Energy Demand

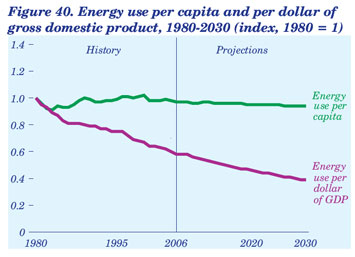

Average Energy Use per Person Levels Off Through 2030

Because energy use for housing, services, and travel

in the United States is closely linked to population

levels, energy use per capita is relatively stable

(Figure 40). In addition, the economy is becoming

less dependent on energy in general.

Energy intensity (energy use per 2000 dollar of GDP)

declines by an average of 1.4 percent per year in the

low growth case, 1.7 percent in the reference case, and

1.9 percent in the high growth case. Efficiency gains

and faster growth in less energy-intensive industries

account for most of the projected decline, more than

offsetting growth in demand for energy services in

buildings, transportation, and electricity generation.

The decline is more rapid in the high economic

growth case, because with higher economic growth

the number of new, more efficient systems grows

faster, and the additional growth is concentrated in

less energy-intensive industries. As energy prices

moderate over the longer term, energy intensity declines

at a slower rate in the reference, high growth,

and low growth cases.

The AEO2008 cases developed to illustrate the uncertainties

associated with those factors include low and

high growth cases, low and high price cases, and alternative

technology cases (see Appendixes B, C, D, and E).

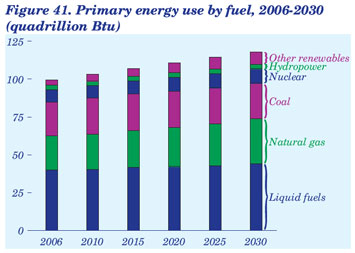

Coal and Liquid Fuels Lead Increases

in Primary Energy Use

Total primary energy consumption, including energy

for electricity generation, grows by 0.7 percent per

year from 2006 to 2030 in the reference case (Figure

41). Fossil fuels account for 55 percent of the increase.

Coal use increases in the electric power sector, where

electricity demand growth and current environmental

policies favor coal-fired capacity additions. About

54 percent of the projected increase in coal consumption

occurs after 2020, when higher natural gas prices

make coal the fuel of choice for most new power

plants under current laws and regulations, which do

not limit greenhouse gas emissions. Increasing demand

for natural gas in the buildings and industrial

sectors offsets the decline in natural gas use in the

electricity sector after 2016, resulting in a net increase

of 5 percent from 2006 to 2030.

The transportation sector accounted for more than

two-thirds of all liquid fuel consumption in 2006, and

60 percent of that share went to LDVs. Demand for

liquid transportation fuels increases by 17 percent

from 2006 to 2030, dominated by growing fuel use for

LDVs, trucking, and air travel. The industrial sector

accounted for 25 percent of total liquid fuel use in

2006, but its share declines to 21 percent in 2030.

AEO2008 also projects rapid percentage growth in

renewable energy production, as a result of the

EISA2007 RFS and the various State mandates for

renewable electricity generation. Additions of new

nuclear power plants are also projected, spurred by

improving economics relative to plants fired with

fossil fuels and by the EPACT2005 PTCs.

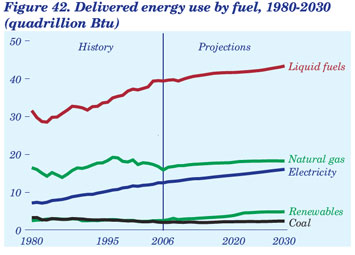

Electricity and Liquid Fuels Lead Rise

in Delivered Energy Consumption

Delivered energy use (excluding losses in electricity

generation) grows by 0.7 percent per year from 2006

to 2030 in the reference case. The growth in electricity

use is driven by growing demand in the residential

and commercial sectors. With the growing market

penetration of electric appliances, residential electricity

use increases slightly faster than the total number

of households, and commercial electricity use outpaces

the growth in commercial floorspace. With different

assumptions about population and economic

growth, average annual growth in delivered energy

use from 2006 to 2030 ranges from 0.3 percent in the

low growth case to 1.0 percent in the high growth

case.

Growth in demand for liquid fuels is led by the transportation

sector, as rising population, incomes, and

economic output boost demand for travel, partially

offsetting improvements in vehicle efficiency (Figure

42). Natural gas use grows more slowly than overall

delivered energy demand, reflecting its relatively

higher cost, particularly in the industrial sector.

