Newmont Mining

Corporation is the world’s largest gold producer with significant assets or operations in the United States, Australia, Peru, Indonesia, Canada, Uzbekistan, Bolivia, New Zealand, Ghana and Mexico. As of December 31, 2004, Newmont had proven and

probable gold reserves of 92.4 million equity ounces and an aggregate land position of approximately 51,500 square miles (133,500 square kilometers). In 2004, we derived more than 65% of our equity gold sales from politically and economically stable

countries, namely the United States, Australia and Canada. Newmont is also engaged in the production of silver, copper and zinc.

Newmont Mining Corporation’s original predecessor corporation was incorporated in 1921 under the laws of Delaware. On February 13, 2002, at a special

meeting of the stockholders of Newmont, stockholders approved adoption of an Agreement and Plan of Merger that provided for a restructuring of Newmont to facilitate the February 2002 acquisitions described below and to create a more flexible

corporate structure. Newmont merged with an indirect, wholly-owned subsidiary, which resulted in Newmont becoming a wholly-owned subsidiary of a new holding company. The new holding company was renamed Newmont Mining Corporation. There was no impact

to the consolidated financial statements of Newmont as a result of this restructuring and former stockholders of Newmont became stockholders of the new holding company. In this report, “Newmont,” the “Company” and “we”

refer to Newmont Mining Corporation and/or our affiliates and subsidiaries.

On February 16, 2002, Newmont completed the acquisition of Franco-Nevada Mining Corporation Limited, a Canadian company, pursuant to a Plan of Arrangement. On February 20, 2002, Newmont gained control of Normandy

Mining Limited, an Australian company, through an off-market bid for all of the ordinary shares of Normandy. On February 26, 2002, when Newmont’s off-market bid for Normandy expired, Newmont had a relevant interest in more than 96% of

Normandy’s outstanding shares. Newmont exercised compulsory acquisition rights under Australian law to acquire all of the remaining shares of Normandy in April 2002. The results of operations of Normandy and Franco-Nevada have been included in

this Annual Report and Newmont’s financial statements from February 16, 2002 forward.

In November 2003, Newmont completed a public offering of 25 million shares of common stock, receiving proceeds of approximately $1.0 billion.

For the years ended December 31, 2004, 2003, and 2002, Newmont had revenues of $4.52 billion, $3.16 billion, and $2.62

billion, respectively. In 2004, 2003 and 2002, Newmont had net income applicable to common shares of $434.5 million, $475.7 million and $154.3 million, respectively.

(1)

Newmont’s corporate headquarters are in Denver, Colorado, USA.

(1)

All references to “dollars,” “U.S.$,” or “$” in this report refer to United States currency unless otherwise specified. References to

“A$” are to Australian currency, “CDN$” to Canadian currency, “NZD$” to New Zealand currency, “IDR” to Indonesian currency and “CHF” to Swiss currency.

For additional information, see Item 7, Management’s Discussion and Analysis of Consolidated

Financial Condition and Results of Operations.

Segment Information, Export Sales, etc.

Newmont predominantly operates in a single industry, namely exploration for and production of gold and copper. Newmont’s major operations are in North America, South America, Indonesia and Australia/New Zealand. Newmont also has two

significant development projects in Ghana, West Africa. Newmont also has a Merchant Banking Segment and an Exploration Segment. See Note 25 to the Consolidated Financial Statements for information relating to our business segments, our domestic and

export sales, and our customers.

Products

Gold

General.

Newmont sold

7.0 million equity ounces of gold in 2004, 7.4 million equity ounces in 2003 and 7.6 million equity ounces in 2002. References in this report to “equity ounces” or “equity pounds” mean that portion of gold or base metals,

respectively, produced, sold, or included in proven and probable reserves that is attributable to our ownership or economic interest. For the years ended December 31, 2004, 2003 and 2002, 81%, 98% and 98%, respectively, of Newmont’s revenues

were attributable to gold sales.

Approximately 39% of

Newmont’s equity gold sales in 2004 and 2003 came from North American operations and 61% came from overseas operations. Of Newmont’s 2004 equity gold sales, approximately 22% came from Yanacocha and 7% from Indonesia. As of December 31,

2004, approximately 46% of our total long-lived assets were related to operations outside North America, with 19% of that total in Indonesia and 11% in Peru.

Most of Newmont’s revenue comes from the sale of refined gold in the international market. The end product at each of Newmont’s gold operations,

however, is generally doré bars. In certain limited circumstances Newmont sells doré directly to a customer, but generally, because doré is an alloy consisting mostly of gold but also containing silver, copper and other metals,

doré bars are sent to refiners to produce bullion that meets the required market standard of 99.95% pure gold. Under the terms of refining agreements, the doré bars are refined for a fee, and Newmont’s share of the refined gold

and the separately-recovered silver are credited to Newmont’s account or delivered to buyers, except in the case of the doré produced from Newmont’s operation in Uzbekistan. Doré from that operation is refined locally and the

refined gold is physically returned to Newmont for sale in international markets.

Newmont has interests in two gold refining businesses: a 40% interest in the AGR Matthey joint venture in Australia, which is one of the world’s largest gold refineries and the largest distributor into the Asian

market; and a 50% interest in European Gold Refineries SA in Switzerland, which owns 100% of a gold refining business and 66.65% of a gold distribution business.

Gold Uses.

Gold has two main categories of use—product fabrication and investment.

Fabricated gold has a variety of end uses, including jewelry, electronics, dentistry, industrial and decorative uses, medals, medallions and official coins. Gold investors buy gold bullion, official coins and high-karat jewelry.

Gold Supply.

The worldwide supply of gold

consists of a combination of new production from mining and the draw-down of existing stocks of bullion and fabricated gold held by governments, financial institutions, industrial organizations and private individuals. In recent years, mine

production has accounted for 60% to 70% of the total annual supply of gold.

Gold Price.

The following table presents the annual high, low and average

afternoon fixing prices for gold over the past ten years, expressed in U.S. dollars per ounce on the London Bullion Market.

Year

High

Low

Average

1995

$

396

$

372

$

384

1996

$

415

$

367

$

388

1997

$

362

$

283

$

331

1998

$

313

$

273

$

294

1999

$

326

$

253

$

279

2000

$

313

$

264

$

279

2001

$

293

$

256

$

271

2002

$

349

$

278

$

310

2003

$

416

$

320

$

363

2004

$

454

$

375

$

410

2005 (through March 3, 2005)

$

435

$

411

$

424

Source

of Data: Kitco and Reuters

On March 3, 2005, the afternoon fixing price for gold on the London Bullion Market was $430.20 per ounce and the spot market price of gold on the New York

Commodity Exchange was $429.40 per ounce.

Newmont generally

sells its gold or doré at the prevailing market prices during the month in which the gold or doré is delivered to the customer. Newmont recognizes revenue from a sale when the price is determinable, the gold or doré has been

delivered, the title has been transferred to the customer and collection of the sales price is reasonably assured.

Copper

General.

At December 31, 2004, Newmont had a 52.875% economic interest (a 45% ownership interest) in the Batu Hijau mine in

Indonesia, which began production in 1999. Production at Batu Hijau is in the form of a copper/gold concentrate that is sold to smelters for smelting and refining. During 2004, Batu Hijau sold concentrates containing 378.8 million equity pounds of

copper and 396,300 equity ounces of gold. The 100% owned Golden Grove operation in Western Australia produces concentrates that contain copper, gold, lead and zinc. Golden Grove sold concentrates containing 43.5 million pounds of copper during 2004.

Except for hedged commitments (see Note 16 to the Consolidated Financial Statements), the majority of Newmont’s copper production is sold under long-term contracts at market prices, and the balance on the spot market. For the years ended

December 31, 2004, 2003 and 2002, 19%, 2% and 1%, respectively, of Newmont’s revenues were attributable to copper sales.

