|

|

|

Print  Download Reader

Download Reader

|

|

|

Print Download Reader

Appendix C - Information on HHS Improper Payment and Recovery Auditing InitiativesNarrative Summary of Implementation Efforts for FY 2005 and Agency Plans for FY 2006 - FY 2008 The Improper Payments Information Act of 2002 (IPIA) requires that Federal agencies annually review all programs and activities that it administers and identify all such programs and activities that may be susceptible to significant improper payments. For high-risk programs, the IPIA requires that various information related to its improper payment activities be reported on annually. The Office of Management and Budget (OMB) issues guidance for reporting on improper payment activities in the Performance and Accountability Report (PAR). In accordance with the IPIA and OMB guidance, the following information is being provided. I. Describe your agency’s risk assessment(s), performed subsequent to compiling your full program inventory. List the risk-susceptible programs (i.e., programs that have a significant risk of improper payments based on OMB guidance thresholds) identified through your risk assessments. Be sure to include the programs previously identified in the former Section 57 of OMB Circular A-11. HHS developed a risk assessment model in FY 2003 to be used Department-wide in conducting program risk assessments of its programs as required under the IPIA. During FY 2004 and FY 2005, HHS worked with the OMB, a contractor with expertise in risk analysis, and the HHS Office of Inspector General (OIG) to address any potential deficiencies in the model and/or identify where the model might be strengthened. Program risk assessments were completed for FY 2005. While HHS did not identify any high-risk programs in its FY 2005 risk assessment work, seven HHS programs were previously identified as high-risk programs in OMB Circular A-11, Section 57. These seven programs are: Medicare, Medicaid, State Children’s Health Insurance Program (SCHIP), Temporary Assistance for Needy Families (TANF), Foster Care, Head Start and Child Care. The sections below contain information on HHS activities related to estimating and reducing improper payments in these programs. II. Describe the statistical sampling process conducted to estimate the improper payment rate for each program identified. A. Medicare- The Medicare fee-for-service (FFS) improper payment estimate is derived from two programs: the Comprehensive Error Rate Testing (CERT) Program and the Hospital Payment Monitoring Program (HPMP). Each component represents about 50 percent of the total FFS Medicare payments. The CERT Program calculates the error rate for Carriers, Durable Medical Equipment Regional Carriers, and non-Prospective Payment System (PPS) inpatient Part A claims submitted to Fiscal Intermediaries (FIsFish). The HPMP calculates the error rate for PPS inpatient hospital claims submitted to the FIsFish. The methodology includes:

B. Medicaid - Twenty-four states determined Medicaid payment accuracy rates in year three of the Payment Accuracy Measurement (PAM) Pilot. All 24 states determined payment accuracy rates for the FFS component and 12 states also determined payment accuracy rates for the Managed Care (MC) component. In the FFS component, the states conducted three types of reviews�medical, data processing, and eligibility�and categorized improper payments found through the reviews using the same error codes. In the MC component, processing and eligibility reviews were performed, but no medical reviews were conducted. States drew a proportional, stratified random sample of Medicaid claims across the major service categories. All states used a standard methodology and the same formula to compute the payment accuracy rates. Samples were drawn from a universe of all Medicaid FFS claims and MC capitation payments paid by the states from October 1 through December 31, 2003 (the first quarter of FY 2004). C. State Children’s Health Insurance Program (SCHIP) - Fifteen states determined SCHIP payment accuracy rates in year three of the PAM Pilot. Of the 15 states that measured SCHIP payment accuracy rates in FY 2004, ten states reviewed FFS components, seven states reviewed MC components; one state only reviewed eligibility; and three states reviewed both FFS and MC components. In the FFS component, states conducted three types of reviews�medical, data processing, and eligibility�and categorized improper payments found through the reviews using the same error codes. In the MC component �processing and eligibility reviews were performed, but no medical reviews were conducted. Samples were drawn from a universe of all SCHIP FFS claims and MC capitation payments paid by the states from October 1 through December 31, 2003. Each state had the option of designing the sample to achieve 3 percent precision at the 95 percent confidence level or 4 percent precision at the 90 percent confidence level for the FFS and MC components. All states used a standard methodology and the same formula to compute the accuracy rate. D. Temporary Assistance for Needy Families (TANF) - The extensive flexibility of state TANF Program operations and the prohibitions on data collection in the TANF legislation have continued to present challenges to identifying an effective and cost efficient methodology for measuring improper payments in the TANF Program. However, during FY 2005 HHS continued to engage in various activities to identify and reduce improper payments in the TANF Program. These activities include: Information Sharing - HHS developed a survey instrument to solicit information from states on state systems and practices for identifying and reducing improper payments in the TANF Program. States are being asked to voluntarily provide information on how they define improper payments, the process (es) used to identify such payments, and what actions are taken to reduce or eliminate improper payments. A repository for this information will be posted on an HHS/ACF website and will be available for viewing by all states. Public Assistance Reporting Information System (PARIS) - The PARIS is a voluntary project that enables participating states’ public assistance data to be matched against several databases to help maintain program integrity and detect and deter improper payments in several programs (TANF, Medicaid and U.S. Department of Agriculture’s Food Stamp Program). HHS engaged in a number of activities to improve data match capability and usefulness and increase state utilization of PARIS. These activities included engaging in outreach activities to encourage states to participate in the PARIS match process; making a conference contract award to enable all PARIS participating states to meet in Washington, DC for HHS training in utilizing the PARIS to its fullest capability; and making an award to a contractor to evaluate the PARIS, formulate recommendations for improving and enhancing its usefulness, and develop a uniform reporting format. TANF A-133 Audit Pilot - During FY 2005, HHS obtained agreement from one state to engage in a pilot to undergo a more in-depth review of TANF expenditures as part of its audit required under OMB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations. The objective of the pilot is to explore the viability of estimating improper payments in the A-133 audit process. In the expanded A-133 audit, the auditors used a statistical sample of a fixed size for a test of controls (attribute sampling method). The auditors reviewed 208 TANF cases to achieve a 95 percent confidence level with an expected deviation rate of 2.25 percent. E. Foster Care - Title IV-E Foster Care eligibility reviews, promulgated in regulations at 45 CFR 1356.71(c), are conducted to ensure that Federal title IV-E funds are used only for eligible children who are placed with eligible providers. Since FY 2000, HHS has systematically conducted more than 70 title IV-E reviews in 50 states, the District of Columbia, and Puerto Rico. HHS determined an estimate of improper payments for the title IV-E Foster Care Program using the data collected in these reviews as well as data from state quarterly fiscal reports from FY 2001 to FY 2004. During these reviews, a team comprised of Federal and state staff validates the accuracy of a state’s IV-E claims for reimbursement of payments made on behalf of eligible children placed in eligible homes and institutions.Each review specifies the number of error cases and amount of payment errors determined from the review of a sample drawn from the state’s overall title IV-E caseload for its six-month Period Under Review (PUR). An error case is defined as a case in which a payment is made on behalf of an ineligible child during the PUR . Payment errors may include payments for error cases, “ineligible” payments made to non-error cases which failed to meet an eligibility criterion outside the PUR, and “unallowable” payments for services not covered by title IV-E (e.g. therapy). F. Head Start - HHS is legislatively required to perform reviews of each Head Start Program every three years. In the conduct of these reviews in FY 2004 and FY 2005, various data was collected to determine an estimate of improper payments for these years. A payment error is defined as a payment for an enrolled child from a family whose income exceeds the allowable limit (in excess of the 10 percent program allowance for families above the income limit). Fifty programs were selected from the population of programs scheduled for review in FY 2005. An appropriate sampling strategy was utilized to determine the number of children’s records to be pulled for each of the 50 selected programs to result in an estimate at plus or minus 2.5 percent precision at a 90 percent confidence interval. G. Child Care - The complexity of the Child Care and Development Fund (CCDF) and the broad flexibility that the states have in the design and administration of the Program have presented challenges in identifying a methodology for estimating improper payments in the Program. However, during FY 2004, HHS initiated an improper payment pilot project to assess the efforts of several states to prevent and reduce improper payments in their Child Care Programs. Eleven states worked with HHS in assessing the adequacy of state systems, databases, policy, and administrative structures to detect, prevent, and identify payment errors in the Child Care Program. In FY 2005, HHS expanded state participation from 11 to 18. As part of the pilot project, site visits were conducted in four states during FY 2005. These visits studied client eligibility, specifically, the states’ ability to verify information received from clients during the initial eligibility process or otherwise to establish eligibility correctly. For this four-state error rate study, a research team used a random sampling approach to select a sample of 150 children per state for review, which provided a statistical basis for a 90 percent confidence interval of +/- 6 percent.. In addition, interviews were conducted with five other states to gather information about improper payment activities in those states. During FY 2006, HHS will be continuing to work with the states to identify an appropriate strategy for determining estimates of payment errors in the Child Care Program. III. A. Explain the corrective actions your agency plans to implement to reduce the estimated rate of improper payments. Include in this discussion what is seen as the cause(s) of errors and the corresponding steps necessary to prevent future occurrences. If efforts are already underway, and/or have been ongoing for some length of time, it is appropriate to include that information in this section. B. For grant-making agencies with risk susceptible grant programs, discuss what your agency has accomplished in the area of funds stewardship past the primary recipient. Include the status on projects and results of any reviews. A. Medicare - A significant problem among the FY 2004 findings was a high insufficient-documentation rate by providers. To address the insufficient-documentation problem, HHS took the following steps during FY 2005:

Based on the FY 2004 findings, HHS has identified and initiated the following corrective actions during FY 2005:

As a result of these actions, the Medicare paid claims error rate decreased from 10.1 percent ($21.7 billion in gross payments), to 5.2 percent ($12.1 billion in gross payments) from FY 2004 to FY 2005. The FY 2005 paid claims error rate of 5.2 percent exceeded HHS’ Medicare Fee for Service Contractor Error Rate GPRA goal of 7.9percent. Because of this dramatic improvement, HHS has revised its GPRA goals for 2006 and beyond as follows:

(Part B of this section is not relevant to the Medicare Program.) B. Medicaid - HHS has worked closely with each state participating in the PAM pilot to develop and implement a methodology for estimating payment error rates in the Medicaid Program for all states. HHS will provide recommendations for state corrective action plans based on the results of the PAM year three pilot. The emphasis of the pilot was for each state to individually measure the payment accuracy of its program since the Medicaid Program is unique to each state. HHS expects that each state will continue to identify and implement corrective action measures based on the results of the pilot projects and the states own experiences with its Medicaid Program. HHS has also engaged in other activities. The Health Care Fraud and Abuse Control (HCFAC) account includes at least two projects (the hiring of 100 staff positions to do prospective reviews of state Medicaid operations, and the Medicare/Medicaid data match program) designed to identify improper payments and areas in need of improved payment accuracy. The HHS OIG also continues to receive money from the account to conduct audits on the Medicaid Program. (Part B of this section is not relevant to the Medicaid Program.) C. State Children’s Health Insurance Program (SCHIP) - HHS has worked closely with each state participating in the PAM pilot to develop and implement a methodology for estimating payment error rates in the SCHIP Program for all states. HHS will provide recommendations for state corrective action plans based on the results of the PAM year three pilot. The emphasis of the PAM pilots was for each state to individually measure the payment accuracy of its program since the SCHIP Program is unique to each state. HHS expects that each state will continue to identify and implement corrective action measures based on the results of the pilot projects and the states own experiences with its SCHIP Program. (Part B of this section is not relevant to the SCHIP Program.) D. Temporary Assistance for Needy Families (TANF) - HHS has not yet identified or developed a methodology for determining an estimate of payment errors. However, as noted in Section II.D, HHS is engaging in various activities to identify and reduce improper payments in the TANF Program. HHS policies and procedures for subrecipient monitoring and oversight are consistent with what is allowed by the TANF legislation and related program and grant regulations and provided for in OMB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations. E. Foster Care - In an analysis of the improper payments that were identified, HHS determined that six types of eligibility errors were found more than 50 times across these samples and accounted for 84 percent of all errors found in the title IV-E reviews. The frequency of the remaining types of eligibility errors ranged from 1 to 36, with most of the error types occurring 12 or fewer times across all samples. The most frequently occurring errors are:

Since nearly 70 percent of states were found to have at least one provider licensing/approval error, ensuring that title IV-E Foster Care children are placed with licensed approved providers appears to be the most common challenge across states receiving title IV-E funds. The states compliance in meeting the requirements necessary for Federal financial participation in the title IV-E Program is monitored through the existing protocol associated with the title IV-E Foster Care eligibility reviews, promulgated in regulations at 45 CFR 1356.71(c). Related activities include:

The PIP must be developed by state staff in consultation with Federal staff and must include the following components:

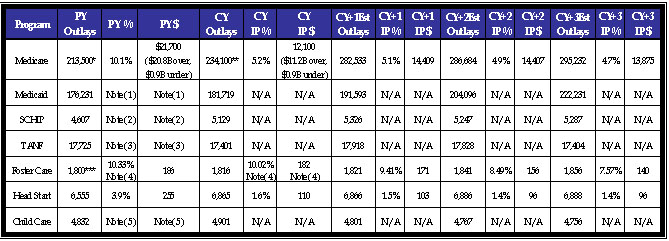

HHS policies and procedures for subrecipient monitoring and oversight are consistent with what is allowed by the Foster Care legislation, related program and grant regulations, and provided for in OMB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations. F. Head Start - During FY 2005, HHS undertook various actions to address the causes attributed to the improper payments identified and reported on in the FY 2004 PAR. To improve recruiting and enrollment practices, an Information Memorandum was sent to all programs reiterating the need to adhere to 45 CFR 1305, “Eligibility, Recruitment, Selection, Enrollment and Attendance in Head Start.” Further, HHS added to the FY 2005 Program Review Instrument for Systems Monitoring Guide a requirement that the teams review a sample of children’s files using the same data collection form which is used in the reviews conducted for the purpose of estimating payment errors. As a result of these actions, the Head Start payment error rate decreased from 3.9 percent in FY 2004 to 1.6 percent in FY 2005. In FY 2006, HHS will continue to require examination of a sample of files to obtain information regarding the Program’s compliance with income eligibility program requirements as part of all reviews conducted under 45 CFR 1305. HHS policies and procedures for subrecipient monitoring and oversight are consistent with what is allowed by the Head Start legislation, related program and grant regulations, and provided for in OMB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations. G. Child Care - HHS identified potential sources of payment error in the states participating in the Child Care pilot (discussed in Section II.G.). HHS and the states are working together to address potential errors identified during pilot activities. HHS policies and procedures for subrecipient monitoring and oversight in the Child Care and Development Fund (CCDF) are consistent with what is allowed by the Child Care legislation, related program and grant regulations, and provided for in OMB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations. Primary recipients of CCDF funds are lead agencies from states, territories, and Tribes, usually the Department of Human Services, Human Resources, Social Services or Workforce Development. Subrecipients include, but are not limited to, Child Care Resource and Referral Agencies, Community Action Agencies, contracted providers, and agencies responsible for administering quality dollars or other earmarked funds. HHS receives biennial CCDF plans and regular reports from states, territories, and Tribes that detail how they implement the CCDF Program, how they spend their allotment of CCDF funds, and the nature of services provided (i.e., children and families served, number and types of providers). Through review of these plans and reports, staff monitors the performance of grantees and work with grantees where problems arise. In addition, formal complaints are investigated as they are received, according to procedures set by the CCDF regulations. IV. The table below is required for each reporting agency. Please note the following changes from prior year reporting: (1) all risk susceptible programs must be listed in this chart whether or not an error measurement is being reported; (2) where no measurement is provided, agency should indicate the date by which a measurement is expected; (3) if the Current Year (CY) is the baseline measurement year, indicate by either footnote or by “n/a” in the Prior Year (PY) column; (4) if any of the dollar amount(s) included in the estimate correspond to newly established measurement components in addition to previously established measurement components, separate the two amounts to the extent possible; (5) include outlay estimates for CY +1, +2, and +3; and (5) agencies are expected to report on CY activity, and if not feasible, then PY activity is acceptable. Future year outlay estimates (CY+1, +2 and +3) should match the outlay estimates for those years as reported in the most recent President’s Budget . Note that over-and under-payments should be indicated if this information is available. The absolute value of the dollars and the rates should be shown - do not net the figures. Improper Payment Reduction Outlook FY 2004 - FY 2008