Industrial biomass accounts for the largest share of

end-use consumption of renewable energy. Currently

it is used mostly as a byproduct fuel in the pulp and

paper industry, but that use will be surpassed by

consumption of biomass heat and co-products from

ethanol manufacture when the biofuel mandate

under EISA2007 reaches 36 billion gallons in 2022.

Consumption of nonmarketed solar, geothermal, and

wind energy also increases dramatically in the projections;

however, it continues to account for less than

1 percent of all delivered energy use in the residential

and commercial sectors.

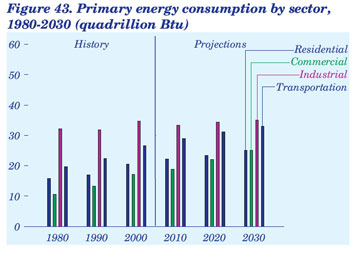

U.S. Primary Energy Use Climbs

to 118 Quadrillion Btu in 2030

The most significant impact of EISA2007 is in the

transportation sector, where the CAFE standard for

LDVs is raised to 35 mpg in 2020. Still, from 2006

to 2030 the transportation sector sees the secondlargest

increase in energy consumption, at 5 quadrillion

Btu (Figure 43), as a result of increases in vehicle

miles traveled, jet fuel consumption, and demand for

fuels such as E10, E85, and diesel to displace motor

gasoline.

EISA2007 has little effect on the commercial sector,

where energy demand continues to expand more

rapidly than the economy as a whole. Dependence on

natural gas and electricity, already heavy in the residential

and commercial sectors, increases over time.

Demand for electricity grows faster than demand for

natural gas in both sectors, however, because electricity

is used for a wider diversity of applications (including

the fastest growing end uses, office equipment,

personal computers, and televisions), whereas natural

gas is used mainly for space heating, cooking, and

water heating, which grow more slowly than households

and floorspace.

The variation in residential and commercial energy

demand between the high and low price cases is relatively

small, and natural gas consumption accounts

for most of the difference. In the industrial sector,

fuel use in 2030 is higher in the high price case than in

the reference case, reflecting differences in CTL,

ethanol, and biodiesel production. Different growth

rates for manufacturing output in the low and high

macroeconomic growth cases account for most of the

difference in industrial energy consumption between

the two cases.

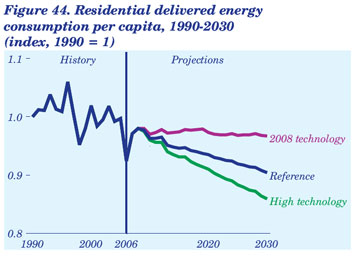

Residential Energy Use per Capita

Varies With Technology Assumptions

Residential energy use per person has remained fairly

constant since 1990 (taking into account year-to-year

fluctuations in weather), with increases in energy

efficiency offset by consumer preference for larger

homes and by new residential uses for energy. Over

the past 10 years, the weather has generally been

warmer than the 30-year average, causing energy use

per person to remain mostly below its 1990 level.

Given the preponderance of warmer winters and

summers, the AEO2008 projections define normal

weather as the average of the most recent 10 years of

historical data, which decreases the need for heating

fuels, such as natural gas and fuel oil, and increases

the need for electricity used for air conditioning, all

else being equal [79].

In the AEO2008 projections, residential energy use

per capita changes with assumptions about the rate at

which more efficient technologies are adopted. The

2008 technology case assumes no increase in the efficiency

of equipment or building shells beyond those

available in 2008. The high technology case assumes

lower costs, higher efficiencies, and earlier availability

of some advanced equipment. In the reference

case, residential energy use per capita is projected to

fall below the 2006 level after 2024. The 2008 technology

case approximates an upper bound on residential

energy use per capita in the future: delivered energy

use per capita in the residential sector remains above

the 2006 level through 2030, when it is 7 percent

higher than projected in the reference case (Figure

44). The high technology case provides a lower bound,

falling below the 2006 level after 2016 and reaching a

2030 level that is 5 percent below the reference case

projection.

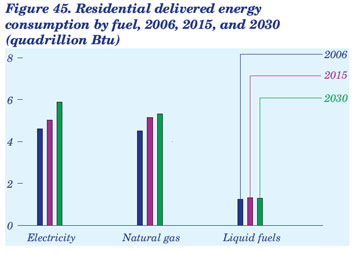

Household Uses for Electricity

Continue To Expand

In 2006, households consumed more electricity than

natural gas for the first time, as warmer winter temperatures

reduced the need for natural gas heating.

