid assets, which most often are in the form of checking and savings accounts, certificates of deposit, cash, and sometimes stock in the employer company. An illustration of a passbook savings account follows:

A statement savings account may also be maintained. Periodic statements (monthly, quarterly or semi-annually) will be sent from the bank and reflect the transactions during the period.

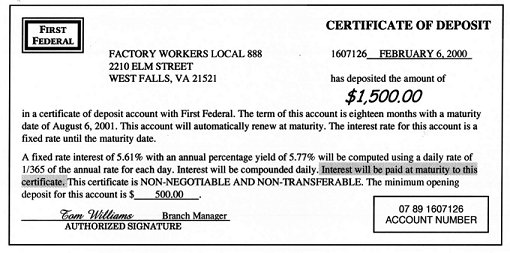

Another common form of savings for a union is a certificate of deposit (CD). Unlike a passbook savings account, the money in the CD cannot be easily withdrawn for a designated time period without payment of a penalty. Interest is paid by the bank on the CD and may be deposited to the union's checking or savings account or deposited into the certificate. These terms should be specified on the CD or clarified with your union officers. In the illustration below, the certificate of deposit specifies that the interest on this CD will be applied to the CD when it matures on August 6, 2001.

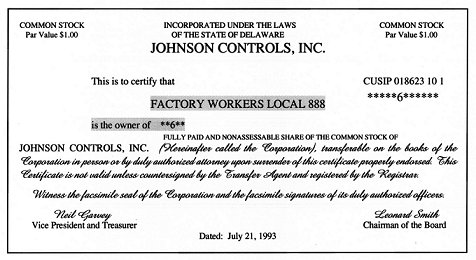

Some unions own stock for investment purposes or buy stock in the company that employs their members so they can get financial statements about their employer. The stock certificate will generally identify the number of shares of stock held by the union. In the illustration below, Factory Workers Local 888 is the owner of six shares of stock in Johnson Controls Incorporated.

Unions also retain fixed assets like buildings, automobiles, computer equipment, and furniture. In addition to inventories of fixed assets showing their original cost, estimated current value, or book value, unions should also retain various documents showing ownership of these assets, such as property deeds, mortgage payment statements, car titles, and equipment warranties. These documents should be kept in a secure place, such as a safe deposit box at the union's bank.

Liabilities

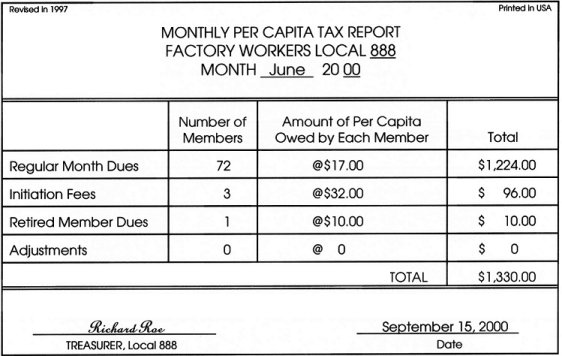

Any bill owed by a union but not yet paid is considered to be a liability. Liabilities might include an electric bill which has not been paid, taxes payable to the IRS, mortgage payments, or any other financial obligation. Another example of a liability would be per capita taxes owed to your parent body. In the monthly per capita tax report shown below, Factory Workers Local 888 is submitting a late payment (in September 2000) for its June 2000 per capita taxes.

Some parent bodies require that their affiliates use prescribed forms to record their receipts, disbursements, assets, and liabilities. If you have any questions concerning the types of records which are required by your parent body, you should review your constitution or contact your parent body for assistance.

A

accounting — A system of recording and conveying information about an individual or organization in financial terms.

asset — Anything of value owned by the union such as cash, furniture, etc.

audit — A systematic examination of financial books and records involving analyses, tests, and confirmations to determine their accuracy, completeness, and compliance with established standards.

authorization — An established process in which purchases and/or other disbursements are approved by union officers or members.

B

bank balance — The amount of money in a bank account on a particular date as recorded by the financial institution on bank statements.

bank statement — A statement sent by the bank to a checking account customer, such as a union, showing deposits, checks cleared, service charges, interest earned, and ending balances for a specified period, usually one month.

bond — Insurance protecting an organization, such as a union, against financial loss through fraud or dishonesty.

book balance — The amount of money in a bank account on a particular date as recorded by the union in its financial records.

book value — The amount shown in the union’s records for a particular asset, normally the cost of the asset less accumulated depreciation.

