UI PERFORMS

CY 1998 Annual Report

U.S. Department of Labor

Employment and Training Administration

Unemployment Insurance Service

August 1999

Material contained in this publication is in the public domain and may be reproduced, fully or partially, without permission of the Federal Government. Source credit is requested but not required. Permission is required only to reproduce and copyright material contained herein.

This material will be made available to sensory impaired individuals upon

request.

Voice phone: 202-219-7664

TDD* phone 1-800-326-2577

*Telecommunications Device for the Deaf.

Alexis M. Herman, Secretary

Employment and Training Administration

Raymond Bramucci, Assistant Secretary

Unemployment Insurance Service

Grace A. Kilbane, Director

August 1999

This CY 1998 report is the second comprehensive UI PERFORMS Annual Report. It is intended to give a representative overview of Unemployment Insurance operational performance during the 12 months ending December 31, 1998. Thus, it presents the results of key indicators of the full range of UI operational performanceóbenefits, appeals, tax and cash management. At various times, the Department may supplement this report with reports in greater depth on individual areas, or present the same material using a different format.

UI PERFORMS

UI PERFORMS is the umbrella term adopted to designate the Departmentís closed-loop system for promoting continuous improvement in UI operational performance. The goal of UI PERFORMS is to ensure that the systemís ultimate customersóUI beneficiaries and subject employersóreceive ever-increasing quality of services. Key elements of the enhanced system are a revised set of performance objectives, developed in partnership with the States, for which the Department and the States will be held accountable; increased validation of data reported; and revitalized performance planning and improvement processes. In 1996, UIS began efforts to revise and enhance the various components of this closed-loop system as part of the UI PERFORMS initiative. The Department realized it would take several years to implement all changes envisioned; therefore, it phased in changes to the various components as they were completed. Most initial efforts focused on implementing or changing the systemís three principal performance measurement modules. These are the Tax Performance System (TPS) which assesses the timeliness, completeness and accuracy of tax processing operations; the Benefit Accuracy Measurement (BAM) program which assesses accuracy of benefit payments and eventually decisions to deny; and Benefits Timeliness and Accuracy (BTQ) which embraces measurements of the timeliness and quality of benefit claims, payment and appeals operations. The performance indicators in this report are drawn from those systems plus the report on Benefit Payment Control activities.

To assess the state of performance and promote continuous improvement, the two advisory groups which have developed and guided the implementation of the UI PERFORMS system identified over 50 key performance measures. They designated ten of the most important of these as "Tier I" measures and instructed the Department to establish uniform national criteria for them representing minimally acceptable performance. States performing below a criterion would be required to include a corrective action plan in their annual State Quality Service Plan. Persistent performance below a criterion could result in various actions by the Department including the withholding of administrative grants. Because these measures have national criteria, the Tier I measures must be measured consistently and have comparable meanings in all States.

In the fall of 1998 the Department asked the UI system and its stakeholders to comment on nine of the original ten measures, and the national criteria identifying minimally acceptable performance. (See Unemployment Insurance Program Letter (UIPL) 4-99 and Federal Register Notice 63 FR 63544, November 20, 1998). The Department deferred seeking comment on the tenth measure, timeliness of depositing tax contributions into the Clearing Account, until some States could resolve measurement inconsistencies. In the spring of 1999, the Department promulgated the final Tier I measures and their associated criteria by UIPL and Federal Register Notice. Table 1, on page 5, lists the measures, their criteria, and when they become effective. This report includes every Stateís performance on all nine Tier I measures.

For a variety of reasons, the new measures and criteria become effective at various times between the date of issuance of the UIPL and Fiscal Year 2005. The measures and criteria now used to implement the Secretaryís Standards for Initial Claims timeliness and Lower Authority Appeals timeliness cannot be changed until the new UI PERFORMS regulation supersedes the regulations in which they are embodied. Some criteria are being delayed to give States time to raise performance, which is now considerably below the criteria in many States, or to work out measurement irregularities.

The UIPL which implements the new UI PERFORMS Tier I measures also identifies the so-called Tier II performance measures. Although many Tier II measures cover dimensions of performance as significant as Tier I measures, States may differ enough in these areas that the measures have varying meanings from one State to another. Thus, the Department will issue no national criteria for these measures. Instead, the States and the ETA Regional Offices will negotiate performance targets for those being emphasized in the current State Quality Service Plan (SQSP). Many of the performance measures included in this report are Tier II measures. Appendix B lists the complete set of Tier II measures. This report includes State performance on about a third of the Tier II measures.

THE MAIN UNEMPLOYMENT INSURANCE MEASUREMENT SYSTEMS

Most of the UI performance measures use data from one of three measurement subsystems: Benefits Timeliness and Quality, Benefit Accuracy Measurement, and Tax Performance System. These were all developed to give a fuller view of State performance and thus better to permit the Department to exercise its role as a partner in ensuring that claimants and employers receive high-quality UI services.

The Department of Labor, Employment and Training Administration (ETA), Unemployment Insurance Service (UIS) has the responsibility by law, as mandated in Title III of the Social Security Act, for assuring that State Employment Security Agencies (SESAs) operate an effective and efficient unemployment insurance program. Various provisions of Federal law require that certain UI activities be performed promptly and accurately. Section 303(a)(1) of the Social Security Act requires, as a condition of a State's receiving UI administrative grants, "[s]uch methods of administration. . .as are found by the Secretary of Labor to be reasonably calculated to insure full payment of unemployment compensation when due."

| TABLE 1 TIER I MEASURES | Criterion | |||

|---|---|---|---|---|

| Present | FY 2000 | FY 2002 SQSP or New Reg |

FY 2005 | |

| First Payment Timeliness | ||||

| % of 1st Payments within 14/21 days: IntraState UI, full weeks | 87 | 87 | ||

| % of 1st Payments within 35 days: IntraState UI, full weeks | 93 | 93 | ||

| % of 1st Payments within 14/21 days: InterState UI, full weeks | 70 | 70 | ||

| % of 1st Payments within 35 days: InterState UI, full weeks | 78 | 78 | ||

| % of 1st Payments within 14/21 days: Intra + Inter State UI, UCFE, UCX Programs, full + partial weeks |

90 | 90 | ||

| % of 1st Payments within 35 days: Intra + Inter State UI, UCFE, UCX Programs, full + partial weeks |

95 | 95 | ||

| Nonmonetary Determinations | ||||

| % of Separation Issues determined within 21 days of Detection Date (Intra + Inter State UI, UCFE, UCX) |

80 | 80 | ||

| % of Nonseparation Issues determined within 14 days of Detection Date (Intra + Inter State UI, UCFE, UCX) |

80 | 80 | ||

| % of Separation and Nonseparation Determinations with Quality Scores >80 points | 75 | 75 | ||

| Appeals | ||||

| % of Lower Authority Appeals decided within 30 Days of Filing | 60 | 60 | 60 | 60 |

| % of Lower Authority Appeals decided within 45 Days of Filing | 80 | 80 | 85 | 85 |

| % of Lower Authority Appeals decided within 90 Days of Filing | 95 | 95 | ||

| % of Higher Authority Appeals decided within 45 Days of Filing | 50 | 50 | 50 | |

| % of Higher Authority Appeals decided within 75 Days of Filing | 80 | 80 | 80 | |

| % of Higher Authority Appeals decided within 150 Days of Filing | 95 | 95 | 95 | |

| % of Lower Authority Appeals with Quality Scores at least 85% of potential points |

80 | 80 | 80 | |

| Tax/Cash Management | ||||

| % of New Status Determinations within 90 days of Quarter End Date | 60 | 60 | 60 | |

| % of New Status Determinations within 180 days of Quarter End Date | 80 | 80 | 80 | |

| Acceptance Sample for Accuracy of 60 New Status Determinations --Pass with No More than 6 Failed Cases |

Pass | Pass | ||

| Days Worth of Deposits in Clearing Account before Transfer to UTF | <= 2 | |||

| Ratio of average daily loanable balance in Clearing Account to Avg. daily Transfer to UT |

<= 1.75 | <= 1.0 | ||

The UI PERFORMS measures computed using data from the BTQ, BAM, TPS and other administrative data systems represent the Departmentís continuing effort to provide ever more accurate and useful information on the functioning of all UI program activities. These systems are designed and managed with certain considerations in mind, primarily:

Benefit Accuracy Measurement System

The UI Benefit Accuracy Measurement (BAM) program, formerly Benefits Quality Control (BQC), became mandatory in the fifty States, the District of Columbia, and Puerto Rico on October 5, 1987, for operation in calendar year (CY) 1988. This is the eleventh year for which calendar year data from the program have been published.

BAM is a diagnostic tool used to identify payment errors and measure the effect of previously initiated corrective actions. BAM is based on random samples of UI payments. The sampling procedures are designed to produce samples that are representative of a State's universe of paid UI claims. Each sample represents one compensated week of benefits. Each case in the sample is thoroughly reviewed for compliance with the State's UI laws, regulations, policies, and operating procedures. BAMís premise is that dollars overpaid and underpaid can be estimated by projecting the results from a State's BAM sample to its entire population of payments. The BAM program gathers information to assist States in developing program improvement plans to correct problems in their UI benefit payment systems and to enable them to measure the effects of implementing those plans. States also use this information in implementing policies to ensure accurate administration of their laws, regulations, and operating procedures.

The Department has one overriding goal for BAM: to ensure that the UI program operates with the highest degree of accuracy attainable within available administrative resources. The BAM methodology is a sound means for measuring the accuracy of State UI administration, and thus, BAM is an integral part of the Secretary's oversight system. It is the major vehicle by which the Department oversees the accuracy of State UI benefit payments.

Readers are strongly cautioned that it may be misleading to c ompare one State ís BAM overpayment and underpayment rates with those of other States. No two Statesí written laws, regulations, or policies specifying eligibility conditions are identical, and differences in these conditions influence the potential for error. States with stringent, complex provisions will tend to have higher overpayment rates than those with simpler, more straightforward provisions, for example.

Program Development. The basic concept of intensive investigations of small but representative samples of cases was first applied to UI in the late 1970s. A National Commission on Unemployment Compensation (NCUC) study in six metropolitan areas revealed that the "true error rate" of UI payments in the test sites was several times higher than that reported by the measurement systems then in place. One important conclusion was that field verifications must supplement desk reviews to accurately estimate the UI payment error rate. The Department applied the approach, now called Random Audit (RA), at the State level and by 1984, 46 States operated RA programs.

In the summer of 1983, an Interagency Benefit Payment Oversight Committee reviewed the findings from RA and other systems for measuring and correcting payment errors in the UI system and recommended that the Department establish a UI Quality Control program. After developmental work and policy review, most States began implementing the Benefits Quality Control (BQC) program on a voluntary basis in April 1986. The BQC program was established by regulation on September 3, 1987.

In July 1993, following a period of pilot testing, States were permitted to conduct certain portions of the field verifications by mail, telephone and fax instead of in person. In 1996, the Department began implementing other changes to BAM recommended by the Performance Enhancement Workgroup (PEWG). The programís name was changed to Benefit Accuracy Measurement from Benefits Quality Control, and States no longer were required to release their annual error rates to the public media. On January 1, 1997, allocated annual sample sizes were reduced to 360 in the ten smallest States and 480 in the rest, and States were given the option of conducting all aspects of verifications by mail, phone and fax. The Department also began designing a pilot test of the use of the BAM methodology to determine the accuracy of decisions denying eligibility.

Program Scope. BAM covers the three largest permanently authorized unemployment compensation (UC) programs: regular State UI (including benefits paid on the basis of combining wages), the federally-funded Unemployment Compensation for Federal Employees, and Unemployment Compensation for Ex-service members. Together, these programs accounted for 92.8% of benefit outlays in CY 1997. The BAM sample does not include UC benefits paid under Trade Adjustment Assistance, Disaster Unemployment Assistance, the interstate arrangement, or any Federal extended benefits program.

Although denied claims and appeals are not directly investigated, the BAM universe includes approximately 86% of all decisions. BAM covers monetary, separation, and nonmonetary/nonseparation issues which affect the claimant's eligibility for benefits but directly samples only those which the agency decided to pay. The BAM underpayment rate is based on payments which are less than the amount the claimant should have received. BAM underestimates the underpayment rate because erroneously denied claims are not identified. A successful 5-State pilot test of applying the BAM methodology to measuring denied claim accuracy (including claims filed on an interstate basis) concluded in September 1998. The Department intends to include some denial decisions in the BAM program in 2000. The quality, including the accuracy, of benefit appeal decisions is reviewed and assessed quarterly under the BTQ system. There is no plan to incorporate appeal decisions into BAM.

CY 1998 Sample Size. The States received sufficient resources to investigate a total of 23,760 cases in CY 1998. Individual State sample sizes varied, with the ten smallest States receiving resources to investigate a sample of 360, and the 42 larger States receiving resources to investigate a sample of 480, cases per year. Some States chose to draw larger samples, and 26,353 cases were completed in CY 1998, an average of 507 cases per State.

Data Collected. BAM investigators compile a data record on each case consisting of up to 116 required elements and any additional elements defined and collected at each State's discretion. Since all States have computerized records on weeks compensated, many of the data elements can be transferred from the stateís mainframe database directly to the BAM computer record at the time the case is selected for investigation. This both reduces coding time and minimizes coding and data entry errors.

Most elements pertain directly to UI eligibility, relating to the claimantís benefit history, base period work, monetary eligibility, reason for separation, ability to work, availability for work, and work search effort. Data on age, sex, and ethnic classification are gathered to verify the representativeness of the BAM samples. The data record concludes with elements related to error classification, including type of error (if any), amount of error, the responsible party, the cause, and the point of detection. Multiple errors can be detected in the course of one BAM case investigation and documented in the database.

The Department provides each State with computer hardware and software to store, retrieve, and analyze its own BAM data. States also have received remote terminals, printers, and modems so that outstationed investigators can enter case information directly in the BAM computer record.

Data Collection Methodology. The BAM investigator obtains information pertaining to the monetary, separation, and continuing eligibility issues for the payment selected, and various claimant characteristics. This is done through in-person and telephone contacts with the claimant, various employers, and third parties such as labor unions and employment agencies identified by the claimant. This information is compared to agency records to determine its impact on the accuracy of the payment received by the claimant. The BAM investigation also determines whether decisions conformed to State law, policy, and procedures.

Benefits Timeliness and Quality

Development. The existing Benefits Timeliness and Quality (BTQ) measurement suite is a lineal descendent of the Quality Appraisal measures. These were initially developed in 1975 by a Federal-State task force. It developed a comprehensive system called the Performance Appraisal Package after considering all existing performance and promptness measures.

The Performance Appraisal consisted of three measurement systems: "A Performance Based Quality Control Program for Nonmonetary Adjudication" (known as QPI), the Appeals Quality Package, and portions of a State UI Self Appraisal. The results of the new appraisals were reviewed by the National Office together with States and Regional Offices, and Desired Levels of Achievement (DLAs) were established for many of the activities reviewed. DLAs were first established for Fiscal Year 1978 and were revised along with the evaluation package, which was renamed "UI Quality Appraisal" in 1979. The DLAs were used to supplement the Secretary's Standards to measure the quality of State operations. Secretary's Standards are mandated in two areas: timeliness of processing lower authority appeals (20 CFR 650) and timeliness of intrastate and interstate first benefit payments (20 CFR Part 640).

