Legislation and Regulations

Because analyses by EIA are required to be policy-neutral, the projections in AEO2008 are based on Federal and State laws and regulations in effect on or before December 31, 2007. The potential impacts of pending or proposed legislation, regulations, and standards—or of sections of legislation that have been enacted but that require implementing regulations or appropriation of funds that are not provided or specified in the legislation itself—are not reflected in the projections. Throughout 2007, however, at the request of the Administration and Congress, EIA has regularly examined the potential implications of proposed legislation in Service Reports (see "EIA Service Reports on Proposed Legislation Released Since January 2007").

Examples of Federal and State legislation incorporated in AEO2008 include:

• EISA2007, signed into law on December 19, 2007, which (a) includes an expanded RFS requiring the use of 36 billion gallons of ethanol by 2022; (b) creates an attribute-based minimum CAFE standard of 35 mpg by 2020 for cars and trucks; (c) establishes a program of CAFE credit trading and transfer; (d) extends and then phases out the CAFE credits established under the Alternative Motor Fuels Act of 1988 (AMFA); (e) creates various appliance efficiency standards; (f) establishes a lighting efficiency standard starting in 2012; (g) requires industrial electric motors to meet the premium motor efficiency standards of the National Electrical Manufacturers Association (NEMA); and (h) creates or enhances a number of other programs related to industrial waste heat or natural gas efficiency, energy use in Federal buildings, weatherization assistance, and manufactured housing (see below for more detailed discussion of the provisions in EISA2007 and their handling in AEO2008)

• The provisions of EPACT2005 that remain in effect and have not been superseded by EISA2007, including: mandatory energy conservation standards; numerous tax credits for businesses and individuals; elimination of the oxygen content requirement for Federal reformulated gasoline (RFG); extended royalty relief for offshore oil and natural gas producers; authorization for DOE to issue loan guarantees for new or improved technology projects that avoid, reduce, or sequester GHGs; a PTC for new nuclear facilities; and extension and expansion of the PTC for electricity generated from renewable fuels

• The Military Construction Appropriations Act of 2005, which contains provisions to support construction of the Alaska natural gas pipeline, including Federal loan guarantees during construction

• The Working Families Tax Relief Act of 2004, which includes tax deductions for qualified cleanfuel and electric vehicles and changes in the rules governing oil and natural gas well depletion

• The American Jobs Creation Act of 2004, which includes incentives and tax credits for biodiesel fuels and a modified depreciation schedule for the Alaska natural gas pipeline

• State RPS programs, including the California RPS passed on September 12, 2002 • The Clean Air Act Amendments of 1990 (CAAA- 90), which included new standards for motor gasoline and diesel fuel and for heavy-duty vehicle emissions

• The National Appliance Energy Conservation Act of 1987

• State programs for restructuring of the electricity industry.

Examples of Federal and State regulations incorporated in AEO2008 include the following:

• The Mobile Source Air Toxics rule released by the EPA on February 9, 2007 (MSAT2), which establishes controls on gasoline, passenger vehicles, and portable fuel containers designed to significantly reduce emissions of benzene and other hazardous air pollutants [7]

• New stationary diesel regulations issued by the EPA on July 11, 2006, which limit emissions of nitrogen oxides (NOx), particulate matter, sulfur dioxide (SO2), carbon monoxide, and hydrocarbons to the same levels required by the EPA’s nonroad diesel engine regulations.

More detailed information on recent legislative and regulatory developments is provided below.

Energy Independence and Security Act of 2007: Summary of Provisions

The Energy Independence and Security Act of 2007 was signed into law on December 19, 2007, and became Public Law 110-140 [8]. Provisions in EISA2007 that require funding appropriations to be implemented, whose impact is highly uncertain, or that require further specification by Federal agencies or Congress are not included in AEO2008. For example, EIA does not try to anticipate policy responses to the many studies required by EISA2007, nor to predict the impact of research and development (R&D) funding authorizations included in the bill. Moreover, AEO2008 does not include any provision that addresses a level of detail beyond that modeled in NEMS, which was used to develop the AEO2008 projections. AEO2008 addresses only those provisions in EISA2007 that establish specific tax credits, incentives, or standards, including the following:

• RFS requirements for the use of 36 billion gallons of ethanol per year by 2022, with corn ethanol limited to 15 billion gallons. Any other ethanol or biodiesel may be used to fulfill the balance of the mandate, but the balance must include 16 billion gallons per year of cellulosic ethanol by 2022 and 5 billion gallons per year of biodiesel by 2012.

• A new CAFE standard for LDVs (cars and light trucks) of 35 mpg by 2020. The Act also specifies that vehicle attribute-based standards are to be developed separately for cars and light trucks.

• A CAFE credit and transfer program among manufacturers and across a manufacturer’s fleet.

• Extension through 2019 of the CAFE credits specified under the AMFA. EISA2007 reduces the maximum credit by 0.2 mpg for each model year after 2014 and phases it out entirely by model year 2020.

• Appliance energy efficiency standards for boilers, dehumidifiers, dishwashers, clothes washers, external power supplies, and commercial walk-in coolers and freezers.

• Lighting energy efficiency standards for generalservice incandescent lighting in 2012 and sooner for general-service tubular fluorescent lighting and metal halide lamp fixtures.

• Standards for industrial electric motor efficiency, requiring industrial motors of various sizes to meet the NEMA premium motor efficiency standards.

• Standards for energy use in Federal buildings, requiring a 30-percent reduction by 2015. The following discussion provides a summary of the EISA2007 provisions included in AEO2008 and some of the provisions that could be included if more complete information were available about their funding and implementation. This discussion is not a complete summary of all the sections of EISA2007. More extensive summaries are available from other sources [9].

End-Use Demand

Buildings Sector

EISA2007 affects residential and commercial buildings in three specific areas: appliance and lighting energy efficiency, energy savings in private-sector buildings and industry, and energy savings in government and public institutions.