Over the past decade, residential electricity use has

grown steadily, as a result of the increase in air conditioning

use and the introduction of new applications.

That trend is expected to continue in AEO2008

(Figure 45). In 2030, electricity use for home cooling

is 38 percent higher than the 2006 level in the reference

case, as the U.S. population continues to migrate

to the South and West, and older homes convert from

room air conditioning to central air conditioning. A

projected 25-percent increase in the number of households

also increases the demand for appliances, and

total electricity use in the residential sector increases

by 27 percent from 2006 to 2030 in the reference case.

Natural gas and liquid fuels are used in the residential

sector primarily for space and water heating. Few

new uses have emerged over the past decade, and few

are expected in the future. Thus, natural gas and

liquids consumption per household decreases as the

energy efficiency of furnaces and building components

continues to improve.

The 2008 technology and high technology cases provide

high and low ranges for the projections. In the

high technology case, for example, high-efficiency air

conditioners and condensing gas furnaces become

more prevalent. Recent developments in solid-state

lighting technologies, such as light-emitting diodes

(LEDs), are reflected in the reference case as a reduction

of up to 85 percent in the amount of electricity

needed to provide a given amount of useful light.

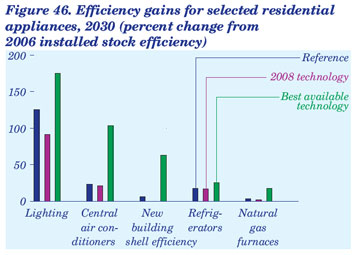

Increases in Energy Efficiency

Are Projected To Continue

The energy efficiency of new household appliances

plays a key role in determining the types and amounts

of energy used in residential buildings. As a result of

stock turnover and purchases of more efficient equipment,

energy use by residential consumers, both per

household and per capita, has fallen over time. In the

2008 technology case, which assumes no efficiency

improvement of available appliances beyond 2008 levels,

normal stock turnover results in higher average

energy efficiency for most end uses in 2030, as older

appliances are replaced with more efficient models

from the existing stock of appliances (Figure 46).

The largest gains in residential energy efficiency are

projected in the best available technology case, which

assumes that consumers purchase the most efficient

products available at normal replacement intervals

regardless of cost, and that new buildings are built to

the most energy-efficient specifications available,

starting in 2009. In this case, residential delivered

energy consumption in 2030 is 27 percent less than in

the 2008 technology case and 22 percent less than in

the reference case. Purchases of new energy-efficient

products, especially compact fluorescent and solidstate

lighting and condensing gas furnaces, reduce

energy use without lowering service levels.

Several current Federal programs, including Zero

Energy Homes and ENERGY STAR Homes, promote

the use of efficient appliances and building envelope

components, such as windows and insulation. In

the best available technology case, use of the most

efficient building envelope components available can

reduce heating requirements in an average new home

by more than 60 percent.

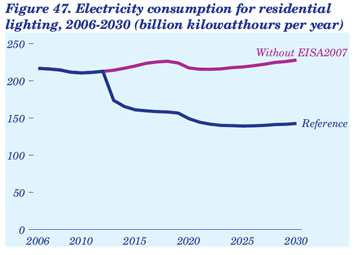

Residential Electricity Use for

Lighting Is Expected To Decline

Residential electricity use for lighting accounted for

about 16 percent of the sector’s total electricity consumption

in 2006, making it the second largest use for

electricity in households. In the AEO2008 reference

case, electricity use for lighting declines as a result of

the lighting efficiency standards in EISA2007, which

require general-service incandescent light bulbs to

reduce wattage by about 28 percent by 2014, increasing

to 65 percent in 2020. DOE is required to examine

the potential for tighter standards after 2020, but the

details are uncertain and are not included in the

AEO2008 reference case.

Figure 47 summarizes residential lighting use in the

AEO2008 reference case and a case without EISA-2007. Given the relatively rapid turnover in incandescent

lighting, EISA2007 achieves electricity savings

immediately, reducing lighting demand by 27 percent

(59 billion kilowatthours) in 2015. With continued

tightening of the standard through 2020, demand

for lighting is reduced by 85 billion kilowatthours

in 2030, as efficient lighting options, mainly LEDs,

gain market share.