Copper Uses.

Refined copper, the final product from the treatment of concentrates, is incorporated into wire and cable

products for use in the construction, electric utility, communications and transportation industries. Copper is also used in industrial equipment and machinery, consumer products and a variety of other electrical and electronic applications and is

used to make brass. Copper substitutes include aluminum, plastics, stainless steel and fiber optics. Refined, or cathode, copper is also an internationally traded commodity.

Copper Price.

The price of copper is quoted on the London Metal Exchange in

terms of dollars per metric ton of high grade copper. The volatility of the copper market is illustrated by the following table, which shows the dollar per pound equivalent of the high, low and average prices of high grade copper on the London Metal

Exchange in each of the last ten years.

Year

High

Low

Average

1995

$

1.47

$

1.23

$

1.33

1996

$

1.29

$

0.83

$

1.04

1997

$

1.23

$

0.77

$

1.03

1998

$

0.85

$

0.65

$

0.75

1999

$

0.84

$

0.61

$

0.71

2000

$

0.91

$

0.73

$

0.82

2001

$

0.83

$

0.60

$

0.72

2002

$

0.77

$

0.64

$

0.71

2003

$

1.05

$

0.70

$

0.81

2004

$

1.49

$

1.06

$

1.30

2005 (through March 3, 2005)

$

1.54

$

1.39

$

1.46

Source

of Data: London Metal Exchange

On March 3, 2005, the closing price of high grade copper was $1.51 per pound on the London Metal Exchange.

Hedging Activities

Newmont

generally avoids gold hedging. Newmont’s philosophy is to provide shareholders with leverage to changes in metal prices by selling its gold production at market prices. Newmont has, on a limited basis, entered into derivative contracts to

protect the selling price for certain anticipated gold and copper production and to manage risks associated with commodities, interest rates and foreign currencies.

At the time of Normandy’s acquisition, three of Normandy’s affiliates had substantial derivative instrument

positions. Normandy entered into gold forward sales contracts with fixed and floating gold lease rates, but did not enter into contracts that required margin calls and had no outstanding long-dated sold call options.

Following the acquisition, and in accordance with Newmont’s philosophy

regarding gold hedging, the Normandy hedge positions were reduced by approximately 9.6 million ounces from February 16, 2002 to December 31, 2004. Gold forward sales contracts and other “committed hedging obligations” were reduced by 7.5

million ounces by delivering production into the contracts or through early close-outs. Similarly, uncommitted contracts for 2.1 million ounces were either delivered into, were allowed to lapse or were closed out early. As of December 31, 2004, the

Normandy hedge positions had been reduced to 324,750 uncommitted ounces with a negative mark-to-market valuation of $9 million.

During the year ended December 31, 2004, Newmont entered into copper option collar contracts.

For additional information, see Hedging in Item 7A, Quantitative and

Qualitative Disclosures about Market Risk, and Note 16 to the Consolidated Financial Statements.

Merchant Banking

Merchant

Banking is a “reportable segment” for financial reporting purposes. Merchant Banking, also referred to as Newmont Capital, manages a Royalty Portfolio, an Equity Portfolio, and a Downstream Gold Refining business, and engages in Value

Realization activities (managing interests in oil and gas, iron ore, and coal properties as well as providing in-house investment banking and advisory services).

Merchant Banking manages Newmont’s Royalty Portfolio. Royalties generally offer a natural hedge

against lower gold prices by providing free cash flow from a diversified set of assets with limited operating, capital or environmental risk while retaining upside exposure to further exploration discoveries and reserve expansions. Merchant Banking

seeks to grow Newmont’s royalty portfolio in a number of different ways, and looks for opportunities to acquire existing royalties from third parties or to create them in connection with transactions. Merchant Banking also identifies current

Newmont properties or exploration targets for sale if they are incompatible with our core objectives. In the case of a sale, Merchant Banking often seeks to retain royalty or other future participation rights in addition to cash or other

consideration received in the sale. Through this process, Newmont intends to continue to benefit from any discoveries made by other operators on lands on which we have a royalty, and to obtain revenues from the properties without incurring operating

or capital risk.

In 2004, Newmont’s royalty interests and

investments generated $65.8 million in

Royalty and dividend income

. Newmont has royalty interests in Barrick Gold Corporation’s Goldstrike and Eskay Creek mines, Placer Dome’s Henty and Bald Mountain mines and Stillwater

Mining’s Stillwater and East Boulder palladium-platinum mines, among others. Newmont also has a significant oil and gas royalty portfolio in western Canada. During the year, new royalties were added through property transactions and asset

sales. A land lease program in Nevada is accelerating exploration of non-core lands with Newmont retaining royalties and future participation rights. For additional information regarding Newmont’s royalty portfolio, see Item 2, Properties,

Royalty Properties, below.

As of December 31, 2004, Merchant

Banking’s Equity Portfolio had a market value of approximately $0.5 billion. The Equity Portfolio is primarily composed of our investments in Kinross Gold Corporation, Canadian Oil Sands Trust and Gabriel Resources, Ltd.

Merchant Banking also manages our interests in downstream gold refining and

distribution businesses (40% interest in AGR Matthey Joint Venture (“AGR”) and 50% interest in European Gold Refineries (“EGR”)). Merchant Banking earned $2.6 million in

Equity income of affiliates

through its investments

in AGR and EGR in 2004.

Merchant Banking’s Value

Realization activities include managing the reserve delineation program on our 100% owned heavy oil leases in Alberta, Canada, and advancing our other interests in coal, iron ore and natural gas.

Merchant Banking provides advisory services to Newmont to assist it in

managing its portfolio of operating and property interests. The Merchant Banking group helps Newmont maximize net asset value per share and increase cash flow, earnings and reserves by working with Newmont’s exploration, operations and finance

teams to prioritize near-term goals within longer-term strategies. Merchant Banking is engaged in developing value optimization strategies for operating and non-operating assets, business development activities, potential merger and acquisition

analysis and negotiations, monetizing inactive exploration properties, capitalizing on Newmont’s proprietary technology and know-how and acting as an internal resource for other corporate groups to improve and maximize business outcomes. In

2004, Merchant Banking’s assistance was provided in the sale of non-core properties including Bronzewing in Australia, Perama in Greece and Midwest Uranium in Canada. In addition, Merchant Banking participated in the restructuring of Australian

Magnesium Corporation, which eliminated all remaining Newmont obligations.

A key aspect of these advisory services is assisting Newmont in extracting economies of scale with its partners and neighboring mines. Merchant Banking continues to evaluate district optimization opportunities in

Nevada, Australia and Canada, covering a broad range of alternatives, including asset exchanges, unitization, joint ventures, partnerships, sales, spinouts and buyouts.

Exploration

Exploration is a

“reportable segment” for financial reporting purposes. Newmont’s exploration group is responsible for all activities, regardless of location, associated with the Company’s world-wide efforts to discover mineralized material and

advance such mineralized material into proven and probable reserves.

Exploration work is conducted in areas surrounding our existing mines for the purpose of locating additional deposits and determining mine geology, and in

other prospective gold regions globally. Our exploration teams employ state-of-the-art technology, including airborne geophysical data acquisition systems, satellite location devices and field-portable imaging systems, as well as geochemical and

geological prospecting methods, to identify prospective targets. Newmont spent $192.4 million in 2004, $115.2 million in 2003 and $88.9 million in 2002 on

Exploration, research and development

.

As of December 31, 2004, Newmont had proven and probable reserves of 92.4

million equity ounces. As a result of exploration efforts and the assumption of a higher gold price, Newmont added 12.4 million equity ounces to proven and probable reserves in 2004, with 11.3 million ounces of depletion, divestitures and

reclassifications during the year.

In Nevada, exploration

efforts resulted in proven and probable reserves of 34.0 million equity ounces as of December 31, 2004, after depletion of 3.0 million equity ounces during 2004.