Appliance and Lighting Energy Efficiency. Subtitles A and B in Title III of EISA2007 include provisions with the potential to affect energy demand in the buildings sector. Many of the provisions give DOE the authority to set new efficiency standards or test procedures for new efficiency standards. Where EISA2007 specifies both efficiency levels and effective dates in the standards, they are implemented directly in the NEMS buildings modules. Where specific appliances and future DOE updates to the standards are not specified, they are not included in AEO2008.

Section 301 provides efficiency standards for external power supplies, limiting wattage in both active and no-load mode for units produced after July 1, 2008. DOE is instructed to review the standards in the future, but only the 2008 standard is included in AEO2008. Section 303 increases the Federal efficiency standard for residential boiler units manufactured after September 1, 2012, providing a small increase (less than 5 percent) over the current standard. Dehumidifiers, clothes washers, and dishwashers are subject to new standards between 2010 and 2012, as provided in Section 311. Energy conservation standards for walk-in refrigerators and walk-in freezers established in Section 312 require energy-efficient elements in the doors, walls, motors, and lighting of units manufactured in 2009 or later. Section 313 amends electric motor efficiency standards, and Section 314 adds single-package vertical air conditioners and heat pumps to the packaged air conditioning and heating equipment covered by the standards in EPACT2005. These two provisions address a level of detail that is not modeled in NEMS, and they are not included in AEO2008.

The largest projected energy savings from EISA2007 are the result of energy conservation standards for efficient light bulbs described in Sections 321, 322, and 324. Section 321 requires significant wattage reductions (approximately 28 percent) in incandescent lamps beginning in 2012, increasing to a reduction of about 65 percent in 2020. Section 322 sets standards for general-service fluorescent lamps and incandescent reflector lamps, and Section 324 imposes minimum ballast efficiency standards for metal halide lamp fixtures beginning in 2009. Section 323 mandates the use of energy-efficient lighting fixtures and bulbs to the maximum extent feasible in all Federal buildings starting in 2009.

Energy Savings in Buildings and Industry. Provisions under EISA2007 Title IV, Subtitle A, address energy efficiency in residential buildings. Section 411 reauthorizes funding for weatherization programs through fiscal year (FY) 2012; however, the program has been targeted for elimination by DOE in its most current budget and therefore is not included in AEO2008. Section 413 requires manufactured housing to comply with the most recent version of the International Energy Conservation Code (IECC) starting in 2012. This provision is included in AEO2008. The 2006 version of the IECC represents the most recent code.

Provisions under Title IV, Subtitle B, establish an office and a partnership consortium to promote high-performance green building initiatives. Section 422 specifically directs the establishment of a Zero Net Energy Commercial Buildings Initiative, with the eventual goal of having all U.S. commercial buildings use zero net energy by 2050. The provision includes several research, development, and deployment activities and authorizes funding for the initiative through 2018. Because the activities depend on future appropriations, they are not included in AEO2008.

Title IV, Subtitle C, addresses Federal energy use, updating energy intensity reduction goals and performance standards for Federal buildings, mandating energy and efficiency management, providing for the development of high-performance green building standards for Federal facilities, and directing the establishment of a program to accelerate Federal use of cost-effective technologies and practices. Federal purchasing requirements for energy intensity reduction and performance standards are represented in AEO2008 as a result of earlier Executive Orders and legislation. Other aspects of these provisions either address a level of detail that is not modeled in AEO2008 or are not included because they depend on future appropriations.

Provisions under the other Subtitles of Title IV address data center efficiency, environmental quality in schools, and sustainability and efficiency grants and loans for institutions. These provisions are not included in AEO2008, because they depend on future appropriations or address a level of detail that is not modeled in NEMS.

Energy Savings in Government and Public Institutions. Title V contains a variety of provisions, including promotion of efficiency and environmental measures for the Capitol complex; promotion and permanent authorization of energy savings performance contracts; standards for Federal purchase of specific technologies; and authorization for funding of State energy programs, utility efficiency incentives, and local energy efficiency block grants. Federal purchasing requirements governing purchases of costeffective energy-efficient products are represented in AEO2008 as a result of earlier Executive Orders and legislation. The provisions in EISA2007 Title V are not included in AEO2008, because they depend on future appropriations or address a level of detail that is not modeled in NEMS.

Industrial Sector

EISA2007 includes several provisions in Titles III and IV that could affect energy demand in the U.S. industrial sector; however, provisions in Title VI, Accelerated Research and Development, that may affect industrial energy consumption over the long term are not included in AEO2008.

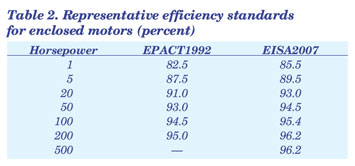

Section 313 of Title III increases or creates minimum efficiency standards for newly manufactured generalpurpose electric motors that must be met within 3 years of enactment (Table 2). Efficiency standards for general-purpose, integral-horsepower induction motors are raised, with the exception of fire pump motors. Minimum standards are created for seven types of poly-phase, integral-horsepower induction motors and NEMA design B motors (201 to 500 horsepower) not covered under the previous standards in the Energy Policy Act of 1992 (EPACT1992). These standards are included in AEO2008 for industrial motor additions.

Sections 451, 452, and 453 direct the EPA to survey all major industrial combustion sources and create a registry of the quantity and quality of waste energy at each site. DOE may provide up to 50 percent of the funding for a feasibility study to determine whether the waste heat can be captured with a 5-year payback. In addition, DOE is authorized to provide grants of nearly $200 million per year to industrial partnerships for research on energy savings. Finally, these sections create a program that collects best practices, designs, processes, and innovations for building energy- efficient data centers. These provisions are not funded and are not included in AEO2008.