The results of the UI Quality Appraisal of all major UI State program activities, reviewed by Regional and National Offices, were distributed to each State to be used in the State Annual Program and Budget Plan (PBP). The data also were published in a UI Quality Appraisal annual report. This mode of presentation served more than one purpose. It indicated levels of performance, absolutely and relative to other States, and by giving performance relative to Secretary's Standards or DLAs it also served as the document of record for determining whether corrective actions plans had to be included in the annual Program Budget Plan submitted by each State.

Because technological changes in SESA operations had made new systems of oversight both possible and necessary, the Department of Labor (DOL) initiated the Performance Measurement Review (PMR) project in 1988 to review and improve the Quality Appraisal measures. The QA process had not been subjected to in-depth review since the mid-1970's. Increasing use of automated and electronic systems, and other operational changes, had transformed the delivery of UI services to the public.

PMR was designed and completed in three phases. The first phase consisted of the analysis of existing benefits time lapse and quality measures to determine their legislative basis and to identify gaps or overlaps in measurement areas, the development of new or revised measures, and the design for a field test of selected measures. State and Federal UI representatives carefully defined time lapse measures and quality measures covering benefit payments, nonmonetary determinations, and lower and higher authority appeals.

In the second phase of the project, six States conducted a 15-month field test of reporting data for the time lapse and quality measures. The evaluation showed that the new measures and the software developed for analysis of results could yield meaningful and statistically valid information in a cost-effective manner.

The third phase involved nationwide implementation of the new benefits time lapse and quality measures as a part of the new closed-loop management system, UI PERFORMS, which was implemented in UI in 1996. The nonmonetary promptness measure, implemented using the detection date of an issue on a claim as the starting point, was not field tested, but was included for implementation at the recommendation of the State-Federal Performance Enhancement Work Group after completion of the field test.

The new measures were embodied in a new "9050" series of reports. These new reports required programming changes in every State to allow reporting of all the measures with their new definitions and new intervals. State implementation of BTQ began with the quality reviews of nonmonetary determinations and lower authority appeals. After creating the universes for sampling, they drew the first samples in October 1996 for the quarter ending September 30, 1996. In January 1997 States began collecting the data from which the timeliness measures are calculated.

Changes in Reporting for Timeliness. The new timeliness measures incorporate changes designed to improve performance measurement in several ways.

Changes in Quality Assessment. Measures based on samples are used to track the quality of SESA nonmonetary determinations and lower authority appeals. The BTQ system made the following changes designed to improve overall assessment:

Benefit Payment Control

The PMR initiative was originally intended to review Benefit Payment Control (BPC) measures, but they were deferred in Phase I. In 1996, a Federal-State workgroup developed 10 measures which were field-tested in three States. In 1998, the UIS circulated two of the tested measures for comment to the UI system but neither received strong support. Until revised measures are implemented, the Department will continue to report the BPC measures for which the Quality Appraisal system specified DLAs. These are the proportions of both fraud and nonfraud overpayments established in the current period which the agency collected.

Tax Peformance System

Development. The Department developed the Tax Performance System (TPS) to assist in exercising its general oversight responsibilities toward the UI program and to help meet its responsibility to protect and maintain the soundness of the Unemployment Trust Fund. At the time the Department began the development of the Benefits Quality Control (BQC) program in 1983, tax oversight consisted principally of review of data reported on the ETA 581 (Contribution Operations) report and periodic program reviews, and reviews of Trust Fund operations. The annual Quality Appraisal Results included indicators for which DLAs had been set: Status Determinations Promptness; Field Audit Penetration; Report Delinquency; Collections Promptness; Promptness of Deposit to the Clearing Account; and two Trust Fund deposit transfer timeliness measures. There was also a measure of field audit performance with no DLA. The long-term Quality Control program design envisioned a tax component.

In 1988 a Revenue Quality Control (RQC) Task Force comprising a small Federal staff assisted by State tax specialists was established to design a quality control program for tax operations. In 1990, the basic system, called Core RQC, was pretested in eight States. In the next two years, eight other States formally pilot tested the RQC approach. In 1993, 49 States began implementing the RQC design voluntarily. Mandatory implementation began in 1995 with changes to the form ETA 581, to obtain data needed for the new Computed Measures. All States implemented all aspects of RQC in January 1996. RQC was later renamed the Tax Performance System.

Methodology. The TPS approach divides tax operation into major functional components. For each function, it specifies key performance objectives based on three basic dimensions of quality: timeliness, accuracy, and completeness. There are performance indicators to measure the attainment of each objective. Measures and review techniques were selected to emphasize quality, cost-effectiveness, and reliance on data obtained as a by-product of ongoing program operations. Because TPS was designed to provide information which tax units can use directly to guide program improvement, it also seeks to gather and disseminate information on best practices in addition to methods for identifying weaknesses. The complete TPS "package" has three assessment components: (1) for timeliness and completeness, Computed Measures; (2) for accuracy, Program Reviews; and (3) to identify best practices, Methods Surveys.

Table 2 shows the methodologies used to review the various tax functions. The combination of Computed Measures, System Reviews, Acceptance Samples, and Methods Surveys is shown in detail to present a well-rounded assessment of each function.

Timeliness and Completeness. Most of the information on timeliness and completeness of UI tax functions were taken from program data obtained from the key tax report, ETA 581. These indices are termed "Computed Measures". The ETA 581 report was revised to ensure that States collected the data for calculating the computed measures.

Accuracy. The Benefits Quality Control model for measuring accuracyóreviewing large samples of end products was found to be expensive and difficult to apply in the tax environment. Instead, a two-step methodology based on financial and program audits was developed, which TPS terms Program Review.

TABLE 2

REVIEW METHODOLOGIES

| TAX FUNCTION | COMPUTED MEASURES |

PROGRAM REVIEW Sys Rev & Sampling |

METHODS SURVEY |

|---|---|---|---|

| STATUS DETERMINATION | X | X | X |

| CASHIERING | X | ||

| REPORT DELINQUENCY | X | X | X |

| COLLECTIONS | X | X | X |

| FIELD AUDIT | X | X | X |

| ACCOUNT MAINTENANCE | X |

The combination of a thorough front-end review and a small acceptance sample efficiently establishes a reasonable assurance of accuracy, directly identifies any areas of program weakness, and immediately indicates where program improvements are needed. If there is a need to know the actual level of a particular tax function's problem, the Acceptance Sample can be readily expanded into a much larger Estimation Sample.

Best Practices. To identify best practices in several tax functions, TPS has designed Methods Surveys. States are required to complete these†every four years. Plans are underway to compile and distribute information on best practices to States and Regions.

This Tax Performance System section of the UI PERFORMS Annual Report for CY 1998 presents only data from the Computed Measures and Acceptance Samples because the System Reviews' examination of State internal controls contains too much detail to present in a brief format without distortion. In addition, Systems Reviews are intended largely to guide State program and Regional staff. Data from Methods Surveys will be compiled and analyzed later, as the necessary programming is delayed because of year 2000 priorities. However, the combination of Computed Measures and Acceptance Sample results provides a concise overview of the quality of State tax operations.

This chapter is divided into three main sections. The first section presents a brief overview of the recent economic conditions and the resultant movement in certain UI tax and benefit activities. The second shows the movement of major benefit payment activities and then reviews the national pattern of selected key benefit payment performance indicators. The third section approaches tax activities in the same way.

ECONOMIC ACTIVITY AND MAJOR PROGRAM ACTIVITIES

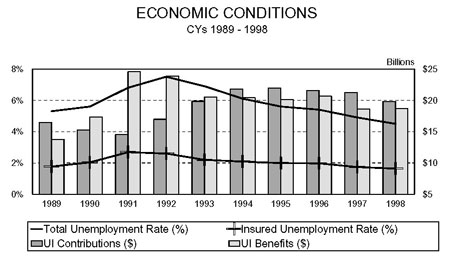

The labor market in 1998 achieved levels of tightness not seen for some three decades, as the total unemployment rate fell to an average of 4.5% and the insured unemployment rate (IUR) to 1.6%. The total unemployment rate has been declining steadily since the most recent recession high of 7.5% in 1992.

The movement in the IUR, which peaked in 1991, has been less pronounced. The peak in the IUR coincides with the peak in benefit payments in 1991 at nearly $25 billion. Benefit payments have since fallen to about $19 billion in 1998. Contributions, on the other hand, reached their 10-year low in 1991 at about $14 billion and rose to a high of over $22 billion in 1994 and 1995 before dropping to under $20 billion in 1998.

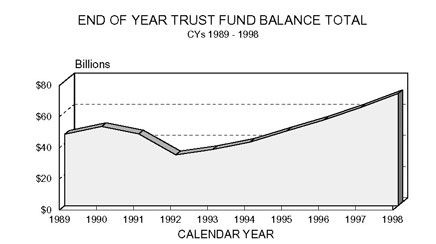

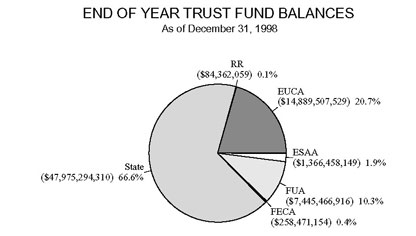

December 31 trust fund balances have risen steadily since their decade low in 1992 as States took advantage of improving conditions to replenish their funds. On December 31, 1998, balances in the UI trust fund reached $72 Billion. Of this, State accounts constituted two thirds and the Extended Unemployment Compensation Account (EUCA) one fifth.

The cost of administering the UI program is expressed as cents per dollar of benefits paid or of taxes collected. Tax activity tends to vary little over the business cycle and hence the cost is quite stable. Benefit payment levels fluctuate much more widely over the cycle than the funds States receive to administer them, causing the benefit cost to vary inversely with the economic cycle.

BENEFIT PAYMENT ACTIVITY

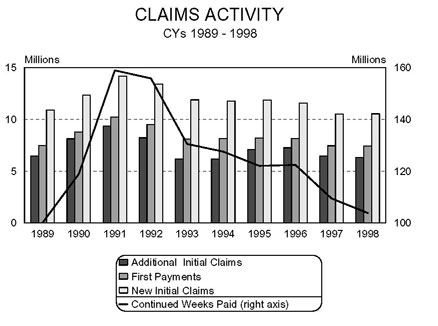

In 1998, unemployment insurance offices handled approximately 11 million new initial claims under the regular State UI, UCFE, and UCX programs. Approximately 4 million claimants were determined to be ineligible for monetary or separation reasons, or found new jobs before filing a first week claimed, so that ultimately about 7 million claimants actually received a first payment. This compares with the 14 million new initial claims filed, and 9 million first payments made, in the recession year 1991. Additional initial claims, over the same period, track first payments closely because they represent occasions when claimantsí benefit payment series were broken by intervening spells of employment. Each additional initial claim filed to resume benefit payments requires the agency to review the reason for separation (but not the monetary eligibility) and may lead to the identification and adjudication of a separation issue.

More striking than the movement in initial claims has been the path of continued weeks claimed. Continued weeks claims depend both on the number of first payments and on the average number of claims filed per benefit year, also called the "average duration."

Economic conditions drive both components of weeks claimed. After reaching a high of 160 million weeks during 1991, the number has fallen sharply to about 105 million in 1998. The great majority of claims filed, and payments made, in any year are intrastate made under the regular State UI program. Table 3 indicates the relative magnitudes of both first payment and continued weeks paid by program in 1998. Overall, interstate claims (State, UCFE, and UCX) constitute only about 3% of all first payments and about 4% of continued weeks paid.

The regular State UI first payments are about 98.7% of the total, UCFE 0.7%, and UCX the remaining 0.6%. About one eighth of first payments, and one twelfth of continued payments, were made for partial and part-total weeks claimed. These shares differ little from one year to the next.

TABLE 3

| FIRST PAYMENTS WORKLOAD | CONTINUED WEEKS PAID WORKLOAD | |||||

|---|---|---|---|---|---|---|

| FULL | PARTIAL | TOTAL | FULL | PARTIAL | TOTAL | |

| INTERSTATE | 208,564 | 12,557 | 221,121 | 3,592,109 | 187,502 | 3,779,611 |

| - STATE UI | 203,625 | 12,366 | 215,991 | 3,476,066 | 179,883 | 3,655,949 |

| - UCFE | 3,748 | 123 | 3,871 | 68,436 | 4,361 | 72,797 |

| - UCX | 1,191 | 68 | 1,259 | 47,607 | 3,258 | 50,865 |

| INTRASTATE | 6,048,157 | 882,690 | 6,930,847 | 81,399,198 | 7,386,244 | 88,785,442 |

| - STATE UI | 5,964,276 | 877,237 | 6,841,513 | 80,066,492 | 7,289,670 | 87,356,162 |

| - UCFE | 41,760 | 3,159 | 44,919 | 735,249 | 55,961 | 791,210 |

| - UCX | 42,121 | 2,294 | 44,415 | 597,457 | 40,613 | 638,070 |

| TOTALS | 6,256,721 | 895,247 | 7,151,968 | 84,991,307 | 7,573,746 | 92,565,053 |

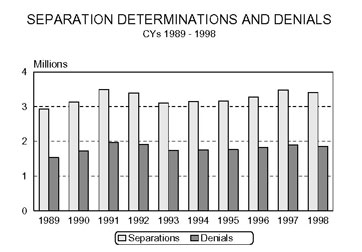

Although separation and nonseparation determinations both follow economic conditions, the relationship to their underlying claims series is not constant. Separation determinations are driven by the combination of new and additional initial claims. Although those claims have fallen since 1995, the number of separation issues adjudicated was actually higher in 1998 than in 1995. The reason is probably to be found in the fact that in good economic times, "clean" lackof- work claims are a smaller proportion of total claims than in recessions.

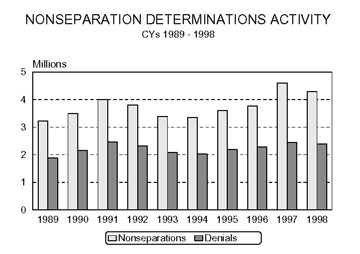

The same general pattern may be seen for nonseparation determinations, which depend on the number of weeks claimed. Nonseparation determinations declined along with continued weeks claimed from 1991 to 1994 but rose until they hit a peak of over 4.5 million in 1997 despite the continued declines in weeks claimed.

Buoyant economic times give claimants greater opportunities to work while claiming benefits, giving rise to a greater proportion of claims with nonseparation issues.