In Peru, equity gold reserves increased to 16.6 million ounces, after depletion of 2.0 million ounces and a reclassification

of 2.0 million ounces to mineralized material not in reserves at Cerro Quilish. At Minas Conga, 4.5 million equity ounces of gold and 1.1 billion equity pounds of copper were added to proven and probable reserves. Minas Conga is a development

project that currently consists of two gold-copper porphyry deposits located northeast of the Minera Yanacocha operating area in the provinces of Celendin, Cajamarca and Hualgayoc.

In Australia/New Zealand, the Company depleted 1.9 million equity ounces during 2004. Australia/New Zealand had proven and

probable reserves of 15.1 million equity ounces at December 31, 2004.

At Batu Hijau, positive mine optimization efforts resulted in proven and probable reserves of 6.3 billion equity pounds of copper and 7.2 million equity ounces of gold as of December 31, 2004, which approximated 2003 reserves,

notwithstanding depletion of approximately 450 million equity pounds of copper and 500,000 equity ounces of gold.

In addition, exploration and mine development efforts in 2004 focused on the Ahafo and Akyem projects in Ghana, substantially increasing proven and

probable reserves there by 3.0 million and 1.1 million, respectively. As of December 31, 2004, the Company reported reserves of 10.6 million ounces at Ahafo and 5.4 million equity ounces at Akyem.

For additional information, see Item 2, Properties, Proven and Probable

Reserves.

Licenses and Concessions

Other

than operating licenses for our mining and processing facilities, there are no third party patents, licenses or franchises material to Newmont’s business. In many countries, however, we conduct our mining and exploration activities pursuant to

concessions granted by, or under contract with, the host government. These countries include, among others, Australia, Bolivia, Canada, Ghana, Indonesia, Peru, New Zealand, Mexico and Uzbekistan. The concessions and contracts are subject to the

political risks associated with foreign operations. See Item 1A, Risk Factors, Risks Related to Newmont Operations, below. For a more detailed description of our Indonesian Contracts of Work, see Item 2, Properties, below.

Condition of Physical Assets and Insurance

Our business is capital intensive, requiring ongoing capital investment for the replacement, modernization or expansion of equipment and facilities. For more information, see Item 7, Management’s Discussion and

Analysis of Consolidated Financial Condition and Results of Operations, Liquidity and Capital Resources, below.

We maintain insurance policies against property loss and business interruption and insure against risks

that are typical in the operation of our business, in amounts that we believe to be reasonable. Such insurance, however, contains exclusions and limitations on coverage, particularly with respect to environmental liability and political risk. There

can be no assurance that claims would be paid under such insurance policies in connection with a particular event. See Item 1A, Risk Factors, Risks Related to Newmont Operations, below.

Environmental Matters

Newmont’s United States mining and exploration activities are subject to various federal and state laws and regulations governing the protection of the environment, including the Clean Air Act; the Clean Water Act; the Comprehensive

Environmental Response, Compensation and Liability Act; the Emergency Planning and Community Right-to-Know Act; the Endangered Species Act; the Federal Land Policy and Management Act; the National Environmental Policy Act; the Resource Conservation

and Recovery Act; and related state laws. These laws and regulations are continually changing and are generally becoming more restrictive. Newmont’s activities outside the United States are also subject to governmental regulations for the

protection of the environment. In general, environmental regulations have not had, and are not expected to have, a material adverse impact on Newmont’s operations or our competitive position.

We conduct our operations so as to protect public health and environment and

believe our operations are in compliance with applicable laws and regulations in all material respects. Each operating Newmont mine has a reclamation plan in place that meets all applicable legal and regulatory requirements. We have made, and expect

to make in the future, expenditures to comply with such laws and regulations. We have made estimates of the amount of such expenditures, but cannot precisely predict the amount of such future expenditures. Estimated future reclamation costs are

based principally on legal and regulatory requirements. At December 31, 2004, $410.3 million was accrued for reclamation costs relating to currently producing mineral properties.

Newmont is also involved in several matters concerning environmental obligations associated with former, primarily historic,

mining activities. Generally, these matters concern developing and implementing remediation plans at the various sites. We believe that the related environmental obligations associated with these sites are similar in nature with respect to the

development of remediation plans, their risk profile and the activities required to meet general environmental standards. Based upon our best estimate of our liability for these matters, $74.9 million was accrued as of December 31, 2004 for such

obligations associated with properties previously owned or operated by Newmont or our subsidiaries. These amounts are included in

Other current liabilities

and

Reclamation and remediation liabilities.

Depending upon the ultimate

resolution of these matters, we believe that it is reasonably possible that the liability for these matters could be as much as 81% greater or 34% lower than the amount accrued as of December 31, 2004. The amounts accrued for these matters are

reviewed periodically based upon facts and circumstances available at the time. Changes in estimates are charged to costs and expenses in the period estimates are revised.

For a discussion of the most significant reclamation and remediation activities, see Item 7, Management’s Discussion

and Analysis of Consolidated Financial Condition and Results of Operations, and Notes 15 and 27 to the Consolidated Financial Statements, below.

Employees

There were

approximately 14,000 people employed by Newmont and our affiliates worldwide at December 31, 2004.

Forward-Looking Statements

Certain statements contained in this report (including information incorporated by reference) are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and

Section 21E of the Securities Exchange Act of 1934, as amended, and are intended to be covered by the safe harbor provided for under these sections. Our

forward-looking statements include, without limitation:

•

Statements regarding future earnings, and the sensitivity of earnings to gold and other metal prices;

•

Estimates of future mineral production and sales, for specific operations and on a consolidated basis;

•

Estimates of future production costs and other expenses, for specific operations and on a consolidated basis;

•

Estimates of future cash flows and the sensitivity of cash flows to gold and other metal prices;

•

Estimates of future capital expenditures and other cash needs, for specific operations and on a consolidated basis, and expectations as to the funding thereof;

•

Statements as to the projected development of certain ore deposits, including estimates of development and other capital costs, financing plans for these deposits, and expected

production commencement dates;

•

Estimates of future costs and other liabilities for certain environmental matters;

•

Estimates of reserves, and statements regarding future exploration results and reserve replacement;

•

Statements regarding modifications to hedge positions;

•

Statements regarding future transactions relating to portfolio management or rationalization efforts; and

•

Estimates regarding timing of future capital expenditures, production or closure activities.

Where we express an expectation or belief as to future events or results, such expectation or belief is expressed in good

faith and believed to have a reasonable basis. However, our forward-looking statements are subject to risks, uncertainties, and other factors, which could cause actual results to differ materially from future results expressed, projected or implied

by those forward-looking statements. Such risks include, but are not limited to: the price of gold and copper; currency fluctuations; geological and metallurgical assumptions; operating performance of equipment, processes and facilities; labor

relations; timing of receipt of necessary governmental permits or approvals; domestic and foreign laws or regulations, particularly relating to the environment and mining; domestic and international economic and political conditions; the ability of

Newmont to obtain or maintain necessary financing; and other risks and hazards associated with mining operations. More detailed information regarding these factors is included in Item 1, Business, Item 1A, Risk Factors, and elsewhere throughout this

report. Given these uncertainties, readers are cautioned not to place undue reliance on our forward-looking statements.

All subsequent written and oral forward-looking statements attributable to Newmont or to persons acting on its behalf are expressly qualified in their

entirety by these cautionary statements. Newmont disclaims any intention or obligation to update publicly any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable

securities laws.

Available Information

Newmont

maintains an internet web site at

www.newmont.com.

Newmont makes available, free of charge, through the Investor Information section of the web site, its Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form

8-K, Section 16 filings and all amendments to those reports, as soon as reasonably practicable after such material is electronically filed with the Securities and Exchange Commission. Newmont has provided same day access to such reports through its

web site since November 15, 2002. Newmont’s Corporate Governance Guidelines, the charters of key committees of its Board of Directors and its Code of Business Ethics and Conduct are also available on the web site. Any of the foregoing

information is available in print to any stockholder who requests it by contacting Newmont’s Investor Relations Department.