In 2007, roughly 200 million compact fluorescent

light (CFL) bulbs were sold in the United States,

accounting for about 10 percent of total sales. Even

without the new standards, CFL sales in the residential

market were expected to continue growing in the

coming years. LED lamps, which are just now being

introduced in the general-service residential lighting

market, reach nearly 20 percent of sales in 2020 without

the EISA2007 standards. With the EISA2007

standards, the market share for LED bulbs in 2020

doubles.

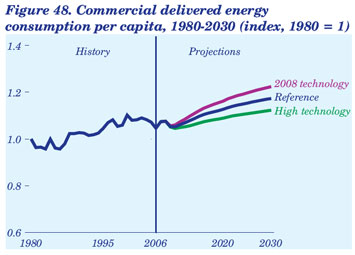

Rise in Commercial Energy Use

per Capita Is Projected To Continue

Assumptions about the availability and adoption of

energy-efficient technologies define the range for

delivered commercial energy use per person in the

AEO2008 projections. Commercial energy consumption

per capita increases by a total of 12 percent from

2006 to 2030 in the reference case, primarily as a

result of rising electricity use as the Nation continues

to move to a service economy. The size of the projected

increase varies from a low of 7 percent in the

high technology case to a high of 17 percent in the

2008 technology case (Figure 48).

In terms of floorspace, growth in the commercial sector

averages 1.2 percent per year from 2006 to 2030,

driven by trends in economic and population growth.

The reference case assumes future improvements in

efficiency for commercial equipment and building

shells, as well as increased demand for services. Consequently,

commercial energy use increases at about

the same rate as floorspace in the reference case, and

commercial energy intensity (delivered energy consumption

per square foot of floorspace) shows little

change, increasing by less than 2 percent. The 2008

technology case assumes no increase in the energy

efficiency of commercial equipment and building

shells beyond those available in 2008. The result is a

4-percent increase in commercial delivered energy

use in 2030 relative to the reference case. In the high

technology case, assuming earlier availability, lower

costs, and higher efficiencies for more advanced

equipment and building shells, delivered energy consumption

in 2030 is 4 percent below the reference

case projection.

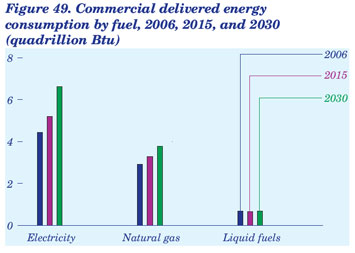

Electricity Leads Expected Growth

in Commercial Energy Use

In the AEO2008 projections, growth in disposable

income leads to increased demand for services from

hotels, restaurants, stores, theaters, galleries, arenas,

and other commercial establishments, which in turn

are increasingly dependent on computers and other

electronic office equipment both for basic services and

for business services and customer transactions. In

addition, the growing share of the population over age

65 increases demand for health care and assistedliving

facilities and for electricity to power medical

and monitoring equipment at those facilities. The reference

case projects increases in commercial electricity

use averaging 1.7 percent per year from 2006 to

2030 (Figure 49). The high technology and 2008 technology

cases provide low and high ranges for the

average annual growth rate of commercial electricity

consumption from 2006 to 2030, at 1.4 percent and

2.0 percent, respectively.

Use of natural gas and liquids for heating shows

limited growth, as commercial activity reflects the

U.S. population shift to the South and West and the

efficiency of building and equipment stocks improves.

Commercial natural gas use grows by 1.1 percent per

year on average from 2006 to 2030 in the reference

case, including more use of CHP in the later years.

While there is little change in liquid fuel consumption,

the projections for natural gas use in 2030 range

from 3.8 quadrillion Btu in the reference case to 4.0

quadrillion Btu in the high growth case and 3.5 in the

low growth case. The high and low oil price cases

show the widest range for liquid fuels use, varying

from 7 percent below to 12 percent above the reference

case projection of 0.7 quadrillion Btu in 2030.

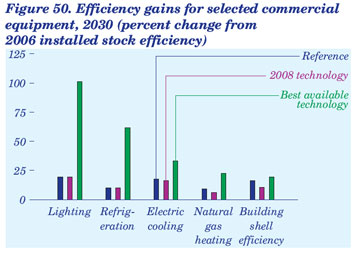

Technology Provides Potential Energy

Savings in the Commercial Sector

The stock efficiency of energy-using equipment in the

commercial sector increases in the AEO2008 reference

case. Adoption of more energy-efficient equipment

moderates the growth in demand, in part

because of existing building codes for new construction

and minimum efficiency standards, including

those in EPACT2005 and EISA2007; however, the

long service lives of many kinds of energy-using

equipment limit the pace of efficiency improvements.