Transportation Sector

EISA2007 Title 1, Section 102, requires that the average manufacturer’s fleet fuel economy for cars and light-duty trucks be increased, starting in 2011, to an average of 35 mpg by 2020, based on the EPA test value used to measure compliance with the CAFE standard. The EPA CAFE test value generally differs from the estimated mpg value on the fuel economy label and, typically, exceeds the actual on-the-road fuel economy of a new vehicle by a significant margin. For model years 2021 through 2030, Section 102 specifies that the average fuel economy must be set at the maximum feasible average for each fleet. In AEO2008, fuel economy standards for LDVs are assumed to remain at the 2020 level. AEO2008 includes attribute-based fuel economy standards for light trucks, given vehicle footprint [10] and sales share. It uses these fuel economy curves to achieve the overall fleet fuel economy standard of 35 mpg. The fuel economy standards for cars are not attribute- based, but they apply to the manufacturer’s fleet of both domestic and imported vehicles. In AEO2008, the fuel economy standard for cars is assumed to increase from 27.5 mpg in 2010 to 41.0 mpg in 2020. For light trucks, the footprint-based average fleet fuel economy standard increases from 24.0 mpg in 2011 to 31.0 mpg in 2020.

Section 103 requires the development of fuel economy standards for work trucks—8,500 pounds to less than 10,000 pounds gross vehicle weight rating (GVWR)— and commercial medium- and heavy-duty on-highway vehicles (GVWR 10,000 pounds or more). The new fuel economy standards require consideration of vehicle attributes and duty requirements and can prescribe standards for different vehicle classes, such as buses used in urban operation or semi-trucks used primarily in highway operation. Section 103 provides a minimum lead time of four full model years before the new fuel economy standard is adopted, and a minimum of three full model years after the new fuel economy standard has been established before the fuel economy standards for work trucks can be modified. Because these fuel economy standards are pending, and because NEMS currently does not model fuel economy regulations for work trucks or commercial medium- and heavy-duty vehicles, this aspect of EISA2007 is not included in AEO2008.

Section 104 establishes a fuel economy credit trading program. Currently, CAFE credits earned by manufacturers can be banked for up to 3 years and can be applied only to the fleets (car or light truck) from which the credits were earned. Starting in model year 2011, the credit trading program will allow manufacturers whose vehicles exceed the minimum fuel economy standards to earn credits that can be sold to other manufacturers whose vehicles fail to achieve the prescribed standards. The credit trading program is designed to ensure that the total fuel savings for manufacturers exceeding the prescribed standards are preserved when credits are sold to manufacturers not achieving the standards.

The credit trading program begins in 2011, and EISA2007 allows manufacturers to apply credits earned to any of the three model years before the model year for which they are earned and to any of the five model years after the credits are earned. Credit transfers within a manufacturer’s fleet are limited to specific maximums: 1.0 mpg for model years 2011 through 2013, 1.5 mpg for model years 2014 through 2017, and 2.0 mpg for model years 2018 and later. NEMS currently allows for sensitivity analysis of CAFE credit banking by manufacturer fleet but does not model the trading of credits among different manufacturers. Consequently, AEO2008 does not include trading of fuel economy credits.

Section 109 extends the CAFE credits specified under AMFA through 2019. Before the passage of EISA-2007, the CAFE credits under AMFA were scheduled to expire after model year 2010. Currently, 1.2 mpg is the maximum CAFE credit that can be earned for selling alternative-fuel vehicles. EISA2007 extends the 1.2 mpg credit maximum through 2014 and reduces the maximum by 0.2 mpg for each following year until it is phased out by model year 2020. NEMS currently does not model CAFE credits earned from alternative-fuel vehicles sales, and AEO2008 does not consider this section of EISA2007.

Petroleum, Ethanol, and Biofuels

This section summarizes the numerous provisions of EISA2007 affecting the supply, composition, and refining of petroleum and related products that are included in AEO2008.

Renewable Fuels Standard

EISA2007 Title II, in Subtitles A and B, includes an updated RFS that increases the requirement for total U.S. consumption of renewable fuels from the 7.5 billion gallons in 2012 as specified in EPACT2005 to 36 billion gallons in 2022. Mandates are set for specific types of renewable fuels, including both conventional biofuels (corn-based ethanol) and advanced biofuels that are not derived from corn starch (such as cellulosic ethanol, butanol, or diesel products and biomass-based diesel [11].

The advanced biofuel requirement comes into effect in 2009 at 0.6 billion gallons and rises to 21 billion gallons in 2022. In 2015 and thereafter, the maximum amount of corn-based ethanol that can be applied to the overall RFS is 15 billion gallons. The cellulosic biofuel requirement starts in 2010 at 0.1 billion gallons and rises to 16 billion gallons in 2022. The biomass- based diesel requirement begins at 0.5 billion gallons in 2009 and rises to 1 billion gallons in 2012, with the remaining years to be determined by the EPA Administrator.

EISA2007 also establishes a life-cycle GHG standard for biofuels. The GHG standard for all biofuels is based on the 2005 emission level for the particular type of transportation fuel. Corn-based ethanol must achieve a 20-percent reduction in life-cycle GHG emissions, which would disqualify future corn ethanol production facilities that use coal for process heat. In addition to being defined as not being derived from corn starch, advanced biofuels are further defined as any renewable fuels that reduce emissions by at least 50 percent. Finally, 60 percent or more of the reduction in emissions must be achieved before any cellulosic biofuel can qualify under that category.

Given uncertainty about whether the new RFS schedule can be achieved, EISA2007 contains a general waiver based on technical, economic, or environmental feasibility. In addition, the cellulosic biofuel mandate includes a credit program that is activated only in years when the mandated level of cellulosic biofuel is judged by the EPA Administrator as unlikely to be met. For all the fuel mandates, if there is a 20-percent deficit in more than two consecutive years or a 50-percent deficit in any one year, regulatory adjustment mechanisms are provided to lower the mandated levels from that point forward. This rule, which could be enacted by the EPA Administrator no sooner than 2016, would modify all applicable volumes (including the overall and advanced biofuel totals) for all subsequent years.

The RFS is included in AEO2008, with cellulosic biofuel credit and waiver provisions that are consistent with those in the existing law. Actual renewable fuel supplies in any year are allowed to exceed the minimum RFS requirements, depending on the availability of technology and feedstocks and the relative costs of renewable fuels and competing petroleum products. Because the RFS does not explicitly specify the level of the mandate after 2022, AEO2008 assumes that it will remain at the 2022 level through 2030.