The Company filed with the New York Stock Exchange (“NYSE”) on May 24, 2004, the annual

certification by its Chief Executive Officer, certifying that, as of the date of the certification, he was not aware of any violation by the Company of the NYSE’s corporate governance listing standards, as required by Section 303A.12(a) of

the NYSE Listed Company Manual. The Company has filed the required certifications under Section 302 of the Sarbanes-Oxley Act of 2002 regarding the quality of its public disclosures as Exhibits 31.1 and 31.2 to this report.

ITEM 1A. RISK FACTORS

Every investor or potential investor in Newmont should carefully consider the following risks, which have been separated into two groups:

•

Risks related to the mining industry generally; and

•

Risks related to Newmont’s operations.

Risks Related to the Mining Industry Generally

A Substantial or Extended Decline in Gold or Copper Prices Would Have a Material Adverse Effect on Newmont

Newmont’s business is dependent on the prices of gold and copper, which are affected by numerous factors beyond Newmont’s control. Factors

tending to put downward pressure on the prices of gold and copper include:

•

Sales or leasing of gold by governments and central banks;

•

A strong U.S. dollar;

•

Global and regional recession or reduced economic activity;

•

Speculative trading;

•

Decreased demand for industrial uses, use in jewelry or investment;

•

High supply from production, disinvestment and scrap;

•

Sales by producers in forward transactions and other hedging transactions; and

•

Devaluing local currencies (relative to gold priced in U.S. dollars) leading to lower production costs and higher production in certain regions.

Any drop in the prices of gold or copper adversely impacts our revenues,

profits and cash flows, particularly in light of our philosophy of avoiding gold hedging. Newmont has recorded asset write-downs in prior years as a result of low gold prices and may experience additional asset impairments as a result of low gold or

copper prices in the future.

In addition, sustained low gold

or copper prices can:

•

Reduce revenues further through production cutbacks due to cessation of the mining of deposits or portions of deposits that have become uneconomic at the then-prevailing gold or

copper price;

•

Halt or delay the development of new projects;

•

Reduce funds available for exploration, with the result that depleted reserves are not replaced; and/or

•

Reduce existing reserves, by removing ores from reserves that cannot be economically mined or treated at prevailing prices.

Also see the discussion in Item 1, Business, Gold or Copper Price.

Gold and Copper Producers Must Continually Obtain Additional Reserves

Gold and copper producers must continually replace reserves depleted by

production. Depleted reserves must be replaced by expanding known ore bodies or by locating new deposits in order for producers to maintain production levels over the long term. Exploration is highly speculative in nature, involves many risks and

frequently is unproductive. No assurances can be given that any of our new or ongoing exploration programs will result in new mineral producing operations. Once mineralization is discovered, it may take many years from the initial phases of drilling

until production is possible, during which time the economic feasibility of production may change.

Estimates of Proven and Probable Reserves Are Uncertain

Estimates of proven and probable reserves are subject to considerable uncertainty. Such estimates are, to a large extent,

based on interpretations of geologic data obtained from drill holes and other sampling techniques. Producers use feasibility studies to derive estimates of operating costs based upon anticipated tonnage and grades of ore to be mined and processed,

the predicted configuration of the ore body, expected recovery rates of metals from the ore, comparable facility, equipment, operating costs, and other factors. Actual operating costs and economic returns on projects may differ significantly from

original estimates. Further, it may take many years from the initial phase of drilling before production is possible and, during that time, the economic feasibility of exploiting a discovery may change.

Increased Costs Could Affect Profitability

Costs at any particular mining location frequently are subject to variation

from one year to the next due to a number of factors, such as changing ore grade, metallurgy and revisions to mine plans in response to the physical shape and location of the ore body. In addition, costs are affected by the price of commodities such

as fuel and electricity. Such commodities are at times subject to volatile price movements, including increases that could make production at certain operations less profitable. A material increase in costs at any significant location could have a

significant effect on Newmont’s profitability.

Mining Accidents or Other Adverse Events at a Mining Location Could Reduce Our Production Levels

At any of Newmont’s operations, production may fall below historic or estimated levels as a result of mining accidents such as a pit wall failure in

an open pit mine, or cave-ins or flooding at underground mines. In addition, production may be unexpectedly reduced at a location if, during the course of mining, unfavorable ground conditions or seismic activity are encountered; ore grades are

lower than expected; the physical or metallurgical characteristics of the ore are less amenable to mining or treatment than expected; or our equipment, processes or facilities fail to operate properly or as expected.

Mining Companies Are Subject to Extensive Environmental Laws and

Regulations

Newmont’s exploration, mining and

processing operations are regulated in all countries in which we operate under various federal, state, provincial and local laws relating to the protection of the environment, which generally include air and water quality, hazardous waste management

and reclamation. Delays in obtaining or failure to obtain government permits and approvals may adversely impact our operations. The regulatory environment in which Newmont operates could change in ways that would substantially increase costs to

achieve compliance, or otherwise could have a material adverse effect on Newmont’s operations or financial position. For a more detailed discussion of potential environmental liabilities, see the discussion in Environmental Matters, Note 27 to

the Consolidated Financial Statements.

Our Operations Outside North America and Australia Are Subject to Risks of Doing Business Abroad

Exploration, development and production activities outside of North America and Australia are potentially subject to political and economic risks,

including:

•

Cancellation or renegotiation of contracts;

•

Disadvantages of competing against companies from countries that are not subject to U.S. laws and regulations, including the Foreign Corrupt Practices Act;

•

Changes in foreign laws or regulations;

•

Royalty and tax increases or claims by governmental entities, including retroactive claims;

•

Expropriation or nationalization of property;

•

Currency fluctuations (particularly in countries with high inflation);

•

Foreign exchange controls;

•

Restrictions on the ability of local operating companies to sell gold offshore for U.S. dollars, or on the ability of such companies to hold U.S. dollars or other foreign currencies

in offshore bank accounts;

•

Import and export regulations, including restrictions on the export of gold;

•

Restrictions on the ability to pay dividends offshore;

•

Risk of loss due to civil strife, acts of war, guerrilla activities, insurrection and terrorism;

•

Risk of loss due to disease and other potential endemic health issues; and

•

Other risks arising out of foreign sovereignty over the areas in which our operations are conducted.

Consequently, Newmont’s exploration, development and production activities outside of North America and Australia may

be substantially affected by factors beyond Newmont’s control, any of which could materially adversely affect Newmont’s financial position or results of operations. Furthermore, in the event of a dispute arising from such activities,

Newmont may be subject to the exclusive jurisdiction of courts outside North America or Australia, which could adversely affect the outcome of a dispute.

Newmont has substantial investments in Indonesia, a nation that since 1997 has undergone financial crises and devaluation of its currency, outbreaks of

political and religious violence, changes in national leadership, and the secession of East Timor, one of its former provinces. These factors heighten the risk of abrupt changes in the national policy toward foreign investors, which in turn could

result in unilateral modification of concessions or contracts, increased taxation, denial of permits or permit renewals or expropriation of assets. If this were to occur with respect to the Batu Hijau Contract of Work, Newmont’s financial

condition and results of operations could be materially adversely affected.

In July 2004, a criminal complaint was filed against P.T. Newmont Minahasa Raya (“PTNMR”), the Newmont subsidiary that operated the Minahasa mine in Indonesia, alleging environmental pollution relating to

submarine tailings placement into nearby Buyat Bay. The Indonesian police detained five PTNMR employees during September and October of 2004. The police investigation and the detention of PTNMR’s employees was declared illegal by the South

Jakarta District Court in December of 2004, and the police have appealed that decision to the Indonesian Supreme Court. A civil lawsuit, which was filed by three residents of Buyat Pante, a village located near the Minahasa mine, was settled without

payment to the plaintiffs in December 2004. In addition, on March 9, 2005, the Indonesian Ministry of the Environment reportedly filed a civil lawsuit against PTNMR and its President Director in relation to these allegations.