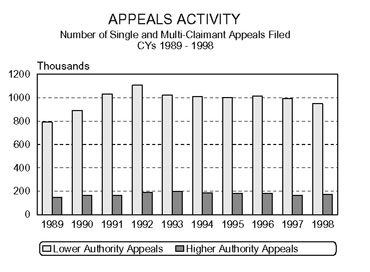

Most appeals are filed by claimants, upon receiving a denial for either separation or nonseparation reasons. Slightly over half of all nonmonetary determinations result in a denial. In 1998, about 4.2 million nonmonetary determinations, 55% of the total, were denied. About one in four (in 1998: 23%) went to a first level appeal, and of those about 18% went to a higher-authority appeal. Since 1991, the number of lower-authority appeals filed has remained quite constant, about one million a year, with only a slight increase to 1.1 million in the recession year 1992 and a slight drop to 950,000 in 1998. Higher authority appeals have displayed a gentle downturn since their peak in 1993.

BENEFIT PAYMENT PERFORMANCE

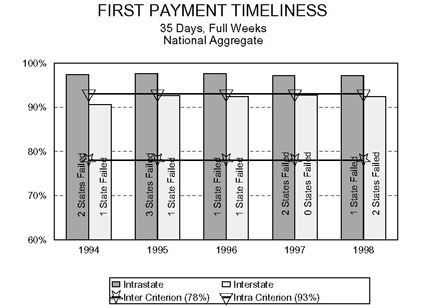

First Payment Timeliness

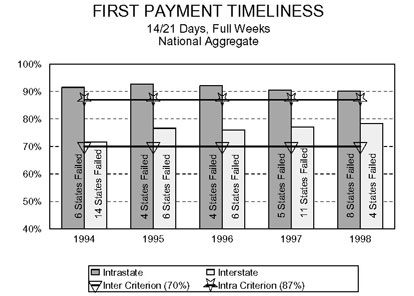

One of the UI systemís flagship measures is first payment time lapse. Criteria, set on a measure of the timeliness of full weeks of unemployment only, have been set to implement Secretaryís Standards for first payments made within 14/21 days and 35 days for both intrastate and interstate payments since 1978. At the 14/21 day level, aggregate timeliness performance reached its peak in 1995 and has drifted down slightly since for intrastate payments, while interstate performance has trended upward.

The charts show that the aggregate performance can be a misleading indicator of the number of States failing to meet the Secretaryís criteria. The number of states missing the criteria fluctuates much more widely than the aggregate.

For 35-day performance, the overall pattern is the same, with intrastate performance trending down slightly since 1995; intrastate performance jumped up from 1994 to 1995 and has been flat since. At both levels, aggregate performance is comfortably above the criteria.

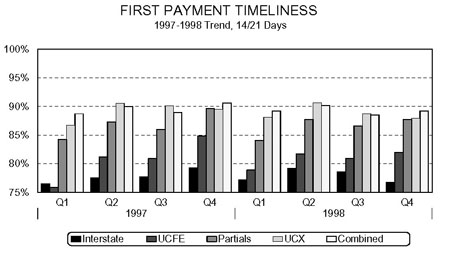

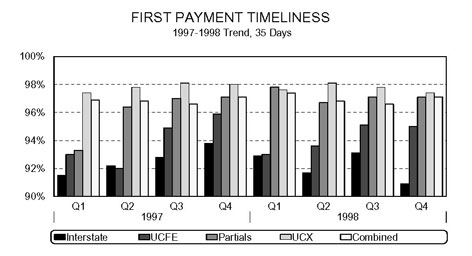

In July 1999 the Department issued the new the UI PERFORMS performance criteria (see introduction for the criteria and their effective dates). New 14/21-day and 35-day criteria based on a combined measure will replace the old criteria illustrated above when the new UI PERFORMS regulation becomes effective. The new measure will combine all first payments for partial as well as full weeks, intrastate and interstate payments, and payments made under the UCFE and UCX programs as well as State UI. The next two charts show 1998 performance under this combined measure, and illustrate the performance of the combined measures's various components other than the dominant intrastate, full weeks, State UI element.

In 1998, aggregate performance under the combined measure was about 5 percentage points below the Secretaryís Standard measure at 14/21 days, pulled down by all its new components. However, the differences are virtually nil at 35 days.

Time lapse performance is highly seasonal. Performance at the 14/21-day level tends to be lowest in the first and third calendar quarters and highest in the second quarter for most components. The second and third quarters tend to be lowest at 35 days.

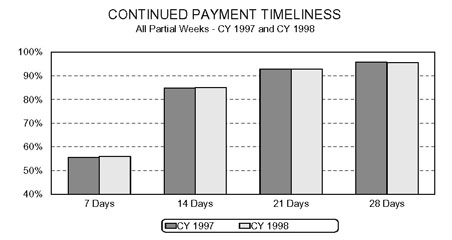

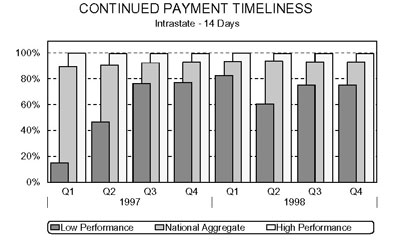

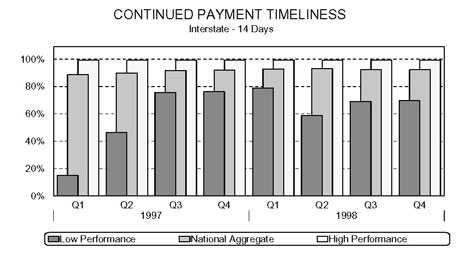

Continued Weeks Timeliness

Overall, States paid over 60% of continued claims within 7 days in 1998, and over 90% within two weeks. Average performance at 7 and 14 days for partial weeks has run about 5 percentage points below the aggregate for the last two years.

In contrast to first payment time lapse, continued weeks payment time lapse has virtually no seasonality. Time lapse performance for both intrastate and interstate payments exhibited a gentle upward trend throughout all the quarters of 1997 and 1998, due apparently to improvements in performance among the worst-performing States.

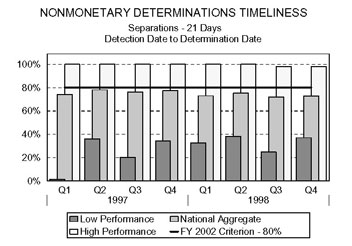

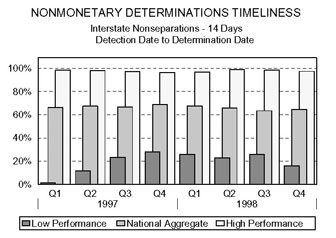

Nonmonetary Determinations Timeliness

Aggregate separation performance--the percent of separation determinations made within 21 days of the date the State detected an issue--lay below the 80% criterion which will go into effect in Fiscal Year 2002.

Aggregate performance was worse during 1998 than 1997 and has trended down each quarters since its peak in 1997:2. It does appear that performance in the worst state is improving, however.

Aggregate performance on the claim interstate component--interstate performance is traditionally lower than intrastate for most measures--is quite similar to the criterioned aggregate measure, except for the worst-performing State, where it is noticeably lower than the aggregate. There is no obvious seasonal pattern to nonmonetary time lapse.

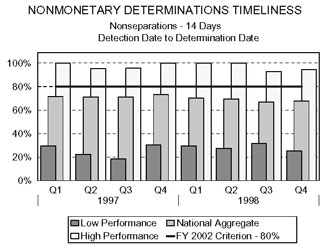

For nonseparation determinations, aggregate performance has run about 10 percentage points below the 80% within 14-day criterion throughout both 1997 and 1998. Like separation time lapse, it has also worsened slightly during 1998. There is about a 60-point difference in performance between the bestand worst-performing State.

As with separations, the performance on interstate nonseparation determinations has declined slightly from 1997 to 1998 and lies slightly below the aggregate measure.

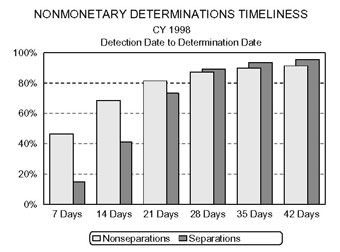

The adjacent chart shows the pattern of decision time lapse for issuing both kinds of determinations at different intervals in 1998. Nearly half of nonseparation issues were decided within the first week after detection, versus only 15% of separations (nearly all separations require obtaining information from employers). The percentage of nonseparation determinations exceeded those for separations at the 14-day interval (the nonsep criterion interval) and 21-day interval (the separation criterion interval). At 28 days and longer, States had issued a higher percentage of separations than nonseparation. By 35 days, they have made more than 90% of both kinds of determinations.

States reported that they detected separation issues much earlier than nonseparation issues in 1998. Over 90% of separation issues were detected within 21 days, whereas by 42 days, they had detected less than 85% of nonseparation issues.

Appeals Timeliness

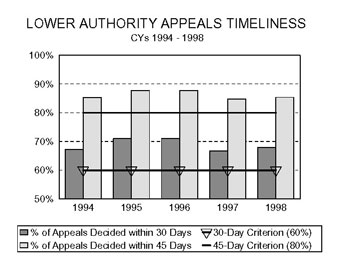

Appeals performance is one of the most cyclically sensitive UI activities and thus has benefited from the decline in unemployment rates. However, the improvement has been reflected much more in the number of States passing the criteria than in the aggregate performance. Throughout the past five years, the aggregate percentage of appeals decided within 30 days rose from 68% in 1994 to about 71% in both 1995 and 1996, but has since dropped to under 70% again.

The percentage of appeals decided within 45 days followed the same pattern so that both series show no trend. The number of States passing the Secretary's criteria shows a down trend more in keeping with the improvement in economic conditions.

The past five years have also shown regular improvement in Higher Authority time lapse. The rise in aggregate time lapse has been accompanied by regular declines in the number of States that would have failed to meet the new Tier I criteria established in 1999.

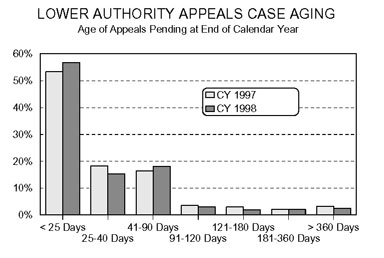

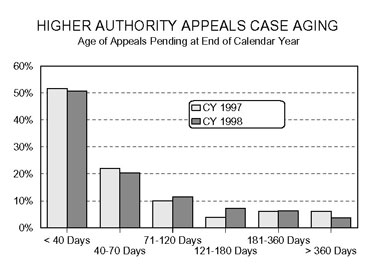

Supplementing the measures of how quickly States decide appeals is the age of undecided or pending appeals at the end of the year. The chart below shows that at the end of 1998, 57% of all undecided Lower Authority appeals had been filed less than 25 days ago (and hence were still likely to be decided within the first time lapse interval of 30 days). Further, this was an improvement over the 53% less than 25 days old at the end of 1997. The percentages of very old (91+ days) undecided appeals also declined slightly between 1997 and 1998.

The pattern is different for Higher Authority Appeals; the shares of appeals still able to meet time lapse (<40 and 40-70 days) rose slightly from 1997 to 1998, with corresponding increases in the shares at all longer age categories except for the last one of >360 days.