In order to achieve the biofuel consumption levels mandated in EISA2007, significantly more biofuels must be consumed than can be blended into gasoline as E10. Other than requiring studies involving ethanol pipelines and similar infrastructure issues, EISA2007 does not directly provide for infrastructure improvements that may be necessary. In AEO2008, the amount of ethanol in excess of what can be consumed in E10 is assumed to be used in E85. Flexiblefuel vehicles are assumed to be available in sufficient numbers to use the required amounts of E85, and E85 distribution infrastructure is assumed to be built over a technically practicable period. The infrastructure development costs are spread across all transportation fuels.

E85 infrastructure costs potentially could be reduced if biobutanol or ethanol-gasoline blends containing more than 10 percent ethanol (other than E85) were able to meet a significant portion of the RFS; however, AEO2008 assumes that neither will actually contribute to meeting the EISA2007 mandates. At present there is little commercial activity for biobutanol, and only a few tests are under way [12]. Automakers and engine manufacturers are concerned about ethanol-related problems in vehicles built to run on gasoline blends no higher than E10, because higher ethanol blends are corrosive to engines not designed to handle them, and their use could adversely affect performance and cause vehicle warranties to be voided [13].

Amortization of Geological and Geophysical Expenditures

EISA2007 extends the 5-year amortization period for geological and geophysical expenditures by major integrated oil companies to 7 years as of the enactment of the bill. Because the NEMS oil and gas supply model does not directly represent geological and geophysical expenditures, this change is not included in AEO2008.

Electricity

EISA2007 includes few provisions that affect electricity generation or transmission. Title XIII, Smart Grid, promotes a modernization of the electricity transmission and distribution system to strengthen reliability and energy efficiency. Funding is provided for research and demonstration projects, as well as matching funds for qualifying investments. States are to encourage, but not require, utilities to adopt smart grid technology and allow them to recover their costs through rate increases. The bill does not include enough specific information to support NEMS projections of changes in investment or prices for electricity transmission and distribution, but it is implicitly assumed in AEO2008 that electricity will be provided reliably.

Coal

Industries that rely on coal could benefit from EISA- 2007 Title VII, Carbon Capture and Sequestration, if CO2 emissions are restricted in the future. Sections 702 through 711 expand authorized funding and provide greater detail on the carbon capture and development program originally established in EPACT2005, Section 963. EISA2007 Sections 702 through 711 are not included in AEO2008, because the authorized funds have not been appropriated and the effects of the included research, development, and other projects are uncertain.

Section 702 authorizes $240 million per year from 2008 through 2012 for carbon sequestration projects, an increase from the amount authorized in EPACT- 2005. Among the R&D programs supported under Section 702 are the development of a minimum of seven large-scale geologic sequestration projects, with each project capable of injecting at least 1 million tons of CO2 annually. Geologic formations that potentially could be used for sequestration include operating or depleted oil and natural gas fields, unmineable coal seams, deep saline or basalt formations, and deep geologic resources from which economical geothermal heat is extracted. Monitoring, mitigation, and verification of CO2 containment are also required under Section 702.

Section 703 authorizes additional funding of $200 million per year from 2009 through 2013 for R&D projects focused on capture, purification, compression, transportation, and injection of CO2 emitted from industry sources. In the decision to undertake Section 703 projects, the Secretary of Energy may prioritize projects that include sequestration programs described under Section 702; however, integration is not a requirement for funding. As noted above, these R&D provisions are not included in AEO2008.

Section 706 recognizes that the CCS program must adhere to the Safe Drinking Water Act. Additional provisions in EISA2007 authorize funds for the education and training of individuals to work in the CCS field. None of these provisions is specifically reflected in AEO2008.

Section 711 requires the Secretary of the Interior and the Director of the United States Geological Survey (USGS) to develop an assessment of the potential, including geographical extent and capacity, of geologic formations to sequester carbon. The Secretary of Energy and the Secretary of the Interior are further charged with the responsibility for creating a database of possible sequestration sites, ranked by capacity and risk. Section 711 authorizes total funding of $30 million from 2008 through 2012. This section does not pertain directly to AEO2008 and is not included.

Renewable Energy

In addition to the renewable energy provisions affecting the transportation, industrial, and buildings sectors, EISA2007 contains provisions authorizing several R&D programs for renewable energy use in the electric power sector. Specifically, Title VI calls for renewed, new, or enhanced R&D, educational, and technology transfer programs in the areas of solar energy (Sections 601-607), geothermal energy (Sections 611-625), and marine and hydrokinetic energy (Sections 631-636). Section 656 authorizes the Renewable Energy Innovation Manufacturing Partnership to advance manufacturing methods that use renewable energy. Appropriations for the authorized programs are not provided in the bill, however, and the programs are not included in AEO2008.

Other titles in EISA2007 contain provisions directly related to renewable electricity generation, but they either call for programs to be established or require specific appropriations that have not been made and, therefore, are not included in AEO2008. Section 803 authorizes direct grants for eligible renewable energy development projects. Section 806 is a nonbinding “sense of the Congress” statement that the Nation should strive to achieve a 25-percent renewable share of total energy consumption by 2025, while also providing sufficient food, feed, and fiber from agricultural resources. This statement does not contain any enforceable provisions or require any specific policy actions. Section 807 requires the Secretary of Interior to compile a comprehensive assessment of domestic geothermal resources. Section 1002 calls for the establishment of a workforce training program for trades related to renewable and energy efficiency. Section 1201 establishes a loan program for small businesses that want to purchase renewable energy or energy efficiency systems. Section 1207 establishes a program to support venture capital funding for new renewable energy businesses.

Federal Fuels Taxes and Tax Credits

The AEO2008 reference case incorporates current regulations that pertain to the energy industry. This section describes the handling of Federal taxes and tax credits in AEO2008, focusing primarily on areas where regulations have changed or the handling of taxes or tax credits has been updated.