Independent sampling and testing of Buyat Bay water and fish, as well as area

residents, conducted by the World Health Organization and the Australian Commonwealth Scientific and Industrial Research Organization,

confirm that PTNMR has not polluted the Buyat Bay environment, and, therefore, has not adversely affected the fish in the Bay or the health of nearby

residents. The Company remains steadfast that it has not caused pollution or health problems and will continue to vigorously defend itself against these allegations. However, Newmont cannot predict the outcome of these actions or whether additional

legal actions may occur. Any of these actions could adversely affect our ability to operate in Indonesia.

During the last several years, Minera Yanacocha, of which Newmont owns a 51.35% interest, has been the target of numerous local political protests,

including ones that blocked the road between the Yanacocha mine complex and the city of Cajamarca in Peru. During September 2004, individuals from the Cajamarca region conducted a sustained blockade of the road in protest of drilling activities at

Cerro Quilish, one of the ore deposits within the Yanacocha mine complex. Yanacocha suspended all drilling activities at Cerro Quilish, and the blockade was resolved. At the request of Yanacocha, the Cerro Quilish drilling permit was revoked in

November 2004. Newmont has reassessed the challenges involved in obtaining required permits for Cerro Quilish primarily related to increased community concerns. Based upon this reassessment, Newmont has reclassified the deposit’s 1.98 million

equity gold ounces from proven and probable reserves to mineralized material not in reserves as of December 31, 2004. We cannot predict whether these incidents will continue, nor can we predict the government’s continuing positions on foreign

investment, mining concessions, land tenure, environmental regulation or taxation. The continuation or intensification of protests or a change in prior governmental positions could adversely affect operations in Peru.

Recent violence committed by radical elements in Indonesia and other

countries, and the presence of U.S. forces in Iraq and Afghanistan, may increase the risk that operations owned by U.S. companies will be the target of further violence. If any of Newmont’s operations were so targeted it could have an adverse

effect on our business.

Our Success May Depend on Our

Social and Environmental Performance

Newmont’s

ability to operate successfully in communities around the world will likely depend on our ability to develop, operate and close mines in a manner that is consistent with the health and safety of our employees, the protection of the environment, and

the creation of long-term economic and social opportunities in the communities in which we operate. Newmont has implemented a management system designed to promote continuous improvement in health and safety, environmental performance and community

relations. However, our ability to operate may be adversely impacted by accidents or events detrimental (or perceived to be detrimental) to the health and safety of our employees, the environment or the communities in which we operate.

Remediation Costs for Environmental Liabilities May Exceed the

Provisions We Have Made

Newmont has conducted

extensive remediation work at two inactive sites in the United States. At one of these sites, remediation requirements have not been finally determined, and, therefore, the final cost cannot be determined. At a third site in the United States, an

inactive uranium mine and mill formerly operated by a subsidiary of Newmont, remediation work at the mill is ongoing, but remediation at the mine is subject to dispute and has not yet commenced. The environmental standards that may ultimately be

imposed at this site remain uncertain and there is a risk that the costs of remediation may exceed the provision that has been made for such remediation by a material amount.

Whenever a previously unrecognized remediation liability becomes known or a previously estimated cost is increased, the

amount of that liability or additional cost can materially reduce net income in that period.

The Use of Hedging Instruments May Prevent Gains Being Realized from Subsequent Price Increases

Newmont does not intend to enter into material new gold hedging positions and intends to continue to decrease gold hedge positions over time by

opportunistically delivering gold into our existing hedge contracts, or

by seeking to eliminate our hedge position when economically attractive. Nonetheless, Newmont currently has gold hedging positions and may, from

time-to-time, enter into hedge contracts for copper, other metals or commodities, interest rates or foreign currencies. In 2004, Newmont entered into copper hedging positions covering approximately 459 million pounds of copper. If the gold, copper

or other metal price rises above the price at which future production has been committed under these hedge instruments, Newmont will have an opportunity loss. However, if the gold, copper or other metal price falls below that committed price,

Newmont’s revenues will be protected to the extent of such committed production. In addition, we may experience losses if a hedge counterparty defaults under a contract when the contract price exceeds the gold, copper or other metal price.

For a more detailed description of the Newmont hedge

positions, see the discussion in Hedging in Item 7A, Quantitative and Qualitative Disclosures About Market Risk, and Note 16 to the Consolidated Financial Statements.

Currency Fluctuations May Affect Costs

Currency fluctuations may affect the costs that we incur at our operations. Gold is sold throughout the world based

principally on the U.S. dollar price, but a portion of Newmont’s operating expenses are incurred in local currencies. The appreciation of non-U.S. dollar currencies against the U.S. dollar can increase the costs of gold production in U.S.

dollar terms at mines located outside the United States, making such mines less profitable. The currencies that primarily impact Newmont’s results of operations are the Australian and Canadian dollars.

During 2004, the Australian and Canadian dollars strengthened by an average

of 13% and 7%, respectively, against the U.S. dollar. This increased U.S. dollar reported operating costs in Australia and Canada by approximately $56.6 million and $4.8 million, respectively. For additional information, see Item 7,

Management’s Discussion and Analysis of Consolidated Financial Condition and Results of Operations, Results of Operations, Foreign Currency Exchange Rates, below. For a more detailed description of how currency exchange rates may affect costs,

see discussion in Foreign Currency in Item 7A, Quantitative and Qualitative Disclosures About Market Risk.

Our Level of Indebtedness May Affect Our Business

As of December 31, 2004, Newmont had debt of $1.6 billion, as compared to $1.1 billion as of December 31, 2003. Our level of indebtedness could

have important consequences for our operations, including:

•

Newmont may need to use a large portion of its cash flow to repay principal and pay interest on our debt, which will reduce the amount of funds available to finance our operations

and other business activities;

•

Newmont’s debt level may make us vulnerable to economic downturns and adverse developments in Newmont’s businesses and markets; and

•

Newmont’s debt level may limit our ability to pursue other business opportunities, borrow money for operations or capital expenditures in the future or implement our business

strategy.

Newmont expects to be able to pay

principal and interest on our debt by utilizing cash flow from operations and Newmont’s ability to meet these payment obligations will depend on our future financial performance, which will be affected by financial, business, economic and other

factors. Newmont will not be able to control many of these factors, such as economic conditions in the markets in which Newmont operates. Newmont cannot be certain that our future cash flow from operations will be sufficient to allow us to pay

principal and interest on our debt and meet our other obligations. If cash flow from operations is insufficient, we may be required to refinance all or part of our existing debt, sell assets, utilize existing cash balances, borrow more money or

issue additional equity. We cannot be sure that we will be able to do so on commercially reasonable terms, if at all.

Our Interest in the Batu Hijau Mine in Indonesia May Be Reduced Under the Contract of Work

Under the Batu Hijau Contract of Work with the

Indonesian government, beginning in 2005 and continuing through 2010, a portion of each foreign shareholders’ equity interest in the project must be offered for sale to the Indonesian government or to Indonesian nationals. The price at which

such interest must be offered for sale to the Indonesian parties is the highest of the then-current replacement cost, the price at which shares of the project company would be accepted for listing on the Jakarta Stock Exchange, or the fair market

value of such interest in the project company as a going concern. An Indonesian national currently owns a 20% interest in Batu Hijau, which would require Newmont and Sumitomo, collectively, to offer a 3% interest to the Indonesian government or to

Indonesian nationals in 2006. Pursuant to this provision of the Batu Hijau Contract of Work, it is possible that the ownership interest of the Newmont/Sumitomo partnership in Batu Hijau could be reduced to 49% by the end of 2010.