* PY Outlays for Medicare FFS are from the November 2004 Improper Medicare FFS Payments Report (which were based on CY 2003 claims) ** CY Outlays for Medicare FFS are from the November 2005 Improper Medicare FFS Payments Report (which were based on FY 2005 claims) *** FY 04 Outlays of $4,404 reported in the FY 2004 PAR for the Foster Care Program included administrative costs. Since the payments reviewed in determining the estimated FY 2004 and FY 2005 estimated error rates did not include administrative costs, the PY outlay amount was revised to reflect maintenance payments only. NOTE:

V. Discuss your agency’s recovery auditing effort, if applicable, including any contract types excluded from review and the justification for doing so; actions taken to recoup improper payments, and the business process changes and internal controls instituted and/or strengthened to prevent further occurrences. In addition, complete the table below. During FY 2004, HHS implemented a Department-wide recovery auditing program as required by Section 831 of the Defense Authorization Act of 2002. This includes awarding a contingency fee contract to a recovery auditing firm in June 2004. During FY 2005, the recovery auditing firm completed its review of a substantial portion of the $11.1 billion of FY 2002 and FY 2003 contract payment transactions subject to review. Although the auditors identified $2.1M of potential improper payments, $1.3M was determined to be related to payment that were voided and/or for which credits had already been applied. HHS is working on recovering $0.8 of payments determined to be improper. Also, HHS is required under the Medicare Prescription Drug Improvement Modernization Act of 2003 (MMA) to conduct a demonstration project to demonstrate the use of recovery audit contractors under the Medicare Integrity Program in identifying underpayments and overpayments and recouping overpayments under the Medicare Program for services for which payment is made under Part A or B of title XVIII of the Social Security Act. One of the outcomes of this demonstration is to see if the recovery auditing contractors can help lower the error rates in these states by (1) improving provider compliance more quickly than states that do not have recovery auditing contractors, and (2) allowing regular contractors to spend fewer resources on post-payment review and focus more time and effort on prepayment review and education. HHS is conducting the demonstration in the three states with the highest Medicare utilization rates and has committed administrative dollars to creating a database to facilitate communication and to track the progress of the demonstration. The recovery audit contractors have been given almost one billion claims that Medicare paid between FY 2002 and 2004 and the recovery auditors are tasked with reviewing these claims to determine improper payments. Each fiscal year the recovery auditor will receive the prior fiscal years’ paid claims. The recovery auditors will use complex medical review and proprietary software to complete their analysis. HHS is committed to tracking the progress of the demonstration and to using the information to improve the claim payment accuracy rate. At the end of FY 2005, the demonstration was still in the start-up phase and recovery information was not yet available.