Excise Taxes on Highway Fuel

The handling of Federal highway fuel taxes remains unchanged from AEO2007 [14]. Gasoline is assumed to be taxed at 18.4 cents per gallon, diesel at 24.4 cents per gallon, and kerosene jet fuel at 4.4 cents per gallon [15]. Taxes are not adjusted for inflation and remain at the same nominal values throughout the projections. State fuel taxes are calculated on the basis of a volume-weighted average of gasoline, diesel, and jet fuels sold. The handling of State fuel taxes was updated as of July 2007 [16].

Biofuels Tax Credits

The most significant change for AEO2008 is in the handling of Federal fuels taxes and credits that pertain to biofuels. Several Federal tax credits are available for liquid fuel blenders who blend ethanol into gasoline or biodiesel into diesel fuel or heating oil. Under the Volumetric Ethanol Excise Tax Credit (VEETC) [17], blenders are eligible for a tax credit of $0.51 per gallon of ethanol blended. Thus, the tax credit is equal to $0.051 per gallon for E10 and $0.434 per gallon for E85 [18]. The credit is scheduled to expire at the end of 2010. Biodiesel also receives a tax credit under VEETC, equal to $1.00 per gallon for “agri-biodiesel” and $0.50 per gallon for “wastegrease biodiesel” made from recycled vegetable oils and animal fats. Currently, the credits are scheduled to expire in 2008 [19, 20]. In AEO2008, both tax credits are assumed to expire according to the provisions of existing laws [21].

EPACT2005 provides small producers of ethanol, up to 60 million gallons [22], with an income tax credit of $0.10 per gallon on production volumes up to 15 million gallons. Because the credit affects only a small portion of the overall ethanol supply and is scheduled to expire on December 31, 2008, it is not included in AEO2008.

Ethanol Import Tariff

Two duties currently are imposed on imported ethanol. The first is an ad valorem tariff of 2.5 percent; the second is a tariff of $0.54 per gallon, which is applied after the ad valorem tariff. The second tariff, which was set to expire in October 2007 but has been extended to January 1, 2009, allows for limited dutyfree imports from designated Central American and Caribbean countries, not exceeding 7 percent of domestic production in the previous year. In the AEO2008 projections, ethanol imports increase after the tariff expires.

Production Tax Credits for Renewable Electricity Production

The handling of the Federal PTC for renewable electricity has been updated for AEO2008 to be consistent with current legislation. The PTC, which was set to expire on December 31, 2007, was extended to December 31, 2008, by the Tax Relief and Health Care Act of 2006, Public Law (P.L.) 109-432. It provides a benefit of $0.020 per kilowatthour (real 2007 dollars) for the first 10 years of an eligible renewable energy facility’s operation, boosting the growth of U.S. wind capacity in the near term. In the AEO2008 reference case, wind capacity in the electric power sector grows from 15.9 gigawatts in 2007 to 20.2 gigawatts in 2008, as compared with the AEO2007 projection of 16.6 gigawatts in 2008.

Mobile Source Air Toxics Rule

On February 9, 2007, the EPA released its MSAT2 rule, which will establish controls on gasoline, passenger vehicles, and portable fuel containers. The controls are designed to reduce emissions of benzene and other hazardous air pollutants [23]. Benzene is a known carcinogen, and the EPA estimates that mobile sources produced more than 70 percent of all benzene emissions in 1999. Other mobile source air toxics, including 1,3-butadiene, formaldehyde, acetaldehyde, acrolein, and naphthalene, also are thought to increase cancer rates or contribute to other serious health problems.

The MSAT2 rule sets a revised specification for benzene, which will take effect in 2011. The regulations on passenger vehicles, which will control hydrocarbon emissions in colder temperatures, will be implemented from 2010 to 2015. The rule also sets more stringent controls on portable fuel containers, beginning in 2009. The MSAT2 rule has been included in AEO2008 by modifying the NEMS representation of refinery processing of catalytic reformer feed. Although virtually every refinery will meet the requirement in a different way, most will involve treatment of the feed or product or the operation of the catalytic reformer.

Beginning on January 1, 2011, all gasoline products (including both reformulated and conventional gasoline) produced at refineries will be required to contain no more than 0.62 percent benzene by volume. (This does not apply to gasoline produced or sold in California, which is already covered by the current California Phase 3 Reformulated Gasoline program.) Approved small refineries will be required to conform to the rule by 2015. The second part of the standard requires that the actual average benzene levels that each refinery produces be no greater than 1.3 percent by volume by July 1, 2012 (July 1, 2016 for small refiners). The actual level is the level reached without use of any credits.

The published rule for gasoline benzene control includes an averaging, banking, and trading (ABT) program that is consistent with past EPA fuel regulations, allowing refiners to choose the most economical compliance strategy to meet the 0.62-percent annual average standard either by investing in new technology or by buying credits from the ABT program. From 2007 to 2010, the ABT program allows refiners to build “early credits” by making qualifying benzene reductions earlier than required. In 2011 and beyond, refiners and importers can generate “standard credits” by producing or importing gasoline with benzene levels below 0.62 volume percent on an annual average basis. The credits will be interchangeable between refiners and importers nationwide and can be “banked” for future use. The 3-year lag following establishment of the credit program provides the time necessary for small refiners to finish capital projects that are needed to meet the new standards without relying on credits. The rule also establishes a temporary hardship provision, which will provide refiners and importers with temporary relief from the benzene standards under certain rare circumstances (such as a refinery fire or natural disaster).

EPACT2005 Loan Guarantee Program

Title XVII of EPACT2005 authorized DOE to issue loan guarantees for projects involving new or improved technologies to avoid, reduce, or sequester GHGs. The law specified that the amount of the guarantee would be up to 80 percent of a project’s cost. EPACT2005 also specified that DOE must receive funds equal to the “subsidy cost” either through the Federal appropriations process or from the firm receiving the guarantee [24]. As discussed in AEO2007, this program, by lowering borrowing costs, can have a major impact on the economics of capital-intensive technologies [25].