The most rapid increase in overall energy efficiency

for the commercial sector occurs in the best available

technology case, which assumes that only the most

efficient technologies are chosen, regardless of cost,

and that new building shells in 2030 are 19 percent

more efficient than the commercial buildings stock in

2006. With the adoption of improved heat exchangers

for space heating and cooling equipment, solid-state

lighting, and more efficient compressors for commercial

refrigeration, commercial delivered energy consumption

in 2030 in the best technology case is 12

percent less than in the reference case and 16 percent

less than in the 2008 technology case.

In the 2008 technology case, which assumes equipment

and building shell efficiencies limited to those

available in 2008, energy efficiency in the commercial

sector still improves from 2006 to 2030 (Figure 50),

because the technologies available in 2008 can provide

savings relative to equipment currently in place.

When businesses consider equipment purchases,

however, the additional capital investment needed to

buy the most efficient technologies often carries more

weight than do future energy savings.

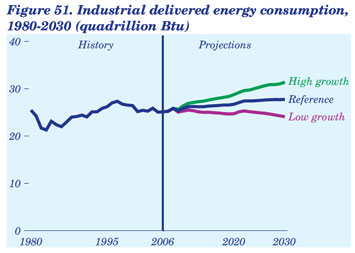

Economic Growth Cases Show Range

for Projected Industrial Energy Use

In the AEO2008 reference case, industrial value of

shipments grows at an annual rate of 1.3 percent

from 2006 to 2030. Industrial delivered energy consumption

increases by just 0.4 percent per year, from

25.1 quadrillion Btu in 2006 to 27.7 quadrillion Btu in

2030, as increased efficiency and changes in the composition

of output partially offset growth. In the low

economic growth case, industrial value of shipments

grows by 0.5 percent per year, and delivered energy

consumption falls to 24.2 quadrillion Btu in 2030. In

the high growth case, industrial value of shipments

grows by 2.0 percent per year, and energy consumption

rises to 31.7 quadrillion Btu in 2030, 14 percent

higher than in the reference case (Figure 51). The

variation in industrial output growth among the

three cases is well within the typical range over the

past 16 years, when output grew by 1.7 percent per

year on average from 1990 to 2007, and annual

growth rates ranged from 5.7 percent to a decline of

4.7 percent.

The construction and chemical industries were particularly

affected by the recent economic slowdown,

and their future growth is expected to be modest

(averaging 0.5 percent per year for the construction

industry from 2006 to 2030 in the reference case). As

a result, energy consumption in the construction

sector declines from 2.4 quadrillion Btu in 2006 to 2.2

quadrillion Btu in 2030, with about 70 percent of the

decrease attributed to reduced use of asphalt. The

bulk chemical industry shows little growth from 2006

to 2030, and its fuel consumption for energy and feedstock

totals only 5.6 quadrillion Btu in 2030, as compared

with an estimated 6.8 quadrillion Btu in 2006.

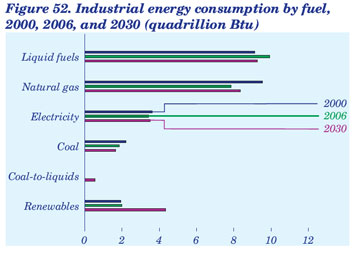

Industrial Fuel Choices Vary

Over Time

Industries adjust their fuel and product mixes over

time to respond to changing markets, as indicated by

the falling share of industrial coal use for process

steam and the rapid increase in coal use for production

of liquid fuels in the AEO2008 reference case

(Figure 52). Traditional coal use falls slightly as the

use of metallurgical coal in steelmaking declines,

reflecting the difficulty of building additional coke

ovens in the United States. Industrial demand for

steam coal as a boiler fuel also declines, as industrial

processes become more efficient and use less steam,

and as the growth of energy- and steam-intensive

industries slows. As a result, consumption of steam

coal in the industrial sector declines by 0.3 percent

per year in the reference case projection.