VI. Describe the steps the agency has taken and plans to take (including time line) to ensure that agency managers (including the agency head) are held accountable for reducing and recovering improper payments. HHS is issuing interim scorecard ratings for the HHS Operating and Staff Divisions, which have helped facilitate HHS leadership discussion and accountability on the improper payment initiatives. Further, in FY 2004, HHS performance plan objectives were established which require that managers “identify and address weaknesses in grant systems(s), procurement systems(s) and finance offices to ensure recovery of improper payments and to reduce the number of improper payments by the Department.” Similar performance plan objectives were included in FY 2005 and 2006 performance plans. A. Describe whether the agency has the information systems and other infrastructure it needs to reduce improper payments to the levels the agency has targeted. B. If the agency does not have such systems and infrastructure, describe the resources the agency requested in its FY 2006 budget submission to Congress to obtain the necessary information systems and infrastructure. A. Medicare - HHS has the information systems and other infrastructure it needs to reduce improper Medicare FFS payments to the levels that HHS has targeted. HHS has several systems that contain information that allows it to identify developing and continuing aberrant billing patterns based upon a comparison of local payment rates with state and national rates. All the systems, both at the contractor level and at the central office level, are tied together by a high-speed secure network that allows rapid transmission of large data sets between systems. Transmissions are made nightly and include all claims processed during the preceding day. B. Medicaid- HHS will be implementing the Payment Error Rate Measurement (PERM) Program in FY 2006 using a national contractor to determine state Medicaid FFS payment error rates. The information systems and other infrastructure that would be valuable to HHS in reducing improper payments will not be known until implementation is near or at completion and actual results become available. C. State Children’s Health Insurance Program (SCHIP) - HHS expects to begin measuring SCHIP error rates in FFS, MC, and eligibility components in FY 2007. The information systems and other infrastructure that would be valuable to HHS in reducing improper payments will not be known until implementation of the measurement plan is near or at completion and actual results become available D. Temporary Assistance for Needy Families (TANF) - HHS has not yet developed a methodology for estimating payment errors in the TANF Program and therefore has not established reduction targets. E. Foster Care - HHS usesthe Adoption and Foster Care Analysis and Reporting System for the regulatory reviews. Utilizing this existing source of data reduces the burden on states to draw their own samples, promotes uniformity in sample selection, and employs the database in a practical and beneficial manner. No other systems or infrastructure are needed at this time. F. Head Start - HHS has the information systems and infrastructure needed to reduce improper payments to the levels that HHS has targeted for the Head Start Program. G. Child Care - HHS has not yet developed a methodology for estimating payment error in the Child Care Program and therefore has not established reduction targets. VIII. Describe any statutory or regulatory barriers which may limit the agencies’ corrective actions in reducing improper payments and actions taken by the agency to mitigate the barriers’ effects. A. Medicare - No statutory or regulatory barriers have been identified. B. Medicaid - During the pilot projects, states administered on a voluntary basis the Medicaid payment error measurement for each participating state, which was the basis for calculating the Medicaid improper payment estimates. HHS adopted a national contracting strategy with expected implementation beginning in FY 2006. Because states administer the Medicaid and SCHIP Programs, the ability of HHS to obtain state compliance is limited in the absence of statutory authority to hold states accountable for meeting targets for the reduction and recovery of improper payments. C. State Children’s Health Insurance Program (SCHIP) - During the pilot projects, states administered on a voluntary basis the SCHIP payment error measurement for each participating state, which was the basis for calculating the SCHIP improper payment estimates. HHS adopted a national contracting strategy with expected implementation beginning in FY 2006. In FY 2007, CMS expects to begin measuring SCHIP error rates in FFS, MC, and eligibility components. Because states administer the Medicaid and SCHIP Programs, the ability of HHS to obtain state compliance is limited in the absence of statutory authority to hold states accountable for meeting targets for the reduction