In August 2006, DOE announced its first solicitation for $2 billion in loan guarantees. Even though the entire subsidy costs would be paid by successful applicants, DOE believed that authorization from Congress in an appropriations bill was required, and because there was no such authorization at the time, the requests were considered “pre-applications.” Consequently, the effects of the solicitation were not included in AEO2007. In February 2007, DOE did receive authorization to issue a total of $4 billion in guarantees. To codify DOE’s view that authorization is needed, the omnibus appropriations bill for FY 2008 passed by Congress in December 2007 (H.R. 2764) and its accompanying conference report required DOE to submit a loan guarantee implementation plan to both the House and Senate Appropriations Committees for approval 45 days before DOE issues any future solicitations.

The conference report also directed DOE “to make no authority in excess of” $38.5 billion for FY 2008 and FY 2009 [26] and allocated the $38.5 billion cap as follows: $18.5 billion for nuclear plants; $6 billion for carbon capture technologies; $2 billion for advanced coal gasification units; $2 billion for “advanced nuclear facilities for the ‘front end’ of the nuclear fuel cycle”; and $10 billion for technologies related to renewables, energy conservation, distributed energy, and electricity generation, transmission, and distribution.

The guidelines that accompanied the August 2006 solicitation—which stated that DOE would only guarantee up to 80 percent of a project’s debt—were criticized by some in the investment community and the nuclear industry for failing to take maximum advantage of the loan guarantee provision in EPACT- 2005, which allows DOE to guarantee up to 80 percent of a project’s cost [27]. The final rule that formalized the guidelines, issued in October 2007, allows for up to 100 percent of the project debt to be guaranteed. This approach was codified in EISA2007.

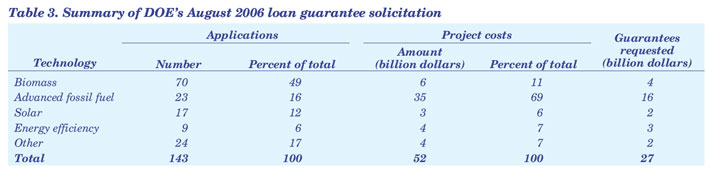

Because future solicitations have not yet been issued and remain subject to approval of a loan guarantee implementation plan by the Appropriations Committees, only the effects of the August 2006 solicitation are included in AEO2008. Table 3 summarizes the number of applications and the requested amounts that could be guaranteed for various technologies in the solicitation. In total, DOE received 143 applications for $27 billion in loan guarantees for projects costing $51 billion [28]. In October 2007, DOE released information about the 16 projects and sponsors that will be invited to submit full applications. Because the final approval process will take some time, AEO2008 assumes that the dollar amount of the approved guarantees will be roughly proportional to the requested guarantees. Accordingly, AEO2008 includes an additional 1.2 gigawatts of capacity at advanced coal-fired power plants and 250 megawatts at solar power plants that are built as a result of the loan program. (The other projects in the October 2007 announcement were for technologies that are outside the scope of AEO2008.)

State Renewable Energy Requirements and Goals: Update Through 2007

In recent years, the AEO has tracked the growing number of States that have adopted requirements or goals for renewable energy. While there is no Federal renewable generation mandate, the States have been adopting such standards for some time. AEO2005 provided a summary of all existing programs in effect at that time [29], and subsequent AEOs have examined new policies or changes to existing ones [30,31]. Since the publication of AEO2007, four States have enacted new RPS legislation, and five others have strengthened their existing RPS programs. In total, 25 States and the District of Columbia now have mandatory RPS programs (Table 4). At least four other States—Missouri, North Dakota, Vermont, and Virginia— have voluntary renewable energy programs.

All mandatory State RPS programs enacted as of the end of 2007 are represented in the AEO2008 reference case. While States differ in aspects such as eligible generation technologies and compliance penalties, a regional representation was created for modeling purposes. With the exception of California and New York, where eligible future renewable generation is uncertain because of funding limitations for State-supported programs, all States were assumed to meet their program targets, consistent with regionally aggregated compliance schedules. EIA estimated compliance generation in California and New York based on regional costs and authorized funding levels. In estimating diverse State mandates on a regional level, some precision is lost; however, including the State RPS programs in the reference case results in a better projection that is more consistent with current legislation and regulation. If recent trends continue, the State RPS programs will exert growing influence over the national energy mix.

Four States enacted new mandatory RPS programs over the past year:

New Hampshire. In May 2007, the State enacted an RPS which requires that the renewable share of energy consumed for electricity generation increase through 2025, reaching nearly 24 percent by 2025 [32]. Approximately 16 percent of all electricity sales must be from renewable facilities that begin operation after 2006. New Hampshire will collaborate with the New England control area to establish a renewable energy certificate (REC) program. Eligible generation must occur within New England or be consumed by costumers in the area. In this legislation, different renewable technologies are given distinct classifications with minimum generation requirements and compliance penalties. Solar power, which has the highest compliance penalty, must make up 0.3 percent of total sales by 2015 to reach the mandate.

North Carolina. The State established an RPS in August 2007 with different targets for investor- owned utilities, municipal suppliers, and electric cooperatives [33]. Investor-owned utilities must generate 12.5 percent of their total electric sales from renewable generation sources by 2021. Until 2018, one-quarter of this requirement can be met through the implementation of energy efficiency technologies. After 2018, 40 percent of the requirement can be met through the use of energy efficiency technologies. Municipal suppliers and electric cooperatives have a renewable mandate of 10 percent of retail electricity sales by 2018. In addition to the energy efficiency provision, municipal suppliers and electric cooperatives may meet a majority of the mandate through demand- side management and the use of large hydroelectric facilities. North Carolina will use an REC market, and limited out-of-State generation qualifies in meeting the RPS.