C

cancelled check — An original check which has cleared through the bank.

cash — Money, negotiable checks, certificates of deposit, and balances in savings and checking accounts.

cash reconciliation — A comparison of the union’s account balances with the records of the bank (bank statement), listing differences to bring the balances into agreement.

certificate of deposit — A certificate from a bank stating that a customer, such as a union, has a specified sum on deposit which will earn a specific rate of interest for a specific period of time.

checkoff — The authorized withholding of dues, fees, or other assessments from union members’ wages by an employer for transmittal to the union.

check stub — The part of a check or receipt retained as a record of payment.

credit memo — An internal memorandum used by banks to increase the fund balance in an account containing a brief explanation of why the account was increased. A duplicate copy of the memorandum is forwarded to the customer with the regular bank statement.

D

debit memo — An internal memorandum used by banks to decrease the fund balance in an account containing a brief explanation of why the account was decreased. A duplicate copy of the memorandum is forwarded to the customer with the regular bank statement.

deposit slip — A bank document prepared by the account holder, such as a union, that reflects the amount deposited into an account.

depreciation — A systematic process by which the original cost of a long term asset, such as a building, is reduced and carried on the union’s books at a lesser figure. (See book value)

direct pay — Payments of dues or other fees made directly to the union by members by cash or check (as opposed to payments received indirectly through a checkoff arrangement with the employer).

disbursements — Money paid out by the union.

disbursements journal — A chronological list of all union payments made in which the date, check number, amount, payee, and purpose are recorded.

disbursements reconciliation — A comparison of the union’s disbursement records with the records of the bank (bank statements), listing differences to bring the balances into agreement.

dues — A periodic payment to a union by members which establishes them as members in good standing. The amount is generally included in the bylaws and constitution and is approved by a secret ballot vote of the membership.

E

endorser — One to whom ownership of a negotiable document, such as a check, is transferred by endorsement.

endorsement — Signature appearing on the back of a union check as evidence of the legal transfer of ownership, especially in return for cash or credit indicated on its face.

F

fiduciary duty — The requirement in law that union officers hold and manage union funds only for legitimate union purposes.

financial officer — The union’s constitutional officer whose responsibilities include the handling of union receipts, disbursements, and assets.

financial records — All records relating to the receipt, management, and disbursement of union funds. These include, but are not limited to, receipts records, minutes of meetings in which financial decisions are made, bank statements, expense vouchers, cancelled checks, debit memoranda, receipts and disbursements journals, etc.

fixed assets — Those assets acquired for use by the union with no intention of selling them until their usefulness is diminished, such as land, buildings, office equipment, furniture, etc.

I

interest — Money earned on union bank accounts or investments or the charge or cost for using money, frequently expressed as a rate per period, usually one year, called the interest rate.

invoice — A detailed list of goods purchased by a union or services rendered to a union with an account of all costs.

L

liability — An obligation or a debt.

liquid asset — Cash, or assets that can be easily converted to cash, such as savings accounts and certificates of deposit.

lost time — Time spent by an individual, away from his/her regular job, on union business.

lost time payment — Reimbursement for wages lost while conducting union business.

M

member ledger cards — Individual collection records for union members which contain all of the pertinent information concerning a member’s dues, fees, and assessment payments to the union.

N

negotiate — To transfer ownership of a financial instrument (like a check) to another (such as a bank) in return for a thing of value (usually cash).

non-sufficient funds (NSF) — A situation where the balance in an account is not sufficient to cover the amount of checks written on the account. Such checks are commonly referred to as “bounced” checks.

O

outstanding checks — Checks written by the union which have not yet been deducted from the union’s checking account balance by the bank.

outstanding deposits — Deposits that have been recorded by a union but have not yet been received (and recorded) by the bank. Also called “deposits in transit.”

P

payee — A person to whom money is paid.

per capita tax — A per member assessment, usually by a parent body, that unions must remit periodically.

R

receipt — A document which the union provides to confirm that money has been collected or which a vendor provides to confirm that goods or services have been provided to the union.

receipts — Can refer to documents cited above or money received by a union.

receipts journal — A chronological listing of union receipts including the date, amount, source, and purpose of each receipt.

receipts reconciliation — A comparison of the union’s receipts records with the records of the bank (bank statement), listing differences to bring the balances into agreement.

reconcile — A method of calculating the correct amount of cash in a bank account by taking the opening balance of the account, adding any receipts, deducting any disbursements (not including outstanding checks), and comparing the result with the bank statement ending balance.