Natural gas consumption, excluding lease and plant

use, increases from 6.7 quadrillion Btu in 2006 to 7.1

quadrillion Btu in 2030—only slightly less than in

1990 (7.2 quadrillion Btu). Consumption of liquid

fuels falls slightly, from 9.9 quadrillion Btu in 2006 to

9.3 quadrillion Btu in 2030, but remains the largest

category of industrial energy consumption. About

three-quarters of industrial liquids consumption is

for nonfuel uses or as a byproduct in the refining

industry. Industrial consumption of purchased electricity

grows by just 0.1 percent per year. The only

industrial fuels for which significant increases are

projected are coal used in CTL plants and biofuel for

ethanol production. From no commercial production

in 2006, coal use for CTL grows to 0.6 quadrillion Btu

in 2030 in the reference case, and biofuel use for

ethanol production increases eightfold, to 2.3 quadrillion

Btu in 2030.

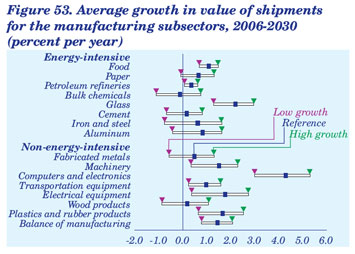

Energy-Intensive Industries Grow

Less Rapidly Than Industrial Average

In the AEO2008 reference case, average annual

growth in value of shipments for the manufacturing

sectors ranges from a decline of 0.1 percent per year

(bulk chemicals) to an increase of 4.3 percent per year

(computers). The pattern is similar in the economic

growth cases (Figure 53).

For the bulk chemical industry, value of shipments

grows slowly for several years and then falls slightly

over the last decade of the projection, as export demand

falls and other countries increase production.

The annual rate of growth in the energy-intensive

manufacturing group (0.7 percent) is lower than in

the non-energy-intensive group (1.9 percent). Glass is

the only energy-intensive subsector with a growth

rate above 2 percent per year in the reference case.

The growth rate for the industrial sector as a whole in

the final 10 years of the projection is slightly lower

than in the earlier years (1.2 percent compared with

1.4 percent). Growth rates for the individual

subsectors vary considerably, with about one-quarter

of them growing more rapidly in the final decade.

The projected growth rates for value of shipments

in the industrial subsectors in the high and low

economic growth cases generally are symmetrical

around the reference case. Industries with the most

rapid projected growth in the reference case also have

relatively more rapid growth in the high and low

economic growth cases. The range across economic

growth cases and subsectors is substantial, from a

decline of 1.1 percent per year for bulk chemicals in

the low economic growth case to an increase of 5.3

percent per year for computer manufacturing in the

high economic growth case.

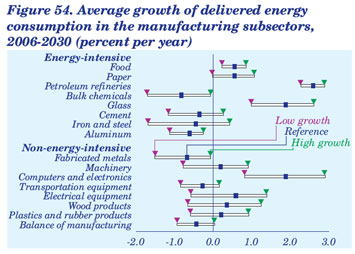

Energy Consumption Growth Varies

Widely Across Industry Sectors

The range of projections for industrial energy consumption

in AEO2008 largely reflects uncertainty

about the rate of economic growth. Average annual

growth in total delivered energy consumption in the

industrial sector from 2006 to 2030 ranges from a

decline of 0.1 percent in the low economic growth case

to an increase of 1.0 percent in the high economic

growth case. In 2030, consumption is 3.5 quadrillion

Btu lower in the low economic growth case and 4.0

quadrillion Btu higher in the high economic growth

case when compared with the reference case. Thus,

across the cases, the range for industrial energy

consumption in 2030 is 7.5 quadrillion Btu.

In the reference case, energy consumption growth

varies substantially among industry subsectors

(Figure 54). Delivered energy consumption falls over

the projection period for one-half of the energyintensive

industries (bulk chemicals, cement, iron

and steel, and aluminum) as a result of relatively slow

output growth rates, combined with expected

changes in production technology over the projection

period. The declines are reinforced by modest increases

in energy prices after 2020. In general, the

subsectors with the highest growth rates in energy

consumption are those with the highest growth rates

in value of shipments (computers and glass). The petroleum

refining sector is an exception. As refineries

shift to alternative feedstocks for liquids production

(biofuels, coal, heavier crude oil), more energy is required

per unit of output than is used for traditional

petroleum-based refining. Energy consumption at

refineries increases from 3.9 quadrillion Btu in 2006

to 7.3 quadrillion Btu in 2030—more than the total

growth in industrial sector energy consumption.