Oregon. The State enacted an RPS in June 2007, with standards that vary according to the size of the electricity provider [34]. Larger utilities must produce 25 percent of their electricity sales from renewable resources by 2025. Medium-sized suppliers have a 10-percent requirement and small providers a 5- percent requirement. Any renewable power plant coming online after 1995 is considered eligible toward meeting the State renewable energy goal. Oregon will use an REC market exclusive to the State, and credits will be capped at a price yet to be determined.

Washington. Voters approved Initiative 937 in November 2006, enacting the Nation’s second ballot RPS [35]. The law covers 84 percent of Washington’s sales, affects the State’s 17 largest suppliers, and specifies that 15 percent of their electricity load must be generated from renewable energy by 2020. Eligible generation includes any renewable facility that comes on line after 1999. The 17 suppliers also must identity feasible areas of conservation and publish implementation plans to achieve demand reductions. Failure to comply with the RPS or the conservation measures will result in a penalty to the generator of 5 cents per kilowatthour of generation.

Five States significantly changed their existing RPS requirements:

Delaware. The State enacted Senate Bill (S.B.) 19 in July 2007, increasing the required RPS from 10 percent to 20 percent of electricity by 2019 [36]. It also created a solar photovoltaic (PV) provision under which 2 percent of electricity must originate from solar PV by 2019. Both the solar target and the renewable target consist of escalating interim milestones. The existing schedule of alternative compliance payments (ACPs) is not affected [37], but the bill does provide for separate solar ACPs with a minimum value of $250 per megawatthour—much higher than the standard ACPs. In-State solar PV generation receives triple credits toward meeting the RPS.

Colorado. House Bill 1281 strengthened the RPS that was approved by voters in 2004 by increasing the amount of renewable energy required in 2015 from 10 percent to 15 percent of sales [38]. It also added the requirement that 20 percent of total electricity sales by investor-owned utilities must come from renewable energy by 2020. Investor-owned utilities also are required to generate 2 percent of their sales with solar energy technologies. House Bill 1281 created a less stringent standard for electric cooperatives and municipal utilities, requiring that only 10 percent of sales be from qualifying sources by 2020. It also establishes that generation within Colorado receives 125 percent of the value that out-of-State energy would earn.

Connecticut. The State revised its RPS requirement in June of 2007 as part of Public Act 07-242 [39]. The revisions extended the RPS to 2020, with a 27-percent requirement in that year. Most of the standard is to be met through renewable technologies using wind, solar, sustainable biomass, and wave energy. Generation from surrounding States is eligible. There are separate rules requiring CHP systems and efficiency enhancements (4 percent). Three percent of the total may be met from waste-to-heat facilities and conventional biomass. Suppliers that do not comply face a penalty of 5.5 cents that will be used to fund renewable development.

Illinois. In August 2007, the State’s voluntary renewable goal was replaced by a mandatory RPS [40]. Suppliers with more than 100,000 customers are required to provide 25 percent of their electricity from qualifying facilities by 2025, with several interim requirements. Three-quarters of the facilities must be wind powered. Until 2011, lower cost in- State resources must be used unless they are proven exhausted, in which case out-of-State generation would qualify. After 2011, no preference is given to Illinois resources over others in the region. The costs associated with the mandates are capped and reviewable.

Minnesota. Minnesota’s new RPS regulations became effective in February 2007. They created two standards, one for Xcel Energy and another for other suppliers [41]. Previously, Minnesota had a voluntary standard. The Xcel milestones are the most significant, with 30 percent of all power required to come from renewable energy by 2020. Approximately 83 percent of the power from renewables must come from wind turbines. Other suppliers, including municipal utilities, have until 2025 to meet a smaller goal of 25 percent. The State Public Utilities Commission is still constructing an REC trading system, and the role that interstate or interregional credits will play is still unknown.

State Regulations on Airborne Emissions: Update Through 2007

Implementation of the Clean Air Interstate Rule

States are moving forward with implementation plans for the Clean Air Interstate Rule (CAIR) [42]. The program, promulgated by the EPA in March 2005, is a cap-and-trade system designed to reduce emissions of SO2 and NOx. States originally had until March 2007 to submit implementation plans, but the deadline has been extended by another year. CAIR covers 28 eastern States and the District of Columbia. States have the option to participate in the cap-andtrade plan or devise their own plans, which can be more stringent than the Federal requirements. To date, no State has indicated an intent to form NOx and SO2 programs with emissions limits stricter than those in CAIR, and it is expected that all States will participate in the EPA-administered cap-and-trade program. CAIR remains on schedule for implementation, and AEO2008 includes CAIR by assuming that all required States will meet only the Federal requirement and will trade credits.

A similar program, the Clean Air Mercury Rule (CAMR), was promulgated by the EPA in March 2005 to reduce emissions of mercury [43]. On February 8, 2008, the U.S. Court of Appeals found CAMR to be unlawful and voided it, ruling that the EPA had not proved mercury to be a pollutant eligible for regulation under a less stringent portion of the Clean Air Act. Because the court’s ruling came too late for EIA to remove the CAMR provisions from its analysis, AEO2008 includes consideration of CAMR. Regardless of CAMR, however, some States have implemented plans calling for mandatory 90-percent cuts in mercury emissions from all plants of a certain size. More stringent modeling of mercury emissions limits in some regions may be necessary when State actions have been finalized.

State Greenhouse Gas Initiatives

RGGI. Since the end of 2006, three additional States have joined the Regional Greenhouse Gas Initiative (RGGI) [44]. Currently, RGGI includes 10 members: Connecticut, Delaware, Maine, Massachusetts, New Hampshire, New Jersey, New York, Rhode Island, Vermont, and Maryland.

Although AEO2008 does not include RGGI, given the current uncertainty about the program’s structure and allowance trading, several States are now moving forward with their draft implementation plans. Massachusetts, Maine, and New York have released public drafts for comment. Each of those plans closely follows the model rules published in August 2006, requiring that 100 percent of the allowances be auctioned. It is thought that all RGGI States are likely to follow the same precedent, with a limited number of giveaway credits. RGGI formally begins in January 2009. Some States will have to enact legislation to make the program legally binding, whereas others have State agencies that already have such authority and do not need to pass new laws. As of late 2007, Vermont was the only RGGI State that had enacted a new law.