S

signatory — The individual authorized by the union to sign checks.

signature cards — Cards signed at the bank, for a specific account, with the signatures of those authorized to make transactions on the account.

supporting documents — Checkoff lists, bills, invoices, and other documents maintained by the union to verify the accuracy of the entries made in the union records and deposits and withdrawals made on the union’s accounts.

T

trace — To follow a receipt of a payment (to the union) to an entry in the union’s receipts journal and then from these entries to a related deposit slip and corresponding entry on the union’s bank statement; or to follow a union disbursement from authorization of expenditure through the invoice, bill, check stub or other record into the union’s disbursements journal and then from the journal to the related cancelled check and corresponding entry on the union’s bank statement.

transfer of funds — The movement of cash between accounts held by the union. Such transactions do not represent receipts or disbursements, as the union neither receives nor disburses cash.

V

void check — A union check made invalid because of a mistake made in its preparation.

voucher — A union claim form for reimbursement of expenses, mileage, lost time, etc., which documents the date, amount, and purpose of the payment owed to the preparer of the voucher.

W

withdrawal slip — Bank document prepared by the account holder, such as a union, that reflects the amount withdrawn from an account.

Checklist for Conducting Audits in Small Unions

This checklist has been developed by the Office of Labor-Management Standards (OLMS) to help Trustees and other persons with financial responsibilities in small unions (annual receipts less than $50,000) audit the financial records of their unions and ensure compliance with certain requirements of the Labor-Management Reporting and Disclosure Act of 1959, as amended (LMRDA). This checklist features a 10-step audit that concentrates on reviewing key financial areas and is specifically designed to save time, yet still provide for a meaningful, systematic review of financial books and records. The 10-step audit is not a “traditional” audit but rather a limited, focused review that was developed for Trustees from small unions with little or no financial training or experience. It is modeled after techniques successfully used by OLMS. The 10-step audit should help Trustees carry out their primary responsibility to ensure that union funds and other assets are properly accounted for and used solely for the benefit of their union and its members.

Planning

|

Meet with the other Trustees or audit officials to discuss general responsibilities, assign duties, and select a team leader. |

|

Review any forms, manuals, and handbooks created by your parent body which outline your duties and responsibilities, including any required standard audit report forms. Also review your union’s constitution and bylaws, especially those provisions dealing with dues rates, officer salaries and expenses, lost time policies, officer duties, and spending approval procedures. |

|

Obtain and review your union’s most recent audit report and LM-3 or LM-4 annual financial report. |

|

Meet with the principal financial officers of your union to seek their cooperation and support. Find out if any special situations occurred (salary increases, convention, supplemental financial support from parent body, office break-in and related insurance claims, etc.) during the audit period. |

|

Determine the person you should deal with to obtain access to necessary financial records and explanations on how these records are maintained. |

|

Select an audit period, develop a general timetable for completion of your work, and confirm that all necessary financial records (including Executive Board and membership meeting minutes) will be available. |

|

Contact your union’s parent body or one of the OLMS offices listed on the last page of this pamphlet if questions arise about any phase of your audit. |

10-Step Audit

Disbursements – Steps 1 & 2

Trace cancelled checks to the bank statements and disbursements journal.

Locate all cancelled checks for at least two months in your audit period and confirm that the amounts of each check match the amounts for the corresponding entries on your union’s bank statements. Compare these checks with the corresponding entries in the disbursements journal. Confirm that the payee, date, and purpose are properly recorded in the disbursements journal.

Examine your union’s disbursements journal for the entire audit period and make a list of any disbursements that appear to be unusual or out of the ordinary. Review the supporting bills, vouchers, invoices, and membership meeting minutes for all of these disbursements and confirm that they were made for legitimate union purposes, as approved by the membership.

Receipts – Steps 3 & 4

Locate all checkoff statements for the period and confirm that each checkoff check is recorded in your union’s receipts journal. Select at least two months and confirm that the amounts recorded in the receipts journal match corresponding entries on your union’s bank statements. Alternatively, if all dues are received directly from members, conduct similar procedures to make sure that this dues money was properly recorded and deposited.

Locate all original receipts for at least two months and confirm that all non-dues checkoff income (interest, rent, refunds) cited on these records matches corresponding entries in the receipts journal. Trace these entries from the journal to corresponding entries on your union’s bank statements.

Assets – Steps 5 & 6

Locate all bank statements for the audit period. If any bank accounts were closed during the period find out what happened to the proceeds from these accounts. Make a list of all active bank accounts at the end of your audit period. Record the ending balances for each bank account as shown on your union’s bank statements. Add together these figures to calculate the total liquid assets at the end of the audit period. Determine that all withdrawals during the audit period from savings accounts, money market accounts, or certificates of deposit were used for legitimate union purposes, as approved by the membership.