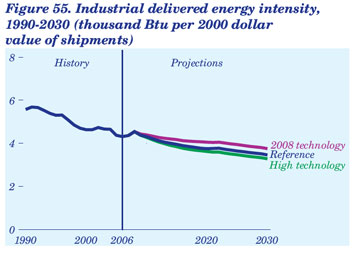

Energy Intensity in the Industrial

Sector Continues To Decline

From 1990 to 2006, energy consumption in the industrial

sector increased by only 0.5 quadrillion Btu

(3 percent), while the value of shipments increased

by 33 percent. Thus, industrial delivered energy use

per dollar of industrial value of shipments declined

by an average of 1.6 percent per year from 1990 to

2006 (Figure 55). Factors contributing to the drop in

energy intensity include continued restructuring

that reduced the industrial sector share of the most

energy-intensive industries; higher petroleum and

natural gas prices since 1998, which stimulated

greater improvements in energy efficiency; and hurricane-related shutdowns in 2005.

The energy-intensive industries’ share of industrial

output fell from 23 percent in 1990 to 21 percent in

2006; and in 2030 their share is projected to be 18

percent. Consequently, even if no specific industry

showed a reduction in energy intensity, the aggregate

energy intensity of the industrial sector would

decline. The shift in output share to less energyintensive

industries accounts for 84 percent of the

projected change in industrial energy intensity in the

reference case [80].

The technology cases represent alternative views of

the evolution and adoption of energy-saving technologies

in the industrial sector. In the high technology

case, industrial energy intensity falls by 1.1 percent

per year, compared with 0.9 percent per year in the

reference case. In the 2008 technology case, energy

intensity improves by only 0.5 percent per year.

Across the technology cases, industrial energy consumption

in 2030 varies over a range from 26.5 to

30.3 quadrillion Btu.

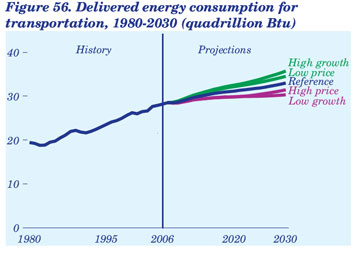

Growth in Transportation Energy Use

Is Expected To Slow

Delivered energy consumption in the transportation

sector grows at an average annual rate of 0.7 percent

in the AEO2008 reference case, from 28.2 quadrillion

Btu in 2006 to 33.0 quadrillion Btu in 2030 (Figure

56). That rate is less than the historical rate of 1.4

percent per year from 1980 to 2006, because the new

EISA2007 fuel economy standards, slower economic

growth, and higher fuel prices lead to efficiency improvements

and slower growth in travel demand.

Transportation energy consumption is influenced by

a variety of factors, including economic growth, population

growth, fuel prices, and vehicle fuel efficiency.

AEO2008 includes cases that examine the impacts of

those factors on delivered energy consumption. In

2030, transportation sector energy consumption is

about 8 percent higher in the high economic growth

case and 8 percent lower in the low economic growth

case than in the reference case, and it is about 5 percent

lower in the high price case and 5 percent higher

in the low price case than in the reference case.

By mode, the largest share of total transportation

energy consumption is for travel by LDVs (cars,

pickup trucks, sport utility vehicles, and vans). The

modes with the largest increases in energy demand

are heavy trucks (medium and large—classes 3

through 8—freight trucks and buses) and aircraft.

Heavy vehicles, which accounted for 18 percent of the

sector’s total energy use in 2006, account for 20 percent

in 2030 in the reference case. With expected

strong growth in demand for air travel and more

investment in infrastructure, air travel also accounts

for a growing portion of total energy consumption (13

percent in 2030, up from 9 percent in 2006).

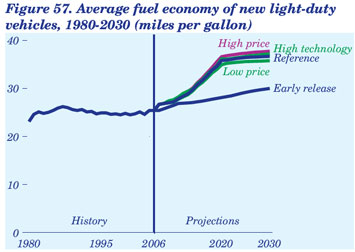

EISA2007 Improves Fuel Economy

of Light-Duty Vehicles

Light trucks have made up a steadily growing share of

U.S. LDV sales in recent years, accounting for more

than 50 percent of all new LDVs in 2006, compared

with 21 percent in 1980 [81]. Consequently, despite

fuel economy improvements, the average fuel economy

of new LDVs declined from a 1987 peak of 26.2

mpg to a low of 25.4 mpg in 2005 and remained at

roughly that level in 2006 (Figure 57).

EISA2007, enacted in December 2007, sets a new

CAFE standard of 35 mpg for LDVs in 2020. Without

EISA2007 (in the early release case), some advanced

vehicle technologies are adopted, and the average fuel

economy for new LDVs increases to 30.0 mpg in 2030.