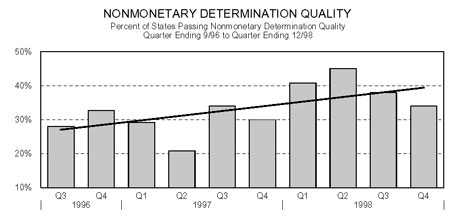

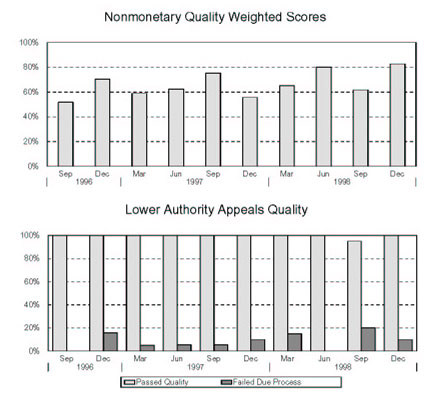

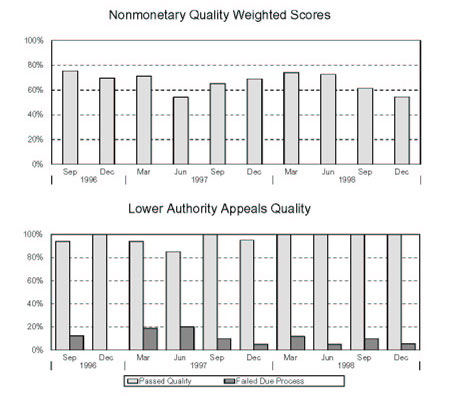

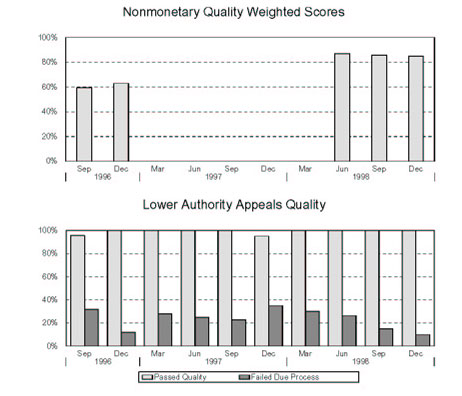

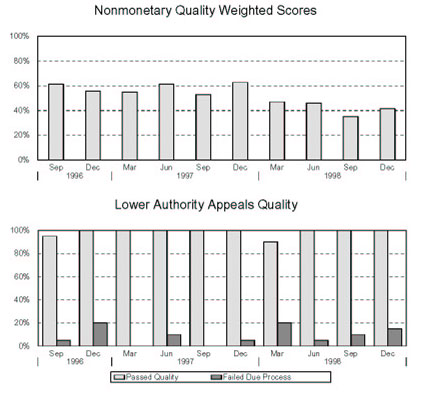

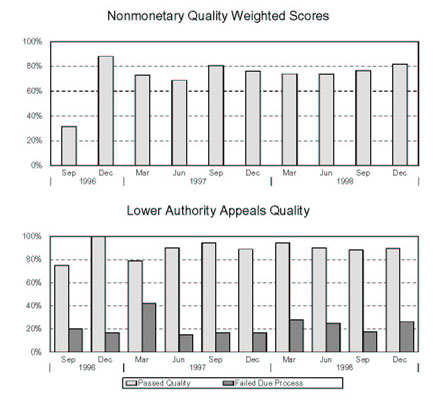

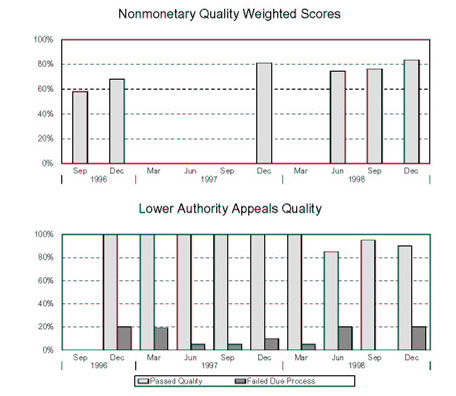

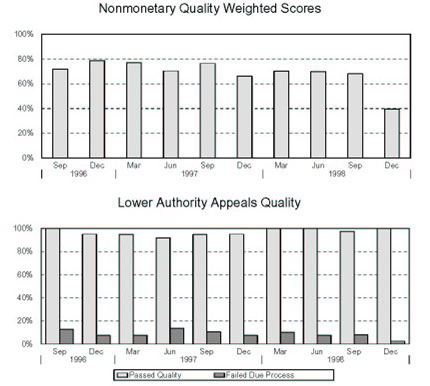

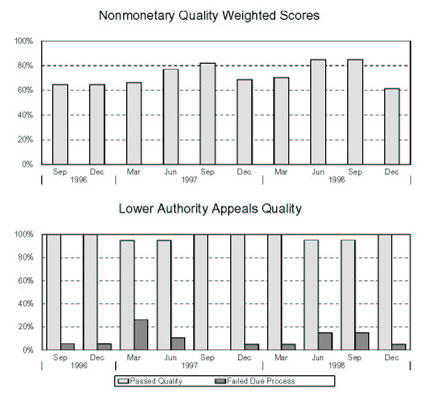

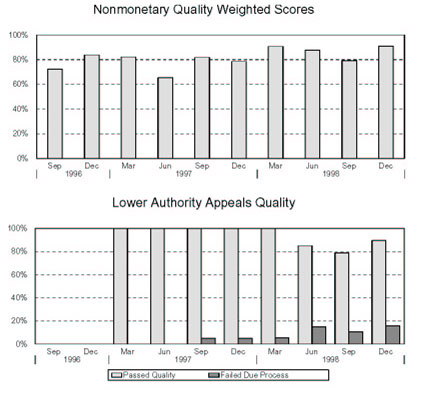

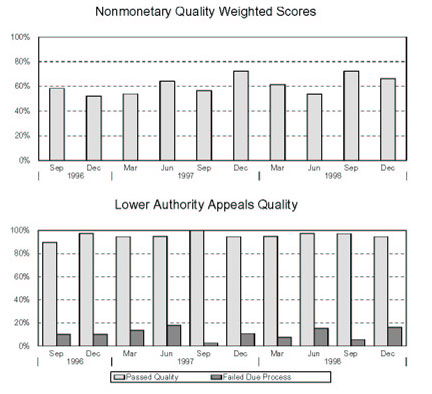

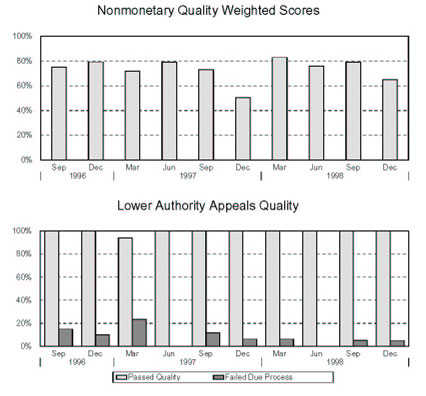

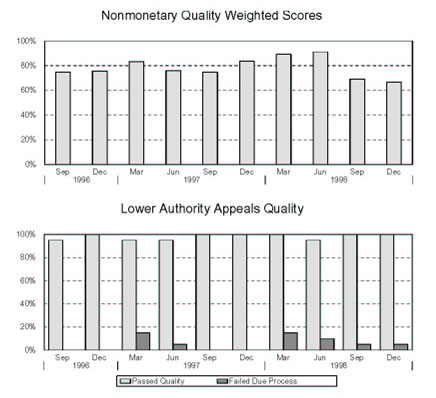

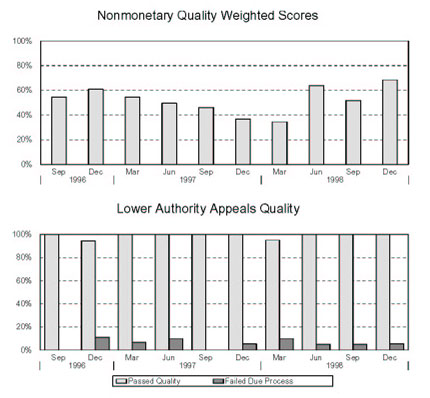

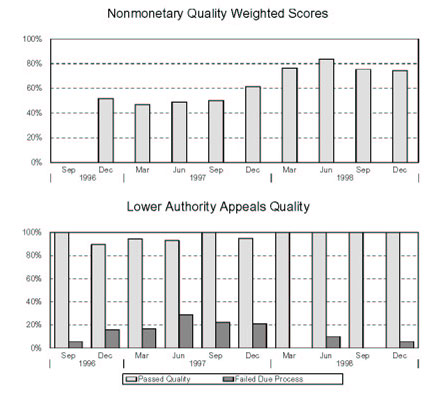

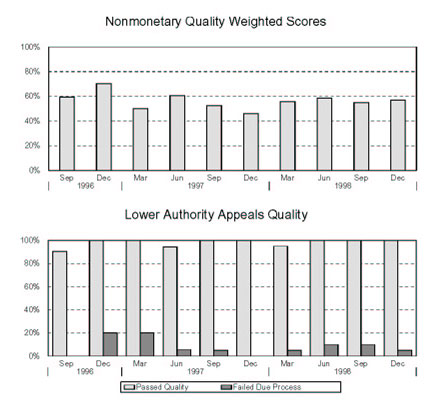

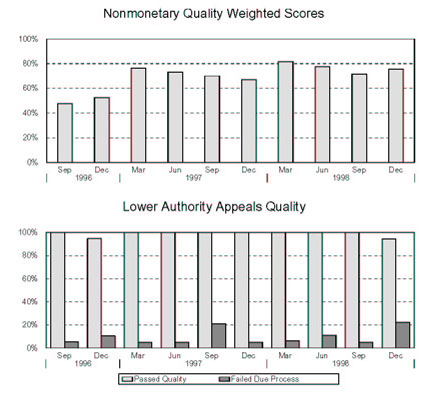

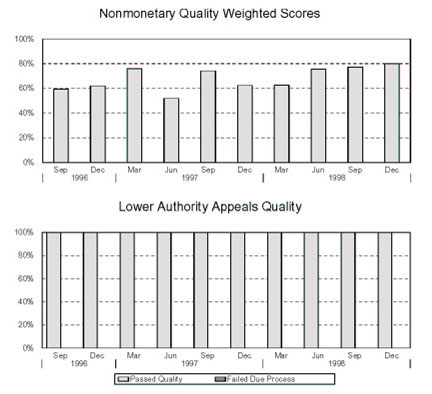

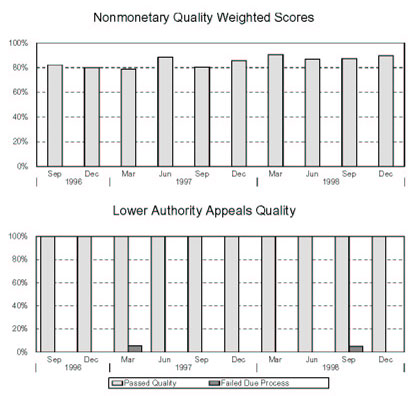

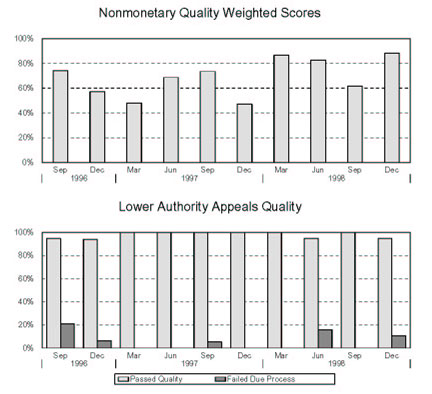

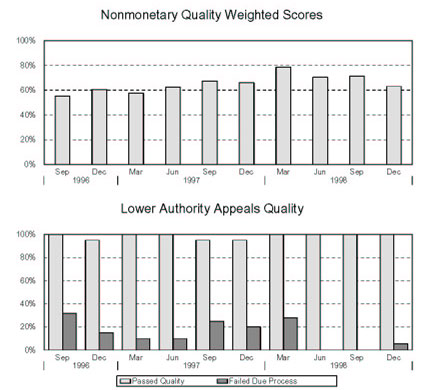

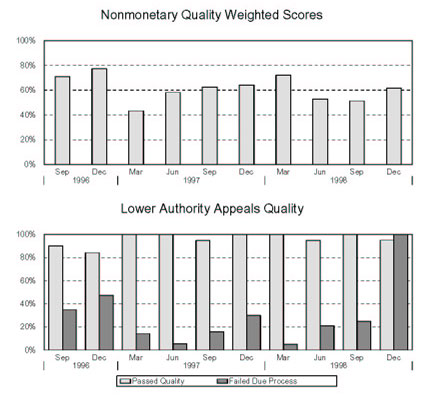

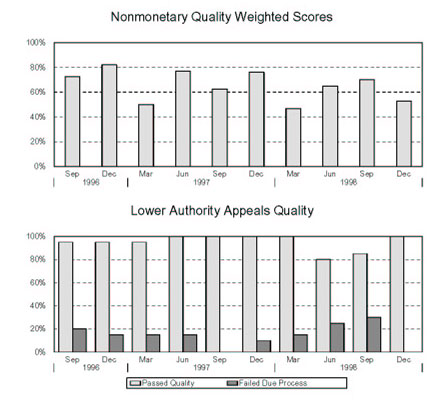

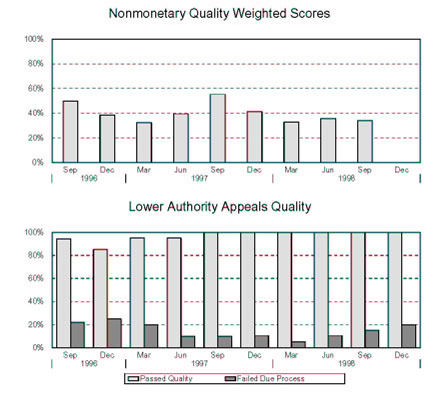

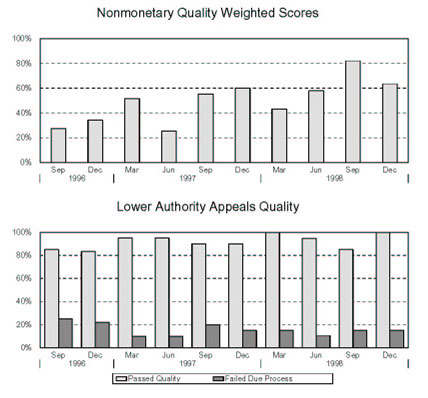

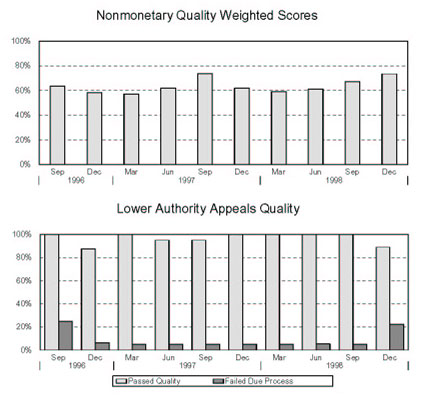

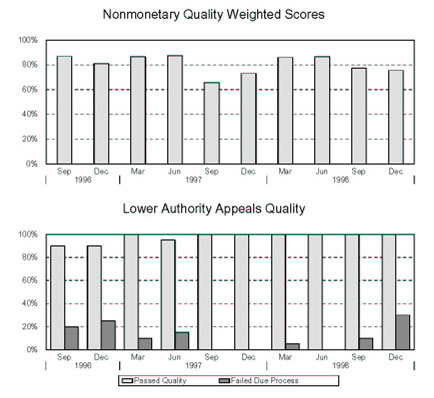

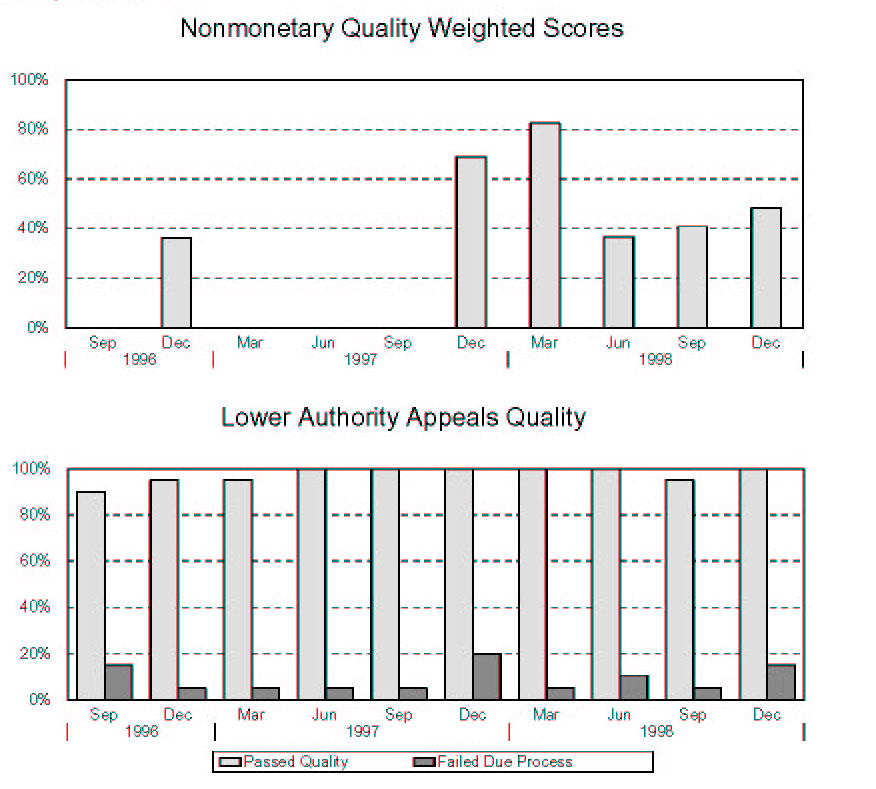

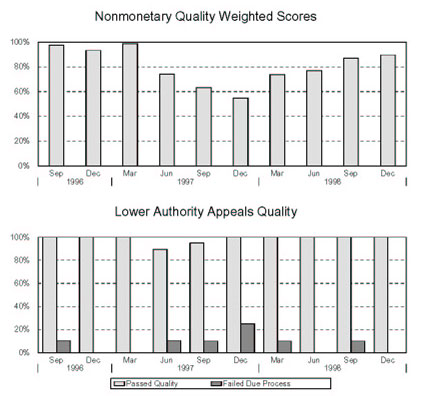

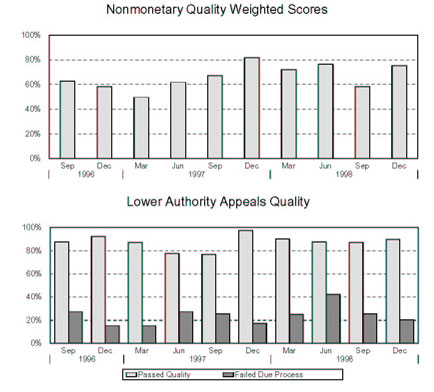

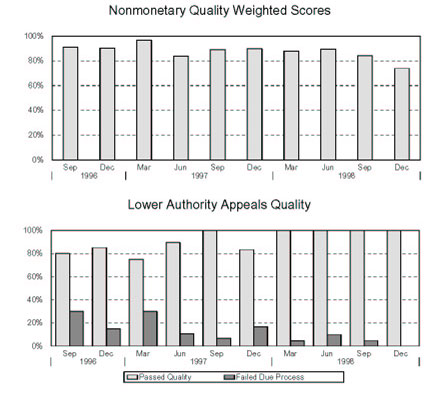

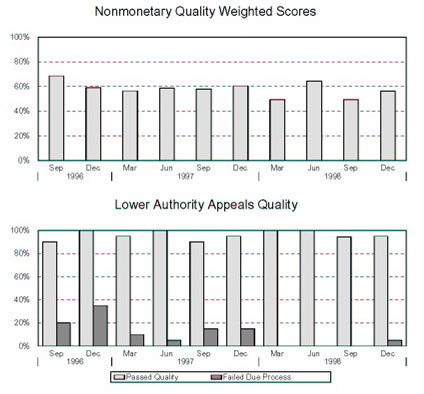

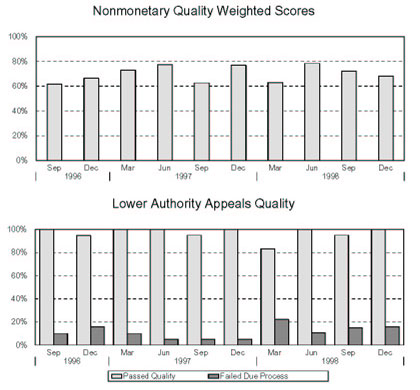

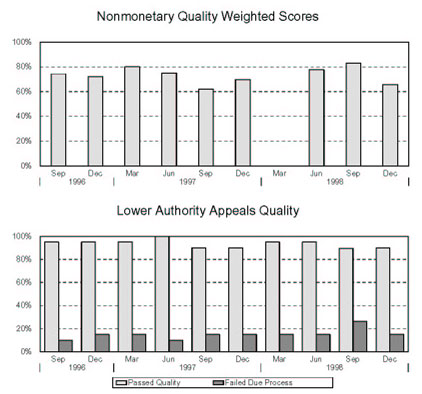

Nonmonetary Determinations Quality

The chart below shows that nonmon quality improved considerably between 1997 and 1998. The percentage of cases with passing quality scores (greater than 80 points) jumped from about 29% to nearly 40%.

The percentage of States that would have passed the new Tier I criterion--75% or more of their cases have scores of over 80 points--trended upward since the first quality samples were drawn and evaluated for the third quarter of 1996.

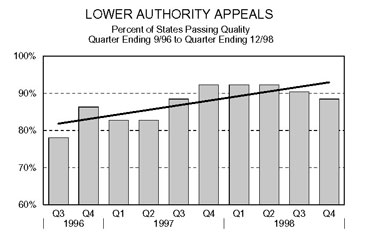

Lower Authority Appeals Quality

UI PERFORMS established a new Tier I performance criterion for appeals quality: 80 percent of appeals must pass with at least 85% of potential points. The scores of the due process subset of rating elements are also tabulated. For a case to pass the due process evaluation every element must be scored satisfactory.

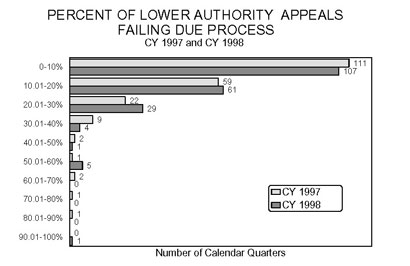