Occurrence of Events for Which We Are Not Insured May Affect Our Cash

Flow and Overall Profitability

We maintain insurance

policies to protect ourselves against certain risks related to our operations. This insurance is maintained in amounts that we believe to be reasonable depending upon the circumstances surrounding each identified risk. However, Newmont may elect not

to have insurance for certain risks because of the high premiums associated with insuring those risks or for various other reasons; in other cases, insurance may not be available for certain risks. Some concern always exists with respect to

investments in parts of the world where civil unrest, war, nationalist movements, political violence or economic crisis are possible. These countries may also pose heightened risks of expropriation of assets, business interruption, increased

taxation and a unilateral modification of concessions and contracts. Newmont does not maintain insurance policies against political risk. Occurrence of events for which Newmont is not insured may affect our cash flow and overall profitability.

Our Business Depends on Good Relations with Our

Employees

Newmont could experience labor disputes,

work stoppages or other disruptions in production that could adversely affect us. At December 31, 2004, unions represented approximately 20% of our worldwide work force. On that date, Newmont had 1,098 employees at its Carlin, Nevada operations, 211

employees in Canada at its Golden Giant operations, 2,727 employees in Indonesia at its Batu Hijau operations, 41 employees in New Zealand at its Martha operation, 325 employees in Bolivia at its Kori Kollo operation, 628 employees at its Australia

operations, and 552 employees in Peru at its Yanacocha operation, working under a collective bargaining agreement or similar labor agreement. Currently there are labor agreements in effect for all of these workers.

Our Earnings Could Be Affected by the Prices of Other Commodities

The earnings of Newmont also could be affected by the

prices of other commodities such as fuel and other consumable items, although to a lesser extent than by the price of gold or copper. The prices of these commodities are affected by numerous factors beyond Newmont’s control.

Title to Some of Our Properties May Be Defective or Challenged

Although we have conducted title reviews of our

properties, title review does not necessarily preclude third parties from challenging our title. While Newmont believes that it has satisfactory title to its properties, some risk exists that some titles may be defective or subject to challenge. In

addition, certain of our Australian properties could be subject to native title or traditional landowner claims, but such claims would not deprive us of the properties. For information regarding native title or traditional landowner claims, see the

discussion under the Australia section of Item 2, Properties, below.

We compete with other mining companies to attract and retain key executives

and other employees with technical skills and experience in the mining industry. We also compete with other mining companies for rights to mine properties containing gold and other minerals. There can be no assurance that Newmont will continue to

attract and retain skilled and experienced employees, or to acquire additional rights to mine properties.

Certain Factors Outside of Our Control May Affect Our Ability to Support the Carrying Value of Goodwill

At December 31, 2004, the carrying value of our goodwill was approximately

$3.0 billion or 24% of our total assets. Such goodwill has been assigned to our Merchant Banking ($1.6 billion) and Exploration ($1.1 billion) Segments, and to various mine site reporting units ($0.3 billion in the aggregate). This goodwill arose in

connection with our February 2002 acquisitions of Normandy and Franco-Nevada, and it represents the excess of the aggregate purchase price over the fair value of the identifiable net assets of Normandy and Franco-Nevada. We evaluate, on at least an

annual basis, the carrying amount of goodwill to determine whether current events and circumstances indicate that such carrying amount may no longer be recoverable. This evaluation involves a comparison of the fair value of our reporting units to

their carrying values.

Based on valuations of the Merchant

Banking and Exploration Segments, the Company concluded that the fair values significantly exceeded the respective carrying values as of December 31, 2004. The fair values of the reporting units are based in part on certain factors that may be

partially or completely outside of our control, such as the investing environment, the discovery of proven and probable reserves, commodity prices and other factors. In addition, certain of the assumptions underlying the December 31, 2004 Merchant

Banking and Exploration valuations may not be easily achieved by the Company, even though such assumptions were based on historical experience and the Company considers such assumptions to be reasonable under the circumstances.

At December 31, 2004, the $1.6 billion carrying value of the Merchant Banking

Segment goodwill represented approximately 65% of the carrying value of the total assets of the Merchant Banking Segment. The December 31, 2004 discounted cash flow analysis for the equity portfolio sub-segment of the Merchant Banking Segment

assumed: (i) a discount rate of 9%; (ii) a time horizon of ten years; (iii) pre-tax returns on investment ranging from 35% starting in 2005 and gradually declining to 15% in 2012 through 2014; (iv) an initial equity portfolio investment of

approximately $0.5 billion; (v) capital infusions of $50 million annually for the next three years; and (vi) a terminal value of approximately $2.2 billion. The December 31, 2004 discounted cash flow analysis for the royalty portfolio sub-segment of

the Merchant Banking Segment assumed: (i) a discount rate of 9%; (ii) a time horizon of ten years; (iii) an annual growth rate of 5% in the royalty portfolio; and (iv) a pre-tax rate of return on investment of 13%. The December 31, 2004 discounted

cash flow analysis for the portfolio management sub-segment of the Merchant Banking Segment assumed: (i) a discount rate of 9%; (ii) a time horizon of ten years; and (iii) a pre-tax advisory fee of 5% on approximately $0.5 billion of transactions

and value-added activities in 2005, with the dollar amount of such transactions and activities increasing by 5% annually thereafter. The December 31, 2004 discounted cash flow analysis for the value realization sub-segment of the Merchant Banking

Segment assumed: (i) a discount rate of 9%; (ii) a time horizon of ten years; and (iii) a pre-tax annual return on investments of $4.2 million. The December 31, 2004 discounted cash flow analysis assumed a combined terminal value for the royalty

portfolio, portfolio management and downstream gold refining sub-segments of approximately $0.7 billion.

At December 31, 2004, the $1.1 billion carrying value of the Exploration Segment goodwill represented approximately 98% of the carrying value of the total

assets of the Exploration Segment. Based on the review of historical additions to proven and probable reserves and on management’s expectation of the growth rate and levels of reserve additions that could be expected to continue in the future,

the discounted cash flow model developed to value the Exploration Segment at December 31, 2004 assumed that (i) the Exploration Segment

would be responsible for 11.0 million ounces of additions to proven and probable reserves in 2005; (ii) such additions would increase by 5% annually; and

(iii) approximately 9.1%, 8.7%, 8.3% and 7.9% of additions in years 2005, 2006, 2007 and 2008, respectively, would represent ounces that had previously been valued in the Normandy purchase accounting. In addition, the discounted cash flow model for

the Exploration Segment assumed, among other matters: (i) a 16-year time horizon, including a seven-year time lapse between additions to proven and probable reserves and the initiation of production and a five-year production period; (ii) a discount

rate of 8%; (iii) a terminal value of approximately $5.8 billion; (iv) an average gold price of $375 per ounce during the time horizon; (v) total cash costs per ounce of $230; and (vi) capital costs of $50 per ounce. The Company believes that any

model used to value the Exploration Segment will need to take into account the relatively long time horizon required to evaluate the activities of the Exploration Segment.

In the absence of any mitigating valuation factors, the Company’s failure to achieve one or more of the December 31,

2004 valuation assumptions will over time result in an impairment charge. Accordingly, no assurance can be given that significant non-cash impairment charges will not be recorded in the future due to possible declines in the fair values of our

reporting units. For a more detailed description of the estimates and assumptions involved in assessing the recoverability of the carrying value of goodwill, see Item 7, Management’s Discussion and Analysis of Consolidated Financial Condition

and Results of Operations, Critical Accounting Policies, below.