WCI. In February 2007, the governors of Arizona, California, New Mexico, Oregon, and Washington established the Western Climate Initiative (WCI).

Utah and the Canadian provinces of British Columbia and Manitoba have since joined as full partners. Six additional U.S. States and several Canadian provinces participate as observers. The eight full partners have agreed to the goal of decreasing emissions to 15 percent below 2005 levels by 2020, but little else about the program has been decided. Although the WCI is leaning heavily toward a cap-and-trade system, the specifics of covered emissions, State allowance allocations and trading, emissions accounting, and offsets—among other items—still are being negotiated. AEO2008 does not include the WCI, because it remains to be seen how the program will function and what the penalties for noncompliance will be.

WCI has a task force that will assemble a program model rule by August 2008. Some WCI partner States already have GHG laws or goals, while others, such as Utah, do not. The agreement does not override the binding GHG laws in California, Oregon, and Washington, but it does require WCI partners to join the Climate Registry, which is a collaboration of 39 U.S. States, Canadian provinces, and Mexican states seeking uniform GHG accounting and reporting.

California. California’s S.B. 1368 [45] makes it illegal to enter into new long-term contracts to serve the State’s electricity demand with power plants that produce GHG emissions in excess of 1,100 pounds per megawatthour of electricity generated—effectively prohibiting the construction of new coal-fired facilities without carbon sequestration, even if they are located in a neighboring State. AEO2008 includes the impact of S.B. 1368 through limits on coal-fired electricity generation serving California.

California’s Assembly Bill (A.B.) 1493, which would establish GHG emissions standards for LDVs, is not considered in the AEO2008 reference case. A.B. 1493 was signed into law in July 2002, and regulations were released by the California Air Resources Board in August 2004 and approved by California’s Office of Administrative Law in September 2005 [46]. The emission standards would be applied to lightduty noncommercial passenger vehicles manufactured for model year 2009 and beyond [47]. The standards, specified in terms of CO2-equivalent emissions, would apply to vehicles in two size classes: passenger cars and light-duty trucks with a loaded vehicle weight rating of 3,750 pounds or less; and light-duty trucks with a loaded vehicle weight rating greater than 3,750 pounds and a gross vehicle weight rating less than 8,500 pounds. The CO2-equivalent emissions standard for light trucks would include noncommercial passenger trucks between 8,500 pounds and 10,000 pounds. The regulations were to become effective in January 2006 and set near-term emission standards that were to be phased in between 2009 and 2012. The mid-term emission standards were to be phased in between 2013 and 2016. After 2016, the emissions standards would be left unchanged.

Before California can implement the GHG emission standards for vehicles established in A.B. 1493, it must receive a waiver from the U.S. EPA. The EPA, however, has denied California a waiver to regulate GHG emissions from mobile source under the Clean Air Act. Expressing concern about the establishment of regional emissions standards for new motor vehicles, the EPA reasoned that the effects of climate change in California did not support the need for a regional standard.

In October 2003, California, 11 other States, 3 cities, and several environmental groups filed a petition in the U.S. Court of Appeals, arguing that the EPA should regulate GHG emissions from vehicles. In July 2005, a three-judge panel ruled 2 to 1 in the EPA’s favor, stating that the agency was not required to regulate GHGs under the Clean Air Act. The decision was overturned in April 2007 by the U.S. Supreme Court, which ruled that the EPA has authority under Section 202 of the Clean Air Act to regulate GHG emissions from automobiles. Nonetheless, on December 19, 2007, the EPA again denied California’s request for a waiver [48]. On January 2, 2008, California and 15 other States sued the EPA, challenging its decision to deny the wavier [49].

AEO2008 also does not include consideration of California A.B. 32, which mandates a 25-percent reduction in California’s GHG emissions by 2020. Implementing regulations have not been drafted and are not due to be finalized until January 2012.

Washington and Oregon. Washington and Oregon have joined California in the enactment of State GHG legislation. In May 2007, Washington’s Governor Christine Gregoire signed S.B. 6001 [50], which mandates cuts in emissions and performance standards for power plants. The legislation targets reductions to 1990 emissions levels in the State by 2020, to 25 percent below the 1990 levels by 2035, and to 50 percent below the 1990 levels by 2050. Washington has not yet mandated the program specifics, such as the type of system that will be used to meet the targets. Additional action from the governor, the utilities, and the State’s transportation commission will be required.

Washington State has also adopted the same standards included in California S.B. 1368. Oregon, which has CO2 regulations for natural-gas-fired plants but not for other fossil-fuel-based power systems, passed its GHG reduction law in August 2007. The law has the same 2020 reduction goal as Washington’s and also requires that emissions growth be capped by 2010. It establishes the Oregon Global Warming Commission, a body will have 25 members with various backgrounds who will serve as an advisory board to State and local governments. Like Washington and California, Oregon has not determined the specific procedures to be followed in implementing the required emissions reductions.

Other States. Many other States have goals and other provisions for GHG reductions and accounting of emissions from stationary sources. In May 2007, Montana’s Governor Brian Schweitzer signed House Bill 25 [51], which requires any new coal-fired generating facility to sequester at least 50 percent of the CO2 it emits. Florida’s Governor Charlie Crist signed three executive orders [52] over the summer concerning his State’s emissions of heat-trapping gases, including an overall State goal to bring emissions to 80 percent below 1990 levels by 2050. An Energy and Climate Change Action Plan will be developed to determine how the State of Florida can reach those reduction goals.

ICAP. Ten U.S. States, all of which are participants in either RGGI or WCI, have entered the International Carbon Action Partnership (ICAP). ICAP, created in October 2007, seeks collaboration among carbon trading programs. Members include nine European Union countries, the European Commission, Norway, and New Zealand. Several other U.S. States have non-binding goals, carbon registry requirements, or energy plans that include recommendations to limit CO2 emissions from stationary sources, including those described above.

Legislation and Regulatios Notes

|