The lower chart shows the number of number of States' quarterly samples in 1997 and 1998 grouped by the percentages of cases failing due process. In 1997, there were both more quarters with 10% or fewer failing cases (111) and more than 30% (16) than in 1998 (107 and 11, respectively).

Benefit Accuracy Measurement Error Rates

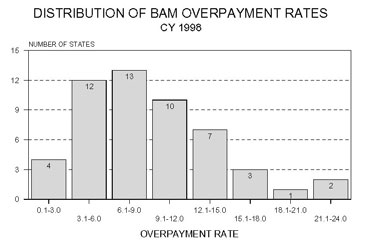

In Calendar Year 1998, the weighted BAM overpayment rate was 8.5%, and the underpayment rate was 0.9%, of benefits paid. Chart 35 illustrates that when first reported, for 1988, the rate exceeded 10%; it declined regularly to 7.5% in 1991, and since then it has stayed in the narrow range of 8% to 8.8%. Underpayments have been approximately 0.9% of benefits every year. Dollars overpaid have been approximately $1.6 billion each year since 1995.

In 1998, four states reported overpayment rates of 3% or less and three over 18%.

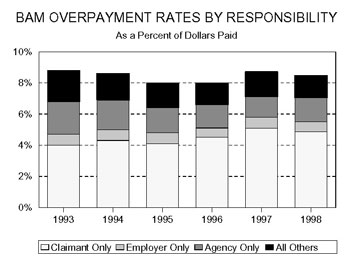

The largest cause of dollars overpaid in 1998 was Benefit Year Earnings violations--failing to report all or part of moneys earned while claiming benefits during the key week--followed by separations violations and then work search. The same pattern prevailed in 1997. Claimant errors were responsible for about 60% of overpayment errors, with claimants and the agency jointly responsible for another fifth.

Benefit Payment Control Recovery Performance

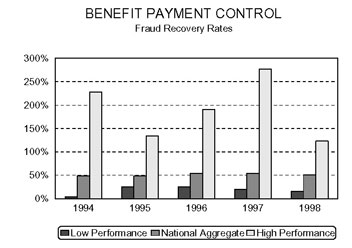

States reported that they recovered approximately 50% of the fraud overpayments they established in 1998, and about 55% of the nonfraud overpayments established. Although the aggregate recovery rate has been quite steady since 1994, the rate of the lowestperforming state has improved considerably for both fraud and nonfraud cases, and has risen steadily each year for nonfraud overpayments.

TAX PROGRAM ACTIVITY AND PERFORMANCE

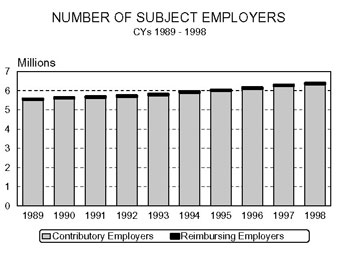

The number of subject employers has grown fairly steadily at a rate of about 1.5% a year since 1989 to a total of 6.4 million in 1998. Of these, about 6.3 million, or 98% were contributory.

The slow, steady annual growth conceals considerable turnover. Measured by status determination activity, turnover is quite high. Each year since 1994, new accounts and inactivations/terminations each amounted to about 13% of liable employers, and successorships close to 3%.