Prepare an updated inventory of your union’s fixed assets such as a computer, a photocopier, or a filing cabinet by determining whether any assets previously held were disposed of during the audit period and whether any assets were acquired during the audit period. Create a list showing all fixed assets at the end of the audit period; either their original cost, estimated current value, or value as carried in your union’s books; and their location.

While completing Steps 1 - 6 you may well encounter difficulties understanding your union’s records or the necessary records to complete the steps may not be immediately available. If this occurs, you should talk to the principal financial officers to resolve these concerns. However, you may also encounter significant problem areas such as altered checks, falsified records, missing assets, or a possible misuse of funds. If this occurs, you should contact your parent body or the nearest OLMS office for assistance. |

LMRDA Compliance – Steps 7 – 10

Locate your union’s LM-3 or LM-4 annual financial report for the latest completed fiscal year and confirm that it was filed on time (within 90 days after the end of your union’s fiscal year) with OLMS. If not, advise the principal financial officers to complete and submit it to OLMS as soon as possible.

Verify that the records maintained by your union are sufficient to clarify or verify the information shown on your union’s LM-3 or LM-4 annual financial reports. If not, advise the principal financial officers that these records must be maintained for at least 5 years after these reports are filed.

Confirm that all officers or employees (in unions with property and annual receipts greater than $5,000) who handle funds are bonded for at least 10% of the funds handled during the previous year to ensure against losses due to fraudulent or dishonest acts. If not, suggest that the principal financial officer contact your parent body or OLMS for assistance.

Determine whether your union made any loans to its officers or employees during the audit period or had any such loans outstanding during the audit period. If any loan exceeded $2,000 at any time, advise the principal financial officers that this is prohibited by the LMRDA and that appropriate repayments should be sought.

Audit Report

Meet with the other Trustees to discuss the overall findings, to confirm that all audit steps have been completed, and to determine whether any unresolved issues remain. |

|

Develop recommendations for improving compliance with the LMRDA’s provisions for financial reporting, recordkeeping, bonding, and loans, and adherence with sound internal financial controls and parent body financial practices and procedures. |

|

Meet with the principal financial officers of your organization to discuss your findings, resolve any remaining concerns, and request consideration for your recommendations. |

|

Prepare an audit report which includes summary information about the completion of the 10-step audit, a brief statement of the financial condition of your union, and any related issues or recommendations. |

|

Present the audit report to your Executive Board and membership, as appropriate, and respond to any questions. |

|

Submit your audit report to your union’s parent body, if required. |

OLMS Assistance

Additional information about the Labor-Management Reporting and Disclosure Act or the Civil Service Reform Act may be obtained from OLMS field offices.

Like any organization, your union must spend money to operate. Most unions have a checking account which is used to make disbursements. Typical disbursements from your union’s checking account might include payments for per capita taxes, hall rentals, office supplies, and lost time to officers. Members expect that when their union spends money it will be for legitimate union purposes and that these expenditures will be properly authorized. Documents, such as your union’s constitution, minutes of meetings, bills, and vouchers, will help you determine why disbursements were made and whether they were authorized by your membership in accordance with your constitution and bylaws. Confirming that established disbursement practices are being followed is essential to ensuring that your union’s funds are being handled responsibly on behalf of all members. Audit Steps 1 and 2 are designed to provide a simple but effective method for examining your local’s disbursements. They will assist you in determining whether payments were for approved, legitimate union business. In addition, they will enable you to determine if payments were properly recorded in your union’s records, allowing for accurate financial reporting to the members of your union, your parent body, and various government agencies. To complete Audit Steps 1 and 2, as well as any optional steps you may select, you will need the following for the audit period: bank statements; cancelled checks; disbursements journal (or check stubs if a journal is not maintained); minutes of membership and Executive Board meetings; and all documents in support of disbursements such as bills, invoices, and vouchers. In addition, you will need any financial forms provided by your parent body. First-time Trustees may want to review the References “Understanding Union Financial Records” and “Union Financial Definitions” at the end of this Guide before beginning Audit Steps 1 and 2.

Trace Cancelled Checks to the Bank Statements and Disbursements Journal By completing Audit Step 1 you should be able to confirm the reliability and completeness of your union’s disbursements records.

If no discrepancies are noted during Audit Step 1, proceed to the next step. However, if you find any questionable items or have some areas of concern, refer to “Common Problems and Solutions” and “Significant Discrepancies” at the end of this chapter.