Our Ability to Recognize the Benefits of Deferred Tax Assets is Dependant on Future Cash Flows and Taxable Income

The Company recognizes the expected future tax benefit from deferred tax assets when the tax benefit is considered to be more likely than not of being

realized. Otherwise, a valuation allowance is applied against deferred tax assets. Assessing the recoverability of deferred tax assets requires management to make significant estimates related to expectations of future taxable income. Estimates of

future taxable income are based on forecasted cash flows from operations and the application of existing tax laws in each jurisdiction. To the extent that future cash flows and taxable income differ significantly from estimates, the ability of the

Company to realize the deferred tax assets recorded at the balance date could be impacted. Additionally, future changes in tax laws in the jurisdictions in which the Company operates could limit the Company’s ability to obtain the future tax

benefits represented by its deferred tax assets recorded at the balance sheet date. At December 31, 2004, the Company recorded $173.6 million and $491.7 million of current and long-term deferred tax assets, respectively.

ITEM 2. PROPERTIES

Gold and Copper Processing Methods

Gold is extracted from naturally-oxidized ores by either heap leaching or milling, depending on the amount of gold contained in the ore and the amenability of the ore to treatment. Higher grade oxide ores are generally processed through

mills, where the ore is ground into a fine powder and mixed with water in slurry, which then passes through a cyanide leaching circuit. Lower grade oxide ores are generally processed using heap leaching. Heap leaching consists of stacking crushed or

run-of-mine ore on impermeable pads, where a weak cyanide solution is applied to the top surface of the heap to dissolve the gold. In both cases, the gold-bearing solution is then collected and pumped to process facilities to remove the gold by

collection on carbon or by zinc precipitation directly from leach solutions.

Gold contained in ores that are not naturally oxidized can be directly milled if the gold is amenable to cyanidization, generally known as free milling ores. Ores that are not amenable to cyanidization, known as

refractory ores, require more costly and complex processing techniques than oxide or free milling ore. Higher-grade refractory ores are processed through either roasters or autoclaves. Roasters heat finely ground ore with air and oxygen to a high

temperature, burn off the carbon and oxidize the sulfide minerals that prevent efficient leaching. Autoclaves use heat, oxygen and pressure to oxidize sulfide minerals in the ore.

Some gold-bearing sulfide ores may be processed through a flotation plant or by bio-milling. In

flotation, ore is finely ground, turned into slurry, then placed in a tank known as a flotation cell. Chemicals are added to the slurry causing the gold-containing sulfides to float in air bubbles to the top of the tank, where they can be separated

from waste particles that sink to the bottom. The sulfides are removed from the cell and converted into a concentrate that can then be processed in an autoclave or roaster to recover the gold. Bio-milling incorporates patented technology that

involves inoculation of suitable crushed ore on a leach pad with naturally occurring bacteria strains, which oxidize the sulfides over a period of time. The ore is then processed through an oxide mill.

At Batu Hijau, mined ore containing copper and gold is crushed to a coarse

size at the mine and then transported from the mine via conveyor to a concentrator. The ore is finely ground and then treated by successive stages of flotation, resulting in a concentrate of copper sulfides containing approximately 30% copper. The

concentrate is transferred by pipeline to port facilities. At the port, the concentrate is dewatered and stored for later reclaiming and loading onto ships for transport to smelters.

Newmont Properties

Production Properties

Set forth

below is a description of the significant production properties of Newmont and its subsidiaries. Total cash costs and total production costs for each operation are presented in a table in the next section of this Item 2. Total cash costs and total

production costs represent measures of performance that are not calculated in accordance with generally accepted accounting principles (“GAAP”). Management uses these non-GAAP financial measures to analyze the cash generating capacities

and performance of Newmont’s mining operations. For a reconciliation of these non-GAAP measures to

Costs Applicable to Sales

as calculated and presented under GAAP, see Item 2, Properties, Operating Statistics.

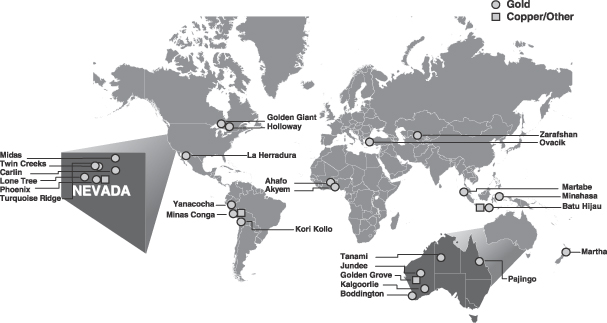

North America

Nevada.

Newmont has been mining gold in Nevada

since 1965. Newmont’s Nevada operations include Carlin, located west of the city of Elko on the geologic feature known as the Carlin Trend, the Twin Creeks mine approximately 15 miles north of Golconda, the Lone Tree Complex near the town of

Valmy, and the Midas mine near the town of the same name. Newmont also participates in the Turquoise Ridge joint venture with Placer

Dome, which utilizes mill capacity at Twin Creeks. The Phoenix gold/copper project located 10 miles south of Battle Mountain, is under construction with

production expected in mid-2006.

Gold sales from

Newmont’s Nevada operations totaled approximately 2.4 million equity ounces for 2004. Ore was mined from 13 open pit mines and four underground mines in 2004. In 2005, initial production will commence at Leeville on the Carlin Trend, the first

shaft accessed mine constructed by Newmont in Nevada. Ore production is expected to begin in late 2005 with an annual production rate of 450,000 to 500,000 ounces. At Phoenix, construction commenced in 2004 for this gold/copper project. Upon

completion in mid-2006, 370,000 to 420,000 ounces of gold and 16 to 40 million pounds of copper will be produced annually.

At year-end 2004, Newmont reported 34 million equity ounces of gold reserves in Nevada. These reserves are distributed 80% at open pit mines and 20% in

underground mines. Process methods assumed over the reserve base are 74% refractory and 26% oxide. Refractory ores require more complex, higher cost processing methods. Refractory ore treatment facilities generated 66% of Nevada’s gold

production in 2004, compared with 71% in 2003, and 66% in 2002. In 2005, the percentage of production from refractory treatment facilities is expected to be approximately 67%. Thereafter, the percentage of production from refractory ores is expected

to range between 69%–75%.

Newmont’s Nevada

operations produce gold from a variety of ore types requiring different processing techniques depending on economic and metallurgical characteristics. To schedule the best use of processing capacity, the Company uses a linear programming model to

guide the flow of both mining sequence selection and routing of ore streams to various plants. Higher-grade oxide ores are processed by conventional milling and cyanide leaching at Carlin (Mill 5), Twin Creeks (Juniper) and Lone Tree. Lower-grade

material with suitable cyanide solubility is treated on heap leach pads at Carlin, Twin Creeks and Lone Tree. Higher-grade refractory ores are processed through either a roaster at Carlin (Mill 6) or through autoclaves at Twin Creeks (Sage) and Lone

Tree. Lower-grade refractory ores are processed by a flotation plant at Lone Tree and either bio-oxidation/flotation or direct flotation at Mill 5. Ore from the Midas mine is processed by conventional milling and Merrill-Crowe zinc precipitation.

Activated carbon from the various leaching circuits is treated to produce gold ore at Carlin and Twin Creeks. Zinc precipitate at Midas is refined on-site.

Newmont owns, or controls through long-term mining leases and unpatented mining claims, all of the minerals and surface area within the boundaries of the

present Nevada mining operations (except for Turquoise Ridge and Getchell described below). The long-term leases extend for at least the anticipated mine life of those deposits. With respect to a significant portion of the Gold Quarry mine at

Carlin, Newmont owns a 10% undivided interest in the mineral rights and leases the remaining 90%, on which Newmont pays a royalty equivalent to 18% of the mineral production. The remainder of the Gold Quarry mineral rights are wholly-owned or

controlled by Newmont, in some cases subject to additional royalties. With respect to certain smaller deposits in the Winnemucca Region, Newmont is obligated to pay royalties on production to third parties that vary from 2% to 5% of production.