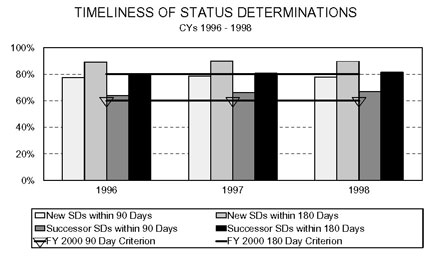

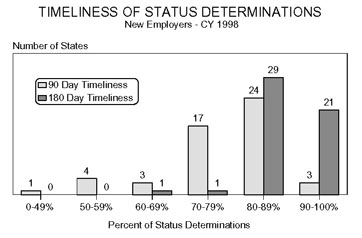

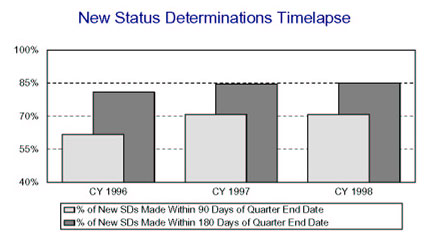

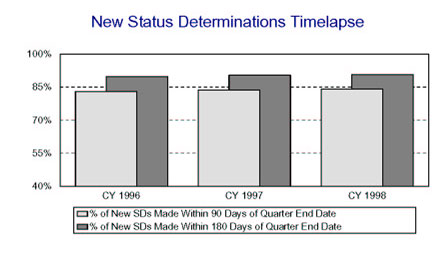

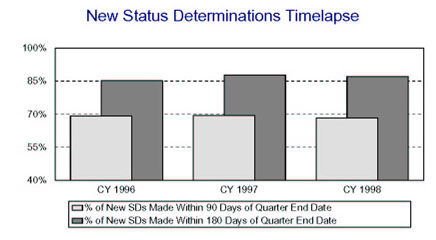

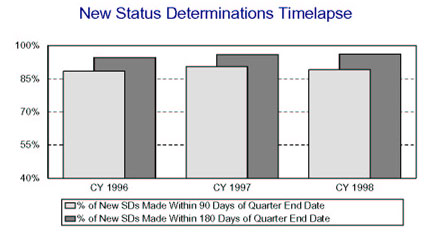

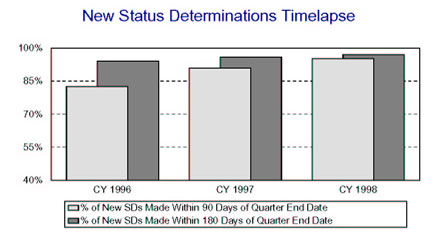

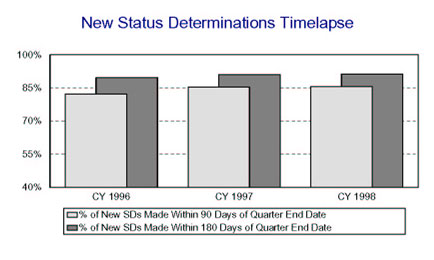

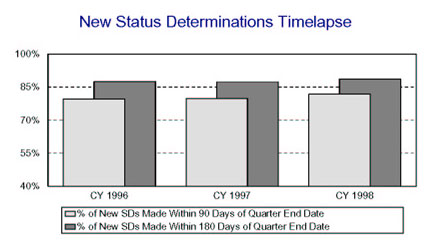

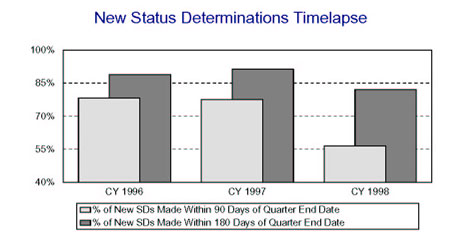

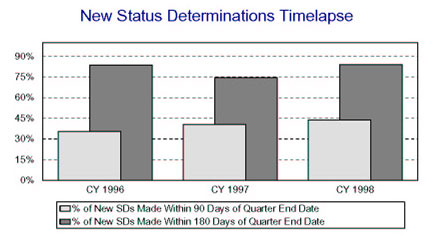

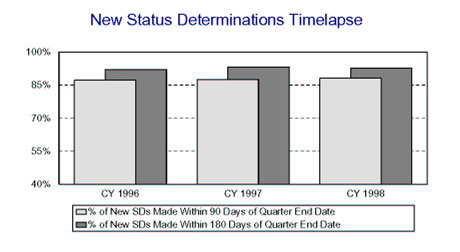

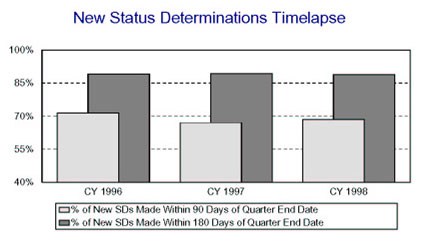

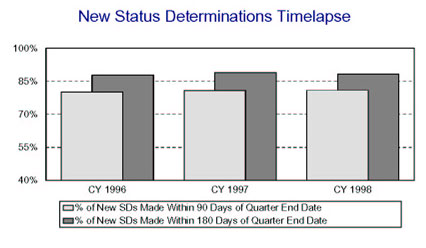

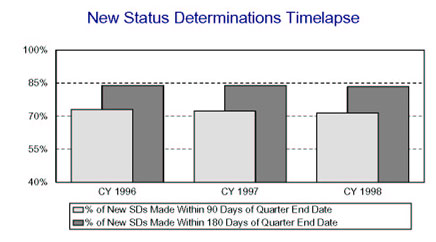

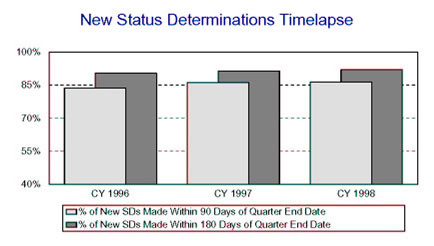

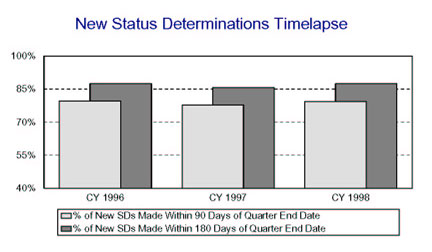

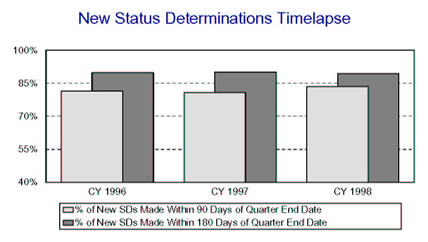

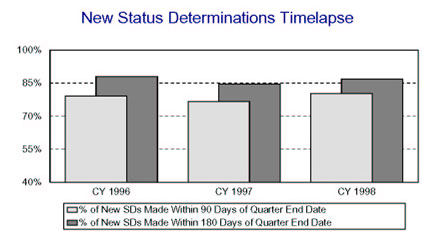

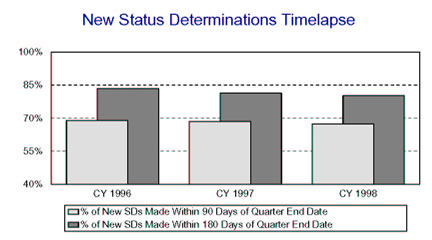

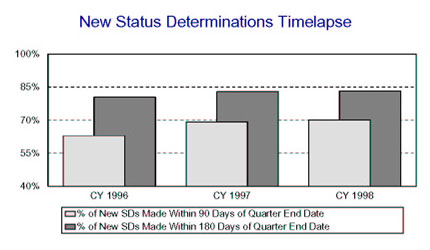

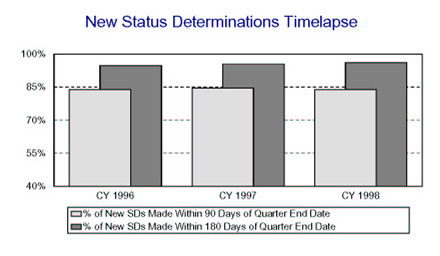

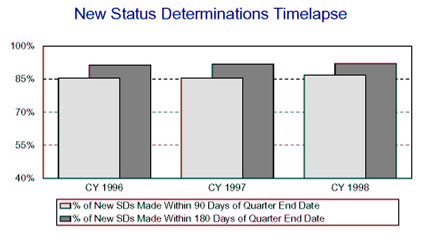

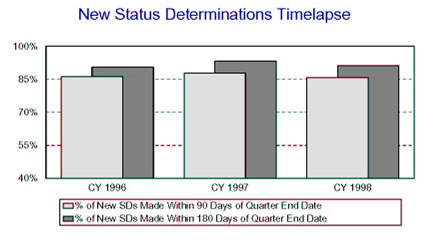

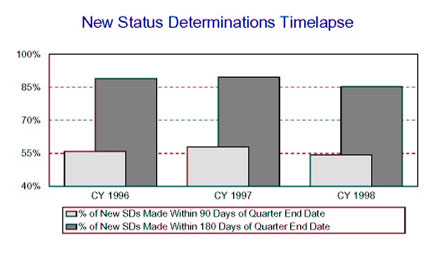

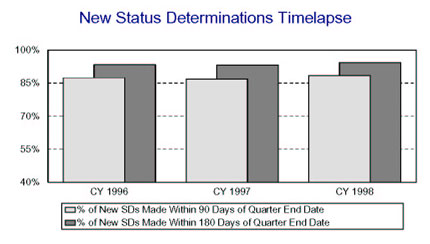

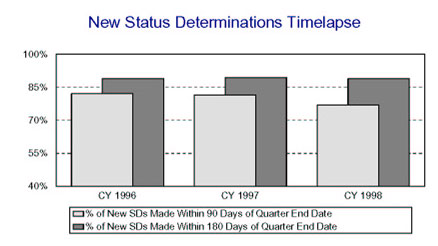

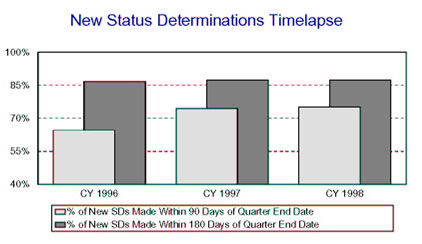

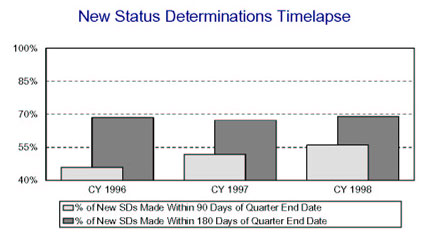

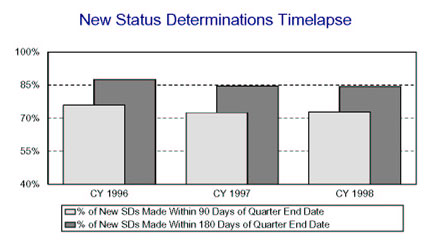

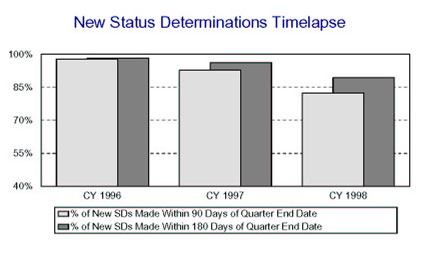

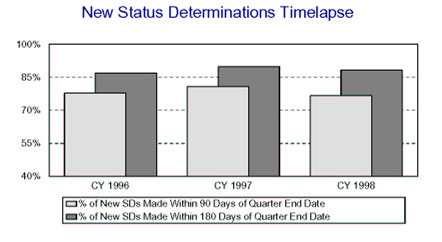

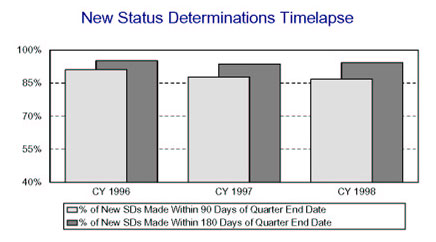

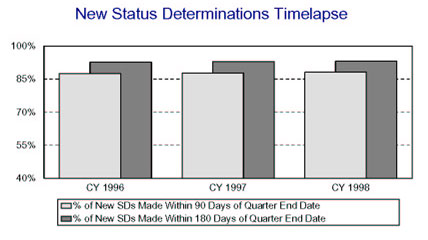

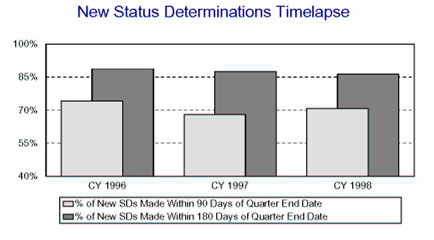

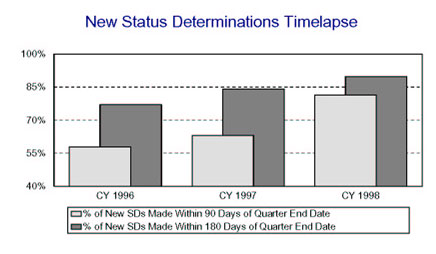

Status Determinations

State performance on both new and successor status determinations has remained quite stable since 1996. Nationally, they make nearly 80% of new determinations within 90 days, well above the new criterion of 60%, and about 90% within 180 days, also well over the new 180-day criterion. Successor timeliness is slower but has improved each year.

However, five States wouldhave failed to meet the 60-day criterion, and three the 180-day mark, in 1998, while two out of five States made all new determinations within 180 days.

States have not improved the accuracy of their status determinations since 1996. The number of States passing the new and successor acceptance samples has been flat at about 50% and 58%, respectively, while the number passing for terminations/inactivations has declined each year.

(Because the recently-announced Tier I criterion for the New Determinations accuracy is based on six allowable failures out of 60 instead of the present two, performance against that criterion would have been better than the figure shows.) The same pattern of declining accuracy holds for the posting of status findings.

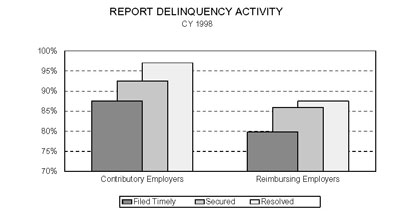

Report Delinquency

State receive more reports on time, and secure or resolve more delinquent reports, from contributory employers than from reimbursing. Over the last three years, there has been no noticeable pattern of improvement or decline in average timely reporting among contributory employers, although the performance of the best State has improved and that of the worstperforming State has worsened.

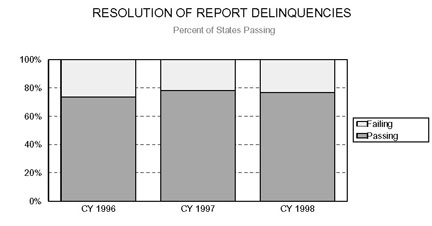

The number of States passing the acceptance sample for quality in delinquent reports operations improved from 1996 to 1997 and has held its level in 1998.

Collections

Just as with reporting, contributory employers are considerably more likely (92% to 81%) to pay due amounts on time than reimbursing.

Although the rates of turnover of delinquent amounts are about the same, States write off or declare doubtful about twice the proportions of unpaid amounts for reimbursing employers as for contributory.

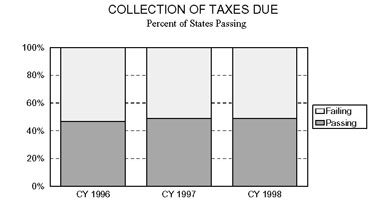

The proportion of total contributory employers taxes due paid timely was higher in 1998 than in 1996, and much higher than in 1997. Although there has been slight improvement from 1996 to 1998, only about half the States pass the acceptance sample for quality operation of the collections function.

Field Audit

In 1998, States audited about 2% of contributory employers. About two in five resulted in some change in the audited employerís liability or taxes due.

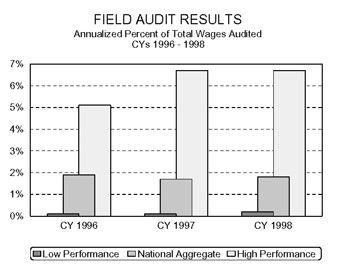

The aggregate penetration of wages is slightly lower than of employers. This suggests that on the whole, many smaller-than-average firms are selected for audit.

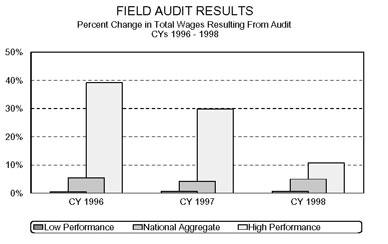

State performance in audit penetration varies considerably: the high State attains a penetration rate of wages which is about three times the average, and the low State about one tenth of the average. For the country as a whole, these audits resulted in a change of about 5% in aggregate wages in 1998, about the same result as in the two previous years. As with wage penetration, the range among States has always been considerable, from the lowest State reporting about 1% of wages changed due to audits to the highest of about 11% in 1998. The reported range was much greater in 1996 and 1997, because of changes reported by the highestchange States.

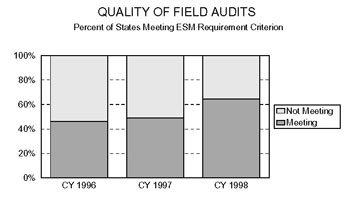

Field audit acceptance sample results have improved noticeably since 1996. In 1996, fewer than 50% passed the acceptance sample for satisfaction of Employment Security Manual audit requirements; by 1998, this had risen to about two thirds.

Account Maintenance

Calendar Year 1998 acceptance sample results show declining performance in the accuracy of most tax functions. The accuracy of field audits improved significantly from previous years.

The Calendar Year 1998 UI PERFORMS results, including data from the Benefit Accuracy Measurement, Benefits Timeliness and Quality , and the Tax Performance System programs, are displayed in a four-page format, individually, for each state. The display includes all Tier I measures and many Tier II measures. The corresponding national data is given as a means of comparison. Additionally, nonmonetary and lower authority appeals quality, and new status determination timeliness are displayed graphically.

The following symbols are used in the State reports:

* State did not report data as of 8/4/99.

** State had a problem in establishing the sample universe.

^ State did not participate in the program.

+ State does not have higher authority appeals.

A description of the footnotes referred to in the Benefit Accuracy Measurement section of the tabular display can be found in Appendix A.

| REPORTED MEASURE | WORKLOAD | STATE RESULTS |

NATIONAL RESULTS |

CRITERION |

|---|---|---|---|---|

| First Payment Timeliness | ||||

| Intrastate UI, full weeks - 14/21 Days | 113,569 | 96.7% | 90.1% | 87% |

| Intrastate UI, full weeks - 35 Days | 113,569 | 98.8% | 97.2% | 93% |

| Interstate UI, full weeks - 14/21 Days | 1,730 | 85.0% | 78.4% | 70% |

| Interstate UI, full weeks - 35 Days | 1,730 | 91.5% | 92.4% | 78% |

| All First Payments - 14/21 Days | 131,086 | 96.2% | 89.2% | 90% (Fiscal Year '02) |

| All First Payments - 35 Days | 131,086 | 98.6% | 97.0% | 95% (Fiscal Year '02) |

| Nonmonetary Determinations Timeliness: Detection Date to Determination Date |

||||

| Nonseparation Determ. within 14 Days | 116,188 | 64.3% | 68.6% | 80% (Fiscal Year '02) |

| Separation Determ. within 21 Days | 41,344 | 73.8% | 73.3% | 80% (Fiscal Year '02) |

| Nonmonetary Issue Detection Timeliness: First Week Affected to Detection Date |

||||

| Nonseparation Issues within 14 Days | 116,188 | 73.2% | 63.1% | none |

| Separation Issues within 21 Days | 41,344 | 93.9% | 90.7% | none |

| Lower Authority Appeals Timeliness | ||||

| Decisions within 30 Days of Filing | 12,929 | 82.9% | 67.9% | 60% |

| Decisions within 45 Days of Filing | 12,929 | 97.0% | 85.4% | 80% |

| Decisions within 90 Days of Filing | 12,929 | 99.6% | 95.5% | 95% (Fiscal Year '02) |

| Higher Authority Appeals Timeliness | ||||

| Decisions within 45 Days of Filing | 2,399 | 73.4% | 62.7% | 50% (Fiscal Year '00) |

| Decisions within 75 Days of Filing | 2,399 | 85.0% | 85.6% | 80% (Fiscal Year '00) |

| Decisions within 150 Days of Filing | 2,399 | 99.2% | 96.3% | 95% (Fiscal Year '00) |

| Combined Wage Program Timeliness | ||||

| Wage Transfers Made within 3 Days | 9,558 | 88.2% | 69.8% | none |

| Wage Transfers Made within 14 Days | 9,558 | 98.4% | 97.3% | none |

| Billing Made within 45 Days | 192 | 75.5% | 92.6% | none |

| Reimbursements Made within 45 Days | 185 | 99.5% | 96.4% | none |

| Continued Claims Payment Timeliness | ||||

| Payments Made within 7 Days | 1,257,022 | 86.9% | 61.4% | none |

| Payments Made within 14 Days | 1,257,022 | 97.0% | 92.5% | none |

| Payments Made within 21 Days | 1,257,022 | 98.9% | 96.3% | none |

| Benefit Quality Measures | ||||

| Nonmon. Determin. with Scores > 80% | 393 | 58.8% | 70.9% | 75% (Fiscal Year '02) |

| LA Appeals with Scores >= 85% | 78 | 97.5% | 90.5% | 80% (Fiscal Year '00) |

| Benefit Payment Control | ||||

| Fraud Overpayment Recovery Rate | 1,941,734 | 53.2% | 50.9% | none |

| Nonfraud Overpayment Recovery Rate | 4,266,552 | 77.2% | 56.1% | none |

| REPORTED MEASURE | STATE RESULTS | NATIONAL RESULTS | CRITERION | |

|---|---|---|---|---|

| Cash Management | ||||

| Average time (days) funds are on deposit before being transferred to Trust Fund | 2.6 | 2.1 days | < 2 (Fiscal Year '00) | |

| Ratio of avg daily loanable balance in Clearing Account to avg daily transfer to Tust Fund | 2.45 | 1.70 | < 1.75 (Fiscal Year '02) | |

| Benefit Accuracy Measurement | ||||

| Total Dollars Paid in Population | $211,507,128 | $18.8 B | none | |

| Sample Size | 702 | 26,353 | none | |

| Proper Payment Rate | 92.5 +/- 1.9 | 91.5% | none | |

| Overpayment Rate | 7.5 +/- 1.9 | 8.5% | none | |

| Underpayment Rate | 0.6 +/- 0.4 | 0.9% | none | |

| Footnotes: | none | |||

| REPORTED MEASURE | STATE RESULTS | NATIONAL RESULTS | ||

|---|---|---|---|---|

| Status Determinations | ||||

| New Employer Determinations: | ||||

| Percentage Made Within 90 Days (Fiscal Year '00 criterion: 60%) | 70.7% | 78.0% | ||

| Percentage Made Within 180 Days (Fiscal Year '00 criterion: 80%) | 84.9% | 89.7% | ||