In the AEO2008 reference case, with the EISA2007

provisions included, the fuel economy of new LDVs

increases to 36.6 mpg in 2030.

The economics of fuel-saving technologies improve

further in the high technology and high price cases,

and consumers buy more fuel-efficient cars and

trucks. In both cases, however, average fuel economy

improves only modestly from the reference case level,

because meeting the CAFE standards in EISA2007

already requires significant penetration of advanced

technologies, pushing fuel economy improvements to

the limit of current economic feasibility. In the low

price case there is little or no economic incentive for

consumers to purchase more fuel-efficient vehicles,

and LDV fuel economy in 2030 is slightly lower than

in the reference case.

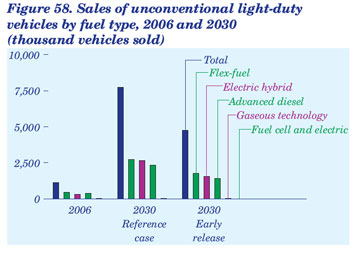

Unconventional Vehicle Technologies

Exceed 25 Percent of Sales in 2030

Concerns about oil supply, fuel prices, and emissions

have driven the development and market penetration

of unconventional vehicles (which can use alternative

fuels, electric motors and advanced electricity storage,

advanced engine controls, or other new technologies).

Unconventional technologies are expected to

play an even greater role in meeting the LDV CAFE

standards in EISA2007. In the reference case (with

EISA2007), unconventional vehicle sales total 7.7

million units (42 percent of new LDV sales) in 2030.

Without EISA2007, only 4.7 million units are sold in

2030, making up 25 percent of total new LDV sales

(Figure 58).

Sales of hybrid vehicles grow to 2.7 million units in

2030 in the reference case, compared with 1.6 million

units without EISA2007. Light-duty diesel engines

with advanced direct injection, which can significantly

reduce exhaust emissions and improve efficiency,

capture 13 percent of the market for new

LDVs in 2030. The availability of ultra-low-sulfur

diesel (ULSD) and biodiesel fuels, along with advances

in emission control technologies that reduce

criteria pollutants, increase the sales of unconventional

diesel vehicles.

Currently, manufacturers have an incentive to sell

flex-fuel vehicles (FFVs), because they receive fuel

economy credits that count toward CAFE compliance.

Although the credits are phased out by 2020 under

EISA2007, FFV sales increase from 454,600 units in

2006 to 2.7 million units in 2030 in the reference case

as a result of the growing use of E85 that is needed to

satisfy the EISA2007 RFS.

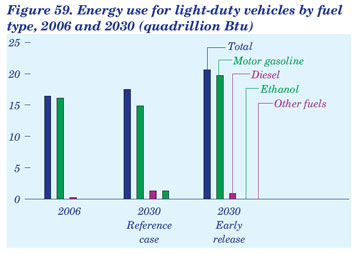

EISA2007 Reduces Light-Duty Vehicle

Fuel Use by 3 Quadrillion Btu in 2030

In the reference case, EISA2007 reduces energy consumption

for LDVs by more than 3 quadrillion Btu

in 2030, from 20.6 quadrillion Btu without EISA2007

to 17.5 quadrillion Btu with the bill (Figure 59).

Although total vehicle sales are approximately the

same in 2030 with and without EISA2007, higher

CAFE standards lead to the savings in energy

consumption.

With EISA2007, LDV motor gasoline consumption

drops by 4.9 quadrillion Btu in 2030, from 19.7

quadrillion Btu to 14.8 quadrillion Btu. Much of the

decline results from switching to unconventional

technologies. Diesel fuel consumption in 2030, including

biodiesel and BTL diesel, is 1.3 quadrillion Btu,

0.4 quadrillion Btu higher than without EISA2007;

and E85 consumption is 1.3 quadrillion Btu in 2030,

up from almost zero without EISA2007. The amount

of ethanol used in blending is about the same in both

cases because of EPA restrictions on ethanol fuel

blending.

As a result of EISA2007, the motor gasoline share of

fuel use for new LDVs in 2030 declines, and the

shares of diesel and ethanol increase. In the reference

case, motor gasoline accounts for 84.7 percent of the

total, down from 95.4 percent without EISA2007.

The diesel fuel share increases to 7.5 percent of total

consumption, and the ethanol share increases to 7.7

percent [82].

Market Trends Notes |