Newmont has a 25% interest in a joint venture with a

subsidiary of Placer Dome Inc. to operate the Turquoise Ridge and Getchell mines. Newmont has an agreement to provide up to 2,000 tons per day of milling capacity at Newmont’s Twin Creeks facility to the joint venture. Placer Dome is the

operator of the joint venture for mining and ore delivery to process. Gold sales of 40,700 ounces were attributed to Newmont in 2004, based on its 25% ownership interest.

Newmont has an ore sale agreement with Barrick Goldstrike Mines to provide feed to the facilities operated by Barrick on the

Carlin Trend. The agreement provides for the sale of whole ore to Barrick. Newmont recognizes attributed gold sales net of the sale price, resulting in gold sales of 28,200 ounces in 2004.

Canada.

Newmont’s Canadian operations

include two underground mines. The Golden Giant mine (100% owned) is located approximately 25 miles (40 kilometers) east of Marathon in Ontario, Canada, and has been in production since 1985. The Holloway mine is located approximately 35 miles (56

kilometers) east of Matheson

in Ontario, and about 400 miles (644 kilometers) northeast of Golden Giant, and has been in production since 1996. The Holloway mine is owned by a joint

venture in which Newmont has an 84.65% interest. The remaining 15.35% interest is held by Teddy Bear Valley Mines. In 2004, the Golden Giant mine sold 160,000 equity ounces of gold, and the Holloway mine sold 67,400 equity ounces of gold.

Mexico.

Newmont has a 44%

interest in the La Herradura mine, which is located in Mexico’s Sonora desert. La Herradura is operated by Industriales Peñoles. The mine is an open pit operation with run-of-mine heap leach recovery. La Herradura sold 68,800 equity

ounces of gold in 2004.

South America

Peru.

The properties of

Minera Yanacocha S.R.L. (“Yanacocha”) are located approximately 375 miles (604 kilometers) north of Lima and 30 miles (48 kilometers) north of the city of Cajamarca. Yanacocha began production in 1993. Newmont holds a 51.35% interest in

Yanacocha. The remaining interests are held by Compañia de Minas Buenaventura, S.A.A. (43.65%) and the International Finance Corporation (5%).

Yanacocha has mining rights with respect to a large land position. Yanacocha’s mining rights were acquired through assignments of concessions granted

by the Peruvian government to a related entity. These mining concessions provide for both the right to explore and exploit. However, Yanacocha must first obtain the respective exploration and exploitation permits, which are generally granted in due

course. Yanacocha may retain mining concessions indefinitely by paying annual fees and, during exploitation, complying with production obligations or paying assessed fines. Mining concessions are freely assignable or transferable. In 2000, Newmont

and Buenaventura consolidated their land holdings in northern Peru, folding them into Yanacocha. The consolidation increased Yanacocha’s land position from 100 to 535 square miles.

The Yanacocha operations contain the Minas Conga deposit, for which a feasibility study was completed in 2004. Yanacocha

added 8.7 million ounces of gold (4.5 million equity ounces) and 2.2 billion pounds of copper (1.1 million equity pounds) to proven and probable reserves at Minas Conga in 2004.

Yanacocha has five separate open pit mines, Carachugo, San José, Maqui Maqui, Cerro Yanacocha and La Quinua.

Reclamation and/or backfilling activities in the mining areas of Carachugo, San José and Maqui Maqui are currently underway. Cerro Yanacocha and La Quinua are still active pits. In addition, Yanacocha has four leach pads and three processing

facilities. Yanacocha’s gold sales for 2004 totaled 3.04 million ounces (1.56 million equity ounces).

Cerro Quilish is one of the ore deposits within the Yanacocha complex. In July 2004, Yanacocha received a drilling permit for the Cerro Quilish deposit

and commenced drilling activities to further define the deposit. During September 2004, individuals from the Cajamarca region conducted a sustained blockade of the road between the City of Cajamarca and the mine site, in protest of these exploration

activities. Yanacocha suspended all drilling activities at Cerro Quilish and the blockade was resolved. At the request of Yanacocha, the Cerro Quilish drilling permit was revoked in November 2004. Yanacocha has reassessed the challenges involved in

obtaining required permits for Cerro Quilish primarily related to increased community concerns. Based upon this reassessment, Yanacocha has reclassified 3.9 million ounces (1.98 million equity ounces) of gold from proven and probable reserves to

mineralized material not in reserves as of December 31, 2004.

Bolivia.

The Kori Kollo open pit mine is on a high plain in northwestern Bolivia near Oruro, on government mining concessions issued to a Bolivian corporation, Empresa Minera Inti Raymi S.A.

(“Inti Raymi”), in which Newmont has an 88% interest. The remaining 12% is owned by Mrs. Beatriz Rocabado. Inti Raymi owns and operates the mine. In 2004, the mine sold 21,700 equity ounces of gold. Mining was completed and the mill

closed in October 2003. Production has continued from residual leaching. Inti Raymi will begin processing oxide ores on leach pads from the Kori Chaca pit and reprocessing high-grade tailings on a new leach pad in 2005.

Prior to the acquisition of Normandy, Newmont owned a 50% interest in the Pajingo mine. The remaining 50% interest in

Pajingo, and all other Australian and New Zealand properties described in this report, were acquired as part of the acquisition of Normandy in February 2002.

In Australia, mineral exploration and mining titles are granted by the individual states or territories. Mineral titles may also be subject to native

title legislation. In 1992, the High Court of Australia held that Aboriginal people who have maintained a continuing connection with their land according to their traditions and customs may hold certain rights in respect of the land, such rights

commonly referred to as native title. Since the High Court’s decision, Australia has passed legislation providing for the protection of native title and established procedures for Aboriginal people to claim these rights. The fact that native

title is claimed with respect to an area, however, does not necessarily mean that native title exists, and disputes may be resolved by the courts.

Generally, under native title legislation, all mining titles granted before January 1, 1994 are valid. Titles granted between January 1, 1994 and December

23, 1996, however, may be subject to invalidation if they were not obtained in compliance with applicable legislative procedures, though subsequent legislation has validated some of these titles. After December 23, 1996, mining titles over areas

where native title is claimed to exist became subject to legislative processes that generally give native title claimants the “right to negotiate” with the title applicant for compensation and other conditions. Native title holders do not

have a veto over the granting of mining titles, but if agreement cannot be reached, the matter can be referred to the National Native Title Tribunal for decision.

Newmont does not expect that native title claims will have a material adverse effect on any of its operations in Australia.

The High Court of Australia determined in an August 2002 decision, which refined and narrowed the scope of native title, that native title does not subsist in minerals in Western Australia and that the rights granted under a mining title would, to

the extent inconsistent with asserted native title rights, operate to extinguish those native title rights. Generally, native title is only an issue for Newmont with respect to obtaining new mineral titles or moving from one form of title to

another, for example, from an exploration title to a mining title. In these cases, the requirements for negotiation and the possibility of paying compensation may result in delay and increased costs for mining in the affected areas. Similarly, the

process of conducting Aboriginal heritage surveys to identify and locate areas or sites of Aboriginal cultural significance can result in additional costs and delay in gaining access to land for exploration and mining-related activities.

In Australia, various ad valorem royalties are paid to state and

territorial governments, typically based on a percentage of gross revenues.

Pajingo.

The Pajingo mine is an underground mine located approximately 93 miles (150 kilometers) southwest of Townsville, Queensland and 45 miles (72 kilometers) south of the local

township of Charters Towers. Prior to the Normandy acquisition, Newmont owned a 50% interest in Pajingo. Following the Normandy acquisition, Newmont owns 100% of Pajingo. In 2004, Pajingo sold 251,400 equity ounces of gold.

Yandal.

In 2004, the Yandal operations

consisted of the Bronzewing and Jundee mines situated approximately 435 miles (700 kilometers) northeast of Perth in Western Australia. The operations sold 379,300 equity ounces of gold in 2004. Newmont owns a 100% interest in Newmont Yandal