| Accuracy In Determinations? (Fiscal Year '02 criterion: <= 6 failed) | ** | 45.8% Pass | ||

| Accuracy In Postings? | ** | 39.6% Pass | ||

| Successor Determinations: | ||||

| Percentage Made Within 90 Days | 47.2% | 67.0% | ||

| Percentage Made Within 180 Days | 77.3% | 81.5% | ||

| Accuracy In Determinations? | P | 54.2% Pass | ||

| Accuracy In Postings? | P | 45.8% Pass | ||

| Inactivations: | ||||

| Accuracy In Determinations? | ** | 64.4% Pass | ||

| Accuracy In Postings? | ** | 64.6% Pass | ||

| Report Delinquency | ||||

| Reports From Contributory Employers: | ||||

| Percentage Filed Timely | 91.9% | 87.4% | ||

| Percentage Secured | 96.1% | 92.5% | ||

| Percentage Resolved | 98.0% | 97.1% | ||

| Reports From Reimbursing Employers: | ||||

| Percentage Filed Timely | 95.4% | 79.8% | ||

| Percentage Secured | 95.8% | 85.9% | ||

| Percentage Resolved | 96.1% | 87.5% | ||

| Appropriate Actions Taken To Resolve Delinquencies? | ** | 76.6% Pass | ||

| Collections | ||||

| Collections From Contributory Employers: | ||||

| Percentage Of Tax Due Paid Timely | 95.9% | 92.0% | ||

| Turnover Ratio - Ratio Of Receivables Liquidated Or Declared Uncollectible/Doubtful To Tax Due | 3.0% | 8.1% | ||

| Percentage of Tax Due Declared Uncollectible/Doubtful | 0.0% | 1.3% | ||

| Accounts Receivable As A Percentage Of Tax Due | 2.8% | 2.2% | ||

| Collections From Reimbursing Employers: | ||||

| Percentage Of Tax Due Paid Timely | 77.9% | 80.6% | ||

| Turnover Ratio - Ratio Of Receivables Liquidated Or Declared Uncollectible/Doubtful To Tax Due | 20.1% | 19.4% | ||

| Percentage of Tax Due Declared Uncollectible/Doubtful | 0.0% | 1.2% | ||

| Accounts Receivable As A Percentage Of Tax Due | 3.7% | 4.6% | ||

| Appropriate Actions Taken To Collect Tax Due? | P | 48.9% Pass | ||

| Cashiering | ||||

| Remittances Deposited Within Three Days? | P | 92.0% Pass | ||

| Field Audit | ||||

| Percent Change In Total Wages Resulting From Audits | 0.6% | 5.0% | ||

| Percentage Of Contributory Employers Audited | 2.0% | 2.0% | ||

| Annualized Percentage Of Total Wages Audited | 1.0% | 1.8% | ||

| Audits Meet Employment Security Manual Requirements? | F | 64.6% Pass | ||

| Account Maintenance | ||||

| Accuracy In Report Processing? | P | 96.0% Pass | ||

| Accuracy In Contributory Employer Billing? | P | 84.8% Pass | ||

| Accuracy In Reimbursing Employer Billings? | ** | 85.7% Pass | ||

| Accuracy In Credits/Refunds? | F | 73.9% Pass | ||

| Accuracy In Benefit Charging? | P | 89.6% Pass | ||

| Accuracy In Experience Rating? | P | 87.8% Pass | ||

** State had a problem in establishing the sample universe.

| Alaska | ||||

| REPORTED MEASURE | WORKLOAD | STATE RESULTS |

NATIONAL RESULTS |

CRITERION |

|---|---|---|---|---|

| First Payment Timeliness | ||||

| Intrastate UI, full weeks - 14/21 Days | 28,040 | 90.5% | 90.1% | 87% |

| Intrastate UI, full weeks - 35 Days | 28,040 | 97.2% | 97.2% | 93% |

| Interstate UI, full weeks - 14/21 Days | 12,163 | 82.2% | 78.4% | 70% |

| Interstate UI, full weeks - 35 Days | 12,163 | 92.8% | 92.4% | 78% |

| All First Payments - 14/21 Days | 45,431 | 87.3% | 89.2% | 90% (Fiscal Year '02) |

| All First Payments - 35 Days | 45,431 | 95.8% | 97.0% | 95% (Fiscal Year '02) |

| Nonmonetary Determinations Timeliness: Detection Date to Determination Date |

||||

| Nonseparation Determ. within 14 Days | 27,166 | 89.4% | 68.6% | 80% (Fiscal Year '02) |

| Separation Determ. within 21 Days | 11,973 | 95.9% | 73.3% | 80% (Fiscal Year '02) |

| Nonmonetary Issue Detection Timeliness: First Week Affected to Detection Date |

||||

| Nonseparation Issues within 14 Days | 27,166 | 78.3% | 63.1% | none |

| Separation Issues within 21 Days | 11,973 | 46.0% | 90.7% | none |

| Lower Authority Appeals Timeliness | ||||

| Decisions within 30 Days of Filing | 2,543 | 63.7% | 67.9% | 60% |

| Decisions within 45 Days of Filing | 2,543 | 90.6% | 85.4% | 80% |

| Decisions within 90 Days of Filing | 2,543 | 99.1% | 95.5% | 95% (Fiscal Year '02) |

| Higher Authority Appeals Timeliness | ||||

| Decisions within 45 Days of Filing | 162 | 44.4% | 62.7% | 50% (Fiscal Year '00) |

| Decisions within 75 Days of Filing | 162 | 82.7% | 85.6% | 80% (Fiscal Year '00) |

| Decisions within 150 Days of Filing | 162 | 96.9% | 96.3% | 95% (Fiscal Year '00) |

| Combined Wage Program Timeliness | ||||

| Wage Transfers Made within 3 Days | 6,420 | 0.0% | 69.8% | none |

| Wage Transfers Made within 14 Days | 6,420 | 94.2% | 97.3% | none |

| Billing Made within 45 Days | 96 | 100.0% | 92.6% | none |

| Reimbursements Made within 45 Days | 81 | 84.0% | 96.4% | none |

| Continued Claims Payment Timeliness | ||||

| Payments Made within 7 Days | 632,108 | 44.2% | 61.4% | none |

| Payments Made within 14 Days | 632,108 | 90.6% | 92.5% | none |

| Payments Made within 21 Days | 632,108 | 96.0% | 96.3% | none |

| Benefit Quality Measures | ||||

| Nonmon. Determin. with Scores > 80% | 228 | 72.2% | 70.9% | 75% (Fiscal Year '02) |

| LA Appeals with Scores >= 85% | 78 | 96.2% | 90.5% | 80% (Fiscal Year '00) |

| Benefit Payment Control | ||||

| Fraud Overpayment Recovery Rate | 787,509 | 73.9% | 50.9% | none |

| Nonfraud Overpayment Recovery Rate | 1,050,641 | 90.3% | 56.1% | none |

| Alaska | ||||

| REPORTED MEASURE | STATE RESULTS | NATIONAL RESULTS | CRITERION | |

|---|---|---|---|---|

| Cash Management | ||||

| Average time (days) funds are on deposit before being transferred to Trust Fund | 1.6 | 2.1 days | <= 2 (Fiscal Year '00) | |

| Ratio of avg daily loanable balance in Clearing Account to avg daily transfer to Tust Fund | .20 | 1.70 | <= 1.75 (Fiscal Year '02) | |

| Benefit Accuracy Measurement | ||||

| Total Dollars Paid in Population | $92,772,219 | $18.8 B | none | |

| Sample Size | 481 | 26,353 | none | |

| Proper Payment Rate | 92.5 +/- 2.4 | 91.5% | none | |

| Overpayment Rate | 7.5 +/- 2.4 | 8.5% | none | |

| Underpayment Rate | 1.4 +/- 0.5 | 0.9% | none | |

| Footnotes: | #1 | |||

| Alaska | ||||

| REPORTED MEASURE | STATE RESULTS | NATIONAL RESULTS | ||

|---|---|---|---|---|

| Status Determinations | ||||

| New Employer Determinations: | ||||

| Percentage Made Within 90 Days (Fiscal Year '00 criterion: 60%) | 84.0% | 78.0% | ||

| Percentage Made Within 180 Days (Fiscal Year '00 criterion: 80%) | 90.6% | 89.7% | ||

| Accuracy In Determinations? (Fiscal Year '02 criterion: <= 6 failed) | F | 45.8% Pass | ||

| Accuracy In Postings? | F | 39.6% Pass | ||

| Successor Determinations: | ||||

| Percentage Made Within 90 Days | 79.2% | 67.0% | ||

| Percentage Made Within 180 Days | 86.8% | 81.5% | ||

| Accuracy In Determinations? | F | 54.2% Pass | ||

| Accuracy In Postings? | F | 45.8% Pass | ||

| Inactivations: | ||||

| Accuracy In Determinations? | P | 64.4% Pass | ||

| Accuracy In Postings? | P | 64.6% Pass | ||

| Report Delinquency | ||||

| Reports From Contributory Employers: | ||||

| Percentage Filed Timely | 90.8% | 87.4% | ||

| Percentage Secured | 96.3% | 92.5% | ||

| Percentage Resolved | 99.3% | 97.1% | ||

| Reports From Reimbursing Employers: | ||||

| Percentage Filed Timely | 93.8% | 79.8% | ||

| Percentage Secured | 95.9% | 85.9% | ||

| Percentage Resolved | 98.5% | 87.5% | ||

| Appropriate Actions Taken To Resolve Delinquencies? | P | 76.6% Pass | ||

| Collections | ||||

| Collections From Contributory Employers: | ||||

| Percentage Of Tax Due Paid Timely | 88.3% | 92.0% | ||

| Turnover Ratio - Ratio Of Receivables Liquidated Or Declared Uncollectible/Doubtful To Tax Due | 11.4% | 8.1% | ||

| Percentage of Tax Due Declared Uncollectible/Doubtful | 0.3% | 1.3% | ||

| Accounts Receivable As A Percentage Of Tax Due | 2.0% | 2.2% | ||

| Collections From Reimbursing Employers: | ||||

| Percentage Of Tax Due Paid Timely | 95.7% | 80.6% | ||

| Turnover Ratio - Ratio Of Receivables Liquidated Or Declared Uncollectible/Doubtful To Tax Due | 4.6% | 19.4% | ||

| Percentage of Tax Due Declared Uncollectible/Doubtful | 0.0% | 1.2% | ||

| Accounts Receivable As A Percentage Of Tax Due | 0.4% | 4.6% | ||

| Appropriate Actions Taken To Collect Tax Due? | F | 48.9% Pass | ||

| Cashiering | ||||

| Remittances Deposited Within Three Days? | P | 92.0% Pass | ||

| Field Audit | ||||

| Percent Change In Total Wages Resulting From Audits | 7.0% | 5.0% | ||

| Percentage Of Contributory Employers Audited | 2.2% | 2.0% | ||

| Annualized Percentage Of Total Wages Audited | 2.6% | 1.8% | ||

| Audits Meet Employment Security Manual Requirements? | F | 64.6% Pass | ||

| Account Maintenance | ||||

| Accuracy In Report Processing? | P | 96.0% Pass | ||

| Accuracy In Contributory Employer Billing? | P | 84.8% Pass | ||

| Accuracy In Reimbursing Employer Billings? | F | 85.7% Pass | ||

| Accuracy In Credits/Refunds? | F | 73.9% Pass | ||

| Accuracy In Benefit Charging? | F | 89.6% Pass | ||

| Accuracy In Experience Rating? | P | 87.8% Pass | ||

| Arizona | ||||

| REPORTED MEASURE | WORKLOAD | STATE RESULTS |

NATIONAL RESULTS |

CRITERION |

|---|---|---|---|---|

| First Payment Timeliness | ||||

| Intrastate UI, full weeks - 14/21 Days | 53,436 | 96.1% | 90.1% | 87% |

| Intrastate UI, full weeks - 35 Days | 53,436 | 98.3% | 97.2% | 93% |

| Interstate UI, full weeks - 14/21 Days | 3,157 | 78.2% | 78.4% | 70% |

| Interstate UI, full weeks - 35 Days | 3,157 | 94.2% | 92.4% | 78% |

| All First Payments - 14/21 Days | 61,066 | 94.9% | 89.2% | 90% (Fiscal Year '02) |

| All First Payments - 35 Days | 61,066 | 98.1% | 97.0% | 95% (Fiscal Year '02) |

| Nonmonetary Determinations Timeliness: Detection Date to Determination Date |

||||

| Nonseparation Determ. within 14 Days | 49,935 | 83.9% | 68.6% | 80% (Fiscal Year '02) |

| Separation Determ. within 21 Days | 48,154 | 95.6% | 73.3% | 80% (Fiscal Year '02) |

| Nonmonetary Issue Detection Timeliness: First Week Affected to Detection Date |

||||

| Nonseparation Issues within 14 Days | 49,935 | 87.1% | 63.1% | none |

| Separation Issues within 21 Days | 48,154 | 94.8% | 90.7% | none |

| Lower Authority Appeals Timeliness | ||||

| Decisions within 30 Days of Filing | 12,401 | 83.4% | 67.9% | 60% |

| Decisions within 45 Days of Filing | 12,401 | 96.1% | 85.4% | 80% |

| Decisions within 90 Days of Filing | 12,401 | 98.8% | 95.5% | 95% (Fiscal Year '02) |

| Higher Authority Appeals Timeliness | ||||

| Decisions within 45 Days of Filing | 1,613 | 78.1% | 62.7% | 50% (Fiscal Year '00) |

| Decisions within 75 Days of Filing | 1,613 | 94.0% | 85.6% | 80% (Fiscal Year '00) |

| Decisions within 150 Days of Filing | 1,613 | 98.3% | 96.3% | 95% (Fiscal Year '00) |

| Combined Wage Program Timeliness | ||||

| Wage Transfers Made within 3 Days | 9,364 | 0.0% | 69.8% | none |

| Wage Transfers Made within 14 Days | 9,364 | 99.6% | 97.3% | none |

| Billing Made within 45 Days | 0 | 0.0% | 92.6% | none |

| Reimbursements Made within 45 Days | 0 | 0.0% | 96.4% | none |

| Continued Claims Payment Timeliness | ||||

| Payments Made within 7 Days | 854,114 | 95.0% | 61.4% | none |

| Payments Made within 14 Days | 854,114 | 98.2% | 92.5% | none |

| Payments Made within 21 Days | 854,114 | 99.0% | 96.3% | none |

| Benefit Quality Measures | ||||

| Nonmon. Determin. with Scores > 80% | 388 | 65.4% | 70.9% | 75% (Fiscal Year '02) |

| LA Appeals with Scores >= 85% | 76 | 97.4% | 90.5% | 80% (Fiscal Year '00) |

| Benefit Payment Control | ||||

| Fraud Overpayment Recovery Rate | 2,219,212 | 67.3% | 50.9% | none |

| Nonfraud Overpayment Recovery Rate | 2,030,602 | 68.1% | 56.1% | none |

| Arizona | ||||

| REPORTED MEASURE | STATE RESULTS | NATIONAL RESULTS | CRITERION | |

|---|---|---|---|---|

| Cash Management | ||||

| Average time (days) funds are on deposit before being transferred to Trust Fund | 1.6 | 2.1 days | <= 2 (Fiscal Year '00) | |