and recovery of improper payments. D. Temporary Assistance for Needy Families (TANF) - HHS has not yet developed a methodology for estimating payment errors in the TANF Program which would lend itself to the identification of appropriate corrective action measures for the Program as a whole. In the activities it is undertaking to develop a methodology, HHS is addressing corrective action on a case-by-case basis. E. Foster Care - Current program regulations definethe sample size, the extrapolation of a disallowance following the primary review, and the current corrective action process. Any proposed changes in the compliance framework or current methodology for estimating improper payments would need to be made available for public comment through the rulemaking process and a final rule published prior to implementation. F. Head Start - No statutory or regulatory barriers have been identified. G. Child Care - HHS has not yet developed a methodology for estimating payment errors in the Child Care Program which would lend itself to the identification of appropriate corrective action measures for the Program as a whole. In the activities it is undertaking to develop a methodology, HHS is addressing corrective action on a case-by-case basis. IX. Additional comments, if any, on overall agency efforts, specific programs, best practices, or common challenges identified, as a result of IPIA implementation. HHS has been a leader in the area of monitoring and mitigating improper payments. In FY 1996, the HHS OIG began estimating improper payments in the Medicare FFS Program. In FY 2002, the Department took over the work and under a new error rate measurement methodology, the CERT HPMP, improved on the process and began obtaining more detailed management information. This new level of detail has been extremely valuable in identifying the causes for improper payments in the Medicare FFS Program and for determining the corrective action needed to reduce the error rate. In FY 2005, HHS reduced the Medicare paid claims error rate from 10.1 percent ($21.7B in gross payments), to 5.2 percent ($12.1B in gross payments) from FY 2004 to FY 2005. This rate reduction exceeds the HHS FY 2005 targeted reduction rate of 7.9 percent. HHS also experienced successes in addressing improper payments in other programs. In the Head Start Program, HHS also experienced a significant decline in the payment error rate; from 3.9 percent to 1.6 percent from FY 2004 to FY 2005. Again, HHS exceeded the established reduction target (3.5 percent). In the Foster Care Program, HHS developed a methodology for estimating improper payments and is reporting a payment error rate for the first time. Both the FY 2004 actual rate and preliminary FY 2005 rate are being reported on. HHS will be implementing the Payment Error Rate Measurement (PERM) Program in FY 2006 using a national contractor to determine date Medicaid FFS payment error rates for medical error and data processing error. Further, work toward developing and implementing methodologies for other SCHIP and other components of Medicaid will be continuing throughout FY 2006. In the TANF and Child Care Programs, HHS engaged in numerous activities to identify and reduce improper payments. Since these are block grant programs where program legislation allows states maximum flexibility in operating its programs, it has been difficult to define error in a way that has meaning across the states. Further, there are barriers to requesting information and/or requiring participation in improper payment activities. Although it has been most challenging in identifying effective and cost efficient approaches for estimating payment errors in these programs, HHS is engaging in numerous activities working toward identification of appropriate strategies for estimating improper payments in these programs. While the successes that HHS has been able to achieve in its improper payment initiatives are due to a number of reasons, two stand out. First, HHS leadership recognizes the importance of these initiatives in its overall stewardship responsibilities and has played an active role in ensuring the improper payment initiatives are appropriately prioritized and that related performance objectives are met. Second, HHS leadership recognizes the value of what the HHS OIG and the OMB can contribute to the HHS initiatives as it develops and implements strategies and has ensured that they are consulted appropriately as the work progresses. The commitment and involvement of HHS leadership has been instrumental to the progress HHS has been able to achieve in its improper payment initiatives. In FY 2006, HHS hopes to overcome the challenges it faces in estimating payment errors in the TANF and Child Care Programs. Further, HHS will be working toward reducing payment errors for not only those programs where it is undertaking PMA improper payment activities, but also where it identifies any opportunity in the course of financial and program operations. |