| Ratio of avg daily loanable balance in Clearing Account to avg daily transfer to Tust Fund | 0.65 | 1.70 | <= 1.75 (Fiscal Year '02) | |

| Benefit Accuracy Measurement | ||||

| Total Dollars Paid in Population | $123,745,079 | $18.8 B | none | |

| Sample Size | 480 | 26,353 | none | |

| Proper Payment Rate | 89.3 +/- 3 | 91.5% | none | |

| Overpayment Rate | 10.7 +/- 3 | 8.5% | none | |

| Underpayment Rate | 0.4 +/- 0.3 | 0.9% | none | |

| Footnotes: | none | |||

| Arizona | ||||

| REPORTED MEASURE | STATE RESULTS | NATIONAL RESULTS | ||

|---|---|---|---|---|

| Status Determinations | ||||

| New Employer Determinations: | ||||

| Percentage Made Within 90 Days (Fiscal Year '00 criterion: 60%) | 68.2% | 78.0% | ||

| Percentage Made Within 180 Days (Fiscal Year '00 criterion: 80%) | 87.1% | 89.7% | ||

| Accuracy In Determinations? (Fiscal Year '02 criterion: <= 6 failed) | F | 45.8% Pass | ||

| Accuracy In Postings? | F | 39.6% Pass | ||

| Successor Determinations: | ||||

| Percentage Made Within 90 Days | 63.2% | 67.0% | ||

| Percentage Made Within 180 Days | 81.2% | 81.5% | ||

| Accuracy In Determinations? | F | 54.2% Pass | ||

| Accuracy In Postings? | F | 45.8% Pass | ||

| Inactivations: | ||||

| Accuracy In Determinations? | F | 64.4% Pass | ||

| Accuracy In Postings? | F | 64.6% Pass | ||

| Report Delinquency | ||||

| Reports From Contributory Employers: | ||||

| Percentage Filed Timely | 89.7% | 87.4% | ||

| Percentage Secured | 98.0% | 92.5% | ||

| Percentage Resolved | 102.5% | 97.1% | ||

| Reports From Reimbursing Employers: | ||||

| Percentage Filed Timely | 92.0% | 79.8% | ||

| Percentage Secured | 98.9% | 85.9% | ||

| Percentage Resolved | 100.7% | 87.5% | ||

| Appropriate Actions Taken To Resolve Delinquencies? | F | 76.6% Pass | ||

| Collections | ||||

| Collections From Contributory Employers: | ||||

| Percentage Of Tax Due Paid Timely | 96.7% | 92.0% | ||

| Turnover Ratio - Ratio Of Receivables Liquidated Or Declared Uncollectible/Doubtful To Tax Due | 3.4% | 8.1% | ||

| Percentage of Tax Due Declared Uncollectible/Doubtful | 0.4% | 1.3% | ||

| Accounts Receivable As A Percentage Of Tax Due | 1.3% | 2.2% | ||

| Collections From Reimbursing Employers: | ||||

| Percentage Of Tax Due Paid Timely | 89.3% | 80.6% | ||

| Turnover Ratio - Ratio Of Receivables Liquidated Or Declared Uncollectible/Doubtful To Tax Due | 9.8% | 19.4% | ||

| Percentage of Tax Due Declared Uncollectible/Doubtful | 0.0% | 1.2% | ||

| Accounts Receivable As A Percentage Of Tax Due | 1.1% | 4.6% | ||

| Appropriate Actions Taken To Collect Tax Due? | P | 48.9% Pass | ||

| Cashiering | ||||

| Remittances Deposited Within Three Days? | P | 92.0% Pass | ||

| Field Audit | ||||

| Percent Change In Total Wages Resulting From Audits | 2.5% | 5.0% | ||

| Percentage Of Contributory Employers Audited | 2.4% | 2.0% | ||

| Annualized Percentage Of Total Wages Audited | 2.2% | 1.8% | ||

| Audits Meet Employment Security Manual Requirements? | F | 64.6% Pass | ||

| Account Maintenance | ||||

| Accuracy In Report Processing? | P | 96.0% Pass | ||

| Accuracy In Contributory Employer Billing? | P | 84.8% Pass | ||

| Accuracy In Reimbursing Employer Billings? | P | 85.7% Pass | ||

| Accuracy In Credits/Refunds? | P | 73.9% Pass | ||

| Accuracy In Benefit Charging? | P | 89.6% Pass | ||

| Accuracy In Experience Rating? | P | 87.8% Pass | ||

| Arkansas | ||||

| REPORTED MEASURE | WORKLOAD | STATE RESULTS |

NATIONAL RESULTS |

CRITERION |

|---|---|---|---|---|

| First Payment Timeliness | ||||

| Intrastate UI, full weeks - 14/21 Days | 43,013 | 90.1% | 90.1% | 87% |

| Intrastate UI, full weeks - 35 Days | 43,013 | 97.3% | 97.2% | 93% |

| Interstate UI, full weeks - 14/21 Days | 1,434 | 72.6% | 78.4% | 70% |

| Interstate UI, full weeks - 35 Days | 1,434 | 92.7% | 92.4% | 78% |

| All First Payments - 14/21 Days | 57,369 | 90.4% | 89.2% | 90% (Fiscal Year '02) |

| All First Payments - 35 Days | 57,369 | 97.6% | 97.0% | 95% (Fiscal Year '02) |

| Nonmonetary Determinations Timeliness: Detection Date to Determination Date |

||||

| Nonseparation Determ. within 14 Days | 19,641 | 63.1% | 68.6% | 80% (Fiscal Year '02) |

| Separation Determ. within 21 Days | 27,046 | 54.2% | 73.3% | 80% (Fiscal Year '02) |

| Nonmonetary Issue Detection Timeliness: First Week Affected to Detection Date |

||||

| Nonseparation Issues within 14 Days | 19,641 | 74.0% | 63.1% | none |

| Separation Issues within 21 Days | 27,046 | 71.9% | 90.7% | none |

| Lower Authority Appeals Timeliness | ||||

| Decisions within 30 Days of Filing | 10,166 | 97.3% | 67.9% | 60% |

| Decisions within 45 Days of Filing | 10,166 | 99.4% | 85.4% | 80% |

| Decisions within 90 Days of Filing | 10,166 | 100.0% | 95.5% | 95% (Fiscal Year '02) |

| Higher Authority Appeals Timeliness | ||||

| Decisions within 45 Days of Filing | 1,944 | 90.3% | 62.7% | 50% (Fiscal Year '00) |

| Decisions within 75 Days of Filing | 1,944 | 95.3% | 85.6% | 80% (Fiscal Year '00) |

| Decisions within 150 Days of Filing | 1,944 | 98.1% | 96.3% | 95% (Fiscal Year '00) |

| Combined Wage Program Timeliness | ||||

| Wage Transfers Made within 3 Days | 6,515 | 18.4% | 69.8% | none |

| Wage Transfers Made within 14 Days | 6,515 | 71.6% | 97.3% | none |

| Billing Made within 45 Days | 250 | 20.4% | 92.6% | none |

| Reimbursements Made within 45 Days | 181 | 93.4% | 96.4% | none |

| Continued Claims Payment Timeliness | ||||

| Payments Made within 7 Days | 680,065 | 83.4% | 61.4% | none |

| Payments Made within 14 Days | 680,065 | 96.5% | 92.5% | none |

| Payments Made within 21 Days | 680,065 | 98.5% | 96.3% | none |

| Benefit Quality Measures | ||||

| Nonmon. Determin. with Scores > 80% | 175 | 85.9% | 70.9% | 75% (Fiscal Year '02) |

| LA Appeals with Scores >= 85% | 79 | 89.9% | 90.5% | 80% (Fiscal Year '00) |

| Benefit Payment Control | ||||

| Fraud Overpayment Recovery Rate | 816,423 | 37.2% | 50.9% | none |

| Nonfraud Overpayment Recovery Rate | 1,287,773 | 32.5% | 56.1% | none |

| Arkansas | ||||

| REPORTED MEASURE | STATE RESULTS | NATIONAL RESULTS | CRITERION | |

|---|---|---|---|---|

| Cash Management | ||||

| Average time (days) funds are on deposit before being transferred to Trust Fund | 1.7 | 2.1 days | <= 2 (Fiscal Year '00) | |

| Ratio of avg daily loanable balance in Clearing Account to avg daily transfer to Tust Fund | 0.65 | 1.70 | <= 1.75 (Fiscal Year '02) | |

| Benefit Accuracy Measurement | ||||

| Total Dollars Paid in Population | $173,585,152 | $18.8 B | none | |

| Sample Size | 479 | 26,353 | none | |

| Proper Payment Rate | 92.3 +/- 2.6 | 91.5% | none | |

| Overpayment Rate | 7.7 +/- 2.6 | 8.5% | none | |

| Underpayment Rate | 0.5 +/- 0.3 | 0.9% | none | |

| Footnotes: | none | |||

| Arkansas | ||||

| REPORTED MEASURE | STATE RESULTS | NATIONAL RESULTS | ||

|---|---|---|---|---|

| Status Determinations | ||||

| New Employer Determinations: | ||||

| Percentage Made Within 90 Days (Fiscal Year '00 criterion: 60%) | 51.1% | 78.0% | ||

| Percentage Made Within 180 Days (Fiscal Year '00 criterion: 80%) | 80.9% | 89.7% | ||

| Accuracy In Determinations? (Fiscal Year '02 criterion: <= 6 failed) | ** | 45.8% Pass | ||

| Accuracy In Postings? | ** | 39.6% Pass | ||

| Successor Determinations: | ||||

| Percentage Made Within 90 Days | 44.0% | 67.0% | ||

| Percentage Made Within 180 Days | 78.6% | 81.5% | ||

| Accuracy In Determinations? | ** | 54.2% Pass | ||

| Accuracy In Postings? | ** | 45.8% Pass | ||

| Inactivations: | ||||

| Accuracy In Determinations? | ** | 64.4% Pass | ||

| Accuracy In Postings? | ** | 64.6% Pass | ||

| Report Delinquency | ||||

| Reports From Contributory Employers: | ||||

| Percentage Filed Timely | 91.4% | 87.4% | ||

| Percentage Secured | 98.7% | 92.5% | ||

| Percentage Resolved | 101.9% | 97.1% | ||

| Reports From Reimbursing Employers: | ||||

| Percentage Filed Timely | 95.3% | 79.8% | ||

| Percentage Secured | 98.3% | 85.9% | ||

| Percentage Resolved | 100.3% | 87.5% | ||

| Appropriate Actions Taken To Resolve Delinquencies? | ** | 76.6% Pass | ||

| Collections | ||||

| Collections From Contributory Employers: | ||||

| Percentage Of Tax Due Paid Timely | 97.7% | 92.0% | ||

| Turnover Ratio - Ratio Of Receivables Liquidated Or Declared Uncollectible/Doubtful To Tax Due | 2.5% | 8.1% | ||

| Percentage of Tax Due Declared Uncollectible/Doubtful | 1.1% | 1.3% | ||

| Accounts Receivable As A Percentage Of Tax Due | 1.6% | 2.2% | ||

| Collections From Reimbursing Employers: | ||||

| Percentage Of Tax Due Paid Timely | 96.4% | 80.6% | ||

| Turnover Ratio - Ratio Of Receivables Liquidated Or Declared Uncollectible/Doubtful To Tax Due | 5.5% | 19.4% | ||

| Percentage of Tax Due Declared Uncollectible/Doubtful | 2.7% | 1.2% | ||

| Accounts Receivable As A Percentage Of Tax Due | 1.9% | 4.6% | ||

| Appropriate Actions Taken To Collect Tax Due? | ** | 48.9% Pass | ||

| Cashiering | ||||

| Remittances Deposited Within Three Days? | F | 92.0% Pass | ||

| Field Audit | ||||

| Percent Change In Total Wages Resulting From Audits | 1.4% | 5.0% | ||

| Percentage Of Contributory Employers Audited | 1.9% | 2.0% | ||

| Annualized Percentage Of Total Wages Audited | 0.9% | 1.8% | ||

| Audits Meet Employment Security Manual Requirements? | ** | 64.6% Pass | ||

| Account Maintenance | ||||

| Accuracy In Report Processing? | P | 96.0% Pass | ||

| Accuracy In Contributory Employer Billing? | ** | 84.8% Pass | ||

| Accuracy In Reimbursing Employer Billings? | ** | 85.7% Pass | ||

| Accuracy In Credits/Refunds? | ** | 73.9% Pass | ||

| Accuracy In Benefit Charging? | ** | 89.6% Pass | ||

| Accuracy In Experience Rating? | F | 87.8% Pass | ||

** State had a problem in establishing the sample universe.

| California | ||||

| REPORTED MEASURE | WORKLOAD | STATE RESULTS |

NATIONAL RESULTS |

CRITERION |

|---|---|---|---|---|

| First Payment Timeliness | ||||

| Intrastate UI, full weeks - 14/21 Days | 982,938 | 87.1% | 90.1% | 87% |

| Intrastate UI, full weeks - 35 Days | 982,938 | 96.9% | 97.2% | 93% |

| Interstate UI, full weeks - 14/21 Days | 20,938 | 77.4% | 78.4% | 70% |

| Interstate UI, full weeks - 35 Days | 20,938 | 93.5% | 92.4% | 78% |

| All First Payments - 14/21 Days | 1,059,905 | 86.2% | 89.2% | 90% (Fiscal Year '02) |

| All First Payments - 35 Days | 1,059,905 | 96.8% | 97.0% | 95% (Fiscal Year '02) |

| Nonmonetary Determinations Timeliness: Detection Date to Determination Date |

||||

| Nonseparation Determ. within 14 Days | 1,498,938 | 74.7% | 68.6% | 80% (Fiscal Year '02) |

| Separation Determ. within 21 Days | 582,481 | 90.3% | 73.3% | 80% (Fiscal Year '02) |

| Nonmonetary Issue Detection Timeliness: First Week Affected to Detection Date |

||||

| Nonseparation Issues within 14 Days | 1,459,411 | 54.9% | 63.1% | none |

| Separation Issues within 21 Days | 574,612 | 91.4% | 90.7% | none |

| Lower Authority Appeals Timeliness | ||||

| Decisions within 30 Days of Filing | 180,601 | 48.7% | 67.9% | 60% |

| Decisions within 45 Days of Filing | 180,601 | 70.1% | 85.4% | 80% |

| Decisions within 90 Days of Filing | 180,601 | 88.4% | 95.5% | 95% (Fiscal Year '02) |

| Higher Authority Appeals Timeliness | ||||

| Decisions within 45 Days of Filing | 14,491 | 91.8% | 62.7% | 50% (Fiscal Year '00) |

| Decisions within 75 Days of Filing | 14,491 | 60.8% | 85.6% | 80% (Fiscal Year '00) |